Chapter 78 Emerging Legal Issues in Banking Operations

Kemale Aslanova

Beykent University, Turkey

ABSTRACT

This chapter deals with legal issues in banking activities, which have gained interest during the past decade. It determines the place of legal issues related to banking activities, such as consumer loans, credit cards, and electronic banking, which all have gained even more importance after the last global financial crisis.

The chapter focuses on the comparative analysis of current legal issues in Turkey and in the European Union and the legal issues related to risks in the sphere of electronic banking and suggests potential strategies.Introduction

While the development of electronic transaction in banking activities can offer a variety of benefits to society, there are multiple legal issues and security risks presented by this development. This work discusses several legal issues and risks in the banking activities.

The observation addresses three major issues. The first relates to the legislation which governs the banking activities. Particular emphasis is given to examining legislation in Turkey and comparison with the existing EU legislation. The second issue relates to the analysis of the benefits of electronic banking presented by the development of electronic technology. The third major issue of concern stems from the first and second: risks of electronic banking and possible legislative security issues.

The first section describes the legislation on the banking activities in Turkey. The analysis of the different types of banking activities is also given in the first section. The analysis of the legal banking issues in Turkey is given in the second section. The differences and similarities between the issues in European Union and Turkish Law are given in third section. The benefits of electronic banking, risks and further legal issues are analyzed in the fourth section, with a special emphasis on the development of electronic transactions.

DOI: 10.4018/978-1-4666-6268-1.ch078

.

BANKING ACTIVITIES

The Article 4 of the Turkish Banking Law No.

5411 has defined the activities which the banks can engage in. Based on this article, there are several activities and limitations for engaging in these activities. According to this article (Turkish Banking Law No. 5411):Without prejudice to the provisions of other laws, banks may carry out the following activities:

1. Accepting deposits.

2. Accepting participation funds.

3. Granting any sort of loan, either cash or non-cash.

4. Carrying out any type of payment and collection transactions, including cash and deposit payment and fund transfer transactions, correspondent bank transactions, or use of check accounts.

5. Purchasing transactions of commercial bills.

6. Safe-keeping services.

7. Issuing payment instruments such as credit cards, bank cards and travel checks, and executing relevant activities.

8. Carrying out foreign exchange transactions, trading of money market instruments, trading of precious metals and stones and safekeeping such.

9. Trading and intermediation of forward, future and option contracts, simple or complex financial instruments which involve multiple derivative instruments, based on economic and financial indicators, capital market instruments, goods, precious metals and foreign exchange.

10. Purchase and sale of capital market instruments and repurchasing or re-sale commitments.

11. Intermediation for issuance or public offering of capital market instruments.

12. Transactions for trading previously issued capital market instruments for intermediation purposes.

13. Guarantee transactions like undertaking guarantees and other liabilities in favor of other persons.

14. Investment counseling services.

15. Portfolio operation and management.

16. Primary market dealing for purchase-sales transactions within the framework of liabilities assumed by contracts signed with Treasury Undersecretariat and/or Central Bank and associations of institutions.

17. Factoring and forfeiting transactions.

18. Intermediating fund purchase-sale transactions in the inter-bank market.

19. Financial leasing services.

20. Insurance agency and individual private pension fund services.

21. Other activities to be determined by the Board.

Deposit banks shall not be engaged in activities cited in sub-paragraphs (b) and (t); participation banks shall not be engaged in activities cited in sub-paragraph (a) and development and investment banks shall not be engaged in activities cited in sub-paragraphs (a) and (b).

In an effort to present the banking activities in detail, we formed this section by reviewing the products and services provided by banks in general and regarding the Article 4 of the B anking Law No. 5411. Regarding the products and services offered by banks, banking activities can be divided into individual, corporate, SMEs, credits, credit cards, ATM (Automated Teller Machine) cards, smart cards, investment, and instantly banking activities.

Individual banking activities can include, deposit products, investment, credit, cards, insurance, retirement, payments (invoice, tax, loan, etc.), deposit box, money transfers, checks and bonds, etc.

Corporate banking activities include, credit, project financing, structured financing, derivatives, foreign-trade financing, cash management, investment, credit, cards, and insurance.

Commercial banking activities include investment, credit, cash management, foreign-trade financing, commercial cards, and insurance. SMEs (Small and Medium Size Enterprises) banking activities include, the same but more specific products and services with commercial banking activities but more specific.

