Chapter 80 Identifying Different Forms of Innovation in Retail Banking

Veronique Favre-Bonte

Laboratory Institut de REcherche en Economie et en GEstion (IREGE), University of Savoie, France

Gardet Elodie

Laboratory Institut de REcherche en Economie et en GEstion (IREGE), University of Savoie, France

Catherine Thevenard-Puthod

Laboratory Institut de REcherche en Economie et en GEstion (IREGE), University of Savoie, France

ABSTRACT

To be competitive and capture new customers, banks must develop continuous innovations that can reduce costs, enhance existing service quality, expand current service offerings, and increase market share.

This article proposes a typology of different types of innovation in the retail banking sector on the basis of a case study of the leading French credit institution, Credit Agricole. This bank does not innovate just incrementally, and radical innovations resulted from the launch of a new distribution channel, though several innovations are unrelated to new technology. This study adds to literature on innovation services by enhancing understanding of the different types of innovation. The empirical investigation further shows that the banking sector can develop process innovations, which give the bank a longer term competitive advantage. To innovate radically, the bank should anticipate the impact of its new offerings on different areas of the system.1. INTRODUCTION

Despite growing service-related and innovation management research, researchers continue to call for further studies that can improve understanding of service innovation (Ordanini & Parasuraman, 2010). The service sector remains the “poor relative” in innovation management literature (Gallouj 2002), which concentrates instead on technical

DOI: 10.4018/978-1-4666-6268-1.ch080 innovations (Damanpour, Walker & Avellaneda, 2009), especially in biotechnology, semiconductor, and other such industries (Baum, Calabrese & Silverman, 2000; Gilsing & Nooteboom, 2005; Roij akkers, Hagedoorn & Van Kranenburg, 2005).

Yet such results rarely apply effectively to the service sector (Sundbo, 1997), because of its lack of standardization, as well as the relatively minimal investments in R&D for services, leading to an.

informal, customer-affiliated innovation process (Lusch & Nambisan, 2012). Common criteria for measuring technological innovations, such as the number of patents or R&D budgets, are not valid for services. Innovation in the service sector also is less tangible, reliant on human and relational factors rather than technology (De Jong & Vermeulen, 2003; Ettlie & Rosenthal, 2011). Furthermore, specific forms of innovation generally pertain to particular service sectors, which encourages researchers to concentrate on single-sector studies: five-star luxury hotels (Ordanini & Parasuraman, 2011), hospitals (Djellal & Gallouj, 2005), or retail networks (Cadwallader et al., 2010).

In this study, we focus on the banking sector, which represents approximately 8% of the gross domestic product (GDP) and 4% of employment in member countries of the Organization for Economic Cooperation and Development (OECD, 2008). It also has undergone significant regulatory and technological changes and faced increasing competition in recent years with the arrival of online competitors (Athanassopoulou & Johne, 2004). In this difficult context, banks have had to innovate to remain competitive, whether to lower their costs or differentiate themselves from competitors (Drew, 1994; Han et al., 1998; Reidenbach & Moak, 1986; Storey & Easingwood, 1993). Despite increasing numbers of innovations in the banking sector (OECD, 2005), our knowledge in this area remains uncertain (Athanassopoulou & Johne, 2004; De Jong & Vermeulen, 2003; Menor & Roth, 2006; Oliveira & von Hippel, 2011; Re- idenbach & Moak, 1986). Authors investigating banking innovation often consider the development of new offers (De Jong & Vermeulen, 2003) or implicitly assume that banks cannot innovate beyond new technologies (Ding, Verma & Iqbal, 2007; Karmarkar, 2000; Oliveira & Von Hippel, 2011).

In this sense, an effective framework for innovation in the retail banking sector is lacking.Innovation, in the literature, mainly refers to the creation of value directed toward the customer, though it also might involve other areas, such as a bank’s organization (Oliveira & von Hippel, 2011). It also might feature several dimensions (Avlonitis, Papastathopoulou & Gounaris, 2001), including service concepts, processes (information systems or work methods), organizations (hierarchical level, structures), and external relationships (interfaces, intermediaries). We define innovation as occurring when the bank takes deliberate actions to increase its profits (De Jong & Vermeulen, 2003). With this definition, we aim to clarify the scope of innovation in banking, show how several categories of innovation apply in retail banking, and propose a typology of categories.

We begin by reviewing prior research into innovation in both banking and the general services sectors. With this information, we develop a typology for identifying innovations in the banking sector. Then we apply the proposed typology to France’s main retail bank, the Credit Agricole, to check its relevance. It leads into our discussion of the effects of an innovation on the innovation portfolio and the innovation process. Finally, we note some implications and limitations of our research.

2. INNOVATIONS IN BANKS: PRIOR LITERATURE

Prior literature on the banking sector suffers two main limitations: It focuses on new offers (visible innovations for customers) and assumes technological progress is the only source of innovation. We offer a typology that might better explain variety in banking innovations.

2.1. Limits to Extant Current Research

According to the first research on innovation in the banking sector, banks do not always rely on innovation as a means for development. However, those that establish and formalise development programs for new products perform better than others, whatever their size (Reidenbach & Moach, 1986; Reidenbach & Grubs, 1987).

