Share of the Largest Banks in the United States and Other Countries

It is ironic that the most intense political pressure to break up large banks because of the TBTF argument seems to be in the United States rather than in other major economies, because the size of the biggest banks relative to the size of the economy is much smaller in the United States than in most other economies.

For several decades, the United States restricted banks from opening branches outside the state of their incorporation, which restrained bank size. The McFadden Act of 1927 restricted opening branches across state lines because of concerns about financial sector concentration and difficulties in supervision. By 1990, however, most states allowed out-of-state holding companies to acquire in-state banks, although opposition from a coalition of small banks and insurance companies delayed national legislation removing the restrictions. The Riegle-Neal Interstate Banking Act of 1994 finally provided for standardized branching and acquisitions, allowing well-managed and well-capitalized banks to acquire banks in any state, subject to a ceiling of 10 percent of total US deposits or 30 percent of a single state's deposits (Medley 1994). The act took full force in 1997. The opening of interstate banking provided an opportunity for expansion by the largest banks.

Another institutional change—repeal of the Glass-Steagall Act of 1933—worked in the same direction. Glass-Steagall prohibited firms from operating simultaneously in commercial banking, investment banking, and insurance. In 1999 the Gramm-Leach-Bliley Act repealed this prohibition. With the merger of Citicorp with insurance company Travelers Group in 1998 (with a waiver from the Federal Reserve), Citigroup's assets reached about $740 billion in 1998, compared with $311 billion for Citicorp and $387 billion for Travelers in 1997.[171]

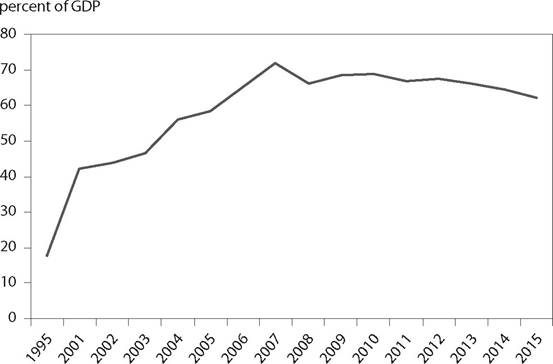

Figure 5.2 shows the combined assets of the 10 largest US banks as a percent of GDP in 1995 and then annually for 2001-15.[172] This ratio surged from 17.5 percent of GDP in 1995 to 42 percent by 2001.

The combined assets of the 10 largest banks peaked at 72 percent of GDP in 2007, easing to 62 percent by 2015. Among the largest banks, real assets fell 18.9 percent at Citigroup, 12.4 percent at Bank of America, 11.5 percent at Goldman Sachs, and 1.8 percent at JPMorgan Chase between 2008 and 2015. (Real assets rose 20.9 percent at Wells Fargo, even after the more than doubling of assets in 2008, when the bank absorbed Wachovia). Like Citigroup, HSBC has substantially downsized, as both banks have curbed their ambitions to maintain a major presence in almost all countries.[173] A change in businessFigure 5.2 Combined assets of 10 largest US banks as percent of GDP, 1995 and 2001-15

Source: Calculated from annual filings of Form 10-K with the Securities and Exchange Commission.

model seems to have dominated at least the cases of Citigroup and HSBC. For the large banks more generally, it seems likely that the increased capital requirements of Basel III played a significant role in the cutbacks.

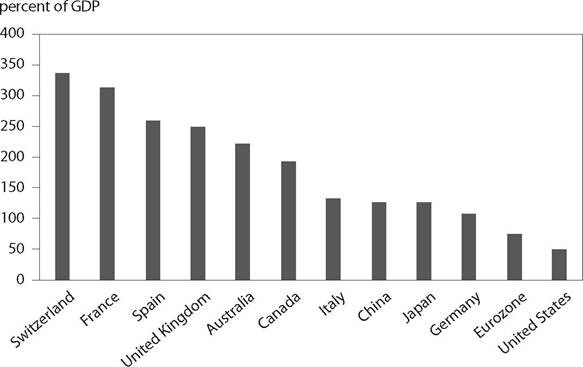

In short, the size of the large US banks relative to GDP rose sharply from the mid-1990s to a peak in 2007, easing somewhat after the Great Recession. Although within the United States this share is perceived as high, it remains modest by international standards. The combined assets of the five largest banks amounted to more than 300 percent of GDP in Switzerland and France in 2015, whereas the share in the United States was only 50 percent (figure 5.3). In both Canada and Australia—two economies that escaped the banking crises of the Great Recession—the assets of the top five banks account for about 200 percent of GDP, four times as much as in the United States. In China and Japan—two other economies that escaped the banking crises of the Great Recession—the ratio is about 125 percent of GDP. The closest one can come to the US share of the biggest banks for a major international economy is the euro area as a whole (75 percent) (figure 5.3).

