FORMULATION OF HYPOTHESES

• Perceived Usefulness (PU): Davis (1989) defines PU as the degree to which a person believes that using a particular system would enhance his or her job performance. From the technology acceptance model proposed by Davis (1989), it is evident that PU is a significant factor affecting acceptance of an information system.

Further, from the prior studies on internet and internet banking, perceived usefulness has been found to be an important determinant in the adoption of internet banking services. So, in the context of internet banking, perceived usefulness may be explained as performing the banking tasks anytime and from any location. Therefore, the following hypothesis has been tested:H1: Perceived usefulness will have a positive effect on the intention to use internet banking.

• Perceived Ease of Use (PEOU): Davis (1989) defines PEOU as the degree to which a person believes that using a system would be free of effort. From the technology acceptance model, PEOU is a major factor which affects the acceptance of information system (Davis et al., 1989). In the context of internet banking, perceived ease of use may be explained as using a system which is perceived to be easier to use than the conventional one. A significant number of studies suggested that perceived ease of use influences intention (Agarwal & Prasad, 1997). Thus, the following hypothesis has been proposed: H2: Perceived ease of use will have a positive effect on the behavioral intention to use internet banking.

• Perceived Risk: Perceived risk, in the context of internet banking may be associated with the financial loss as a result of using the services or with the electronic delivery channel. Black et al. (2001) have analyzed perceived risk in terms of risk of error and the level of security. A large number of studies have found that perceived risk is one of the major factors affecting user adoption of internet banking.

Thus, the following hypothesis has been formulated: H3: Perceived risk will have a negative effect on the behavioral intention to use internet banking.Relative Advantage: Rogers (1962) defines relative advantage as the degree to which an innovation is perceived as being better than the idea it supersedes. Relative advantage in the context of internet banking may be explained as allowing customers to access their bank accounts from any location and at any time of the day in contrary to the traditional banking. Tornatzky et al. (1982) find relative advantage to be an important factor in determining the adoption of new innovations. Also, a large number of studies have found relative advantage as a crucial factor in the adoption of internet banking. This leads to the following hypothesis:

H4: Relative advantage will have a positive effect on the behavioural intention to use internet banking.

Trialability: According to Rogers (1983), consumers might adopt an innovation if they are given the opportunity to try the innovation. Gerrard et al. (2003) define trialability as the degree to which an innovation may be experimented with on a limited basis. In the context of internet banking, trialability can be viewed as the ability to access one’s own account and carrying out the banking transactions on a trial basis preferably at bank premises with the help of bank personnel who will be able to demonstrate how it works and the benefits it offers. This reduces the fear of adopting internet banking services and

encourage the potential customers to adopt it. Thus, the following hypothesis has been tested:

H5: Trialability will have a positive effect on behavioral intention to adopt internet banking

• Conspicuousness: Conspicuousness can be defined as high visibility. It can be viewed as the coverage of internet banking in the media i.e attracting the attention of the society. With such an exposure of internet banking, potential customers could gain knowledge about the services and its benefits.

If such information about the services and benefits can be shared with friends and colleagues, then there is a chance of adoption. Thus, the following hypothesis has been tested:H6: Conspicuousness will have a positive effect on behavioral intention to adopt internet banking.

DATA COLLECTION

The data for this study has been collected by means of a survey conducted in a metropolitan city in India, with the help of a questionnaire. Filled in questionnaires were obtained from three different locations i.e., colleges, corporate offices and banks. This results in a sample that is well distributed in terms of demographics. A total of 450 questionnaire forms were delivered to the customers of private sector banks, out of which 347 filled in forms were received giving a response rate of 77 percent. The questionnaire consists of questions that are related to demographic information, the possible factors affecting the acceptance of internet banking and the use of internet banking services.

The questionnaire has been developed and tested with a focus group consisting of banking professionals. The focus group verified that the hypotheses developed might be the affective factors in explaining the adoption of internet banking. Based on the feedback from the focus group, the questionnaire was modified. Before proceeding with the main survey, the questionnaire was validated through pre-testing. This resulted in an error-free final questionnaire. A five point Likert scale ranging from strongly agree to strongly disagree is used as a basis to know the respondent’s views. The intention to use internet banking services has been chosen as the dependent variable in the model.

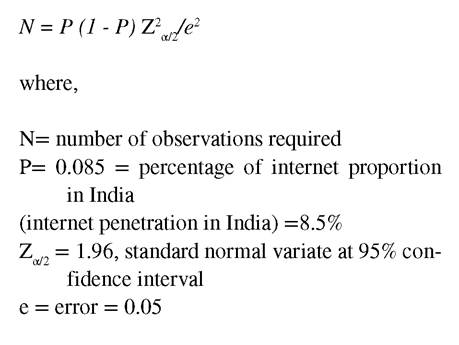

The sample size is calculated using the following general formula.

Thus, the sample required has been obtained as 119. In the actual study, the sample size is chosen as almost thrice the required sample size so that the resultant sample represents the entire population.