Naslund (1986) compares financial and industrial innovation and shows that banks innovate, but their innovations are easy to imitate because they are also easier to implement. A bank that innovates benefits from its market leadership only for a very short time, because its competitors quickly imitate the new service offering (which cannot be patented).Such research appears interested mainly in new service developments (NSD, Sundbo, 1997), largely ignoring other types of innovation, such as service delivery (e.g., Athanassopoulou & Johne, 2004; De Jong & Vermeulen, 2003; Menor & Roth, 2006). Yet the widespread exposure of banking to technological progress has changed many operational aspects of banking, especially in back offices (Cooper & De Brentani, 1991; Lusch & Nambisan, 2012). For example, the automation of administrative tasks allows staff to spend more time with customers in sales and advisory roles. Considering the influence of technological and IT progress, Barras (1986, 1990) offers a theory about the spread of technological innovation in services, such that a bank’s adoption of a new computer system initiates a series of three phases of innovation:

1. The learning curve for the new software causes incremental process innovations, designed to improve service efficiency (e.g., automation of back office functions through a centralised mainframe computer system);

2. Improvements to the service quality stem from more radical process innovation (e.g., ATMs that cut costs and improve quality);

3. Product innovation may appear (home banking).

This theory predicts no innovations beyond technological possibilities; several other authors similarly focus on the role of technology-based innovative banking practices (Ding et al., 2007; Karmarkar, 2000; Oliveira & von Hippel, 2011). For example, Ding et al. (2007) focus on the development of self-service activities (e.g., automatic cheque deposits, account balances, printing of bank statements), for which technology is an essential resource.

Although the impact of technol - ogy on innovation in the banking sector is undeniable, banks also might innovate independently of technology (Djellal & Gallouj, 2005; Gadrey, Gallouj & Weinstein, 1995; Kandampully, 2002; Sundbo, 1997), which is only one component of service delivery. Other factors may initiate innovation: deregulation that allows the introduction of previously prohibited services, changing customer behaviours that create new requirements or needs, or increasing competition that pushes banks to differentiate themselves and develop new human resource skills (Cadwallader et al., 2010). In addition, banking innovations are not always visible, such as social innovations that involve individual behaviours (e.g., new roles for company staff; Cadwallader et al., 2010) or management innovations (Birkinshaw, Hamel & Mol, 2008). In services though, management innovations are even more likely to provide competitive advantage than technological prowess (Mol & Birkinshaw, 2009). Thus the Barras model represents a simplified version of the reality for banks (Gallouj, 2002).Neither the approach that concentrates on NSD nor those based on technology impact take into account the variety of innovation in banking. Therefore, we need a typology that better addresses variety in banking innovation.

2.2. Proposed Typology of the Entire Scope of Banking Innovation

Few authors have tried to compile a typology of innovation in banking. Karmarkar (2000) concentrates on services related to new technologies (Internet, telephone, interactive terminals) and proposes a typology along two axes: means of access (i.e., centralized, such that the client must go to the service, or decentralized, such that the

client can access the service without moving) and the cost of access (from low to high).

With a broader review of innovation in services in general, we find several typologies (Table 1), though most of them rely on a single dimension, such as:

• The element affected by the innovation (product, process, or organization; Belleflamme, Houard & Michaux, 1986; Damanpour et al., 2009; Hamdouch & Samuelides, 2001);

• The degree of novelty of the innovation, which can be combined with its risk level (i.e., new to the organization or new to the world; Birkinshaw et al., 2008);

• Means of production (with or without customer participation; Sundbo & Gallouj, 1998).

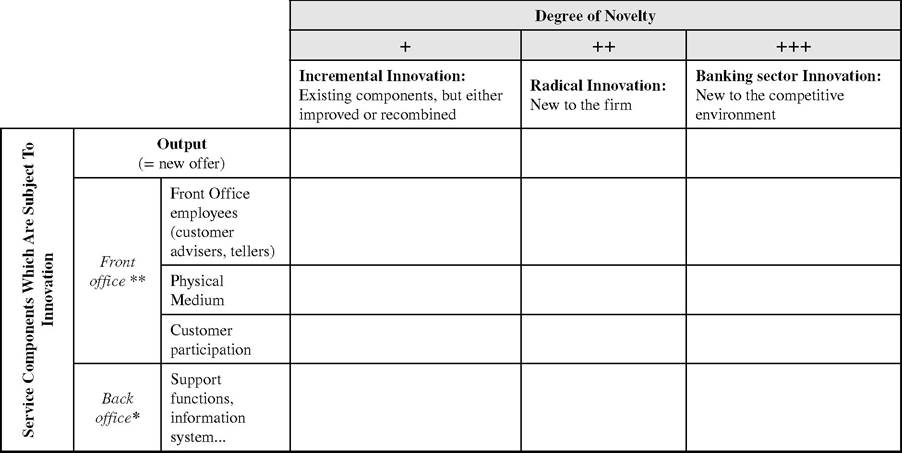

These criteria, though relevant, tend to be isolated and cannot quite encompass the total variety of innovations in banking. Some classifications appear to build on several criteria, but they are not always explicit (de Vries, 2006). In this sense, no existing typologies are sufficiently operational to identify different types of innovation that may exist in the banking sector, which leads us to suggest a two-dimensional matrix (Table 2).

