Vietnam

Realizing opportunities and keeping structural fragilities in check

| GDP | USD408.8bn (World ranking 37) |

| Population | 98.2mn (World ranking 16) |

| Form of state | Communist party-led state |

| Head of government | Nguyen Phu Trong (General Secretary of the Communist Party) |

| Next elections | 2026, Legislative |

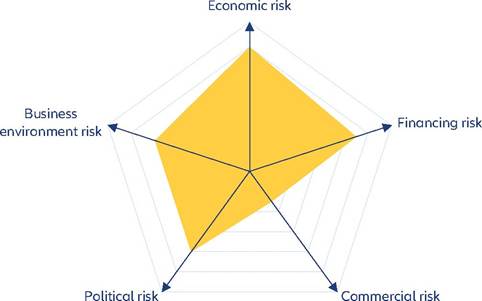

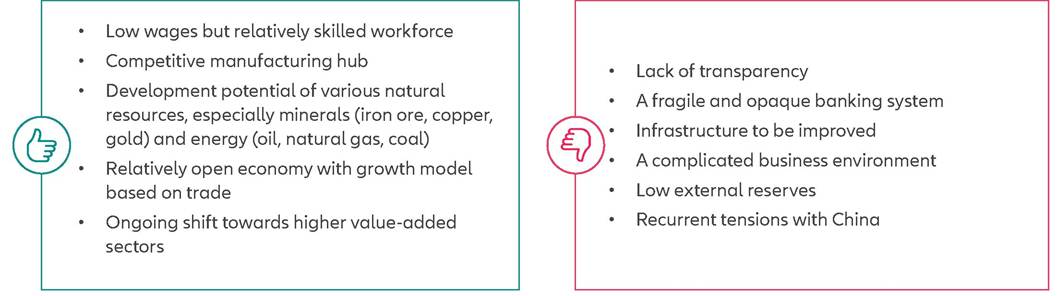

Strengths & weaknesses

Economic overview

Growth to recover and trend towards the long-term potential

Vietnam is a good performer among emerging economies, with nearly +7% growth on average in the three decades before the Covid-19 pandemic and +4.5% on average over 2020-2022.

Against the backdrop of the global economic growth slowdown and weaker external demand, we estimate that real GDP growth declined from +8% in 2022 to +4.7% in 2023 and expect a recovery to +6.3% in 2024. As such, Vietnam will remain one of the fastest-growing economies in the Asia-Pacific region in the upcoming years. Outperforming exports, especially of electronics, machinery and footwear, will remain the key growth drivers, supported by the trend of international firms diversifying their supply chains and relocating their operations to Vietnam. Impacted by higher global commodity prices and the stronger USD since 2022, inflation in Vietnam accelerated and reached an average 3.2% in 2022 and 3.3% in 2023 (from 1.8% in 2021). We expect the inflation rate to remain elevated in 2024 (3.4%) before easing slightly in 2025 (3.1%).Over the longer term, the economy is expected to remain a sturdy growth performer in the region, helped by foreign direct investment, solid demand from Asian and Western markets, strong competitive advantages (low labor costs, high productivity growth and a strategic location), increasing integration in global supply chains and a positioning as a global manufacturing hub. Vietnam may also benefit from some firms' will to divest and diversify from China and find new production sites.

Liquidity risk has increased

Overall, indicators show that Vietnam's short-term financing risk is sensitive, reflecting declining foreign exchange reserves and import cover, as well as high credit growth. With efforts to ensure stability in the VND-USD exchange rate, foreign exchange reserves in Vietnam have fallen and the ratio of money supply M2 to foreign exchange (FX) reserves increased from 529% at the end of 2021 to nearly 700% as of August 2023 (a ratio below 400% is considered adequate). Likewise, the number of months of imports that is covered by FX reserves decreased from 3.9 at the end of 2021 to 2.8 in August 2023 (at least four months is usually deemed appropriate). A heavily managed exchange rate regime so far sustained the risk of a large depreciation. However, if external demand conditions were to deteriorate and FX reserves to fall further, the central bank may at some point no longer be able to defend the VND.

Real domestic credit growth has remained elevated. It showed a downtrend at the beginning of 2023, dropping from nearly +14% y/y in January 2022 to +6.6% y/y in January 2023. However, it has since remained at a relatively elevated level (+6.3% y/y in September 2023), as inflation has been easing and the State Bank of Vietnam (SBV, the central bank) began relaxing monetary policy in March 2023 by reducing the discount rate from 4.5% to 3% and the benchmark refinancing rate from 6% to 4.5%, in an aim to support economic growth after a weaker performance from the external sector.

On the one hand, these policy moves helped alleviating a credit crunch in the property sector, where many firms were facing repayment and refinancing difficulties, leading to an increasing risk of bad debts in the banking sector. On the other hand, continuously rising credit will raise private sector debt-sustainability risks if the economy slows down more than expected.Business environment and political developments

Vietnam's business environment is below average in our assessment of 185 economies. The Heritage Foundation's Index of Economic Freedom 2023 survey assigns Vietnam rank 72 out of 184 economies (a steady improvement from rank 105 in the 2020 survey), reflecting good scores with regard to the tax burden, government spending, business freedom and trade freedom, while weaknesses remain particularly in the areas of investment freedom, financial freedom, property rights, judicial effectiveness and government integrity. The latter is underscored by the World Bank Institute's annual Worldwide Governance Indicators surveys, which indicate considerable weaknesses with regards to the regulatory and legal frameworks, as well as measures to combat corruption. Our proprietary Environmental Sustainability Index puts Vietnam at rank 130 out of 210 economies, reflecting strengths in energy use per GDP and water stress, but weaknesses in terms of climatechange vulnerability, renewable electricity output and the recycling rate.

Political stability is to be expected in the coming years. Vietnam is a one-party state, tightly controlled by the Communist Party of Vietnam (CPV). Nguyen Phu Trong was named general secretary of the CPV for the third consecutive term in early 2021, ensuring policy continuity. The next election for the National Assembly (often characterized as a rubber stamp for the CPV) is scheduled to be held in 2026. CPV General Secretary Nguy?n Phu Tr?ng's policy agenda in the coming years focuses on a high-level anti-corruption campaign, attracting foreign investment, privatizing state- owned enterprises and upgrading infrastructure.

More on the topic Vietnam:

- State-Owned Enterprises in Vietnam: A Brief Overview

- The Ambiguity of Limited War

- On 16 March 1965, an elderly Quaker woman walked along Detroit sidewalks she had known for almost 25 years.

- Hoang’s account of unconstitutional constitution

- Substantive Result and Post-ConstitutionMaking Implementation

- Conclusion

- Conflict Comes to Cambodia

- UCA as constitutional politics

- Antony Robert, Carroll Stuart, Pennock Caroline D. (eds.). The Cambridge World History of Violence. Volume 3: AD 1500-AD 1800. Cambridge University Press,2020. — 710 p., 2020

- We begin the conclusion of this volume with a story of hope.