Chapter 79 A New Macroeconomic Architecture for the Stock Market: A General-System and Cybernetic Approach

Masudul Alam Choudhury

College of Commerce and Economics, Sultan Qaboos University, Oman

ABSTRACT

The old idea of segmented macroeconomics of the financial sector competing with the real economy is replaced by a new model, which manifests strong interaction, integration and co-evolution by circular causation relations between the monetary sector and the real economy with the bridging function of finance and financial instruments.

The Money, Finance, Spending and Real Economy (MFSRE) model emerges. This model formalizes the new architecture for the macroeconomy, and its relationship to the stock market. In this model relating to a reconstructed state of the economy and the emergent structure of the financial architecture, money and spending are treated as complementary elements of growth and development. The overarching structure in the end is the MFSRE with its extensively complementary inter-variables relationship in a general system and cybernetic form of interrelationships. The economic organization of the MFSRE causes price stabilization and economic growth and development. These are signified in the social wellbeing criterion of the good economy. The stock market, exemplified by the empirical case study of Bangladesh’s state of the economy and the Dhaka Stock Exchange, bring out the true example of the macroeconomic analysis. The new financial architecture with its stabilization, sustainability and growth and wellbeing as basic-needs regime of development is contrasted with old macroeconomic belief and policies based on outmoded macroeconomic beliefs and futures.DOI: 10.4018∕978-1-4666-6268-1.ch079

.

INTRODUCTION

Stock market turnover rates, yields, yield rates, and stability are indicators of the health of the economy for those countries that depend upon such a financial institution. But it is not such an important support system for an economy that does not have stock market, and does not need one.

Instead they depend upon real asset pricing mechanism for measuring the economic and social standards. The stock market is then not an essential institution to act as a barometer of economic change. But these two opposite views tell a much larger story about the economic processes and their social effects. Meera (2004, p. 59) puts the emptiness of the casino barometer of a stock market and its underlying financial system in value formation in the following words: “Financial institutions create money out of nothing but lend it out of interest. This characteristic of fiat money called seigniorage is at the root of financial crisis, monetary instability, and unjustness. The fractional reserve requirement also makes possible the creation of additional money through multiple deposit creation. All this has brought about huge volumes of liquidity in the global monetary system, which is responsible for the huge asset price bubbles faced in many countries.”To investigate into these opposite views regarding the financial system with or without stock market we note what lies behind stock market in the organization of asset valuation to protect the wealth of savers and to contribute to and reinforce the relationship that money and finance has with the real economy. Furthermore, stock market stability also requires inflation targeting and a participatory form of development model for the protection and wellbeing of the marginal savers. The ethical principle here linked with the economic objective is derived from Rawls’ Difference Principle (1971) as an example. On the point of national wellbeing Rawls wrote (op cit, p. 14-15):“... inequalities ofwealth and authority are just only if they result in compensating benefit for everyone, and in particular for the least advantaged members of society.” The moral theme underlying the Difference Principle is equally applicable to the purpose of financial stability and social and economic measurement of wealth. The question then stands whether stock markets can deliver such a concept of wellbeing.

Likewise, we need to ask whether there is an alternative economic and socially productive activity that establishes the total wellbeing criterion for the nation.And on this objective issue the structural changes linked with stock market and alternative financial institutions also invoke the nature of participatory role between central bank and commercial bank on the matter of money, finance and real economy complementary relationships. On this issue Mishkin (2007a, p. 55) presents his view: “First, it (central bank) should advocate a change in its mandate to put price stability as the overriding, long-run goal of monetary policy. Second, it should advocate that the price stability goal should be made explicit.. Third, the Fed should produce an ‘Inflation Report’. that clearly explains its strategy for monetary policy and how well it has been doing in achieving its announced inflation goal.”

Furthermore, the issues of monetary relations involving central bank and commercial banks, and inflation targeting to stabilize prices also invoke the study of asset pricing mechanism for the common good on the wellbeing side. On this asset-pricing issue for inflation targeting Mishkin (2007b, p. 59) emphasizes the use of monetary policy for the stabilization of stock market fluctuations. He points out the importance of regulating the monetary policy effect on inflation targeting so that stock market effects on investment as a major form of spending (fiscal side) remains well maintained. Besides this there is need to maintain the transmission effect of stock market changes on household liquidity and household wealth.

Objective

Firstly, a combination of the above-mentioned socio-economic problems faced by the prevalent monetary, financial, and real economy relations is summarized in analyzing the causes of stock market turmoil. Next, the formalization of a new financial architecture with participatory linkages requires development and application of a revolutionary new form of model that is epistemologically premised on unity of knowledge.

From the formalism of the new financial architecture comes out the problems of economy and society discussed above. These comprise firstly, the nature of functional relations between money, finance and real economy that leads to price stabilization, economic growth, monetary and fiscal expansion with appropriate financial instruments.Secondly, there ought to be a dynamic basic- needs regime of development that can bring about, and that springs from the prescribed model of participative inter-relations between money, finance, and the real economy.

Thirdly, in the resulting kind of the sectorally unified model of inter-causal relations the issues of asset valuation, economic diversification, and central bank-commercial banking relations need to be designed. Fourthly, the social wellbeing implications of the emergent money, finance and real economy relations need to be evaluated in the midst ofthe complementary scenario of ethics and economics. In all, the emergent money, finance and real economy relationship with all the intervariable relations between them and involving the ethical, economic and financial dimensions make up a systemic order of ethico-economic integration. We will refer to such inter-causal relations with ethics embedded in that system as the endogenous effect of ethics in the systemic context. We will infer from the analytical results of the systemic model of money, finance, and real economy how stock market stabilization by alternative design can be attained. The stabilization we will be searching for will comprise the dynamic inter-variable relations with money circulations. It will be shown how a select portfolio of financial instruments can be effective in resource mobilization of the financial and physical kinds.

Finally, we will discuss how the spending goals, productivity, technological change, and economic diversification obtained through over inter-variable participation can become effectual. The policy and structural consequences of such systemic interrelations in economic stabilization will be explained.

A REVIEW OF THE LITERATURE

Mark Blaug on Monetarism (Friedman) and Fiscalism (Keynes)

The origin of financial architecture for the stock market arises from the nature and function of money and spending and then takes the course to other critical directions relating to such inter-causal relations. This topic is cast in the incisive words of Mark Blaug (1993, p. 29):”The great debate between Keynesians and monetarists over the respective potency of fiscal and monetary policy has divided the economic profession, accumulating what is by now a simply enormous literature.”

