Chapter 56 The Royal Credit Bank Strategy and Transformation Program: The Gulf Management Strategic Planning

Khaled Hjouj

Management Consulting Executive, Canada

ABSTRACT

This case discusses a strategic planning issue related to unplanned radical change. The Royal Credit Bank is the leading and largest lending bank in the Middle East.

The bank suffered for a long time from bureaucracy, inefficiency, lack of productivity and misalignment with customers’ needs for added value services. The Royal Credit Bank was approaching a change program of a scale and depth that occurs once in most employees’ lifetime. It would transform the bank’s business and operating models, culture, and leadership, impacting virtually every part of the organization. This had profound implications across strategy, leadership, people, and systems. This case highlights the impact of implementing large programs in an outdated banking environment where the challenge is beyond finding the solution. The real challenge was to make the solution work given the environmental issues and challenges faced by the leadership team to make things happen.ORGANIZATION BACKGROUND

The Royal Credit Bank (RCB) is considered to be the largest bank in the Middle East in cash assets. Located in a GCC country, RCB is a government lending institution that provides interest-free loans to citizens. The target audience of the public who are eligible to apply for loans falls into two categories:

Small enterprises, employers, and emerging trades; to encourage them to run their own businesses independently.

Citizens with limited incomes, in order to help them overcome their financial difficulties. This category benefited from loans for social purposes like marriage, family support and renovation, in addition to vocational loans for micro project enterprises.

DOI: 10.4018/978-1-4666-6268-1.ch056

.

The bank aimed to encourage entrepreneurship for individuals and institutions in the country, support the small and medium enterprises to pass the startup phase and grow into an economy contributing organization.

The bank also aims to promote savings and thrift by individuals and institutions in the country through creating the capabilities to enable achieving this purpose.With the capacity of 800 employees, the RCB operated a capital topping $10 billion in cash assets. The bank operations were governed by the Prime Minister’s cabinet. A council of ministers headed by the Minister of Finance set the governing policies of the bank; nevertheless the Royal Monetary Agency was responsible for monitoring the bank’s operations and activities in accordance to the law and the governing and guiding principles.

Since the bank is a government institution, the aim of the bank was not for profit as much as it was to offer economic and social help to citizens and SME’s. The bank had several funds and financing sources which consisted of the following:

• The bank’s capital.

• Government deposits.

• Fees for expenses incurred by the bank in performing its functions as determined by its Board of Directors; loans for social purposes to low-income individuals shall be exempted from such fees.

• The income resulting from investing bank’s funds, balances and assets.

• Allocations or funds granted or loaned to the bank by the government.

• Loans and deposits provided by the Royal Monetary Agency and other public and private institutions and charities.

• Deposits made by the public and guaranteed by the government.

• Saving bonds.

• Securities and collaterals of various types.

• Funds or allocations offered by others as a gives or endowment.

The bank operated through a structure that typically speaks to a government agency, rather than to a commercial bank. Most of the employees are not an exact job fit; some of them have not passed high school. Some others reached a director level only because they were on the job long enough, but not because they had what it takes to do the job. Lack of governance, proper reporting, and guiding principles meant that the day to day work was painted with inefficiency, lack of productivity, bottlenecking, long trace work processes, and untraceable files.

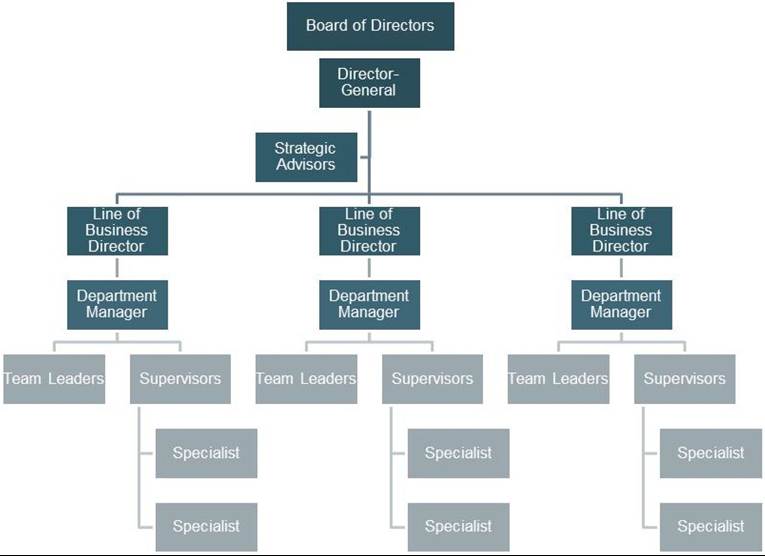

A Board of Directors is assigned by the council of ministers, the BoD should have representative members from several different agencies that assume the regulatory role (i.e. The Royal Monetary Agency), a sponsoring role (i.e. the ministry of finance), or a supervisory role such as the ministry of economy and commerce. The BoD is the supreme authority overseeing the bank’s activities and the achievement of its goals.