The first dimension relates to what exactly is being innovated, that is, the element that will be affected by the novelty. The second dimension relates to the degree of novelty of an innovation (how new?). Regarding the subject of innovation, we adopt Langeard et al.’s (1981) model of five components of a servuction system (neologism used by the authors to describe the production of a service: service + production = servuction). The back-office (i.e internal organization, or backstage) includes all traditional functions of a company that are invisible to the customer (marketing services, human resources, purchasing...) and their operations (working methods, equipment, information systems...). The front office consists of tellers (advisers), the physical medium (equipment used by the staff or customers in service delivery, such as branches, though also more generally the premises on which the service is delivered), and the customer, who is more or less involved in service production (define the problem and/or engage in operational tasks). Finally, the system delivers, as an output, the service or offer to the customer. This model thereby differentiates more service components than a product-process-organization approach, such that it can distinguish what is visible to the customer from that which is not. In addition, we can consider an essential constituent of a banking system, namely, the back office, where fundamental contributions often appear, such as management innovation (Hamel, 2006).

The second dimension, focused on the degree of novelty of the innovation, makes it possible to identify whether banks can develop innovations that are more than minor (Gallouj, 2002). An incremental innovation refers to items already available that the bank improves or recombines (Gallouj & Weinstein, 1997); radical innovations entail elements that are new to the company but already may exist elsewhere; and a banking sector innovation introduces an element that is entirely new, both to the company and the sector at large. We check this proposed typology by applying it to a French retail bank: Credit Agricole.

3. METHODOLOGY AND RESULTS

We use a single case study to understand innovations in the banking sector, such that we detail each innovation developed by the studied firm and situate it in our proposed typology. In addition, we describe two examples of innovation in greater detail to highlight a recurrent phenomenon, namely, the cascade effect of innovation.

1543

Table 1. Service innovation typologies in prior literature

| Authors | Type of Service Studied | Classification Criteria | Identified Type of Innovation | Limits |

| Belleflamme et αl. (1986) | Services in general | Innovation purpose | • Introduction of a new service • Innovation in the production process • Innovation in the Servuction process • Combination of the three | Does not investigate the degree of innovation. Vague about the process of production and servuction. |

| Sundbo and Gallouj (1998) | - | Terms of innovation | • Customized innovation • Ad hoc innovation (coproduction with customer) • Recombination innovation • Incremental innovation • Formalisation innovation | Typology focuses more on the method of production (process) rather than the result |

| Hamdouch and Samuelides (2001) | NICT services (e.g., telecommunications) | Innovation purpose | • Organizational innovations (functions, tools, relations) • Commercial innovations (products, relations to customers) | Too focused on the impact of ICTs on service innovations |

| Diellal and Galloui (2005) | Hospital | Innovation purpose | • Logistical and material transformation trajectory • Logistical and information processing trajectory • Methodological trajectory • Pure service trajectory • Relational trajectory | Categories sometimes seem close, because logistics normally includes the management of information flows |

| De Vries (2006). based on Gallouj and Weinstein (1997) | Several types | Several criteria | • Radical innovation • Incremental innovation • Ad hoc innovation • Architectural innovation | Conceptually interesting, but hard to use (lack of operability). The ad-hoc innovations are non-existent in retail banking. |

| Damampour et al. (2009) | Public service organizations | Innovation purpose | • Service innovation • Technological process innovation • Administrative process innovation | Distinguishes customer-oriented from business-oriented innovations |

Identifying DifferentForms of Innovation in Retail Banking

Table 2. Proposed retail banking typology

* Invisible to the customer, ** Visible to the customer

3.1. Single Case Study Methodology

To assess the relevance of our typology, we study a retail bank in depth to identify various innovations in the past decade and classify them. We selected the Credit Agricole for several reasons. It represents the leading French credit institution, in terms of its equity capital (70.7 billion euros in February 2012), number of employees (more than 80,000), and its market share in retail banking (28% in 2012). Its net banking income also placed the Credit Agricole in a leader position in 2008 (28.5 billion euros for Credit Agricole in 2008; 27,4 for BNP Paribas). In 2012, however, Credit Agricole is at the second place of the market on this criterion basis (35.13 billion euros), behind BNP Paribas (42.4 billion euros)1. As a leader in the retail market, it offers many innovations and has a reputation as one of the most dynamic banks in the marketplace. Furthermore, Credit Agricole is highly decentralized, with 41 autonomous regional entities. We focus on the operations of one such entity, which adopts innovations developed by headquarters while also enjoys independence, being authorised to develop its own innovations.

To identify innovative practices, we conducted ten semi-structured interviews (Table 3), each of about one and a half hours, during 2007 and 2008. The interviews aimed to understand key innovations developed over the past decade, including their nature, origins, degree of novelty, and strategic impact on the entity.

To supplement the interviews, we collected data from internal secondary sources (memoranda written by headquarters, presentations of innovations to employees) and external sources (newspaper articles). The codification process followed recommendations by Huberman and Miles (2003). Each interview was coded and gradually refined, as soon as possible after each interview, providing a basis for subsequent discussions. We also compared the information, when possible, and undertook triangulation across the primary and secondary data.