From such critical observations in the history of economic thought it is clear that financial instruments are to be appointed as ways of mobilizing financial resources into productive activity. Yet because of the relationship that arises between money and real resources by the nature of financial instruments and the institutional function of money with spending (fiscalism), the stock market acquires its specific meaning relating to such relations. If the relations implied here between money, finance and real economy along with the broader perspective of wellbeing are not proper, then instability and volatility causing loss in the wealth of shareholders and individuals disturb the stock market. The result then becomes an unwanted development in the economic system for preserving the efficiency, productivity, stability, and wellbeing that ought otherwise to be engendered by a good non-banking financial institution.

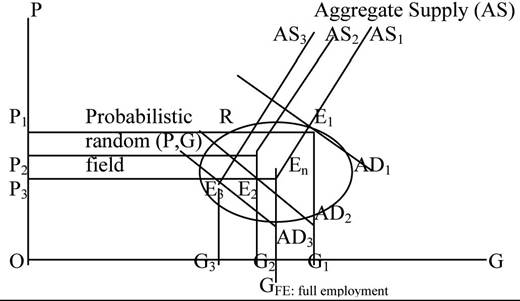

We examine this conflict between monetary and fiscal (spending) regimes and policies defying steady-state equilibrium in Figure 1. Neither Keynes nor Friedman were restful with the idea of steady-state equilibrium with learning behavior caused by interaction between choices of monetary, fiscal (spending), innovative, productive and uncertainty in a changing economic system. Such an economic system remains permanently embedded in the social order. The result is a social political economy (Holton, 1992; Parsons, 1964; Parson & Spenser, 1956).

Consequently, monetary expansion joins with fiscal (real economy spending) expansion and gets interactively causal with productivity, economic growth and prices.1 Figure 1 points out that a deflationary regime of (P,G) remains permanent in the monetarist regime, although it is denied by Keynesian in a productively expanding economy caused by spending (fiscalism). It is unknown where exactly the conflict between monetarism and fiscalism commences near to the full-employment of (P,G). There is no precise point for this. Hence the (P,G)-points becomes a random point in the probabilistic field of many such possible points defined by the intersections of Aggregate Supply (AS) and Aggregate Demand (AD) curves. Thereby, there exists a family of aggregate supply curves (monetarism) and deflated (P,G)-points shown by Ep E2,..., En, etc

In the end, the joint effects of monetarist and fiscal regimes cause perturbations, instability, volatility, and drawdown of productivity in random fields of (P,G)-points in the deflationary domain denoted by R (Choudhury, 2011, 2012).

The price level and growth of output are macroeconomic variables. However, if stock market is considered to be a key signal of economic change then a significant weight is attached to stock market prices and yields. Consequently, stock market (P,G)-values adversely affect all other (P,G)-values. Thereby the macroeconomic indicators of (P,G) are affected.

Mishkin on Stock Market Stability via Inter-Causality Between Money, Finance and Real Economy

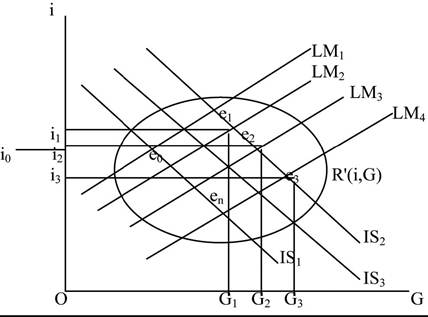

First we note the following mono-causal relationship explained by Mishkin in respect of monetary, fiscal, interest rate, and selected wellbeing variable (employment, E):

Figure 1. Deflationary effect in probabilistic random field of (P,G)-values under monetarist and fiscal expansion

[M↑inclusive of f↑]⇒[random variations (r,c)]⇒ [Deflationary effects on{(P,G) ⇒E] (1)

where, M denotes the quantity of money in circulation; f denotes the fiscal (spending) variables; r denotes real rate of interest; c denotes discount rate; and E denotes employment.

In reference to Figure 1 we note that the bracketed term, [M↑inclusive of f↑], causes volatility and instability in the random probabilistic field R, as shown and explained. Besides, the resulting randomness in (P,G)-probabilistic field also causes productivity to stall and employment to become unstable, as between short-term and long-term employment uncertainties. The principal cause of such randomness and unpredictable behavior of the economic and financial sectors is the variations between short-term and long-term real interest rates and discount rates (r,c). Such variations in r reflect upon the random relations between M and f. The predominance of the stock market on all such variables reigns as the determining factor of economic instability and financial market volatility.

Figure 2 explains the above points. Using the simple version of the macroeconomic IS-LM curve we note the transference of the random

Figure 2. Instability of (i,G)-domain with expansionary monetary and fiscal (spending regimes)

probabilistic field R from Figure 1 to Figure 2 denoted by R' that is now characterized by random equilibrium points such as e0, e1, e2,..., eι etc. The random (r,c) effects are shown to be contained in R' as the domain of (G,r,c)-points. In the 2-dimensional diagram average values of r and c are used and denoted by ‘i'.

The Contest between the Classical, Monetarist, and Fiscalist (Spending) Views of Economic Regimes

Underlying the conflicting effects on price stabilization, economic growth, productive expansion of the economy, and socioeconomic wellbeing, is the absence of complementarities between these goals, and how they can be attained in a consistent and participative way by market-polity integration. The classicists, upon who followed the new classical school, the focus of economic organization was on the market process. Consequently, monetary policy and market process formed the backbone of private sector development. An expansionary monetary policy was found to reduce the real rate of interest. A lower rate of interest ought to stimulate the economy into higher output. But our arguments given above point out that, even though real output would increase by an expansion of real monetary aggregate, this would be at the expense of increasing prices and increasing real rate of interest. Thereby, the increase in real output is adversely dampened by the j oint increases in inflation and real interest rate, the very two horns of the evil economic monster. The effects of monetary regimes on the expansion of the real economy, that is the private sector, cannot be sustained under such adverse price and interest rate effects.2

The Austrian School of Economics was the champion of the classical school of monetary phenomenon. It promoted private monetary unit, the laissez faire concept of this monetary unit as a private regulated commodity of market exchange, and the short-term as opposed to the long-run effectiveness of monetary policy in mobilizing financial resources particularly for reducing unemployment and creating employment. On this matter Hayek (1999, p. 236) wrote: “I think it is very urgent that it becomes rapidly understood that there is no justification in history of the existing position of a government monopoly of issuing money.”

