RESULTS AND ANALYSES

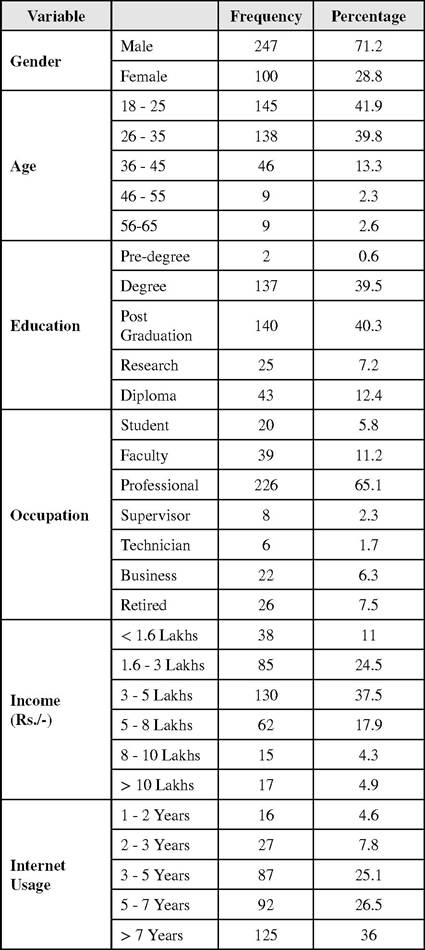

The data was analysed using SPSS version 16.0 (statistical package for social sciences). The demographic profile of the respondents is shown in Table 1.

From Table 1, it is found that 41.9% of the respondents are in the age group 26-35 years, 71.2% of the respondents are male, 40.3% of the respondents are post graduates, 65.1% of the respondents are professionals/officers, 37.5% ofthe

Table 1.

Characteristics of the sample

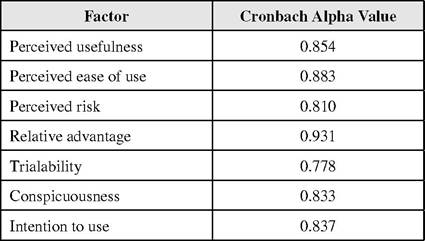

the value of Cronbach’s alpha to be at least 0.7 to show high internal consistency. Cronbach’s alpha values of the factors are shown in Table 2.

In the present study, the Cronbach’s alpha values of all the factors have been found to be higher than the recommended value which shows a high internal consistency of the measures.

A confirmatory factor analysis has been conducted on the items comprising perceived usefulness, perceived ease of use, perceived risk, relative advantage, trialability, conspicuousness and intention to use. The Kaiser criteria of eigen values greater than 1 has been used to determine the initial number of factors to retain. The Kaiser- Meyer-Olkin (KMO) measure was 0.833. From the Bartlett’s sphericity test, the value of chi-square is found to be 7251 with a significance of 0.000. Hence, the constructs have been found to be valid.

Multi-regression analyses are performed to test the hypotheses and to examine the associations among the constructs. The results have been reported in Table 3, Table 4, and Table 5.

Table 2. Cronbach alpha values

respondents are in the income range Rs.3 Lakhs - 5 Lakhs and 36% of the respondents have been using internet for more than 7 years.

Reliability Analysis has been carried out to check the internal consistency of items.

Construct reliability has been analysed by calculating the values ofCronbach’s alpha. Nunnally (1978) recommendsTable 3. Regression model