Table 3. Overview of interviews within the regional bank

| Interview Duration | Interviewee Job | Innovations Studied |

| 1h45 | Marketing Manager | Mozaic/Green Points/Products for Seniors/New agency concept |

| 2h00 | Vice Director | Insurance/Mozaic/Green Points/Products for Seniors/New agency concept |

| 1h30 | Bank service manager | Products for cross-border workers/Intelligent Billing |

| 1h00 | Agency manager | Products for cross-border workers |

| 1h45 | Cheque service officer | Automation of cheque deposits |

| 2h00 | International service employee | Products for cross-border workers |

| 1h00 | Marketing manager assistant | Mozaic/Green Points/Products for Seniors/New agency concept |

| 1h30 | Geographical area manager | Products for cross-border workers |

| 2h30 | Marketing manager | Products for cross-border workers/Mozaic/IHM/Seniors/New agency concept/Green Points/New methods of diagnosis/Square Habitat |

| 1h30 | Logistics officer | New agency concept/, GUI Ergonomics/Intelligent Billing |

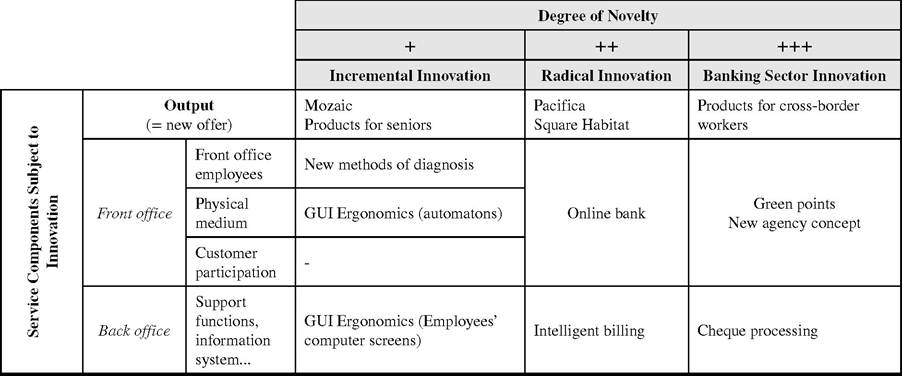

Table 4. The Credit Agricole’s innovations

| Name of the Innovation | Description | Position in the Matrix |

| Mozaic | This specific offer targets young (10-25 years) consumers with a service package that includes various banking products (checking account, credit card, student loan at preferential rates, no fees) and other benefits (discounts on products from corporate partners such as cinemas, CDs, invitations to events). | It implies a new incremental offer, because the various services existed but were recombined and improved (i.e., adapted to the needs of the target market). |

| Loans for senior citizens | These packages include consumer loans, mortgages (lifetime mortgage loan), life insurance contracts, and so forth. | The incremental new offer entails a new assembly and enhancement of existing offers. |

| New methods of diagnosis | By creating branch-level diagnosis tools, this innovation facilitates the work of advisors who deal with insurance, savings, credit, tax optimization, and inheritance issues. These formalisation innovations (Sundbo and Gallouj, 1998) help the staff structure interviews and improve the bank’s understanding of customers. | The incremental innovation enables frontoffice staff to propose offers that better meet customers’ needs and expectations |

| Improved GUI ergonomics | Both customers and back office staff relied on this new graphical user interface (GUI). Customers found an easier to use ATM interface (colours, text, data density, screen layout, messages). For example, customers previously received cash from the machines and then waited to receive their cards. Many customers forgot to remove their card, leading to the need for many card cancellations and increased staff workloads. The innovation required customers to remove their cards before the machine would dispense the cash. The back office staff also began to use Google on their desktops (easier access to information through more fluid navigation, topic-based search assistance on the intranet since November 2007). | These incremental innovations span the front office (visible to the customer), in the form of a physical medium that is constantly improved in cooperation with customers, and the back office. |

| Pacifica (property insurance) | Credit Agricole entered the property insurance market through a subsidiary. It offers customers packages composed of credit and insurance. Unlike its competitors though, Credit Agricole created the first direct link from the insured to service providers, including a single contact and fast service (e.g., file processing within 48 hours). Finally, the offer made to those affected by the situation is new because it proposes to buy brand - new equipment for the client with no condition attached (other insurance company applying a dilapidation pourcentage). | This new offer corresponds to a radical innovation for the company (property insurance is new to Credit Agricole) that requires staff to learn new skills beyond the core business (e.g., creation of a Claims Management Unit). However, the innovation is not new to the market, because other banks offer insurance services. |

| Square Habitat | Credit Agricole real estate agencies process global transactions and leases, or manage property. For example, the new Green Mandate allows sellers to receive compensation if their property has not been sold after three months and one day. In addition, the Credit Agricole is committed to advertising properties on sale every week in the press and provides proof of publication. | this radical innovation entails the company entering a new business market, as real estate agents. The Credit Agricole had to learn new skills beyond its core business. Before 2006, its real estate involvement were limited. However, this activity is not new to the market; the basic service already was provided by traditional real estate agents. |

| Online bank | An internet site allows easy and constant access to accounts and provides an opportunity for access without moving. | This is a front office innovation (teller, physical support, customer participation) in a new distribution channel. It is radical for the company but not for the market; Credit Agricole was not the first bank to launch the concept |

| Intelligent billing system | The new intelligent billing aims to customize service pricing for each customer (defined by age, quality, and so on). It offers a better understanding of the customer through the recording and analysis of data, which can then help customize the offer and retain customers. | As a back office innovation (invisible to the customer), it required the deployment of an ad hoc computer system to identify customer history and simulation and diagnosis software to adapt offers to customers. It is a radical innovation for the company that required new computer skills among the Credit Agricole. |