Hayek’s vision of private unit of currency value is echoed by leading exponents of the Austrian Economic School. On a similar note Ludwig von Mises (1981, p. 478) wrote: “Money is the commonly used medium of exchange. It is a market phenomenon. Its sphere is that of business transacted by individual or groups of individuals within a society based on private ownership of the means of production and the division of labor.” The Austrian School as a great champion of the free market economic order promoted monetary regime over fiscal regime or spending regime including Government expenditure for the public good. According to the Austrian School voiced by von Mises (op cit p. 479), economic destabilization caused by inflationary pressure was due to the role of Government in trying to stimulate the economy with unwanted spending, when contrarily market correction should take care of the adjustment process to establish market equilibrium, and thereby, stable prices. Thus the role of spending regime by including government expenditure was not brought into a complementary relationship with monetary regime.

On this point von Mises (op cit, p. 481) wrote an important note on the market adjustment process of monetary aggregate on which the least role of Government interference, and thereby fiscal policy control, need to be exercised: “The main thing is that the government should no longer be in a position to increase the quantity of money in circulation and the amount of checkbook money - that is 100 percent - covered by deposits paid in by the public.” This appears as an important point to note on the most efficacious and non-inflationary effect of monetary regime in a market economy.

However, the fiscal role of government expenditure to drive money into the productive directions of private sector as Keynesian would have desired, is kept outside of the equation of money and spending with productive and technological change at stable prices and increasing real output. This point has remained an unresolved approach in completing the important factors of progress. These are namely, price stability, increase in real output, decline or replacement of interest rates by inflationary targeting alternative, factor productivity and elastic full-employment point, technological change, and social wellbeing as a combination of market and non-market forces, regimes and policies. All these factors together configure the total resource mobilization under dynamic conditions of socioeconomic change.

The laissez faire monetary theory is projected in the writings of Yeager (1997, p. 412-13) whose striking words in this regard are as follows: “Government would be banished from any role in the monetary system other than that of defining a unit of account or numeraire. We envisage a unit defined in a bundle of goods and services comprehensive enough for the general level of prices quoted in it to be practically steady.” Such a laissez faire conception of monetary exchange in concert with market exchange in real goods and services while an effective way of connecting money with the real economy, it puts ultimate independence of such monetary regime from government interference and governance that would otherwise come about by the presence of spending including government and private spending. The wellbeing objective and sustained economic stabilization by complementarities between the monetary regime and the fiscal (spending) regime as of markets and governments by their complementary roles is not targeted in the laissez faire conception of money and markets. Markets are upheld as the ultimate arbitrator of economic stabilization, growth and productivity generated by technological change.

From the above review of the literature one finds that monetarist approach is predominant in the development of the market process and the private sector. It should then be obvious that the spending regime should combine with the monetarist regime to accelerate the process of market freedom but within the reigns of regulation and controls when the market process becomes destabilizing. The monetarists did not believe in such possibility. Thus monetarism remained disjoint from the spending regimes including government spending, budgetary controls, taxation and resource redistribution. It is obvious that in the absence of fiscal regime to complement with money circulation no fresh productivity of factor inputs, innovation and technological advance can be generated.

Consequently, by leaving the two policies and regimes separate of each other the prospect of economic stabilization with price, real output growth, and lower interest rate remains at best a short-run case. The long-run stabilization is unattainable by the use of any of the two policies and regimes. Thereby, sustainability, which is a long- run target of economic stabilization, is not attained by the use of any of the two policies. This is an economic fact based on the scarcity of resources in the long-run that causes aggregate demand pressures to destabilize the (P,Y,r)-relationship. Also it is a political fact by virtue of the case that the opposite economic and policy perspectives govern the elected party in their short-term lives. These points are brought out by Farmer (2010). Farmer (2010, p. 19) writes on the political versus market adjustment of the non-inflationary stabilization problem: “I take the idea that a sound theory must explain how individuals behave and how their collective choices determine aggregate outcomes. From Keynesian economics, I take the idea that markets do not always work well and that sometimes capitalism needs some guidance. These ideas form a coherent new paradigm for macroeconomics in the twenty-first century.”

We argue in this paper that Governments are subjected to participatory relationship with the private sector as two sides of the same coin. These together aim at attaining economic stabilization, productivity and growth, assimilation of technological change, and bring about social wellbeing. Consequently, the economic, social and ethical goals are mutually inter-causal and thus embedded by organic relationship in the same general system of interrelations. In this way, the political agenda of control and guidance to stem the unwanted market situation is left to the assimilation of knowledge and learning in an evolutionary and civil system of public and private sector understanding through the participatory heart and mind of the social community. Such is a maturing community, whose gaze is attaining the goal that Foucault (see Dreyfus & Rabinow, 1983) referred to as a discursive society. Its totality of mature understanding in the framework of organic unity of relations is Foucault’s usage of the word Episteme.3

Mainstream Consequences of Monetary and Fiscal Regimes Concerning Wellbeing, Money, Spending, Output, Prices, Employment, and Productivity by Technological Change

We can summarize the results of our succinct review of the literature in respect of the prevailing state of relationship between monetary and fiscal regimes across the great divide for the attainment of socioeconomic wellbeing by way of economic stabilization, economic growth, and technological change with productivity. We define this comprehensive objective function as a wellbeing criterion denoted by W(.) as follows:

W = W(y,p,M,F,r,ρ,θ) (2)

where Y denotes real output; p denotes the price level; M denotes the quantity of money; F denotes spending; r denotes the real rate of interest; ρ denotes productivity of factors; and θ denotes technological change.

dW∕dθ = [(∂W∕∂y),(dy∕dθ)]+ + [(∂W∕∂p).(dp∕ dθ)]± + [(∂W∕∂M).(dM∕dθ)]± + [(∂W∕∂F).(dF∕ dθ)]± + [(∂W∕∂r).(dr∕dθ)]±+ [(∂W∕∂ρ).(dρ∕dθ)]+ + (∂W∕∂θ)+ (3)

Our discussion in respect of the prevailing state of the given interrelations between variables point out that an overly dependence on monetary regime without complementarities with fiscal (spending) regime causes technology to be exogenous. Consequently, the simultaneous expansion of monetary and fiscal (spending) regimes is not considered in the light of what Myrdal (1957, 1958) referred to as circular causation relations between the variables signifying growth and development mentioned in this section. Likewise, there is a similar discussion by Young (1928) on the need for simultaneous interrelations between the variables. The same argument is launched against the prescription of fiscal (spending) regime. Consequently, as Blaug has pointed out, the monetary and fiscal (spending) regimes in macroeconomic stabilization and coordination have remain opposed to each other, in as much as also the private sector and public sector focus of monetary and spending regimes, respectively, remain opposed to each other.