The bank has a Director-General, who is appointed recently pursuant to a resolution by the council of ministers upon a recommendation by the Minister of Finance. The Director-General had the following responsibilities:

• Achieve the bank’s objectives.

• Oversee the bank’s management and implement the policies and decisions adopted by the Board of Directors.

• Represent the bank before third parties.

• Collect receivables due to the bank or transferred thereto.

• Develop strategies that address strategic, tactical and operational direction of the bank.

• Sponsor development programs that enhance the bank operations and align with the strategic direction.

• Report quarterly on the bank’s performance and adherence to regulations, compliance to governance and laws.

The organization structure resembled a typical government agency structure. The existing organizational structure of a government agency in an Arab country is rooted earlier to decades back in time, a time when massive, multilayered bureaucracies were seen as the most effective and efficient approach to managing government organizations. According to Islam and El Araby (2007) some of the characteristics that define governmental organizations in the Arab countries are the closed culture, the modest education levels within the workforce, and the limited technical ability to collect, display, and transmit information. These were some of the factors that led to the creation of an opinionated, centralized management system where managers did the thinking and workers were expected to do the assigned work without contribution or question.

As far as this case is concerned, some aspects of the organizational culture may be present within individuals of an organization in the Arab countries. The following are some of those cultural aspects and how they affect directly the change that can be implemented within an organization:

• Power distance will hinder any attempt for effective change, as it contradicts with the enablers of change (Oakland and Tanner, 2006), as well as neglecting an important element of change which is people in case of mal-management (Haridimos, 2005; Islam and El Araby, 2007; Oakland and Tanner, 2006).

• Self-praise; makes it difficult for an organization to agree upon the need of a change unless there is a severe driver for change (Islam and El Araby, 2007).

• Stereotypes may delay change as an idea taken about a supplier or a raw material, may stop using it although it can help in the process of change, unless a vital change is needed (Islam and El Araby, 2007).

Reporting to the Director General (DG); each business line was headed by a director who is accountable and responsible for overseeing the business operations. Within each business line, there were several departments which were headed by managers. Department managers are supported by team leaders, supervisors and specialists.

The recently assigned DG was the main driver of any strategic advancement of the bank. He was in pursuit of enhancing the performance of the bank’s operations by all means, yet there were certain limitations that he faced and had to deal with constantly. Under the supervision of the BoD, he established a program that addresses the bank’s need for development at many levels. The aim of the program was to present the bank to the public through an internationally recognized business model that achieves the target objectives of the bank and serves the public according to the expectations of stakeholders.

When the new DG came on board, he found that the culture of the bank was dominated by a bureaucratic approach to conducting day to day business; the directorates operated in silos in separation of each other and kept boundaries held to maintain power and authority in the director’s hands.

Direc - tors demonstrated the power of authority that they had by narrowing the process progress into their signature of approval on every loan application across the bank. This resulted in many undesired bottlenecks that affected the bank’s operations and created delays in response to public demand. Lack of commitment to the bank’s success due to lack of proper controls, tools, committed management and audit authorities resulted in $200 million of untraceable loans. The bank featured on the first page of the newspaper [which newspaper?] due to poor services and response to loan applicants.When the financial crisis resonated around the world, the effects started to be felt on the ground in the country. More citizens started to knock on the doors of the bank for loans to assist them during

Figure 1. RCB’s organization structure

the difficult times. It didn’t take long before the government took immediate action to remedy the situation by announcing that the bank was granted an additional $3 billion to support a wider range of target citizens and business.

The moment this announcement made it to the media, the bank went through a life-changing experience that resulted in the series of consequences no one anticipated or expected.

SETTING THE STAGE

Arab countries in general suffer from different cultural aspects that act as obstacles to their progress. These cultural aspects are as follows:

1. Resists change (El Araby, Labib and Islam, 2006).

2. Rej ects initiatives that are not Arab originated (El Araby et. al., 2006).

3. Self-praise (Heggy, 1998a; Islam and Labib, 2007).

4. Stereotypes and Conspiracy Theory (Heggy, 1998a; Heggy, 1998b; Islam and Labib, 2007).

5. High Power Distance and High Uncertainty Avoidance (Anjard, 1998; Hofstede, 2003a; Hofstede, 2003b; Islam and Labib, 2007; Macleod and Baxter, 2001).

Organizational change mostly intends to change the organizational state from the undesirable “before” to an improved or desirable future state (Ragsdell, 2000).

In spite of the importance and costs of reaching the desirable state, many change programs fall back from meeting set targets (Oakland and Tanner, 2006).Change is a way of telling people to adopt new ideas in dealing with different aspects of their lives. One of these aspects is introducing new ways of doing things, new ways of seeing themselves, their roles and their interactions with others inside and outside the organization (Sinclair, 1994).