Credit banking activities can be individual, corporate, and commercial. These activities can be in the form of cash-loan or non-cash loan and may include, fast credits, micro credits, consumer credit, education credit, export credit, import credit, home loan, vehicle loan, business loan, project financing, forfeiting, guarantee letter, reference letter, etc.

There are several forms of credit cards according to the scope of the bank and the income level of the consumer (platinum, gold, etc.). Smart cards can serve for transportation applications, university applications, etc.

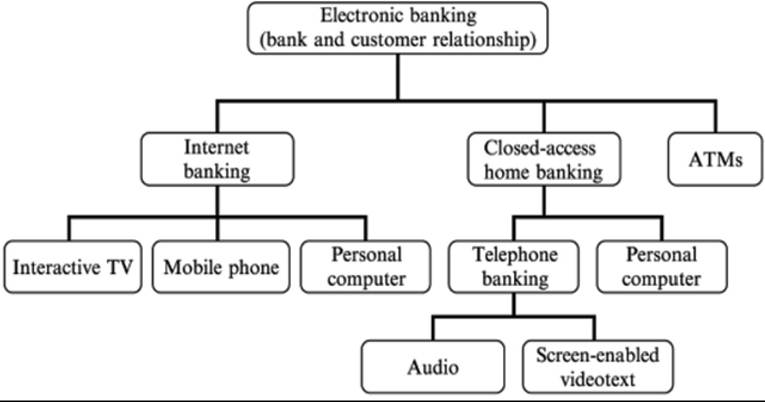

Investment activities can be in the form of investment fund, bonds, bills, stock, gold, derivatives, repo, Eurobond, etc. Banks offer different ways for customers to use electronic banking services (see Figure 1).

Instant banking activities and electronic banking activities can include, internet branch, videophone branch, telephone branch, money transfers, cash point, investment transactions Wap banking, cell phone banking, iPad applications, etc. Electronic money transfers can be in the form of EFT (money transfer to other banks), money orders (among the same accounts and/or to other recipients in the same banks and in form of Turkish Currency and/or Foreign Currency), and foreign currency transfers (by SWIFT, MoneyGram, Western Union, etc.). Electronic investment transactions can include buying and/or selling funds, FX, cross transactions, time deposit accounts, share certificate and/or gold transactions, repo and bills and bonds (Aydin, 2012).

EMERGING LEGAL BANKING ISSUES IN TURKEY

The difference of banks from the other financial institutions is their ability to decrease transactions’ costs, provided service for monitoring risks for investors, and furthermore their ability to provide fast and high amounts of liquidity. On the other hand, since the late 1970’s the world experienced several banking crisis and these crisis have spread over the world very quickly. If a banking crisis (or a financial crisis) cannot be prevented, after affecting the banking system, it carries the risk of affecting the real economy. Especially the last global financial crisis attracted the attention on liquidity while the lack of liquidity in this period caused serious worries. In the meantime, banking system almost restructured through the efforts of Bank for International Settlements and Financial Stability Board and the central banks to create a resilient banking system.

In addition to all these, there is an incredible fast increase in internet and mobile banking activities which brings a new security issues to the table. These type of activities make the legal environment for the banks very important to protect customers, macro economy and also protect banks from themselves (Barth, Gan & Nolle, 2005).Figure 1. Communication methods and access devices in electronic banking

Source: Gkoutzinis, Apostolos, Internet Banking and the Law in Europe: Regulation, Financial Integration, and Electronic Commerce, p. 8, Cambridge University Press, Cambridge, UK, 2006