The result of such dichotomous consequences in macroeconomic theory shows up in the indeterminate signs of the changes in the (p,M,F,θ)- variables by the exogenous effect of technological change. Since such exogenous technological change is positively related to factor productivities, therefore, the effects of M and F remain exogenous on factor productivities. The growth of output, and along with this the dynamics of employment, remain neutral to technological change and productivity growth in the long-run. That is, sustainability of economic stabilization, growth and policy coordination cannot be attained together.

In the end, since technological change denoted by θ remains exogenous to every variable in the category (y,p,M,F,u,ρ) in respect of price stabilization with increasing output, therefore, there cannot exist macroeconomic coordination between M and F regimes in the direction of non- inflationary economic growth. This result was brought out in Figure 1.

The Effects of Exogeneity between Monetary and Spending Regimes on the Stock Market

It was pointed out that if the stock market was assumed to play a significant role in economic growth, the stock market will assume a high weight in the average price level. Consequently, the exogenous effect of technological change on the variables causing non-sustainability of price stabilization and economic growth will also show up in the stock prices. The inability in holding on to stable prices in the field shown in Figures 1 and 2 now establishes a volatile relationship between stock prices and the variations in the real rate of interest. That is, the indeterminacy of nominal interest rate in the domain shown in Figure 2, will intensify the volatility of the stock price.4

Furthermore, as bonds and stocks represent a mirror image of the quantity of money in supply, therefore, variations in the bond and stock prices in the portfolio of financial assets cause volatility in short-term rates of interest. In the world financial markets the volatility of short-term interest-rates has been the cause of stock market volatility. Such variations in turn are the causes of intense degrees of speculation in the stock market with bonds and stocks backed mainly by financial papers. The ultimate result of such volatile movements of stock prices and short-term interest rates is a flight of capital away from the real sector to the financial sector under the force of financial speculation.

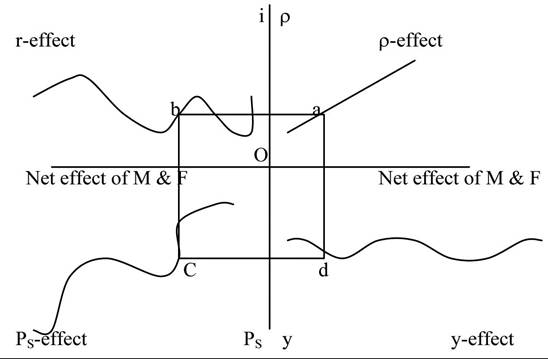

The relationship between the (y,p,M,F,i,u,ρ)- variables under the impact of exogenous technological change can be shown in Figure 3. The exogenous effect of θ on these curves will be certain shifts that remain an empirical fact. There is no exact direction of the shifts. For example, an upward shift of the y-curve could mean an upward shift of the predominant stock price curve Ps, but

Figure 3. Interrelationships between the (y,p,M,F, i,u,ρ) variables under exogenous technological change affecting productivity and net effect of monetary and spending (fiscal) regimes

a lower or higher net result on the r-curve caused by the joint effect of the monetary and spending (fiscal) curves.

Likewise, the productivity curve could shift upward along with the upward shift of r-curve due to the net effect of M and F curves on the income multiplier causing y curve to shift but at the expense of inflationary regime. The unemployment (u) effect will be similar to the y-effect at the long-run evolution of y to its full-employment level with uncertain net effect concerning M and F regimes. In the short-run the same M and F joint effect will yield an accelerated convergence towards full-employment followed by price pressure at the long-run neutrality between M and F and y along the classical version of the aggregate supply curve of output (Friedman, 1960, 1989).

On the other hand, the responses to the various variables to variations in i-variable can be shown by the following expression. The variable u will follow the same form of a random trend along with y under the net volatile effects of M and F and the y-variable and p-variable:

dW/di = [(∂W∕∂y).(dy∕di)]- + [(∂W∕∂p).(dp∕di)]± + {[(∂W∕∂M).(dM∕di)]- + [(∂W∕∂F).(dF∕di)]+}± + [(∂W∕∂i)]-+ [(∂W∕∂ρ).(dρ∕di)]- (4)

Expression (4) shows that the net random (volatility) effect of variations in i depends strongly on the variations in (dp∕di)± and {.}±. Here, by the predominating effect, p = Ps. The same kind of random effects are transmitted to the wellbeing function through the other volatility effects.

How to Stabilize the Economy from the Deleterious Effects of Stock Market Volatility with Knowledge- Induced (y,p,M,F,i,u,ρ)[θ] Variables

The principal objective and the contribution of this paper are to develop a theory of complementarities between monetary and fiscal regimes in the light of circular causal (or inter-causal) relationships between the variables mentioned here. The implications are that M-F complementarities are formed by and result in (circular causation) complementarities and endogenous interrelationships between all the variables. The exception is the replacement of interest rates and interest-bearing financial instruments by trade- related instruments. This is the meaning of the M and F complementarities that enable unified interrelationships between money (M), spending (F), finance (f), and real economy (y,p,u,ρ). We refer to the emergent model as MSFRE-model.

The emergent inter-causal relationships between all the variables in the presence of technological change and gains of productivity while replacing interest-bearing financial instruments with trade-related ones is an evolutionary learning phenomenon. Evolutionary learning is established by an epistemic view of circular causal relations in terms of systemic unity of knowledge (Maturana & Varela, 1987).

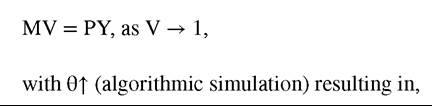

In economic terms there is an opposite movement between trade-related instruments (f) and interest rate caused by bank-savings. Bank savings cause withholding of financial resources from the real economy, while they are driven to interestbearing opposites. Contrarily, if savings are continuously converted into productive spending by way of investment and consumption, then Savings = Spending always. An amount of savings in the bank is converted continuously into spending by way of engaging the productive process and market forces. Government integrates with the market process via specific joint ventures. This relationship yields the micro-money concept and it equates to the value of spending in the perfectly market trading venue. Government becomes an agent of market catalysis.