The change that might occur in an organization affects individuals from top managers down through the organization’s hierarchy (Almaraz, 1994). Managers have to understand the influence of change on their employees and try to solve problems that may occur as a result to this change (Sinclair, 1994). These problems may happen because change is relative and differs from one person to the other, which makes it important to analyze problems that may occur from implementing change from different points of views (Sinclaire, 1994; Ragsdell, 2000).

The effectiveness of companies operations is associated with the extent of implementation of aims, objectives, or targets or precisely with the working effects or results and usually is defined as the degree to which the companies achieve the objectives or the ability to produce desired effects or results. The effects or results in one company are expressed through the organizational performance (Al-Shammari and Hussein, 2008).

The studies and practice show that many changes that have occurred in developing and emerging countries have led to the faster diffusion of strategic planning (Al-Shammari and Hussein, 2008). On account of the problem of the implementation of strategic planning, the main focus of strategic planning literature has shifted to strategic planning effectiveness.

Many authors in their definitions of strategic planning refer to objectives and results and thus to effectiveness of strategic planning. Armstrong (1982, p.198) defines strategic planning as “an explicit process for determining the firm’s long- range objectives, procedures for generating and evaluating alternative strategies, and a system for monitoring the results of the plan when implemented.” Strategic planning consists of planning processes that are undertaken in firms to develop strategies that might contribute to performance (Tapinos, Dyson and Meadows, 2005).

Sherman, Rowley and Armandi (2006, p.10) define strategic planning as “a process that any organization engages in to critically analyze its external and internal environment; formulate a plan of action based on creating the best fit between the firm’s resources and environment opportunities; establish acceptable methods of reducing its own weaknesses and mitigating external threats; identify appropriate tactics for implementing the plan; and then establish methods of measurement that the organization will apply over time to see whether or not the tenets of the strategic plan are leading to the desired results.”

Strategic change needs initiatives and elements for this change to take place; according to (Haridimos, 2005; Islam and El Araby, 2007; Oakland and Tanner, 2006) the most important initiatives are:

• Leadership

• Define Change

• Learning

In an organizational strategic development context, culture and cultural gaps will have a great role in the issue of leadership and learning concerning change and resistance to change, as leaders deal with people and people are affected by culture.

After a difficult period during the credit collapse when economizing was the most desirable strategy, financial services firms focused on sustainability and growth. The key to growing again would often be to build a coherent and reinforcing system of differentiated capabilities - including people, knowledge, tools, and processes - throughout the value chain. The experiences of the banking unit within a large global financial services firm illustrate well the systematic effort required to succeed with a business and IT strategy and transformation program context.

The level of change has now been unprecedented in the financial industry. Delivering once-in- a-lifetime change on a large scale demands many elements such as new leadership attributes, strong governance, and superior people management to help embed a new culture. A bank without these attributes may find that the journey to the new normal is a step too far. But those that make the transition successfully will be well positioned to be among the industry’s high performers of the future.

The performance and role of banks are in the spotlight. More than ever in living memory, banks are under the close scrutiny of politicians, regulators and markets, who are all looking to the banks to deliver on their economic and social roles of enabling commerce, and providing a safe haven to channel savings into productive investment.

Fifteen years back, the bank equipped the business with a banking system that included a proprietary tailor developed banking software, mainframe, thin client user stations, connectivity network that connects the main branches to the headquarters. At that time, that was one of the advanced systems that any bank could possess.

Years passed before the bank started to look into the aging banking system and the overhead that it imposes on the bank to fund the support and maintenance of the system. Since the application was tailored and built on a proprietary code, there was not any vendor out there that could support it except for the company that developed it in the first place. After several years the application was no longer supported in the market, so the bank had to sign a support contract with the vendor to establish a special unit to support this system specifically with a cost of millions of dollars.

The bank did not care to establish an internal capacity for the IT and kept relying solely on the vendor support to manage the IT needs of the bank. The bank leadership didn’t pay attention to this situation for years, although the situation was complicated yet it did not impact the slow pace, low productivity nature of the daily work that the bank employees enjoyed. The silos structure helped in feeding this situation with more complexity due to the fact that the process was a mix of automated and human processed which resulted in the inability to trace a certain loan application file across the process end to end.

The IT department was a small department consisting of sixteen government employees, most of whom were not IT related in specialization. Many had an educational background related to social studies such as history, arts, and basic high school, secretarial diplomas and even religious studies. The policy of the government for hiring employees did not dictate the alignment of specialization of the employee to the target job; many jobs were filled with incompetent and unqualified employees. This resulted in a very weak ability of the department to come any close to reality with advancing the IT systems in the bank, and total reliability on the support vendor which in return placed two employees (50 years and above) in the bank on a full time basis, to support the system and keep the lights on.