Table 4. Continued

| Name of the Innovation | Description | Position in the Matrix |

| Products for cross-border workers | The specific traits of the regional market produce products for crossborder workers, with their high purchasing power and specific needs. For example, they can transfer cross-border wages to a French deposit account (which requires a partnership with foreign banks), foreign currency loans (consumer or real estate) at fixed or variable rates, and savings products that protect customers from unstable exchange rates. | Credit Agricole has been a pioneer in setting up these specific offers for cross-border workers. They thus are new to the world. Although competitors have sought to imitate these offers, Credit Agricole remains one step ahead. |

| Green Points | Credit Agricole gives shops in rural areas the opportunity to provide banking services to their customers (cash withdrawal, bank transfer, applying for a credit card). This helps it maintain close relationships with customers in geographical areas without any branches. A new regulation prohibits staff members from transporting cash outside the branches prompted this innovation. | Despite a new distribution channel and front office innovation, the customer service remains the same. It is a banking sector innovation: no other bank proposes such a distribution channel. |

| New agency concept | A very dense network of entities is a prerequisite for a local strategy. The network determines the frequency of contacts and requires infrastructure to reduce operating costs and improve advice. To this end, the bank has developed a plan to renovate branches by including ATMs and give customers greater autonomy, as well as granting staff more time to undertake operations with higher added value. | This front office innovation redefined the staff mission, required an investment in a wide range of ATMs (physical media), and precipitated greater involvement by customers. With this innovation, Credit Agricole is a pioneer and has the broadest automated network in France; it is therefore a banking sector innovation. |

| New cheque processing | A subsidiary, the Centre of Processing and Payment Operations, allows retailers or individuals to scan cheques, using automation in the branch, and store the information (amount, customer identification). This information goes directly to the Credit Agricole platform, which helps secure transactions (no problems with lost cheques) and applies the credit to customers much faster (one day instead of an average of three days). | For this back office innovation, Credit Agricole had to acquire new technological and organizational skills and make major investments. Moreover, this innovation is a banking sector innovation; Credit Agricole was the first bank to introduce it (some competitors even outsource their cheque processing to Credit Agricole). |

Table 5. The typology applied to the Credit Agricole case

3.2. Credit Agricole’s Innovations

The regional entity we study regularly innovated or adopted innovations from the headquarters in the past decade. We particularly focused on the 12 innovations most frequently cited by the interviewees as real successes (see Table 4 for the description of the 12 innovations). All these innovations thus can be positioned in the matrix (Table 5). Our typology not only can encompass various innovations (despite their differences) but also distinguish among them.

Several observations pertain to the relevance of this matrix. First, no examples of innovations focused only on customers’ degree of participation. It thus appears relatively rare in retail banking for customer participation to change, without prompting from the introduction of a new physic al medium or front office employees. Although the marketing director of the regional entity admits that the focal bank has not developed any such innovation, the competition has done so2. Among the improvements made by innovating front office components (employees or physical medium), the most radical innovations entail the launch of a new distribution channel, which influences three front-office components.

These examples of banking innovation suggest several implications. Although technological progress opens many paths to innovation (online banking, cheque processing), in both the front and back office, many others are unrelated to new technology, such as the new offerings (products for cross-border workers, Pacifica, Square Habitat), some distribution channels (green points), or formal innovations regarding staff contacts with customers (new diagnosis methods). The easing of regulations, new customer needs (Payne et al., 2008), and imitation of competitors (Abrahamson & Fairchild, 1999) are potential sources of innovation, which are at least as important as (if not more important than) information and communication technology progress. These results are consistent with Han et al. (1998) who emphasize the link between market orientation and innovativeness. They also point out, in the case of the French banking market, the value of having a competitor orientation (Day & Wensley, 1988).

These cases of innovation also show that retail banks can produce innovations with a high degree of novelty, though some of them are invisible to customers (e.g., cheque processing). In this case, the question is whether the bank creates value for customers and enhances its competitive advantage. Because back-office innovations lower costs, the

bank can lower its prices or improve its service quality to attain a competitive advantage that may be easier to maintain over time, because its components also are less visible to competitors (Birkinshaw et al., 2008). Those innovations occur less frequently but are more significant in delivering superior value to customers (Parsons, 1991).

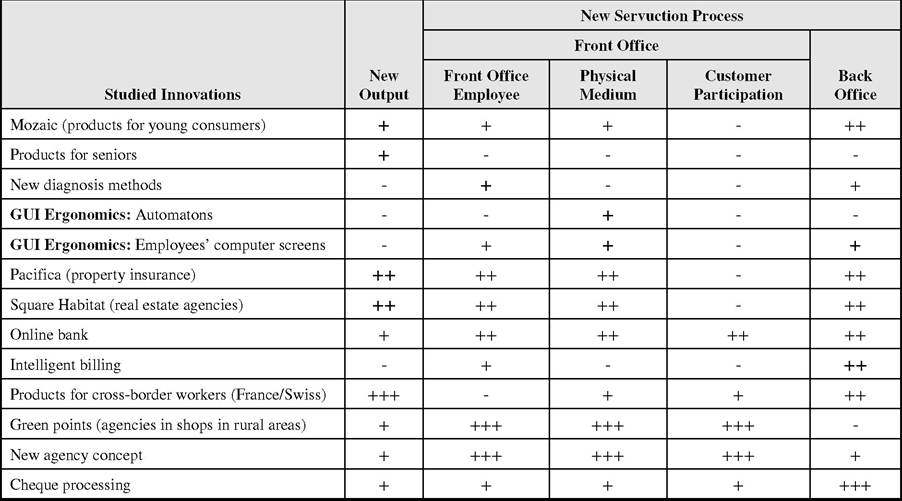

3.3. Cascade Effect

Several innovations also led to other innovations in different areas of the servuction system (Table 6), regardless of whether their initial goal was to propose a new offer to the customer or improve the back office. That is, innovation spreads progressively to reach other elements or even the entire system, a phenomenon already mentioned in prior research (Barras, 1986, 1990; Damanpour & Evan, 1984; Fritsch & Meschede, 2001). However, our analysis shows further that these snowball or cascade effects may not relate to the use of a new technology. A new trend seems to be emerging: the higher the innovation’s degree of novelty, the greater the impact on all the bank organization. A radical innovation or an innovation that the bank is the first (in the market) to implement exerts a greater impact on other parts of the servuction system than an incremental one. Finally, we propose that the starting point for a series of innovations may be the back office, the front office, or even the offering itself.