Consequently, the following results would hold: M.V = P.Y = Spending in nominal terms of price P and real income Y. Here k = 1/V → 1 as V → 100 per cent. That is, the equivalence between money and spending (fiscalism) becomes perfect when the circulation of a quantity of money is project-specific through-out the economy. This is similar to the Austrian concept of laissez faire concept of money. But in our case, the progress towards this perfect equality is through the activity of trade replacing interest rate. That is, savings are converted continuously into spending. Banks are to mobilize savings, not to hold them back -- even for future use. That is because the withdrawal of potential savings from being mobilized causes the output to remain below the potential level.5 This is a continuous phenomenon in an economy that depends on interest rates as the basis of capital accumulation through bank savings. Keynesian idea of bank savings is based on such withdrawals from the real economy (Ventelou, 2005).

The further result is this: The necessary complementarities between the variables {y,p,M,F,f,u,ρ}[θ], mean that all these variables are positively complementary in respect of the systemic knowledge variable denoted by θ. This is an epistemological issue in unity of knowledge. In the real domain it is expressed by continuous reinforcing complementarities. Such unity of knowledge manifest by pervasive complementarities can be attained only by the action of θ on all the variables. Hence θ is of the epistemic category in unity of systemic knowledge. In fact, θ is equivalent to wellbeing, for it represents the continued cause and effect of interaction and integration forming into unity of systemic knowledge across evolutionary learning, as reconstructed interrelations proceed between the interacting and integrating variables.

The epistemic consequences are independent of time. Time is replaced by knowledge as the explanatory factor of dynamics and change. Time is treated as datum for purposes of recording the state of complementarities by endogenous forces, in which policies such as M and F and f participate.

The Generalized MSFRE Model of Unity of Knowledge

First Stage: Estimation of the Circular Causation Relations

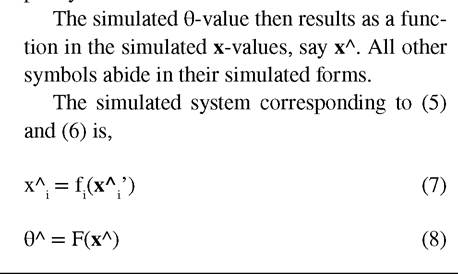

Let x denote the vector {y,p,M,F,f,u,ρ,θ}. In this every variable is induced by θ-values. Let an element x ∈ {y1 p2 M3 F4 f5 u6 ρ7 θ8} i = 128 as marked out against the variables.

Complementary (inter-) relations between the variables imply:

Xi = fi(xi'), (5)

Second Stage: Simulation of the Circular Causation Relations

The estimated coefficients of the system of Equations (5) and (6) are next simulated by giving them improved (revised) values to normatively aim for better levels of complementarities. Such selections are set by institutional discourse and policy measures.

Such estimations and simulations will continue on over new sets of time-series or cross-sectional data. As well as, algorithmically the simulations can be continued on in reiterative processes.

Third Stage: Money, Spending (Fiscalism) and Real

Economy Equivalences

Thus systemic unity of knowledge as episteme continuously simulates the circular causation relations with increasingly ranked θ-values in the case of a 100 per cent mobilization of micro-money circulation in real assets across the economy. A microeconomic (project-specific) outlook to macroeconomic aggregate of the strictly M1 (money supply) and liquidity type (money demand) is implied.

The principal hinge pin of the entire simulation by circular causation premised on unity of knowledge as the episteme underlying reiterative θ-values in complementary socio-economic intervariables relations is the replacement of interestbearing financial instruments by trade-related instruments. This in turn means the replacement of savings as financial withdrawal by banks from the real economy, by mobilization of savings into productive spending instead. Money is thereby mobilized into the real economy by using the appropriate trade-related financial instruments. The MSFRE model is now formulated by Equations (5)-(8) in continuity of evolutionary learning and/ or by continued sequences of estimation and simulation over time-series and cross-sectional data.

Thus an important contribution of this paper is also to note the empirical basis of estimating and simulating the MSFRE by circular causation relations in epistemic reference. This is to extend the theory of circular causation and cumulative causation beyond Myrdal (op cit), Young (op cit) and Kaldor (Kaldor, 1975; see Toner, 1999).

The Stock Market in the Circular Causation Theory of MSFRE

The stock market phenomenon appears as a question: Is the stock market a logically acceptable financial institution in the MSFRE model? The answer centers on the fact that the MSFRE mobilizes financial resources only into real economic activity. The financial instruments therefore, are simply endogenous mappings between the monetary and real economy via the circular causation relations between these sectors. The financial assets are now tied endogenously to real assets that are valued in financial terms and in which all forms of resources are mobilized. Financial assets lose their relevance to bank-savings in interest-bearing instruments.

In the presence of portfolios of real assets, real market exchange (trade) performs the sole function of valuation. Consequently, there is no speculation in such markets to generate wealth and capitalization. Price stability and responsiveness to sustainability as long-run phenomenon complementing the variables by their systemic evolutionary learning (θ-effect) establishes a dynamic basic-needs regime of development under the impact of appropriate technology (ρ) induced by θ.

Mishan’s categorization of systemic interrelations for the MSFRE model can be formulated by the following chain relation:

⇔ implies circular causation of any one variable with the remaining variables, all being induced by evolutionary learning as systemic unity of knowledge between the variables, even as simulation is carried out with increasing θ-ranked values.

The emergence of basic-needs regime of development spells out the attained levels of wellbeing by the social choice of the ‘good things of life’. In it the wellbeing function is simulated under the condition of pervasively complementary relations between the variables as shown, but with the key negative relationship with r and c. It is now logical that price stability will be maintained as output increases in the full MSFRE model.

Now in the absence of any need to have a capital market in the MSFRE form of the dynamic basic- needs regime of development, speculation and independence of the financial sector disappears. Volatility of the financial and economic sectors is annulled. The resulting regime reflects ethical integration with the socioeconomic basic-needs development regime (Streeten, 1981). We have thus established the conformable, sustainable, and complementary circular causation relations with the epistemic choice of knowledge-induced variables through simulation of wellbeing in the MSFRE model taken up in its entirety.