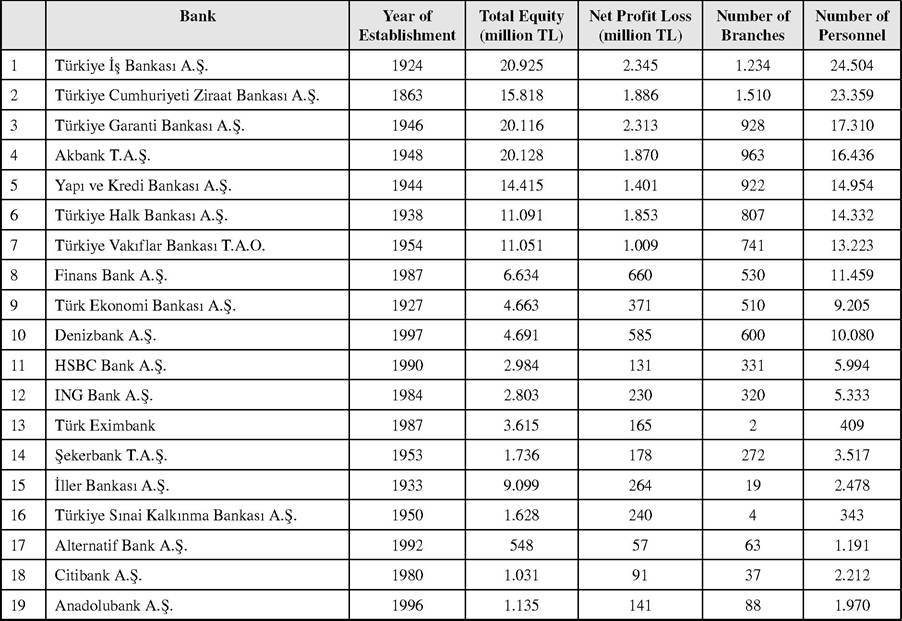

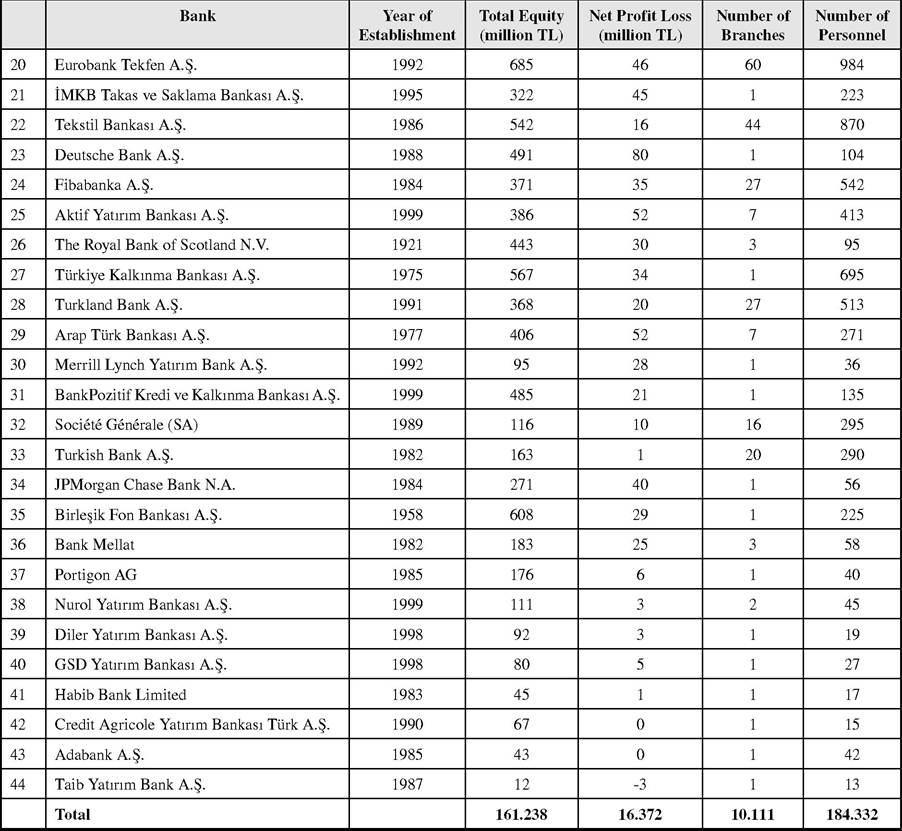

The Table 1 shows the last statistical information on banks in Turkey. As of the end of September, 2012, there are forty four active banks (Table 1).

They have 1,241,732 (million TL) assets, 10,111 branches, 184,332 personnel, and 16,372 (million TL) net profit (The Banks Association of Turkey, 2012a). 31 of these banks are deposit banks (16 of them are foreign investment banks), and 13 are development and investment banks.

21.4% of total shares of these 44 banks have been offered to public, and 55.4% ofthe rest 78.6% belong to investors who are resident in Turkey

Table 1. Banks in Turkey as of end of September 30, 2012

continued on following page

Table 1. Continued

Source: The Banks Association of Turkey, Statistical Reports, Banks According to Their Assets, http://www.tbb.org.tr/tr/banka-ve-sektor- bilgileri∕istatistiki-raporlar∕eylul--2012—aktif-buyukluklerine-gore-banka-siralamasi/1211

and 23.1% belong to foreign investors (The Banks Association of Turkey, 2012b).