The implication would seem to be that if there is major danger posed by the large size of the biggest banks, this danger is substantially smaller in the United States than in other major economies.Figure 5.3 Assets of the five largest banks as percent of GDP in selected economies, 2015

Sources: www.relbanks.com; IMF (2016c).

Bank Resolution and Crisis Management

Just as the question of TBTF is inherently linked to the question of whether there are economies of scale that could make it socially inefficient to break up the large banks, TBTF and the TLAC solution are closely related to the question of whether reforms after the Great Recession addressed the challenge of what might be thought of as “immaculate bankruptcy” for the largest banks.[174] The polite term for bankruptcy in banking is “resolution”— a less alarming term that also implies a much faster workout than in normal corporate bankruptcies, as speed is critical in preventing the failure of one large bank from turning into a systemic crisis.

In the United States, the Dodd-Frank Act of 2010 sought to ensure that shareholders and creditors, rather than taxpayers, bear the burden of bank failure. To address the case of systemically important banks, its Title II provided for Orderly Liquidation Authority (OLA), in which the Federal Deposit Insurance Corporation (FDIC) takes receivership of a large financial company, including not only bank holding companies but also systemically important nonbank financial institutions. In 2013 the FDIC announced its Single Point of Entry (SPOE) approach to implementing OLA, whereby in effect the holding company would be placed into expedited bankruptcy while its key subsidiaries would be kept open and operating, in principle preventing a run on the subsidiaries' liabilities (see Clearing House 2013, Skeel 2014, and Kupiec and Wallison 2015).

The Dodd-Frank legislation took other actions that constrained the ability of the Federal Reserve to address a financial crisis precipitated by difficulties at large financial institutions.

The legislation did not change the Federal Reserve's ability to provide emergency lending to banks through the discount window, within the classic lender-of-last-resort framework for unlimited lending against collateral to solvent banks at a penalty rate in the face of a panic (Bagehot 1873). However, it restricted the Depression-era section 13(3) of the Federal Reserve Act, which provides for emergency lending to nonbank firms in “unusual and exigent” circumstances. The new legislation requires that any such lending be within a program with “broadbased” eligibility rather than designed for single firms. Special vehicles such as Maiden Lane (set up to provide a $29 billion asset guarantee to JPMorgan Chase in exchange for its takeover of Bear Stearns) would probably not be possible now. Nor would the support of nearly $200 billion to AIG or the Federal Reserve's guarantees of about $300 billion in asset-backed securities for Citigroup and about $120 billion for Bank of America in exchange for preferred shares and warrants. The Dodd-Frank legislation also eliminates the scope for the FDIC to provide “open bank assistance,” ruling out such lending as its rescue of Continental Illinois in 1984 and probably its temporary program of guarantees for new bank debt in October 2008 at the height of the crisis (see Cline 2010, 2015d). Whether Dodd-Frank increased or decreased systemic resilience to failure of large financial firms thus turns on whether the improvements from higher capital and liquidity requirements (and TLAC), together with OLA, outweigh the curtailment of lender-of-last- resort capacity.[175]Scott (2016, 93) argues that the Dodd-Frank restrictions “have substantially curtailed the Fed's ability to be an effective lender of last resort in a future crisis and have made our financial system much less stable.” He judges that the requirement for approval by the secretary of Treasury of a special program of support to nonbanks raises the risk of politicization, contributing to uncertainty. Noting that the Federal Reserve indicated in late 2015 that a program in which five or more institutions are eligible to participate would meet the test of “broad-based,” he asks whether the Fed would have to wait to act until five institutions experienced a run at the same time.

He emphasizes that Dodd-Frank constrains use of the discount window for Federal Reserve lending to nonbank affiliates of banks, limiting such pass-through lending to 10 percent of the capital of the bank in the group (p. 104). The effect would be extremely limiting for Goldman-Sachs and Morgan Stanley, whose depository banks constitute only a modest share of their total assets. He concludes that nonbank affiliates that previously could receive funding without limit from their associated depository institutions will now have to go to the Fed directly as nonbanks for loans under section 13(3), subject to its new restrictions. William Dudley, the president of the Federal Reserve Bank of New York, has expressed concern that the Fed currently has “very limited” ability to lend to securities groups in a crisis.[176]Geithner (2016, 18-19) has enumerated the large lender-of-last-resort operations in the Great Recession that would no longer be possible under the constraints of Dodd-Frank. They include support for AIG and the Bear Stearns takeover (Maiden Lane), at about $90 billion each; the increased FDIC insurance ($480 billion); the Asset Guarantee Program support to Citigroup and Bank of America ($419 billion); the FDIC's Debt Guarantee Program for new senior unsecured debt ($346 billion); Treasury's guarantee of money market funds ($3.2 trillion); Troubled Asset Relief Program (TARP) investments in individual firms ($315 billion); Treasury's commitment to Fannie Mae and Freddie Mac ($188 billion); and Treasury's purchase of agency- guaranteed mortgage-backed securities ($142 billion). He argues that “a standing ability to extend broad guarantees to the core of the financial system... does not exist today” and that under these circumstances use of the OLA “would exacerbate rather than mitigate the crisis, intensifying the run on both individual institutions and the system as a whole.”