A Casual Reference to MSFRE Model in the Open Economy

The MSFRE model cogently maintains its consistency and completeness in the open economy case. Very briefly speaking, the foreign direct investments are now diverted away from portfolio (liquidity) investments (savings) into the real economy. The exchange rate mechanism is now determined by productivity spelled out by terms- of- trade.6 Improving terms-of-trade depend upon effective diversification, productive transformation, and trade-orientation along the dynamic basic-needs regime of development. Price stability also stabilizes the terms-of-trade along with price stability. Stock markets are now segmented between the financial products and the real market exchange. Global economic integration of the real markets is causally related with the momentum of technological advance, productivity, and factor prices, prices of goods and services, fair terms- of-trade, and exchange rates.

Inter-country capital mobility occurs by way of resource mobilization into productive spending in the dynamic basic-needs regime of development through market integration in the MSFRE model applied to real markets. Money is now mobilized as financial resource by appropriate participatory financial instruments into the real economy. In these respects appropriate participatory financial instruments such as, equity participation, joint venture, trade financing, co-financing, and profit-sharing are used in a phased out situation of interest-rate and exchange rate mechanism. Inflation targeting is thereby encouraged but within the dynamics of the MSFRE model.

In the end, along with economic stabilization effective terms-of-trade and exchange rate stabilization occurs. This facilitates foreign trade and free flow of tradable goods, resources and services between countries. Along with such free flows in goods and services, capital flow liberalizes in terms of joint ventures, equity participation, co-financing, trade-financing, and profit-sharing ventures. Capital formation now becomes a productive process in the dynamic basic-needs regime of development of the MSFRE model.

The relevance of stock market is now relegated to the above kind of function of maintaining economic stabilization and wellbeing. But to maintain such sustainable future knowledge induction on the continuity of such a process is required. Such evolutionary sustained and systemic learning is the result of the epistemic θ-induction. It requires participatory dynamics integrating together the public and private sectors and the global economic community (Commission on Global Governance, 1995). Formation of such participatory future, which is the result of circular causation between interacting and integrating agencies that are receptive to evolutionary learning in the unification experience, is an example of systemic unification of knowledge.

Empirical Issues: Stock Market and Macroeconomic Indicators- Case of Bangladesh Stock Market Near Financial Collapse

The prevailing reasoning in economic theory relating to the financial sector as a necessary one for a modern economy has disengaged various sectors of the economy on the face of a volatile stock market that inherits the dissociated and competing nature of the economy instead of a complementary one. We take the case of Bangladesh where the stock market volatility neared financial crash. This brought agony to the shareholders, most of whom are marginal savers led away to raise capital from the stock market to become rich by easy buck. But the dream was dashed.

Stock market turmoil started in Bangladesh near to 1210 after a resilient performance in earlier years. The causes cannot be attributed to fluctuations in short-term interest rates, because the discount rate of Bangladesh Bank remained fixed at 5 per cent throughout the period 2006 t0 2009, for which data are available (Table 1).

Instead of fluctuation in short-term interest rates as the cause of stock market volatility the data near to the year of capital-market turmoil in Bangladesh point out that in spite of a slight easing in the rate of inflation the rate of change in manufacturing GDP as a share of total GDP declined throughout the period. This implies that adequate diversification of the Bangladesh economy in the direction of increasing manufacturing did not occur. Hence the total productivity in B angladesh did not show the resilience that should be expected by manufacturing diversification. Diversification here is shown by the rate of change of the percentage share of manufacturing GDP. This remained low and declining on the time-trend.

Table 1. Some critical economic indicators to analyze Bangladesh stock market volatility

| Years | Manufacturing GDP as % Share of Total GDP (%) | Growth Rate of % Share of Manufact GDP (%) | Inflation Rate (% Change of CPI) (%) | Rate of Change in DebtBurden (% rate of Change in External Debt) | M1 as Percentage of Total Monetary Exposure(%) |

| 2006 | 17.21 | 4.11 | 6.73 | 8.98 | 79.87 |

| 2007 | 17.77 | 3.25 | 9.10 | 6.31 | 79.32 |

| 2008 | 17.55 | 0.45 | 8.90 | 7.46 | 80.34 |

| 2009 | 17.87 | 0.11 | 5.42 | 4.08 | 77.04 |

Discount rate was held at 5% throughout this time period.

Source: Statistical, Economic, and Social Research for Islamic Countries (SESRIC) database.

The debt syndrome was also a factor in the stock market volatility. On a trend, the growth rate of external debt outstanding remained high, around an average annual of 6.71 percentage between 2006 and 2009. Thus external flow of investments and global confidence on Dhaka stock market remained weak. The only way to resuscitate the failing stock market was external remittances. This also indicated an unproductive use of remittances in the face of a failing diversification, and thereby productivity of the manufacturing sector.

It is then questionable why the stock prices of most companies in Bangladesh nose-dived as explained later. By mutual exclusion of the above factors by virtue of the data in Figure 2, it is probable that the main cause of the downturn was the lack of diversification and real sector productivity, and the debt problem in Bangladesh economy. Consequently, there was weakening link between the monetary sector and the real economic sector. This fact is further indicated by the continued high percentage distribution of Quasi Money (= Total Quantity of Money - M1) compared to the low percentage of M1. The meaning here is that real money did not flow into the real economy to generate output and thereby productivity. Much of the monetary aggregates in the form of quasimoney were locked in financial savings without a productive backing -- only to increase by interest income. Stock market was a key non-banking sector that used the savings of the banking sector on the basis of financial interest returns. This is sheer speculation intensity in the monetary usage. Whereas, what ought to have been the case of stabilization by and for sustainability would be the complementary linkage between money (i.e. M1), the financial sector (thus banks and stock markets), and the real economy (productivity and economic diversification).

The result of such sectoral segmentation in the otherwise much needed money, finance, and real economy complementary linkages, caused eroding confidence in the investors. Consequently, a flight of capital took place out of Bangladesh stock market. Those who could illegally transfer money out of stock market into the foreign holdings benefited from their corrupt practices at the expense of the marginal savers in the Dhaka stock market.

True asset pricing that would depend most significantly on economic productivity and diversity that are caused by sustained linkages between the monetary sector, the financial sector, and the real economy failed to exist. Thus it is the link between these sectors that otherwise is fundamental for the stabilization and sustainability of the economy and its growing resilience. The stock market became the Achilles' heel for Dhaka stock market volatility and its near dissolution close to the year 2010.

