INTRODUCTION

Nowadays, online trading is regarded as the most potential tool for companies, which will mean a revolution in both the buying habits of consumers and the formulas of relationship between consumers and companies (Sharma and Sheth, 2004).

Currently, over 90% of total OECD firms have access to the Internet. Although in Spain it is slightly lower (86.6%), the trend in recent years shows signs of an approximation to the average OECD countries (AMETIC, 2010).Even though it is true that the use of the Internet will be more or less intensive depending on the sector and size of the company, there are certain sectors, such as finance, tourism and the media, where the Internet has a major presence (Badia, 2002) and shows a value creation (Luque

DOI: 10.4018/978-1-4666-6268-1.ch017

.

and Castaneda, 2007) as well as the generation of significant investments (AMETIC, 2012). In these sectors, as claimed by Rainer and Turban (2009), the Internet is considered to be a revolutionary tool that contributes to change and ways to do business. In this sense, financial institutions have modified their business models, paying special attention to e-Banking.

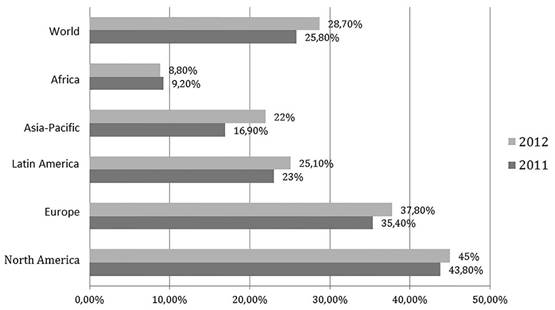

Generally speaking, the use of e-Banking is increasing annually, and at the present moment 28.7% of Internet users make financial transactions online (comScore, 2012) with significant growth prospects (see Figure 1).

In regards to Spain, both the number of Internet users and the use ofmost online services, including e-Banking, have increased as shown in Table 1.

Payment is one of the most important elements of any business because it makes the sale complete. In the case of e-commerce, payment is still an essential element requiring a payment system akin to the medium used. Consequently, e-Banking is presented as the main payment tool in financial transactions online (Molavi et al., 2011).

Thus, e-Banking will be automatically offering modern and traditional bank services and products to customers directly and with the help of electronic connection channels (Alagheband 2006).Meeting the needs of customers along with fulfilling their differentiation and loyalty are the three most important business objectives for financial institutions, thus promoting the loyalty of customers who make payments through online

Figure 1. Percentage of worldwide access of users to e-banking

Table 1. Internet services used for personal reasons in the last three months

| 2011 | 2012 | |

| Total of people who have used the Internet in the last 3 months | 23,196,058 | 24,075,125 |

| Communication services and information access: Sending or receiving emails | 88.10% | 88.50% |

| Other services: Using services related to travel and accommodation | 58.40% | 58.00% |

| Other services: Selling products or services (direct sales, auctions, etc.) | 10.10% | 12.20% |

| Other services: Phoning or making video calls (via webcam) through the Internet | 21.80% | 31.00% |

| Other services: E-banking | 42.00% | 45.40% |

Source: INE (2012)

banking. Due to the privileged position they have enjoyed, financial institutions have not traditionally been characterized by using tools that favored customer loyalty, whereas in recent years, there are multiple actions that are performed in order to make the relationships with their customers profitable, rather than adding new customers, as this is much more expensive than keeping an existing one (Bhattacherjee, 2001).

In recent years, the current situation in the financial sector has been characterized by (Mom- parler, 2008):

1. Increased competition,

2. Development of technological innovations,

3. Greater accessibility to services,

4. Social interaction of financial customers,

5. Requirement of a lower cost per bank transaction,

6. Counting on customers with higher financial knowledge, and

7. Ease of access to new technologies.

This complicated situation has forced financial institutions to enhance and personalize their service level as well as to involve the entire organization in the search for greater linkage and customer profitability using tools such as Customer Relationship Management (CRM).

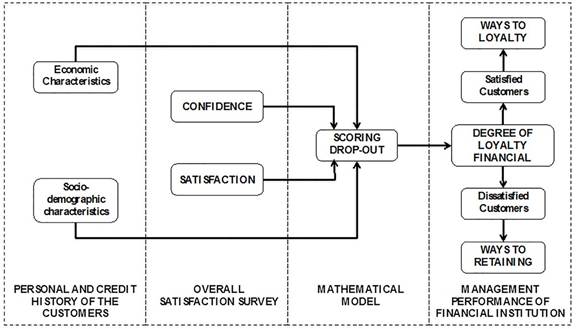

Can statistics help financial institutions and banks in customer faithfulness and loyalty according to their needs? In order to answer this question, this manuscript aims to test the importance that customer loyalty implies for financial institutions and whether that loyalty can bring them a higher profit (Reichheld, 1996), for which empirical research was conducted using a survey of 946 clients of a Spanish financial institution, following the scheme presented in Figure 2. The research results suggest that statistical models provide a great service to detect those customers with high risk of dropping out, though, after viewing a large number of descriptors, a different model can be obtained for each entity within a financial system using, for this, the same methodology.

In this sense, the objective of this work is to determine a method that can assess the existing probability for an e-banking customer not to be faithful to the bank, therefore measuring the risk of loss of an e-banking customer.

For this, we divided the work as follows: in section 2 we define the concept of faithfulness after an extensive review of literature dealing with marketing and consumer behavior. In this regard, we establish the relationships between loyalty and satisfaction and confidence, respectively. In section 3 we present the theoretical relationship of the subject to explain following the concepts defined in previous sections. For this, after posing the objectives and appropriate hypotheses, we propose an empirical model to determine the chance of a customer being loyal or, conversely, leaving the financial institution. In Section 4 we present the results obtained by the proposed model, also analyzing its predictive power. Finally, we reach a series of conclusions and implications from this work.

Figure 2. Outline of the research model

2.

More on the topic INTRODUCTION:

- Introduction

- Introduction

- Introduction

- Introduction

- Introduction

- Introduction

- Introduction

- Introduction

- Introduction

- Introduction