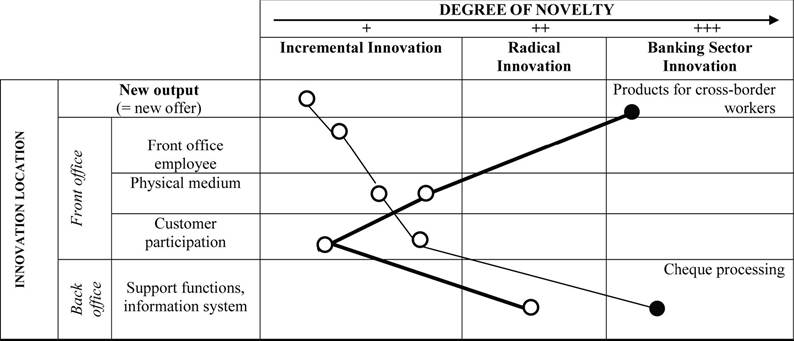

To illustrate the cascade effect, we examine in detail two innovations with different purposes (new offer and back office innovation) but the same degree of innovation (banking sector innovations): products for cross-boder workers and cheque processing (Table 7).

The raison d’etre of the cheque processing innovation was to cut costs, because it was difficult to bill customers for this service. The new organization created by the Credit Agricole allowed customers to deposit cheques 24 hours per day,

Table 6. Cascade effect of studied innovations

Notes: - No innovation in this part; + Incremental innovation; ++ Radical innovation for the firm; +++ Banking sector innovation for the competitive environment. Grey cells correspond to the starting point of an innovation. See Appendix for the description of the 12 innovations.

Table 7. Impacts of cheque processing and products for cross-border workers

Notes: Black points indicate the starting point of the innovation; white points show the impact of the innovation on the other elements of Servuction and therefore the cascade of changes that the innovation has triggered.

using a scanner. The images of the cheques are sent to a central platform that manages the flow from the different branches and credits customer accounts. Two video-coding workshops correct any errors (e.g., misread cheques) and the central cheque processing services compares the image file from the platform with the real cheques. The subsidiary then distributes cheques to the various regional entities and competing banks (checks of less than 5000 euros are archived for 60 days and images are returned to the branches every day). This back-office innovation (starting point) caused other innovations at various levels of the servuction system. In the front office, it prompted:

• Greater degree of customer involvement through cheque scanning;3

• Introduction of new physical media (successive generations of scanners);

• Reduced staff associated with cheque deposits.

In addition, service improved because the customer account is now credited within one, instead of three, days.

Regarding products for cross-border workers, this offer of new services (e.g., transfer of wages, fixed rate foreign currency loans) was accompanied by changes in physical media (specific areas on the website, new machines to change currency) and the back office. Changes in the back office included the development of new computer programs to monitor the stock markets and offer customers a competitive exchange rate, as well as partnerships with foreign banks that aggregated wages deposited by cross-border workers before making the transfer to Credit Agricole in France.

This cascade of innovations gives rise to two key observations. First, a bank that wishes to innovate drastically needs to be able to change the various components of the service system in a coherent manner (Damanpour et al., 2009). It must anticipate the impact of a radical innovation, which can affect different areas of the servuction system. Ettlie and Rosenthal (2011) similarly note the importance of the combined roles of senior managers, middle managers, and professionals in ideation and innovation development processes.

Second, some doubts remain about the relevance of research that only concentrates on new service development, because it can only have a fragmented view of innovation mechanisms or outputs. The introduction of a new offer often produces other types of innovation. The performance of a NSD thus must be linked to another innovation, such as back office innovation.

4. CONCLUSION

Most literature is interested in NSD (Sundbo, 1997) or the role of technology in innovative activity (Oliveira & von Hippel, 2011). Yet innovation takes multiple forms. With this article, we aim for a better understanding of the multiple forms of innovation and propose a typology to classify them. Our case study of Credit Agricole produces four main contributions. First, banks can innovate more than incrementally. They can market and sell completely new offers or implement original servuction processes. Second, banks can develop multiple innovations without any technological advances; for example, changing regulations and the varied needs of customers are important causes of innovation. Managers and customers thus should be encouraged to consider innovative codevelopments of new offerings. Third, our proposed typology can overcome some limits of previous works, by broadening the discussion to all banking innovations, not just to those of new services. Various back office innovations in the banking sector are not visible to the customer but may be strategic, particularly as a means to reduce operating costs. The bank must then take up the challenge of showing how it creates value to customers. Fourth, an innovation is rarely isolated. Especially if it is radical or new to the banking sector, it leads to other innovations in other components of the servuction system. Our typology highlights the impact of each innovation on the entire company.