There would seem to be substantial grounds for questioning the feasibility of a smoothly functioning resolution of one of the largest banks working through the OLA and SPOE.

The approach implies the presence of relatively large assets and subordinated debt at the holding company level and neat compartmentalization of a number of moderately sized subsidiaries, so that the failure of any one of them is moderate in scale compared with the totality of the subsidiaries and bank holding company. The SPOE is premised on transferring all of the assets, short-term debt, derivatives, and senior debt of the bank holding company to a new bridge company but leaving the bank holding company's stock and unsecured long-term debt behind in the bank holding company.[177] The bridge entity would thus be relatively well capitalized. In contrast, the original shareholders in the bank holding company would effectively be wiped out, and the subordinated debt left behind in the bank holding company would be converted into shares in the troubled subsidiary as a form of recapitalizing it.In principle, the real-world productive activity taking place at the troubled subsidiary (not to mention its healthy sibling subsidiaries in the bank holding company) would continue uninterrupted; the only disruption would be the reshuffling of ownership associated with the wiping out of bank holding company shareholders and creditors. The question is whether market panic from failure of one of the largest financial firms would be avoided because markets would be comfortable providing credit to its subsidiaries, even though the bank holding company was in resolution (bankrupt). Retail investors, at least, would seem likely to exit the subsidiaries immediately rather than wait around to see whether the process works.[178] To be sure, the arrangement provides for sizable FDIC funding to the bridge entity and hence to the subsidiaries.

The OLA/SPOE strategy has implications for TLAC. It implies that large bank holding companies will be required to hold substantial subordinated debt to ensure the availability of resources that can be used in the workout process just described. Some analysts are thus concerned that the strategy may lead to increased leverage and financial fragility of these banks. A practical problem is that for a number of large banks, the main banking subsidiary is almost as large as the entire bank holding company. The ideal SPOE configuration would be a number of smaller subsidiaries, each of which is unlikely to get into trouble at the same time as the others. The size of liabilities of the parent holding company is typically only about 3 to 6 percent as large as the liabilities of the subsidiary bank, so existing bank holding company debt could fall considerably short of the amount needed to be converted to equity in recapitalizing the subsidiary bank (Kupiec and Wallison 2015, 184, 192).

Overall, it is questionable that OLA and SPOE have eliminated the crisis risk associated with the collapse of a large US bank. The implication is that sufficient equity capital—and sufficiently effective supervision (including through stress tests)—are essential to help avoid putting them to the test.[179]

In the European Union, there has been a similar shift from lender-of- last-resort action to bail-in in the name of avoiding taxpayer costs. The Bank Recovery and Resolution Directive of April 2014 is even more explicit than Dodd-Frank in enforcing bail-in. When a bank is “in breach of, or is about to breach, regulatory capital requirements,” restructuring can be imposed. Although “in circumstances of very extraordinary systemic stress, authorities may also provide public support instead of imposing losses in full on private creditors,” the authorities can provide such support only “after the bank's shareholders and creditors bear losses equivalent to 8 percent of the bank's liabilities and would be subject to the applicable rules on State aid.”[180] However, as Goodhart and Avgouleas (2014, 32) observe with regard to both the Bank Recovery and Resolution Directive and TLAC, the “market propensity to resort to herding at times of shock means that it is not realistic to believe that generalized adoption of bail-in mechanisms would not trigger contagious consequences that would have a destabilizing effect.” They emphasize that whereas bail-in could be salutary for idiosyncratic bank failure, it would be counterproductive in the face of systemic collapse.

A key feature for the euro area, nonetheless, is that the European Central Bank retains broad lender-of-last-resort authority, as there has been no curtailment in its flexibility analogous to the Dodd-Frank restrictions on the Federal Reserve. In principle, in an incipient bank panic, it could make determinations of underlying bank solvency that would enable it to provide substantial liquidity support, avoiding the transit of numerous institutions into the rigid bail-in requirements of the Bank Recovery and Resolution Directive.

More on the topic Share of the Largest Banks in the United States and Other Countries:

- Cline W.. The Right Balance for Banks. Peterson Institute for International Economics,2017. — 281 p., 2017

- Hyposplenic states

- United States

- POLITICAL ELITES IN THE NEW STATES