One of our legal banking issues (banks exempt from fees) is the legal fees (Banking Law No.

5411 Article 140 and Provisional Article 13; Law No. 492 on Fees). There have been legal justification and the text contradictions between decisions of Supreme Courts’ Special Panel departments and the Assembly of Civil Chambers. Finally the issue has been accepted by the Assembly of Civil Chambers' number 2010/12-443-471 decision. Secondly, Check Law No 5941 has brought many issues, which requires further and detailed discussion (Sanli, 2011).An important discussion on the subject contractual interest and default interest rates continues today. As of 1 July, 2012 The New Turkish Commercial Code No. 6102 (New TCC) has come into effect with the amendments-with the Law No. 6335 Amending the Turkish Commercial Code and Law on Effectiveness and Implementation Form of the Turkish Commercial Code-to the law even before it has come into effect. Article 3 addresses interest rate issue (same as it was in old Commercial Code) and accordingly interest rate is designated freely in commercial affairs. The upper limits of the contractual interest and default interest rates are defined in the Turkish Obligations Code No. 6098 which are in favor of the consumers who use credit cards and consumer credits. On the other hand, there is opinion this is an unfair intervention by the authorities while they should also protect the freedom of contract and freedom of initiative (Demir, 2012; Reisoglu, 2012).

Other issues can be summarized as follows (the limitations of scope do not allow us to further review all of these issues in this study):

• Commercial enterprise pledge.

• Preliminary attachment application on collection of bank receivables.

• Solidarity in terms of deposit accounts.

• The status of deposit of deceased in terms of heirs.

• Cost of filing in credit applications.

• Credit card annual fee.

• Postponement of bankruptcy applications.

• Liquid receivables regarding the execution of indemnity for denial concept.

• Surety in consumer law.

• Electronic banking regulations.

EMERGING LEGAL BANKING ISSUES IN EUROPE

Regarding the existence of 27 member countries, EU legal systems, banking systems and the existence of Union, its regulations and its complex structure, there are several legal issues related to banking activities. However, three of these legal issues have gain more importance nowadays: lack of consumer protection in credit markets, lack of regulations regarding the over-indebtedness or insolvency, and lack of regulation in electronic banking.

In the EU law, one of the important issues is the lack of consumer protection in credit markets. Although, there are several regulations regarding the credits, such as the Consumer Credit Directive and the Markets in Financial Instruments Directive, the EU consumers’ lack of financial literacy is an emerging issue in the EU law. Especially, low-income and low-educated groups are not protected by law in a sufficient manner. The law needs to be updated at least to protect vulnerable groups and consumers from entering into too risky agreements. Banks should be held responsible, and it should include warn for the banks (Mak & Braspenning, 2012).

Another important issue is the lack of regulations regarding the over-indebtedness or insolvency. There are Consumer Credit directives of 1978 and 2009 but neither of them has addressed this issue, nor the other European Union law instrument. Just the Council of Europe Recommendation of 2007 addresses the issue but it is not sufficient in solving the emerging issues. Furthermore, same links between the Union countries increases the risks. The bridge between Denmark and Sweden (2000) could be useful to explain this risk. This bridge created increased relationships between Copenhagen (Denmark) area and the Malmo (Sweden). The over-indebtedness or insolvency issues reflected these areas as several debtors living in the one side, but are debtors in the both sides and filings of these individuals for personal insolvency in either country created serious legal issues. Therefore, there is a need for the member countries to recognize debt adjustment judgments made in another member countries and regulations in this field (Niemi, 2012).

Another emerging legal issue is related to electronic banking. The legal infrastructure of the electronic banking activities in Europe is an adjunction of the “law of contracts, the law-of the banker customer relationships, the law governing distinct banking contracts and services, and in civilian codifications.” Furthermore, in order to protect consumers, investors, and depositors, and maintain the transparency, fairness and disclosure there are special statutes, secondary statutory instruments and regulations (Gkoutzini, 2006). However, there is still lack of regulation in this subject. There are issues regarding the deposit protection and liability of supervisors (e.g. community deposit protection regime’s scope, purpose, and validity) (Dempegiotis, 2008). For instance, in United Kingdom (UK), government agents can charge companies with fines if they cannot protect customers but companies are not obligated to notify customers about the issues related to security breaches. Because of the lack of regulation in this issue, in 2011, 14,000 customers’ credit card details were stolen by the online hackers from one company (Booth, 2011).