The department did not have a director. The leadership of the department consisted of a manager and an experienced independent consultant who helped in leading the day-to-day activities of the team. Neither of them were in a position to drive a strategic development direction or establish added value projects that could collectively put the department back on the right track.

An outdated system, an incompetent team, lack of organizational structure, motivation, direction, leadership and capabilities to do the job properly, were the characteristics of the IT department at RCB. The RCB leadership did not pay attention to the fact that the IT situation of the bank had turned into a time bomb. Despite the fact that there were untraceable files, loans, cases, data in the system and on paper files as well, it did not matter much since the overall mission of the bank was not for profit, given a government driven bureaucratic culture, with absence of the proper audit authority that looks into regulatory compliance in a proper manner. The bank did not realize how serious the situation was until the media announcement of the additional funds that the government provided.

CASE DESCRIPTION

Although the bank was a government institution, it had a huge impact on the private banking and financial services sector. Private banks lost millions in loan business due to what RCB offered in the market, the ceiling reached to supporting businesses up to $3 million, and individuals up to $20 thousand with a 0% interest rate.

The government announcement drew the attention of those who did not think of RCB as a source of financing, considering the financial crisis impact. Everyone started to think of RCB as a gold mine. Shortly after the announcement, the lineup was double the length since the day before and it kept increasing, the bank had to temporarily close its doors and organize the crowds to be able to accommodate them.

The DG was on vacation out of the country at that time, the directors tried their best to contain the situation and keep their calm. That was an unprecedented situation that they experienced. Yet they knew that there will be consequences if they were not up to the level of public expectation of bank’s overall performance.

The Blackout

Right in the middle of all of this chaos, the time had come for something that no one thought would happen. The bank’s network was hacked. The system was brought down, and no one was able to access any information or manage any system files. It was a big hit right in the middle of a crucial time, when the bank was put in front of the public as a source of help. The bank failed to deal with the situation completely.

The hit was very hard; the network penetration was deep and carefully crafted. The department manager at that time and the independent consultant took charge, and tried to fix the issue by calling in all possible sources of help to resolve the situation. However, it took two business days to bring the system up and running again. The two full time support subject matter experts who were planted in the IT department by the banking system vendor; were completely useless because all they knew was related to the code of the system but not comprehensive enough to help in resolving a situation like this, especially that what they know about the system was already outdated considering the new emerging technologies that come out every day.

On the Hot Plate

The DG interrupted his vacation and flew back into the country to manage the situation closely. But it was too late. Right upon his arrival, the bank made it to the front page of all the newspapers. The tension was high and the situation was very sensitive. The bank’s doors remained closed to the public, but other doors were open by other agencies that paid attention to the situation and started to take precautionary action towards getting involved at the right level.

The DG called for an emergency meeting of the BoD, preceded by a meeting with the bank directors for a briefing on the situation and readiness to business continuity action plan. To the DG’s disappointment, nothing was in place to sustain the business continuity and operations. Stepping in the boardroom, the DG was trying to put together something that can save face and could be reasonably discussed as an emergency resolution of the situation.

The discussion in the boardroom was heated and lacked rational thinking in the beginning. However the DG managed to drive the meeting by presenting facts and concluding impacts and remedial actions.Then he presented a recommended fast track approach to address the situation with high level steps that should put things back on the right track. Despite the vulnerability of the situation which would continue to threaten the bank, the accelerated approach that the DG adopted should have helped in fast tracking the solution of the problem. Finally the BoD agreed that it was time to resume operations and face reality with their current situation that they had to handle, trying to avoid getting into the same situation as much as possible.

Defining the Problem

The DG realized that the problem was not only the technology issues at hand; it was mainly the reason why the situation deteriorated to a level where this problem surfaced. The culture of the bank was driving the whole situation, not realizing the importance of the bank’s mission and its impact on the beneficiaries, resulted in an unacceptable organizational behavior.

Some of the problems that were on the surface were due to the aging workforce employed at the bank. In addition to the impact of the isolated unorganized directorates that created bottlenecks, and caused loss of value, due to the employees’ incompetence, and lack of sense of responsibility. Some of that was inherited by the government system; some other was created by the bank’s employees.

The failure to introduce proper banking business systems in the bank years ago was a major issue that the DG was trying to resolve by immediately addressing and eliminating out of the picture. The DG’s understanding of the importance of the revitalization of the IT systems in the bank was unquestionable yet he needed to make sure that he was adopting the right direction to address this part of the problem.

The DG realized that in order for him to create a significant impact on the culture of the bank, he had to make some difficult decisions and introduce some hard changes that help in reshaping the bank’s behavior towards business and clients as well. He was also determined to address this problem through adopting a top down approach, optimistically hoping that the new adopted direction should help in presenting solutions and help further in carrying the change forward.