To come out of the erosion of investor confidence, and to restore confidence by the systemic signs of stabilization and sustainability, the state of the economy reflected in the kind of stock market model would be to pursue complementary linkages between the monetary sector and the real economy by means of appropriate financial instruments. The B angladeshi foreign remittances can then be utilized in investments that would respond to the productivity gains generated by the complementary linkages causing diversification.

This paper therefore developed a generalized system and cybernetic model in the form of a complementary inter-sectoral participative model. The model while being of a system and cybernetic type is also deeply structural and strategic in nature. It invokes fundamental changes that remain embedded by the robust effect of monetary policy, central bank and commercial bank relations, and the responses of the real economy to productive spending in order to support the development of diversified productive projects. Financial instruments that systemically reduce speculation and replace it by increasing levels of financial mobilization are the appropriate ones. We refer to such a participative and inter-sectoral complementary model of money, finance, and real economy linkages as the MFRE model (Mufeedh Choudhury, 2009).

An example of Dhaka Stock Exchange trade summary for February 16, 2012 points out the following picture on stock market volatility: 82 listed firms reported positive net percentage change for the trading day. 185 listed firms reported non-positive net percentage change for the same trading day. The total net percentage change was -161.68%.

CONCLUSION

Our study of the nature and volatility of stock market prices and yields was cast against the theory and performance of some principal macroeconomic indicators. The existing theory of macroeconomic coordination to stabilize the economy has deepened the problem of instability, volatility and unsustainable development due to the failure to complement the good things (indicated by variables) that would stabilize the economy and at the same time maintain the stability and growth of wellbeing. Money and Spending regimes and their inherent policies were complemented together by the endogenous learning process between them across evolutionary knowledge flows. These knowledge flows were derived on basis of the epistemic premise of unity of knowledge idea of inter-variable complementary relations.

Economic theory between monetarism (Friedman) and fiscalism (spending as per Keynes) is fractured beyond repair to date. Instead, a theory of complementary dynamics is required that can be useful for establishing sustainability and stabilization over the long-run. A new theory emerges that designs the complementary and participative dynamics of monetary and fiscal (spending) regimes for accelerated development. This kind of thinking and implementation of the design of the new monetary, fiscal, spending and real economy interrelations was formulated in an analytical model called the MFSRE model.

Economic analysis carried out in the framework of the MFSRE model presented an altogether new perspective of economic stabilization and sustainability by the principle of pervasive complementarities in the case of interest rate being replaced by participatory financial instruments that mobilize savings into the real economy, rather than accumulate them into bank savings. The resulting real economy in such a pervasive complementary systemic framework is the social economy that produces, consumes, distributes and trades in the good things of life. This assumes the design of dynamic basic-needs regime of sustainable development.

The case study of Dhaka Stock Exchange in Bangladesh is discussed as an example. The country is found to rely on old macroeconomic theory, perspectives, indicators and policies. This has established traditional beliefs on the stock market volatility. The experience proves that Bangladesh orientation in macroeconomic theory and its effects on the stock market remains outmoded. A new design of macroeconomic arrangement needs to be formalized and practiced in the interest of economic stabilization and social wellbeing. Such a model was our prescriptive MFSRE model and its conceptual analysis explaining theory and revealing the same by empirical facts.

REFERENCES

Blaug, M. (1993). The methodology of economics. Cambridge, UK: Cambridge University Press.

Choudhury, M. (2009). Money, finance, and the real economy in Islamic banking and finance: Perspectives from the Maqasid as-Shari’ah. Unpublished MSC dissertation, Department of Economics, University of Stirling, UK.

Choudhury, M. (2012). A probabilistic model of random fields. International Journal of Operations Research.

Choudhury, M. A. (2011). Islamic economics and finance: An epistemological inquiry. Bingley, UK: Emerald.

Commission on Global Governance. (1995). Global civic ethic. In Our global neighbourhood, a report of the Commission on Global Governance. Oxford, UK: Oxford University Press.

Dreyfus, H. L., & Rabinow, P. (1983). M. Foucault: Beyond structuralism and hermeneutics, the archeology of the human sciences. Chicago, IL: University of Chicago Press.

Dreyfus, H. L., & Rabinow, P. (1983). The archeology of the human sciences. Chicago, IL: University of Chicago Press.

Farmer, R. E. A. (2010). Will monetary and fiscal policy work? In How the economy works. Oxford, UK: Oxford University Press.

Friedman, M. (1960). Aprogramfor monetary stability. New York, NY: Fordham University Press.

Friedman, M. (1989). Quantity theory of money. New Palgrave: Money.

Hayek, F. A. (1999). Towards a free market monetary system. In S. Kresge (Ed.), Good money, partII, the standard. Chicago, IL: The University of Chicago Press.

Henderson, J. M., & Quandt, R. E. (1971). Microeconomic theory. New York, NY: McGraw-Hill.

Holton, R. L. (1992). Economy and society. London, UK: Routledge.

Kaldor, N. (1975). What is wrong with economic theory? The Quarterly Journal of Economics, LXXXIX(3), 347-357. doi:10.2307/1885256

Maturana, H. R., & Varela, F. J. (1987). The tree of knowledge. London, UK: New Science Library.

Meera, A. K. M. (2004). The theft of nations, returning to gold. Kuala Lumpur, Malaysia: Pelanduk.

Mishkin, F. S. (2007a). What should Central Banks do? Monetary Policy Strategy (pp. 37-58). Cambridge, MA: The MIT Press.

Mishkin, F. S. (2007b). The transmission mechanism and the role of asset prices in monetary policy. Monetary Policy Strategy (pp. 59-74). Cambridge, MA: The MIT Press.

Myrdal, G. (1957). An unexplained general traits of social reality. In Rich lands and poor, the road to world prosperity. New York, NY: Harper & Row.

Myrdal, G. (1958). The principle of cumulation. In P. Streeten (Ed.), Value in social theory, a selection of essays on methodology by Gunnar Myrdal (pp. 198-205). New York, NY: Harper & Brothers Publishers.

Parsons, T. (1964). The structure of social actions. New York, NY: The Free Press of Glencoe.

Parsons, T., & Smelser, N. (1956). Economy and society. London, UK: Routledge & Kegan Paul.

Rawls, J. (1971). A theory of justice. Cambridge, MA: Harvard University Press.