ELECTRONIC BANKING

Benefits of Electronic Banking

Both individuals and business entities use internet and mobile applications to increase their efficiency to gain time and to attract and reach customers in a wider and faster way in case of business entities. These demands changed the way of working, business activities and banking. Banking system not only provides products and services through internet and mobile applications but also is able to reach very personal individual and corporate customer information, and make use of these information systems in order to maintain their activities. Therefore securing their information systems is becoming more important every day and both, legislators need to catch the speed of technology and banks should act in a more responsible manner.

In Turkey, number of registered total (retail and commercial) customers (in thousands) of internet banking who logged in at least once was 21,288 in March 2012 whereas it was 17,950 in the same period of 2011. The number of mobile registered total (retail and commercial) customers who logged in at least once was 1,444,835 in March 2012 whereas it was 912,788 in the same period of 2011 (The Banks Association of Turkey, 2012), see Tables 2, 3, and 4 for more detail.

There are several parties (operators, banks, merchants and customers) in the credit card market. In Turkey, the system operator is the Interbank Card Centre (ICC) and the issuer and acquirer is the banks, while in the USA and Europe, there are two separate financial agents as the issuer and acquirer (Dilek, 2012).

Electronic banking activities in Turkey include the activities given in the earlier parts of the study including ATM, internet and mobile services. More than two third of the bank’s payments are done through internet banking in Turkey. One of the new applications is checks are coded now and banks put them through electronic clearing which minimized the time in the billing process (Aydin, 2012).

This rapid increase in the use of internet and mobile banking services arise for several reasons: a customer (individual and/or corporate) can use these services at any time which means not being dependable on 9 to 5 banking schedule which is a more convenient system, at anywhere without waiting anyone in line, with instant reach to the service, no geographic limits. That’s electronic banking offers mobility, thus saving time and energy; and reaching and following financial information instantly (Lawrence, 2008). Another important benefit is saving money (e.g. lower fees) through electronic banking activities. For instance Europe applies lower fees for electronic banking activities from north to south and from rich to poor (Koskokas, 2011a).

Table 2. Internet banking statistics for Turkey: Number of customers using Internet banking services

| March 2011 (thousand) | December 2011 (thousand) | March 2012 (thousand) | |

| Number of Retail Customers | |||

| Active (A): That logged in at least once in the related three-month period | 6,505 | 7,803 | 8,485 |

| Registered (B): That logged in at least once | 16,253 | 18,106 | 19,322 |

| Registered (C): That logged in at least once in one-year period | 8,498 | 10,389 | 11,304 |

| Active(A)ZrRegistered (B) | 40% | 43% | 44% |

| Number of Commercial Customers | |||

| Active (A): That logged in at least once in the related three-month period | 723 | 803 | 844 |

| Registered (B): That logged in at least once | 1,697 | 1,892 | 1,966 |

| Registered (C): That logged in at least once in one-year period | 860 | 968 | 1,009 |

| Active(A)/Registered (B) | 43% | 42% | 43% |

| Number of Total Customers | |||

| Active (A): That logged in at least once in the related three-month period | 7,227 | 8,606 | 9,329 |

| Registered (B): That logged in at least once | 17,950 | 19,998 | 21,288 |

| Registered (C): That logged in at least once in one-year period | 9,358 | 11,358 | 12,313 |

| Active(A)/Registered (B) | 40% | 43% | 44% |

Source: The Banks Association of Turkey, Internet and Mobile Banking Statistics March 2012, Report Code: DE22, April 2012.