The Advisors

The DG called for a meeting with the IT leadership to discuss the situation and set immediate next steps towards situation resolution. The IT manager and the experienced consultant were not sure how to handle the situation; consequently they agreed that they needed experienced professional help to assist leading the efforts to address the problem. The DG assigned the experienced independent consultant as an acting department director and assigned the manager as a deputy director. At that meeting they agreed that they will bring an experienced consulting firm to help in putting together a plan and implement a solution that saves the bank from the current situation.

The DG did not stop at that point; he also managed to assign one of the highly experienced directors in charge of an initiative that should address the bank’s operating model as a whole. The DG’s vision was to introduce a completely new business and IT operating model that addresses all the issues and puts the bank on the right track in providing excellent services to the public and acts as a main player in the market.

The highly qualified director assumed the role of program manager, collaborating closely with the acting IT director and his deputy to act on the matter, and immediately invited several advisory firms to qualify and bid for this engagement. It didn’t take long before the right firm was selected to partner with the bank towards planning, designing, validating and executing the selected solution in the bank.

Highly qualified subject matter advisors were injected into the bank to support several aspects, but mainly to conduct a current state assessment and help defining the situation as it exists before and after the incident. IT advisors, deep banking industry advisors and experienced project and program managers were plugged to put together an overall approach to create a transformational program that should save the business and enable IT to become a service center.

The Program

Between the program leadership from the bank side and the advisors side, they were able to define a program that addressed three immediate needs:

Phase 1: Immediate projects (quick wins) to resolve the critical IT and business issues.

Phase 2: Short term initiatives (realized in one year) to introduce major change in certain pain areas that impact customer service and operations performance.

Phase 3: Mid to long term initiatives (realized in 3 - 5 years) to address transformational aspects and build capabilities needed to introduce new business and IT functions.

Phase 1 was set to target issues related to process effectiveness and efficiency performance issues. The initiative identified the need to acquire IT systems, banking solutions, and technology infrastructure required to support the overlaying architecture of IT solution stack. On the business side, it targeted designing IT enabled processes that set the direction for the business through a fully automated customer service end-to-end. Another stream was set to address the bank organization structure. This stream aimed to define business functions, governance structure, performance measures and roles and responsibilities in accordance to the target set of capabilities that the bank was planning to operate.

Phase 2 was designed to start as soon as phase I began. It targeted developing aligned business and IT strategic plans that addressed the tactical and operational aspects of the bank. The objective of phase II was to resolve the issues of the day to day operations, and implement an integrated framework for the business that would be enabled by the IT capabilities. Implementing the right tools, processes, and technology solutions, the bank should be able to overcome the issues facing business such as the untraceable loans, poor service offering at the front desk, human dependent processes, and vulnerable technology environment.

Phase 3 was an end to the transformation program, starting midway of phase II, and continuing until the end of the program. It was designed to address the human skills and capabilities, business and technology integration, human capital training and education. The other aspect of this phase was addressing the long term strategic planning, without being under the stress of firefighting mode that the bank was operating through at that time.

CURRENT CHALLENGES FACING THE ORGANIZATION

The program aimed to immediately present solutions to existing problems that kept the bank behind for so long. The organization culture, group dynamics affected by the existing silos, interaction with change management, organizational structure change and its impact on the new direction; finally the leadership and communication style that the bank chose to adopt and continue to practice along the way.

When the Rubber Hits the Road

The program leadership team consisting of the BoD, the director general, the program director, the IT acting director and his deputy, selected members of the business directors and the team of experienced advisors were all focusing on kicking off the program as soon as possible.

In a matter of a couple of weeks, the program plans, structure, scope, targets, milestones, projects outcomes and phase alignment were set. The DG wanted to show immediate progress on the ground internally to the stakeholders, externally to the government agencies involved and to the public who was closely watching for improved results on a daily basis. The program kick-off was announced in the media and had a lot of attention and comments from those who were anticipating this critical move to be either the end or the start of a new era in the bank’s business life.

The program leadership team knew that they are under the microscope and that they had no room for delayed results or unacceptable program outcomes. The pressure was high, yet it was a source of motivation to everyone on the program. Most of the bank directors and leadership team were invited to the kick-off meeting. The anticipation filled the room with tension, and many questions were in most of the attendees’ minds, questioning how things will come around. It was not long before the DG started the introductory speech to announce the program objectives, scope and timelines. In addition to explaining the benefits expected to be delivered out of the program,the DG explained the role of directors in this new process and how cooperative they should be to help the bank advance to the next level and become recognized for its high standards of banking services.

On the Way

The program started with full steam pressure. Everyone was racing against time to show some difference in the shortest time possible. The IT department team was so excited about the journey, however some of them were not that excited to cooperate. This was an expected reaction from employees who are incompetent to cope with the fast pace of the projects, and the daily work that they had to handle. On the business side, the situation was not as promising as the IT side. Most of the employees were close to retirement. They were used to using conventional ways of doing business, totally dependent on manual work. They had the least clue of how to use technology to conduct business. This symptom extended to the department managers and business line directors as well, which created a situation that was not accounted for at all. Those who suffered these symptoms created a wave of aggressive resistance to the program as a whole.

