Strong governance and institutions, in pursuit of fiscal consolidation

| GDP | USD71.2bn (World ranking 79) |

| Population | 3.4mn (World ranking 132) |

| Form of state | Constitutional Republic |

| Head of government | Luis Lacalle Pou (President) |

| Next elections | 2024, General |

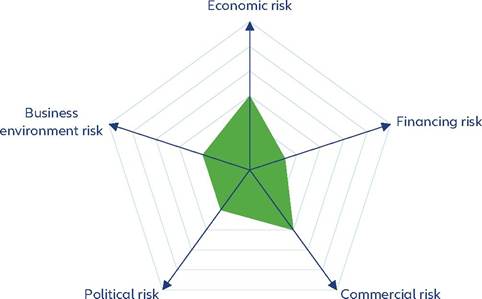

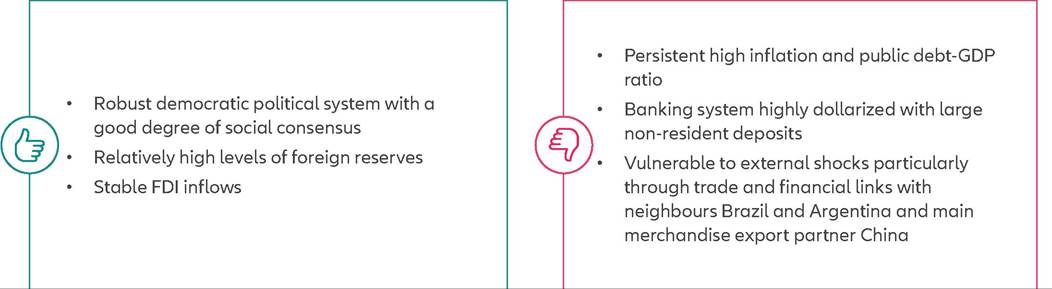

Strengths & weaknesses

Economic overview

Solid basis, conjunctural headwinds

Uruguay experienced a period of high growth from 2004 to 2014 (+5.36% on average), but has since then seen subdued growth.

Its economy held up better than the regional average during the pandemic and it recovered pretty well in 2021 (+5.3%) and 2022 (+4.9%), thanks to strong exports in agricultural commodities. Last year was marked by the most severe drought in 40 years - which hit the whole Southern Cone - which led to subdued exports, a worse fiscal balance and eventually low growth (estimated at +0.8%) in 2023. The country also suffered directly from the economic crisis in Argentina and from the slowdown of the whole region, as tourism revenue constitutes a non-negligible part of its economic structure. Still, Uruguay has a healthy economy, with high income per head, stable FDI inflows and a balanced democratic system which makes it one of the most robust democracies in the world. In 2024, we predict GDP growth to pick up to +3.3%, as the weather conditions ease and allow for a rebound in agricultural production and exports, as well as industrial production and exports. On the longer term, growth should stabilize at just under +3% on average, driven by a well led green transition and resilience in exports.Uruguay has had above-regional inflation for several years now, with levels hovering between 7.8% and 9.8% between 2019-2022. However, inflationary pressures have started to ease since September 2022 on and inflation has continued to decrease, reaching 3.9% y/y in September 2023, owing to lower global commodity prices and easing logistics. Uruguay has an inflation target range of 3-6%, with the Banco Central del Uruguay (BCE) - the Uruguayan central bank - raising its policy rate to a peak of 11.5% in December 2022 and having started an easing cycle since then. The easing cycle should be quite progressive, since lowering the policy rate too quickly could cause peso depreciation, due to a narrowing interest rate differential with the US. The orthodox fiscal policy led by President Lacalle Pou helped tame inflation. We expect a gradual convergence of inflation to below 6% in the 20242025 forecast period.

I ndicators point to a solid fiscal situation

Uruguay has made a strong commitment to fiscal consolidation. Uruguay's resilient fiscal performance in absorbing the Covid-19 pandemic shock, coupled with its track record of adherence to its revised fiscal framework, has strengthened fiscal credibility, increased resilience to economic shocks and reduced the risk of a potentially significant future increase in the public debt burden. The recent adoption of a reform that improves the sustainability of the pension system further signals the commitment to a more prudent fiscal policy in line with its high governance scores. We expect the budget deficit to remain relatively stable at around 2.5% of GDP and the public debt at 60% of GDP over the 2024-2027 forecast period.

The current-account balance in Uruguay reached a deficit of-3.7% of GDP in 2023, it's highest level since the balance became negative in 2020. The loss in exports from the agricultural subdued production is central in understanding the widening deficit of this year, as well as the widening fiscal balance deficit (-3.2% of GDP in 2023).

The outlook should change from now on. However, the rebound in food production and industry and a higher sales tax collection - with the redirection of private consumption towards the domestic side - should support the fiscal situation. Uruguay appears a very solid country on the fiscal side, especially since its fiscal policy is guided by the Consejo Fiscal Asesor (CFA), a council created in 2013. The public debt set at 59.3% of GDP in 2022 and is expected at a stable level, just over 60% in the next years.External finances remain sound, despite their dependence on the primary sector. External debt is likely to set at 85.0% in 2023. Nevertheless, inflows of FDI and a high level of international reserves provide a substantial buffer against external shocks or bulk repayments.

A strong business environment and political stability

Uruguay's business environment is very strong: the country ranks 27th out of 177 in the 2023 Heritage Foundation's Index of Economic Freedom survey and 4th in the Americas. Its best scores are obtained in property rights, judicial effectiveness and business freedom and the country enjoys labor competitiveness. Uruguay appears well protected from corruption and foreign investments don't need preliminary approval. Trade freedom is also well assessed, as the trade- weighted average tariff rate is 9.6%. The only bad score Uruguay obtains is in financial freedom, as the government still takes a big role in the financial sector. The 2022 Worldwide Governance Indicators survey ranks the country 19th, over 209 countries, in control of corruption and in the first quartile for regulatory quality and rule of law. All indicators have improved compared to 2021. Moreover, our proprietary Environmental Sustainability survey of 2023 indicates that the country performs quite well in resistance to water stress, CO2 emissions and renewable electricity output. On the other hand, the recycling rate is poorly rated.

President Luis Lacalle Pou enjoys relatively high levels of popularity, thanks to strong job creation and increasing wages.

The government may leverage its political capital to continue efforts towards fiscal consolidation. We expect the government to expand the number of free-trade agreements (FTAs) Uruguay has outside Mercosur, such as advancing on joining the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) - an initiative also back by Argentina's new President Javier Milei. The government also seeks to increase foreign investment, especially in services. There are still certain risks of increased political tensions as parties seek to differentiate themselves from the current government ahead of 2024 general elections, during which Laacalle Pou cannot run for presidency again. Uruguay remains a strong democracy and therefore political risk appears contained in the next years.