United States

Soft landing in 2024

| GDP | USD25462.7bn (World ranking 1) |

| Population | 333.3mn (World ranking 3) |

| Form of state | Federal Republic |

| Head of government | Joe Biden (President) |

| Next elections | 2024, Presidential and legislative |

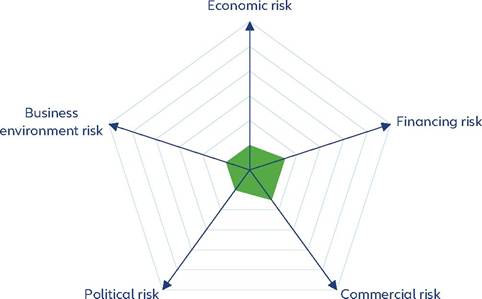

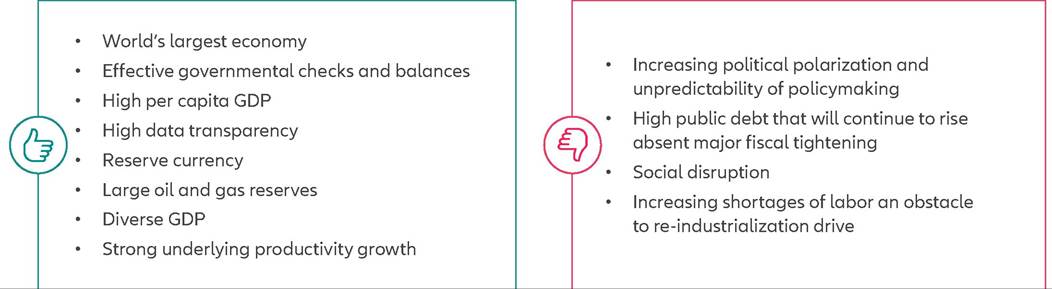

Strengths & weaknesses

Economic overview

Heading for a soft landing as supply-side of the economy improves

The US bounced back rapidly from the pandemic-induced downturn and has been easily outpacing developed market peers since then.

In 2023, the US economy remained remarkably resilient to the Fed-induced sharp rise in interest rates, thanks to the unwinding of consumer savings built up during the pandemic, loose fiscal policy and solid corporate and household balance sheets. Meanwhile, inflation and wage growth have cooled down amid the ending of global supply-chain disruptions, an easing of labor market conditions and the Fed's high credibility in anchoring medium-term inflation expectations close to targeted inflation.For 2024, GDP growth should step down. The high interest rate environment is starting to weaken some segments of the economy beyond construction. Consumer loan delinquencies have started to pick up, while cyclical hiring (e.g., in retail) is losing momentum. Meanwhile, some of the factors that boosted 2023 growth should reverse, such as tighter (though not overwhelming) fiscal policy. At the corporate level, prolonged tight lending standards from banks should lead to a weakening of business investment - already evidenced in lower capex intentions.

Households are expected to slow their usage of pandemic savings - which are still far from being exhausted yet - to fund consumption expenditures: data indicate that households have been increasingly shifting their funds from liquid deposits to less liquid time deposits and money market funds. Against this backdrop, solid private sector balance sheets, falling inflation and an improvement of the supply side of the economy (through a boost to labor supply and a pick-up in productivity) should allow the US economy to head towards a soft landing in 2024Corporate bankruptcies should continue to rise through 2024 as economic momentum falters and catch-up effects from the pandemic continue to play out. However, solid corporate balance sheets (in particular, high cash buffers and low debt-to-equity ratio) should keep them contained. Against this backdrop, the US is expected to retain one of the highest rates of medium-term GDP growth potential amongst large developed markets.

Structural vulnerabilities

The US remains the world's largest economy and, despite its dominance being challenged, the US dollar remains by far the world's largest reserve currency. US financial markets are the largest and the deepest globally, providing cheap and liquid financing. Nevertheless, the economy is carrying a tremendous debt load. Independent research bodies such as the Congressional Budget Office (CBO) expect the public debt load to continue rising rapidly over the coming decades in the absence of ambitious policy measures to rein in spending and/or increase revenues. Increasing political infighting makes this prospect unlikely, at least in the short term.

There is also an inexorable demographic of an aging workforce as “Baby Boomers” are retiring and will continue doing so for much of this decade. At the same time, there will not be enough workers to support this ever-growing population of older, sicker retirees. Labor shortages are set to worsen over the coming years and decades, which will increasingly constraint the ability of the US economy to boost the share of manufacturing significantly.

The US also suffers from persistently high trade and current account deficits. While the Treasury securities used to finance these deficits remain highly liquid, the occasional battles to raise the debt ceiling create unnecessary turmoil in the financial markets and threaten the country's credit rating.

Business environment and political developments

The business environment in the US is very accommodating, consistently ranking amongst the top performers in Ease of Doing Business reports. The hallmarks of the economy include strict enforcement of contracts, the ease of resolving insolvencies, the rule of law in general and the easy access to credit.

Politics is becoming increasingly divisive, both between and within political parties. Repeated disagreements over the debt ceiling and the budget have increased economic and political uncertainties. Some of President Biden's flagship legislation - such as large green subsidies - could be removed or watered down if a Republican wins the presidential election in November 2024. However, measures introduced to counter China's growing influence - such as export restrictions on high-end chips and chipmaking equipment - are unlikely to be phased out by a Republican amid political consensus to rein in China's access to western technology. Moreover, the strong policy push towards re-industrialization is likely to continue whoever wins the White House and Congress in the next elections.

A Trump 2.0 presidency could have far-reaching consequences for both the US and the rest of the world though. Trump's campaign pledges include more customs tariffs being levied - including against western allies - and the seizing of some of China's strategic assets on US soil. On the domestic side, a Trump presidency would probably mean lower taxes and the return of the deregulatory agenda.