Three months into the program, the program team was working hard on gathering requirements, designing future state, designing technology and business architecture, establishing new functions and capabilities. The overall progress was going well and according to the plan, especially that the team was working in the background in separation from the operational layer of the bank. As soon as the interaction reached to the operational layer, the resistance surfaced, and the progress slowed down. The DG was not surprised to learn what was going on. He understood the bank culture very well, and he was anticipating that issues will come along the way. But, he was mainly focusing on showing progress in early stages of the program, which he achieved and was able to mobilize a successful program plan with the involvement of a highly experienced consulting firm.

The program leadership team met to discuss the issues that they were facing, and recommend effective corrective actions and remedial reaction. The advisors team suggested several risk mitigating actions. They also promoted a couple of side streams that focused on immediate response to the issues they were facing. The DG thought that more should be done to help save the effort that was invested and yet to be devoted to complete the program down the road.

The Exit Criteria

The DG worked closely with selected directors and experienced consultants on offering a workable solution that met the interest of the bank leadership direction as well as the employees who were fearing the unknown and what was going to happen to them.

The DG prepared an exit criteria package for those who chose to opt out of the transformation program. The DG’s team designed a lucrative early retirement package that applied to all employees of forty-five years and above. Another option was also offered to employees between forty-five and fifty-five years old to encourage employees to choose for themselves. The second option was to be reassigned to another government agency based on their qualifications and fit in a six month window from accepting the offer.

The two options had to be approved by the BoD and the council of ministers, which was not an easy mission. But the DG used the right cards to facilitate a very successful meeting with the Board of Directors and gain their agreement to move ahead with the approval from the council of ministers. Approximately two weeks later, the two options were presented to the council of ministers. Following a very long discussion and debate about the critical situation the bank is going through, both options were whole heartedly approved. This provided the program leadership team a huge motivational factor to advance further in confidence and achieve more success in meeting the program objectives.

The Transformation

The IT department dug deep into the ground to lay a very solid foundation for a strong future of technology enabled banking services. The direction was to make the IT arm of the bank an enabler of the business at all levels, and promote continuous technology advancement and development. The architectural foundations of the new enterprise banking system were laid down and the selection of a new banking solution started. A fully fledged service oriented organization structure was established to support the new direction, as well as an internationally adopted and recognized set of best practices which were implemented to enable the IT team to operate efficiently and serve the business productively.

The advisors formulated a five year IT and business strategic direction and plan that was aligned with the overall direction of the bank. The strategic plan addressed most of the pain points that the bank was suffering from; it targeted getting rid of the legacy systems, processes, and organizational negative behavior in the shortest time possible (1 to 3 years down the road). A Project Management Office (PMO) department was established to drive and supervise all the projects that would be implemented. An HR training facility was out-sourced to offer continuous training to employees. This initiative targeted enhancing the employees’ soft and hard skills, core business knowledge, business capabilities and work ethics as well.

The ship was sailing in the right direction, and milestones were met with tolerance to time slippage considering the issues that the program leadership team had to handle and navigate. Nearly one year down the road, one hundred-fifty employees opted for one of the options for the exit criteria; two hundred-fifty fresh blood competent employees were hired to support and operate the new capabilities that the bank established around the business and IT. It was about time to announce the outcomes of the strategic planning project and the organizational restructuring project as well.

No Turning Back

A date was set for the first year milestones announcement. The anticipation was mounting and the anxiety was overwhelming the bank employees. They did not know how their future would be shaped and what to expect from that change. Although the program management was closely managing the change through regular announcements, newsletters, integration workshops, team building and intensive training programs targeting the immediately affected employees, the new structure and direction of the bank carried many unrevealed details that would affect everyone’s life.

On the day of the announcement, the leadership of the bank was flown to the headquarters from around the country. The boardroom was stacked with nearly sixty-five management team

members of different levels and business lines. The DG directed the advisors to lead the session and announce the changes, while he commented on the results and provided some direction on the next steps. The Board of Directors agreed to attend later in the session, anticipating that there might be some discussion that they did not want to be part of. Last but not least, the program leadership sat among the audience and facilitated some positive comments and questions, enabling the announcements to be given smoothly. The advisors started the session with a summary of achievements, current status of the program and future targets. The advisors diligently explained the strategy components, opportunities, initiatives, business case and roadmap. Then they turned to the new organization structure announcement. They attentively explained the new structure of business lines, shared services, lines of integration across the bank, governance structure, methods of application, target performance measures and finally the organizational structure that would take effect within thirty days.