| Model | R2 | Adjusted R2 | Std. Error of the Estimate |

| 1 | 0.645 | 0.639 | 0.66406 |

Independent Variables: Conspicuousness, Perceived Risk,

Perceived ease of use, Trialabilty,

Relative advantage, Perceived usefulness, Dependent Variable: Intention to use

Table 4. ANOVA result

| Model | Sum of Squares | df | Mean Square | F | Sig. |

| Regression | 272.766 | 6 | 45.461 | 103.092 | 0.000 |

| Residual | 149.932 | 340 | 0.441 | ||

| Total | 422.698 | 346 |

Table 5. Regression result

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | |

| B | Std. Error | Beta | |||

| (Constant) | 0.070 | 0.268 | 0.263 | 0.793 | |

| Perceived usefulness | 0.504 | 0.059 | 0.423 | 8.490 | 0.000 |

| Perceived ease of use | -0.084 | 0.040 | -0.069 | -2.126 | 0.034 |

| Perceived risk | -0.044 | 0.042 | -0.034 | -1.030 | 0.304 |

| Relative advantage | 0.261 | 0.061 | 0.229 | 4.248 | 0.000 |

| Trialability | -0.031 | 0.048 | -0.021 | -0.638 | 0.524 |

| Conspicuousness | 0.277 | 0.057 | 0.248 | 4.887 | 0.000 |

A linear multiple regression analysis has been carried out on the proposed model, where intention to use is the dependent variable and perceived usefulness, perceived ease of use, perceived risk, relative advantage, trialability and conspicuousness are the independent variables. From the ANOVA result shown in Table 4, it is evident that the model applied is significantly good enough in predicting the outcome variable.

From the results of regression analysis shown in Table 3 it is found that the coefficient of determination R2 is 0.645. This means that 64.5% of the variability in the dependent variable (i.e intention to use internet banking) can be explained by the independent variables such as perceived usefulness, perceived ease of use, perceived risk, relative advantage, trialability and conspicuousness. The R2 value and the adjusted R2 value are very close which implies that the model includes only the factors that are significant, i.e., the model is not over specified.Hence, the multiple regression equation is:

Intention to use internet banking services = 0.070 + 0.504*Perceived usefulness - 0.084 * Perceived ease of use - 0.044*Perceived risk + 0.261*Relative advantage -0.031*Trialability + 0.277*Conspicuousness

According to the hypothesis H1, perceived usefulness will have a positive effect on the intention to use internet banking. From Table 5, perceived usefulness is found to be statistically significant at 0.05 level (β = 0.423, p = 0.000). Thus, the hypothesis H1 has been supported. This suggests that the bank customers perceive internet banking to be useful.

The hypothesis H2 states that perceived ease of use will have a positive effect on the behavioral intention to use internet banking. Table 5 reveals that perceived ease of use is found to be statistically significant at 0.05 level (β = -0.069, p = 0.034). Thus, the hypothesis H2 is supported. This suggests that the bank customers perceive internet banking as easy to use.

According to the hypothesis H3, perceived risk will have a negative effect on the behavioral intention to use internet banking. It is found from Table 5 that perceived risk is statistically insignificant at 0.05 level (β = -0.034, p = 0.304). Thus, the Hypothesis H3 is negated. This means that the bank customers are not finding internet banking transactions to be risky. This may be because of the efforts taken by banks in making the internet transaction more secure.

The hypothesis H4 states that relative advantage will have a positive effect on the behavioural intention to use internet banking. The findings from Table 5 show that relative advantage is statistically significant at 0.05 level (β = 0.229, p = 0.000). Thus, the hypothesis H4 is supported. This means that bank customers are perceiving internet transactions to be relatively advantageous than the traditional banking.

Hypothesis H5 states that trialability will have a positive effect on behavioral intention to adopt internet banking. It is observed from Table 5 that trialability is statistically insignificant at 0.05 level (β = -0.021, p = 0.524). H5 is therefore negated. The possible reason for the failure of the hypothesis is lack of support from the banks to offer the services on a trial basis.

The hypothesis H6 states that conspicuousness will have a positive effect on behavioral intention to adopt internet banking. Table 5 reveals that conspicuousness is found to be statistically significant at 0.05 level (β = 0.248, p = 0.000). Thus, the hypothesis H6 is supported. This means that the higher the visibilty of the banks services in the public media, the higher would be the rate of adoption.

In summary, out of the six hypotheses, four were found to be statistically significant in this empirical study. Rejection of hypothesis H3 reveals that perceived risk has a positive effect on internet banking. Hence, only one hypothesis H5 is rejected.

More on the topic RESULTS AND ANALYSES:

- Model variations and sensivity analysis

- The Netherlands and the UK: The Witteveen Reports and their contradictory results

- REVIEW OF FORENSIC ASSESSMENT INSTRUMENTS

- BACKGROUND AND DEFINITIONS

- Contents

- Risks and sources of policy failure

- FIVE COMPONENTS OF LEGAL COMPETENCIES

- PREFACE

- Oman

- CASE 145: Periods of Gestation