Streeten, P. (1981). From growth to basic needs. In P. Streeten (Ed.), Development perspectives. New York, NY: St. Martin’s Press.

Toner, P. (1999). Conclusion. In Main currents in cumulative causation, the dynamics of growth and development. Houndmills, UK: Macmillan Press Ltd.

Ventelou, B. (2005). Economic thought on the eve of the general theory. In Millennial Keynes. Armonk, NY: M.E. Sharpe.

Von Mises, L. (1981). The return to sound money. In The theory of money and credit (pp. 477-500). Indianapolis, IN: Liberty Fund.

Yeager, L. B. (1997). The fluttering veil, essays on monetary disequilibrium. Indianapolis, IN: The Liberty Press.

Young, A. (1928). Increasing returns and economic progress. The Economic Journal, XXXVIII, 527-542. doi:10.2307/2224097

ENDNOTES

Consider the following compound function between Money, Spending, Growth, Price, and Productivity, F(M,S,G,P,Pr) = Constant. By the Implicit Function Theorem, M = F1(S,G,P,Pr); S = F2(M,G,P,Pr). By the Keynesian argument a full-employment target is attainable by (P,G)-stable relationship. Yet if a further monetary expansion occurs around the full-employment point of (P,G), the built-in income and money multipliers will push the economy into an inflationary phase and still maintain the neutrality of money and spending on the level of output. Thus a contradiction arises between monetary and fiscal regime in a productively expanding economy.

Consider the rate of change in real money denoted by m = M/P: log(m) = logM-logP, yielding m = M- P = [(ay + br) - P], according to the LM-curve in (y,r). Thus, increasing m-values imply m>0. That is, (ay + br) - P > 0; or, y > (P - br)∕a > 0. Since monetary policy is expected to contribute to market process and real sector growth according to the adage of monetarism, therefore, P > br, even with parametric positive variations in variable ‘b’ according to monetarist perspective. Consequently, as r increases along the LM-curve by monetary supply, therefore P increases as well. Stability in (r,P) is lost. Y is drawn back. This conclusion supports the results shown in Figures 1 and 2.

Foucault, M. “By episteme we mean... the total set of relations that unite, at a given period, the discursive practices that give rise to epistemological figures, sciences, and possibly formalized systems. The episteme is not a form of knowledge (con- naissance) or type of rationality which, crossing the boundaries of the most varied sciences, manifests the sovereign unity of a subject, a spirit, or a period; it is the totality of relations that can be discovered, for a given period, between the sciences when one analyses them at the level of discursive regularities.”

Price of stock in perpetuity of $1 yield is written as, P = 1/i. Thereby, as i varies randomly, so also P in the portfolio of long-term assets becomes volatile.

Let Y0 denote GDP at time t = 0,1,2,. ; st denote saving ratio at time t = 0,1,2,.; g denote a constant growth rate of GDP at time t = 0,1,2,. Disposable income after saving at time t = 0 is Y0(1-s), which increases to national income Y1 at time t=1. Y1 = Y0(1-s) (1+g). Likewise, Yt=Y0.(1+g)t (1-s)t. Now consider, ∂Yt∕∂s = -tY0.(1+g)t(1-s) t-1 < 0 ∂Yt∕∂g = tY0.(1-s)t(1+g) t-1 > 0 only due to the positive effect of g but dampened by the negative effect of s. These results remain true irrespective of a moment of time and in the continuous sense. Besides, the argument that a higher volume of savings would grow into more resources for investment in the future contradicts the fact that at any moment of time that volume of savings is a resource withdrawal. That amount of potential resource could otherwise have been used to

perpetuate economic growth and thereby development and social wellbeing.

By definition, effective exchange rate (e) is e = ppip = [(∑px1.x1)∕∑x1]∕[(∑pmj.Mj)∕∑Mj] = [ΣMj∕ΣXi]. [(Σpχi.Xi)∕(Σpmj.Mj)] = α,T where, PX denotes average price of total exports X. pM denotes average price of total imports M. Xi denote specific (i) export quantities. Mj denote specific (j) import quantities. pχi denote specific (i) prices of imports. p j denote specific (j) import prices. α = [ΣMj∕ ΣXi] is a stabilizing constant in a dynamic basic-needs of sustainability. T = [(Σpχi.Xi)/ (Σpmj.Mj)] denotes stable terms-of-trade (T) in a dynamic basic-needs regime of development. Hence, exchange rates remain stable and avoid the interest-rate and exchange rate policed mechanism. This replacement comes about by the active epistemic conduct of wellbeing by θ-ranked values that reflect the actual and the simulated levels of unity of knowledge by complementarities between the variables in economic stabilization. In the end, effective exchange rate formula in the productivity driven dynamic basic-needs regime of development is given by, [e = α.T] [θ]; now with the extended vector of circular causation relations between the variables, {y,p,M,F,f,r,u,ρ,Imports, Exports, Export prices, Import prices, e, T, α)[θ]. Note here the endogenous nature of all the variables in circular causation relations under the induction by θ-ranked values causes the coefficient-like parameter α to be variable under the dynamic effects of learning in the sustainability of the dynamic basic-needs of development.

This work was previously published in International Journal of Innovation in the Digital Economy (IJIDE), 4(2); edited by Elena Druica and Ionica Oncioiu, pages 1-17, copyright 2013 by IGI Publishing (an imprint of IGI Global).

More on the topic Chapter 79 A New Macroeconomic Architecture for the Stock Market: A General-System and Cybernetic Approach:

- Chapter 18 Modeling the FX Market Traders’ Behavior: An Agent-Based Approach

- The market simulates the FX market trading activity on at the level of a market-maker market.

- Surgical Approach: General Principles

- A general concept of an economic system

- Chapter 24 A Conceptual Framework for Online Stock Trading Service Adoption

- Chapter 26 International Stock Investment Portfolio Management Strategies for Emerging Economies

- Chapter 41 Connectionism and Cognitive Architecture: A Critical Analysis Jerry A. Fodor and Zenon W. Pylyshyn

- The Macroeconomic Model

- Cybernetic Aspects

- Chapter 55 Establishing the Linkage between Internal Market Orientation and Service Innovation

- Chapter 64 A Diagnosis of the Determinants of Dividend Payout Policy in India: A Factor Analytical Approach

- Market Research: Finding the Market Gap

- Market Research: Finding the Market Gap

- Chapter 66 The Adoption Process of Payment Cards: An Agent-Based Approach