Our findings also have practical implications for banks seeking to innovate. In particular, it is useful to recognize the different types of innovation that can provide a more or less sustainable competitive advantage. Managers should classify these innovations, using our typology, to identify their firm’s degree of innovation-especially with regard to innovations with a high degree of novelty that are invisible to customers (e.g., cheque processing). In this case, customers cannot perceive the innovation directly, even though it provides a sustainable benefit compared with competitors’ offers. Moreover, technological progress is not the sole source of innovation. It is possible to develop innovations that have no connection to new technology. Retail bank managers can look to regulations, new customer needs, and competitors for potential sources of innovation.

Of course, our results and implications are limited by the methodology used: our case study focused on innovation in one part of the banking sector (retail banking), one company (Credit Agricole) and one country (France). It is difficult to generalize results from a single case study. However, the Credit Agricole is a relatively representative bank of retail banking in France and Europe, thanks to its leading position in the French market and Europe (n°1 in France, n°3 in Europe) and through its presence in over 70 countries. Nevertheless, the phenomena studied here could be different in case of other types of banks. Future work could then look at the relevance of our results, including our typology, in investment banking. Furthermore, as every industry has special traits, empirical research in other types of industries could help establish the generalizability of our typology. Moreover, additional research might determine the importance of the process of implementing innovations in the banking sector by looking beyond the core organization (i.e., collaborators such as business partners or customers). The cascade effect we highlighted also should encourage researchers to apply qualitative methods to investigate banking innovation. In line with De Jong and Vermeulen (2003), for the process of emerging innovation, we propose further study of these processes that depends on their type. Doing so may lead to a better assessment of the cascade effect; in turn, organizations may require a long-term view of customer relationships, that does not fit well with the short-term financial goals that tend to drive capital markets.

REFERENCES

Abrahamson, E., & Fairchild, G. (1999). Management fashion: Lifecycles, triggers and collective learning processes. Administrative Science Quarterly, 44, 708-740. doi:10.2307/2667053

Athanassopoulou, P., & Johne, A. (2004). Effective communication with lead customers in developing new banking products. International Journal of Bank Marketing, 22(2/3), 100-125. doi:10.1108/02652320410521719

Avlonitis, G., Papastathopoulou, P., & Gounaris, S. (2001). An empiric ally-based typology of product innovativeness for new financial services: Success and failure scenarios. Journal of Product Innovation Management, 18, 324-342. doi:10.1016/ S0737-6782(01)00102-3

Barras, R. (1986). Towards a theory of innovation in services. Research Policy, 15, 161-173. doi:10.1016/0048-7333(86)90012-0

Barras, R. (1990). Interactive innovation in financial and business services: The vanguard of the service revolution. Research Policy, 19, 215-237. doi:10.1016/0048-7333(90)90037-7

Baum, J. A. C., Calabrese, T., & Silverman, B. S. (2000). Don’t go it alone: Alliance network composition and startups’ performance in Canadian biotechnology. Strategic Management Journal, 21(3), 267-294. doi:10.1002/ (SICI)1097-0266(200003)21:33.0.CO;2-8

Belleflamme, C., Houard, J., & Michaux, B. (1986). Innovation and research and development process analysis in service activities. Brussels, EC, FAST Occasional papers n°116.

Birkinshaw, J., Hamel, G., & Mol, M. J. (2008). Management innovation. Academy of Management Review, 33(4), 825-845. doi:10.5465/ AMR.2008.34421969

Cadwallader, S., Burke, C., Bitner, M. J., & Ostrom, A. L. (2010). Frontline employee motivation to participate in service innovation implementation. Journal of the Academy of Marketing Science, 38(2), 219-239. doi:10.1007/s11747-009-0151-3

Cooper, R. G., & de Brentani, U. (1991). New industrial financial services: What distinguishes the winner. Journal of Product Innovation Management, 8, 75-90. doi:10.1016/0737- 6782(91)90002-G

Damanpour, F., & Evan, W. M. (1984). Organizational innovation and performance: the problem of organisational lag. Administrative Science Quarterly, 29, 392-409. doi:10.2307/2393031

Damanpour, F., Walker, R. M., & Avellaneda, C. N. (2009). Combinative effects of innovation types and organizational performance: A longitudinal study of service organizations. Journal of Management Studies, 46(June), 650-675. doi:10.1111/j.1467-6486.2008.00814.x

Day, G. S., & Wensley, R. (1988). Assessing advantage: A framework for diagnostic competitive superiority. Journal of Marketing, 52, 1-20. doi:10.2307/1251261

De Jong, J., & Vermeulen, P. A. M. (2003). Organizing successful new service development. A literature review. Zoetermeer: EIM.

De Vries, E. J. (2006). Innovation in services in networks of organizations and in the distribution of services. Research Policy, 35(7), 1037-1051. doi:10.1016/j.respol.2006.05.006

Ding, X., Verma, R., & Iqbal, Z. (2007). Self-service technology and online financial service choice. International Journal of Service Industry Management, 18(3), 246-268. doi:10.1108/09564230710751479

Djellal, F., & Gallouj, F. (2005). Mapping innovation dynamics in hospitals. Research Policy, 34, 817-835. doi:10.1016/j.respol.2005.04.007

Drew, S. A. W. (1994). Downsizing to improve strategic position. Management Decision, 32(1), 4-11. doi:10.1108/00251749410050624

Ettlie, J. E., & Rosenthal, S. R. (2011). Service versus manufacturing innovation. Production Innovation Management, 28, 285-299. doi: 10.1111/ j.1540-5885.2011.00797.x

Fritsch, M., & Meschede, M. (2001). Product innovation, process innovation, and size. Review of Industrial Organization, 19, 335-350. doi:10.1023/A:1011856020135