All eyes turned to the group of managers and directors - totaling 10 - who immediately knew that the value of their signature on file was blown away. It was clear to the attendees that the new structure directly affected their roles, and set them for elimination from the new organization structure. They denounced the new direction accusing the team of being unfair and unappreciative of their dedicated service to the bank. Apparently a leak happened before the session, and they came prepared to set the meeting on fire. However, the program leadership team was also very well prepared, supported by the DG and the BoD, and the DG immediately took charge of the situation. He explained to the audience the impact on the business if the current course of business as usual continued to evolve. The bureaucratic behavior of the directors, managers and others would put the bank in a worse situation than before. If someone chose not to cooperate, they would still be maintained as employees of the bank, yet they would be placed in a position newly created to accommodate those who needed time to adapt. The position was called “business process advisor,” a role that was completely stripped from any authority or power; and the employee was to be informed on a need to know basis.

The DG came with a ready-made list of employees who would be moved into that position. He announced the names in the meeting and offered the two exit criteria options for those who chose to object and refused to move as directed. Such a life changing stand! It was more of a Mexican standoff with big business decision guns being pulled in a crowded room. Silence suddenly filled the room before the DG said: “We are all gathered here to move ahead, we don’t have the choice of going back, and there is no turning back. Either you accept to sail ahead with us or you make the choice to stay on the safe shore that I just offered.”

SOLUTIONS AND RECOMMENDATIONS

As of that day, nothing has stayed the same. The bank advanced with the transformation program as planned and managed to achieve most of the sought after benefits. The bank certainly continued to serve the public with the highest degree of dedication and commitment to quality banking services. It was the bank’s mission to make people’s life easier, which the leadership translated into reality with their assurance of advancing and serving the public as expected of them, considering the acts presented about the bank, the industry dynamics, the economic situation and the internal challenges. The overall situation could have been mitigated years ago if the management of the bank paid attention to staying on course with the advancement ofthe business services offering and technology driving forces that shape the business behavior in a certain industry.

The impact of a business and IT strategy with transformation programs is huge when it targets a highly visible bank in the financial industry. The leadership of the institution should always be aware of the consequences if they make it to the front page with a scandal or an undesired situation.

A better rigorous approach should be brought into the process of establishing transformational programs, intensive planning, impact assessment, organizational dynamics, politics, business performance, scope of change, timelines and peoples readiness to produce results, interaction with external parties, and last but not least working as one unit to achieve a defined target.

Change is a permanent phenomenon. It is necessary due to external forces like technology, systems, and social changes interacting with the internal variables of the organization. According to Hovemeyer (1993), to implement change, Kurt Lewin’s model of unfreezing the situation, implementing a change and refreezing could have been put into action. Individual, group and organizational changes take place continuously. Individual change refers to change in attitude, perception and also acquiring new skills to cope up with external environment (Hovemeyer, 1993).

Watson (2002) argued that change is structured when it is planned, and it is unstructured when change is implemented as a reaction to a particular situation. There is great resistance to change because of the fear of the unknown. Therefore, the bank employees must be educated, trained, made party to change and the benefits of change must be divided between the employees and the organization. It is the sensitive handling of employees’ emotions making them psychologically ready to implement change that will ultimately work for better success.

Fear must be removed from people’s minds. Change must be taken in the positive manner for the growth of the organization. It is difficult to predict which strategy will succeed in implementing the change. Efficient communication, educating the people about impending change, participation, and active involvement and last but not the least sharing the benefits of change with people is the essential requirement for overcoming resistance to change (Coch and French, 1948).

Barney and Griffin (1992) discussed that the growth oriented organizations have to study the internal and external environment while making suitable changes. Introduction of information technology, knowledge revolution, technology advancement, competition due to global market scenario, high expectations of customers due to social revolution, and last but not least, the work pressure an employee is facing has made it necessary to carry out organizational development in a planned way.

It is imperative to improve organizational culture, redesign and redefine jobs and accord full freedom of action and autonomy to workers so that the organization is always a learning organization. Organization development therefore is a planned process of change in an organization’s culture through utilization of behavioral science technologies (Watson, 2002).

However, as much as it may sound as a cliche, it is still an inescapable fact that people are the main resource of any organization. Without its members, an organization is nothing. An organization is only as good as the people who work within the group. In today’s increasingly global and competitive environment the effective management of people is even more important for organizational survival and success. Accordingly, the underlying theme of this case has been the impact of implementing business and IT strategy with transformation programs and the importance of the role of management as an integrating activity. It has been concerned with interactions among the structure and operation of organizations, the process of management and the behavior of people at work.

The nature of organizational behavior and the practice of management should not be considered in a vacuum but within an organizational context and environment. In this case we discussed that other external factors could also affect the internal behavior and cause change of direction of business. It is imperative to understand that not seeing the future could be a main source of fear of the present.

REFERENCES

Al-Shammari, H., & Hussein, A. R. T. (2007). Strategic planning-firm performance linkage: Empirical investigation from an emergent market perspective. Advanced in Competitiveness Research, 15(1-2), 15-26.