Table 3. Internet banking statistics for Turkey: Investment transactions

| December 2011 | March 2012 | Net Change | March 2012 | ||||

| Number of Transactions (thousand) | Volume of Transactions (million TRY) | Number of Transactions (thousand) | bgcolor=white>Volume of Transactions Number of Transactions (thousand) | Volume of Transactions (million TRY) | Average Volume of Transactions (million TRY) | ||

| Investment Funds | 2,483 | 21,002 | 2,333 | 18,886 | -150 | -2,116 | 8.1 |

| Foreign Currency Transactions | 2,382 | 24,169 | 2,364 | 18,695 | -18 | -5,474 | 7.9 |

| Time Deposit Accounts | 591 | 14,908 | 650 | 14,540 | 59 | -368 | 22.4 |

| Realized Share Certificate | 4,957 | 17,686 | 5,289 | 20,285 | 665 | 5,600 | 3.8 |

| Repurchasing Agreements | 116 | 4,234 | 108 | 3,496 | -8 | -737 | 32.5 |

| Bonds and Bills | 95 | 1,235 | 101 | 1,099 | 6 | -136 | 10.9 |

| Gold Transactions | 478 | 2,769 | 442 | 1,582 | -36 | -1,187 | 3.6 |

| VOB | 330 | 3,920 | 263 | 6,957 | -67 | 3,037 | 26.5 |

| Total | 11,432 | 59,922 | 11,550 | 85,540 | 117 | -4,382 | 7.4 |

Source: The Banks Association of Turkey, Internet and Mobile Banking Statistics March 2012, Report Code: DE22, April 2012.

Table 4. Internet banking statistics for Turkey: Financial transactions

| March 2011 | December 2011 | March 2012 | ||||

| Number of Transactions (thousand) | Volume of Transactions (million TRY) | Number of Transactions (thousand) | Volume of Transactions (million TRY) | Number of Transactions (thousand) | Volume of Transactions (million TRY) | |

| Money Transfers | 39,877 | 230,080 | 46,424 | 277,861 | 48,238 | 275,048 |

| Payments | 28,588 | 11,494 | 33,258 | 14,203 | 34,305 | 13,641 |

| Credit Card Transactions | 8,160 | 6,373 | 9,057 | 7,978 | 9,505 | 8,293 |

| Other Transactions | 1,823 | 21,228 | 1,709 | 21,908 | 2,201 | 24,042 |

| Total | 78,448 | 269,175 | 90,448 | 321,949 | 94,249 | 321,023 |

Source: The Banks Association of Turkey, Internet and Mobile Banking Statistics March 2012, Report Code: DE22, April 2012.

Risks of Electronic Banking

It is a serious challenge for the legislators to catch the speed of technology and make regulations simultaneously. This challenge results in insufficient protection for consumers by governing bodies and customers do not have control and monitor power over the activities of banks. Also, both internet and mobile banking activities require significant security applications which should be offered by the banks.

The lack of this assistance would result in frauds, information theft, identity theft, not being able to reach the personal account, and improper transfers in accounts. The main technology issues related to internet banking are: security, privacy (anonymity); authentication (difficulty to ensure that encrypted transactions cannot be changed in the final stage), and divisibility (the issue of being able to divide electronic fund just like the real money, such as into different units of currency). Banks offer several security features for their customers in an effort to decrease these risks such as ‘ security token devices’ which can be in the form of PIN (login password)∕TAN (one time password), signature based electronic banking (digitally and encrypted signing transactions); ‘Attacks’ which are designed to deceive the user in steeling login data and valid TAN; and ‘countermeasures’ such as digital certificates against information theft or manipulation of transactions (Koskokas, 2011b).

From a legal point of view, the contract between the bank and customer allows the information transmission from customer to bank and from bank to customer leading to establishment, change, exercise, or discontinuance of liabilities and legal rights. Therefore, these processes could result in legal issues for both parties which require clear and detailed regulations in this field (Weber, 2010).

In order to regulate the electronic banking environment several international standards have been set. Banks have to adopt most of these standards in order to provide the security in their IT systems for the resilience and standardization of the banking system, for the security of their customers, and to prevent fraudulent activities:

• Banking for International Settlements (BIS): “Management and Supervision of Cross Border Electronic B anking Activities” (2003)

• BIS: “Risk Management Principles for Electronic Banking” (2001)

• Information Systems Audit and Control Association (ISACA): “COBIT 4” and “COBIT 5” (information and technology governance framework)

• International Organization for Standardization (ISO): “ISO/IEC 27002:2005 (for information security management)

• The Committee of Sponsoring

Organizations (COSO): “Enterprise Risk Management-ERM-Framework”

• Corporate Governance Codes (regulated by laws-such as New TCC the sub-clause C of Article 375 and Article 336 and-regard- ing the banking activities-regulation and supervision agencies-such as Regulation on Corporate Governance Principles by Banking Regulation and Supervision Agency) (Kondabagil, 2007).