Gadrey, J., Gallouj, F., & Weinstein, O. (1995). New modes of innovation: How services benefit industry. International Journal of Service Industry Management, 6, 4-16. doi:10.1108/09564239510091321

Gallouj, F. (2002). Innovation in services and the attendant myths. Journal of Socio-Economics, 31, 137-154. doi:10.1016/S1053-5357(01)00126-3

Gallouj, F., & Weinstein, O. (1997). Innovation in services. Research Policy, 26, 537-557. doi:10.1016/S0048-7333(97)00030-9

Gilsing, V. A., & Nooteboom, B. (2005). Density and strength of ties in innovation networks, an analysis of multimedia and biotechnology. European Management Review, 2, 179-197. doi:10.1057/palgrave.emr.1500041

Hamdouch, A., & Samuelides, E. (2001). Innovations dynamics in mobile phone services in France. European Journal of Innovation Management, 4(3), 153-167. doi:10.1108/EUM0000000005670 Hamel, G. (2006). The why, what, and how of management innovation. Harvard Business Review, (February): 72-84. PMID:16485806

Han, J. K., Kim, N., & Srivastava, R. K. (1998). Market orientation and organisational performance: Is innovation a missing link? Journal of Marketing, 62, 30-45. doi:10.2307/1252285

Huberman, A. M., & Miles, M. B. (2003). Qualitative data analysis: An expanded source book. Paris, France: De Boeck University.

Kandampully, J. (2002). Innovation as the core competency of a service organisation: The role of technology, knowledge and networks. European Journal of Innovation Management, 5(1), 18-26. doi:10.1108/14601060210415144

Karmarkar, U. S. (2000). Financial service networks: Access, cost structure and competition. In

E. Melnick, P. Nayyar, M. Pinedo, & S. Seshadri (Eds.), Creating value in financial services. Kluwer. doi:10.1007/978-1-4615-4605-4_14

Langeard, E., Bateson, J. E. G., Lovelock, C. H., & Eiglier, P. (1981). Services marketing: New insights from consumers and managers. Boston, MA: Marketing Science Institute Report No. 81-104.

Lusch, R. F., & Nambisan, S. (2012). Service innovation: A service-dominant (S-D) logic perspective. Working paper, University of Arizona.

Menor, L. J., & Roth, A. V. (2006). New service development competence in retail banking: Construct development and measurement validation. Journal of Operations Management, 25(4), 825-846. doi:10.1016/j.jom.2006.07.004

Mol, M. J., & Birkinshaw, J. (2009). The sources of management innovation: When firms introduce new management practices. Journal of Business Research, 62, 1269-1280. doi:10.1016/j. jbusres.2009.01.001

Naslund, B. (1986). Financial innovations. A comparison with R&D in physical products. Stockholm, Sweden: EFI Research Paper/Report.

OECD. (2005). Promoting innovation in services. In Organisation for economic co-operation and development. OECD Publications.

Oliveira, P., & von Hippel, E. (2011). Users as service innovators: The case of banking services. Research Policy, 40, 806-818. doi:10.1016/j. respol.2011.03.009

Ordanini, A., & Parasuraman, A. (2011). Service innovation viewed through service-dominant logic lens: A conceptual framework and empirical analysis. Journal of Service Research, 14(1), 3-23. doi:10.1177/1094670510385332

Parsons, A. L. J. (1991). Building innovativeness in large U.S. corporations. Journal of Services Marketing, 5, 5-20. doi: 10.1108/EUM0000000002530

Payne, A. F., Storbacka, K., & Frow, P. (2008). Managing the co-creation of value. Journal of the Academy of Marketing Science, 36, 83-96. doi:10.1007/s11747-007-0070-0

Reidenbach, R., & Grubs, M. (1987). Developing new banking products. Englewood Cliffs, NJ: Prentice Hall.

Reidenbach, R., & Moak, D. (1986). Exploring retail bank performance and new product development: A profile of industry practice. Journal of ProductInnovation Management, 3(3), 187-194. doi:10.1111/1540-5885.330187

Roij akkers, N., Hagedoorn, J., & van Kranenburg,

H. (2005). Dual market structures and the likelihood of repeated ties-evidence from pharmaceutical biotechnology. Research Policy, 34, 235-245. doi:10.1016/j.respol.2005.01.004

Storey, C., & Easingwood, C. (1993). The impact of new product development proj ect on the success of financial services. Service Industries Journal, 13(3), 40-54. doi:10.1080/02642069300000049

Sundbo, J. (1997). Management of innovation in services. Service Industries Journal, 17(3), 432-455. doi:10.1080/02642069700000028

Sundbo, J., & Gallouj, F. (1998). Innovation in services in seven European countries. Rapport pour la Commission Europeenne, DG XII, Programme TSER, Project SI4S, July.

ENDNOTES

1 http://www.credit-agricole.com/Le-Groupe/ Presentation-du-groupe ; http://www. culturebanque.com/classement-banques- francaises-2012/

2 Specifically, Laydernier Bank offers a sponsorship system, whereby customers obtain benefits if they recommend that others open a bank account.

3 The customer deposits cheques without support from staff, then a receipt is automatically produced.

This work was previously published in International Journal of Service Science, Management, Engineering, and Technology (IJSSMET), 4(4); edited by Ghazy Assassa and Ahmad Taher Azar, pages 43-57, copyright 2013 by IGI Publishing (an imprint of IGI Global).