Al-Shammari, H., & Hussein, A. R. T. (2008). Strategic planning in emergent market organizations: Empirical investigation. International Journal of Commerce and Management, 18(1), 47-59. doi:10.1108/10569210810871489

Almaraz, J. (1994). Quality management and the process of change. Journal of Organizational Change Management, 7(2), 6-14. doi:10.1108/09534819410056096

Anjard, R. (1998). Total quality management: Key concepts. The TQM Magazine, 47(7), 238-247.

Armstrong, J. S. (1982). The value of formal planning for strategic decisions: Review of empirical research. Strategic Management Journal, 3(3), 197-211. doi:10.1002/smj.4250030303

Barney, J. B., & Griffin, R. W. (1992). The management of organizations: Structure, strategy and behavior. Boston: Houghton Mifflin Co.

Bernard, M., & Stogdill. (1990). Hand book of leadership (3rd ed.). New York: Free Press.

Coch, L., & French, J. R. P. Jr. (1948). Overcoming resistance to change. In Reading in Social Psychology. New York: Holt, Rinehart and Winston, Inc.

Divis, K. (1977). Human behaviour at work. New Delhi, India: McGraw-Hill Publishing Co. Ltd.

El Araby, S. A., Labib, A. A., & Islam, A. E. (2006). Performance measurement: A general review. Paper presented at the 9th International QMOD (Quality Management and Organisational) Conference. Liverpool, UK.

Haridimos, T. (2005). Afterword: Why language matters in the analysis of organizational change. Journal of Organizational Change Management, 18(1), 96-104. doi:10.1108/09534810510579878

Heggy, T. (1998a). The Arab mind. Retrieved April 25,2013 from http ://www.tarek-heggy. com/

Heggy, T. (1998b). The phobia of cultural invasion. Retrieved April 25, 2013 from http://www. tarek-heggy.com/

Hofstede, G. (2003a). Geert Hofstede cultural dimensions for the Arab countries. Retrieved April 20, 2013 from http://www.geert-hofstede. com/hofstede_arab_world.shtml

Hofstede, G. (2003b). Hofstede’s dimension of culture scales. Retrieved April 20, 2013 from http://www.geert-hofstede.com

Hovemeyer, V. A. (1993). How effective is your team? Training & Development, 68.

Islam, A. E., & El-Araby, S. A. (2007, July). Change management in Arab countries- A general review. Paper presented in the 8th International Conference of Quality Managers (8th ICQM), Quality Managers and the Management Challenges in the 21st Century, Teheran, Iran.

Islam, A. E., & Labib, A. A. (2007). Performance measurement and culture in Arab countries. Paper presented at the 1st Annual Conference, Total Quality Management in Service Industries (TQMISI). Alexandria, Egypt.

Macleod, A., & B axter, L. (2001). The contribution of business excellence models in restoring failed improvement initiatives. European Management Journal, 14(4), 392-403. doi:10.1016/S0263- 2373(01)00042-1

Oakland, J. S., & Tanner, S. J. (2006). A new framework for managing change. Paper presented in the 9th QMOD Conference, Creativity, Governance and Transformation - the Building Blocks for Excellence. Liverpool, UK.

Ragsdell, G. (2000). Engineering a paradigm shift? A holistic approach to organisational change management. Journal of Organizational Change Management, 13(2), 104-120. doi:10.1108/09534810010321436

Sherman, H., Rowley, D. J., & Armandi, B. R. (2006). Strategic management: An organization change approach. Lanham, MD: University Press of America.

Sinclair, J. (1994). Reacting to what? Journal of Organizational Change Management, 7(5), 32-40. doi:10.1108/09534819410068895

Tapinos, E., Dyson, R. G., & Meadows, M. (2005). The impact of performance measurement in strategic planning. International Journal of Productivity and Performance Management, 54(5/6), 370-384. doi:10.1108/17410400510604539

Watson, T. J. (2002). Organising and managing work: Organisational, managerial and strategic behaviour in theory and practice. New York: Financial Times Prentice Hall.

KEY TERMS AND DEFINITIONS

BoD: Board of Directors.

Change Management: Is an approach to managing the transition to a target future state of individuals, teams, and organizations.

DG: Director-General.

GCC: Gulf Cooperating Council.

RCB: Royal Credit Bank.

Strategic Planning: Is a structured process of defining an organization strategy, or direction, and making informed decisions on managing its resources to pursue this strategy and achieve the desired goals.

Transformation Strategy: Is about adopting the organizational strategic programs and change culture, to formulate fundamental improvements in how business is conducted in order to industry and market evolution.

This work was previously published in Cases on Management and Organizational Behavior in an Arab Context, edited by Grace C. Khoury and Maria C. Khoury, pages 316-336, copyright 2014 by Business Science Reference (an imprint of IGI Global).