RESULT

The last global financial crisis presented that an unsupervised banking system with lack of regulations, consumers’ lack of knowledge regarding the banking activities, and uncontrolled and unanalyzed credits given by the banks could result in serious lack of liquidity which would also affect the real economy. After the crisis and with the influence of recession, bankruptcies, shrinking demand, increasing unemployment rates, emerging legal issues regarding the credits and credit cards draw attention to the complex products of banks, credit quality and the need for regulations to protect consumers in this field. Another important and related issue is the rapidly emerging technologic structure of the banking activities.

In this field BIS plays an important role whereas it has the power of making regulations for the banking system globally. But these regulations should be further supported with the legislations in countries. Legal frameworks should catch the speed of electronic banking in order to protect consumer, banking system, and transparency, and bank’s responsibility in this field should be defined clearly and sanctions should be deterrent (Weber, 2010).

The risks inherent to electronic banking activities should be defined clearly and updated and measures should be regulated by the banking regulatory and supervisory agencies. These agencies supervision frequency and technology should be improved. First of all, the legislation related to electronic banking should consider bank and consumer relations while it is very loose because of the complex and changing structure of the electronic activities.

Banks should be more responsible while providing their products and services, in the customer information process regarding the banking activities, secure their IT systems, update them according to the emerging technologies and test all their electronic activities before applying them.

REFERENCES

Aydin, H. (2012). Finans ve bankacilikta sonraki adim konferansi. Bilisim Zirvesi, 2, 1-3.

Banks Association of Turkey. (2012a). Internet and mobile banking statistics. Retrieved from www.tbb.org.tr

Banks Association of Turkey. (2012b). Statistical reports, bank and branch statistics. Turkish Banking Law No. 5411.

Barth, R. J., Gan, J., & Nolle, E. D. (2005). Global banking regulation and supervision: What are the issues and what are the practices. In E. Klein (Ed.), Global Banking Issues. New York: Nova Science Publishers Inc.

Booth, L. (2011). Getting hacked off. London: Post.

Demir, S. (2012). Turk borclar kanunu’nun para borclarinda faize iliskin getirdigi yenilik ve sinir- lamalar. Ankara Barosu Dergisi, 70, 207-234.

Dempegiotis, S. I. (2008). The hard-to-drive tandem of immunity and liability of supervisory authorities: Legal framework and corresponding legal issues. Journal of Banking Regulation, 9(2), 131-149. doi:10.1057/jbr.2008.5

Dilek, S. (2012). On-us transactions in credit card market in Turkey and rational banks. International Research Journal of Finance and Economics, 131(96), 128-143.

Gkoutzinis, A. (2006). Internet banking and the law in Europe: Regulation, financial integration and electronic commerce. Cambridge, UK: Cambridge University Press. doi:10.1017/ CBO9780511494703

Kondabagil, J. (2007). Risk management in electronic banking: Concepts and best practices. Singapore: John Wiley & Sons (Asia) Pte. Ltd.

Koskokas, I. (2011). The pros and cons of internet banking: A short review. Business Excellence and Management, 1(1), 49-58.

Lawrence, J. (2008). The budget kit: The common cents money management workbook (5th ed.). New York: Kaplan Publishing.

Mak, V., & Braspenning, J. (2012). Errare huma- num est: Financial literacy in European consumer credit law. Journal of Consumer Policy, 35(3), 307-332. doi:10.1007/s10603-012-9198-5

Niemi, J. (2012). Consumer Insolvency in the European legal context. Journal of Consumer Policy, 35, 443-459. doi:10.1007/s10603-012-9215-8

Reisoglu, S. (2012). Turk borclar kanunu’n yurulugu ve uygulama sekli hakkinda kanunun bankacilik islemleri acisindan degerlendirilmesi. Istanbul, Turkey.

Sanli, E. (2011). Opening statement at the emerging legal issues in banking activities meeting. Bankacilar Dergisi, 76, 19-20.

Weber, H. R. (2010). Legal issues in mobile banking. Journal of Banking Regulation, 11(2), 129-145. doi:10.1057/jbr.2009.16

This work was previously published in Global Strategies in Banking and Finance, edited by Hasan Dincer and Umit Hacioglu, pages 358-368, copyright 2014 by Business Science Reference (an imprint of IGI Global).