THE IMPORTANCE OF BEING SKEPTICAL

By now, the reader presumably understands why this chapter is entitled “The Adversarial Nature of Financial Reporting.” The issuer of financial statements has been portrayed in an unflattering light, invariably choosing the accounting option that will tend to prop up its stock price, rather than generously assisting the analyst in deriving an accurate picture of its financial condition.

Analysts have been warned not to partake of the optimism that drives all great business enterprises, but instead to maintain an attitude of skepticism bordering on distrust. Some readers may feel they are not cut out to be financial analysts if the job consists of constant naysaying, of posing embarrassing questions, and of being a perennial thorn in the side of companies that want to win friends among investors, customers, and suppliers.Although pursuing relentless antagonism can indeed be an unpleasant way to go through life, the stance that this book recommends toward issuers of financial statements implies no such acrimony. Rather, analysts should view the issuers as adversaries in the same manner that they temporarily demonize their opponents in a friendly pickup basketball game. On the court, the competition can be intense, which only adds to the fun. Afterward, everyone can have a fine time going out together for pizza and beer. In short, financial analysts and investor-relations officers can view their work with the detachment of litigators who engage in every legal form of shin-kicking out of sheer desire to win the case, not because the litigants’ claims necessarily have intrinsic merit.

Too often, financial writers describe the give-and-take of financial reporting and analysis in a highly moralistic tone. Typically, the author

exposes a tricky presentation of the numbers and reproaches the company for greed and chicanery.

Viewing the production of financial statements as an epic struggle between good and evil may suit a crusading journalist, but financial analysts need not join the ethics police to do their job well.An alternative is to learn to understand the gamesmanship of financial reporting, perhaps even to appreciate on some level the cleverness of issuers who constantly devise new stratagems for leading investors off the track. Outright fraud cannot be countenanced, but disclosure that shades economic realities without violating the law requires truly impressive ingenuity. By regarding the interaction between issuers and users of financial statements as a game, rather than a morality play, analysts will find it easier to view the action from the opposite side. Just as a chess master anticipates an opponent’s future moves, analysts should consider which gambits they themselves would use if they were in the issuer’s seat.

“Oh no!” some readers must be thinking at this point. “First the authors tell me that I must not simply plug numbers into a standardized spreadsheet. Now I have to engage in role-playing exercises to guess what tricks will be embedded in the statements before they even come out. I thought this book was supposed to make my job easier, not more complicated.”

In reality, this book’s goal is to make the reader a better analyst. If that goal could be achieved by providing shortcuts, the authors would not hesitate to do so. Financial reporting occurs in an institutional context that obliges conscientious analysts to go many steps beyond conventional calculation of financial ratios. Without the extra vigilance advocated in these pages, the user of financial statements will become mired in a system that provides excessively simple answers to complex questions, squelches individuals who insolently refuse to accept reported financial data at face value, and inadvisably gives issuers the benefit of the doubt.

These systematic biases are inherent in selling stocks.

Within the universe of investors are many large, sophisticated financial institutions that utilize the best available techniques of analysis to select securities for their portfolios. Also among the buyers of stocks are individuals who, not being trained in financial statement analysis, are poorly equipped to evaluate annual and quarterly earnings reports. Both types of investors are important sources of financing for industry, and both benefit over the long term from the returns that accrue to capital in a market economy. The two groups cannot be sold stocks in the same way, however.What generally sells best to individual investors is a “story.” Sometimes the story involves a new product with seemingly unlimited sales potential. Another kind of story portrays the recommended stock as a play on some current economic trend, such as declining interest rates or a step-up in defense spending. Some stories lie in the realm of rumor, particularly those that relate to possible corporate takeovers. The chief characteristics of most stories are the promise of spectacular gains, superficially sound logic, and a paucity of quantitative verification.

No great harm is done when an analyst’s stock purchase recommendation, backed up by a thorough study of the issuer’s financial statements, is translated into soft, qualitative terms for laypersons’ benefit. Not infrequently, though, a story originates among stockbrokers or even in the executive offices of the issuer itself. In such an instance, the zeal with which the story is disseminated may depend more on its narrative appeal than on the solidity of the supporting analysis.

Individual investors’ fondness for stories undercuts the impetus for serious financial analysis, but the environment created by institutional investors is not ideal, either. Although the best investment organizations conduct rigorous and imaginative research, many others operate in the mechanical fashion derided earlier in this chapter. They reduce financial statement analysis to the bare bones of forecasting earnings per share, from which they derive a price-earnings multiple.

In effect, the less conscientious investment managers assume that as long as a stock stacks up well by this single measure, it represents an attractive investment. Much Wall Street research, regrettably, caters to these institutions’ tunnel vision, sacrificing analytical comprehensiveness to the operational objective of maintaining up-to-the- minute earnings estimates on vast numbers of companies.Investment firms, moreover, are not the only workplaces in which serious analysts of financial statements may find their style crimped. The credit departments of manufacturers and wholesalers have their own set of institutional hazards.

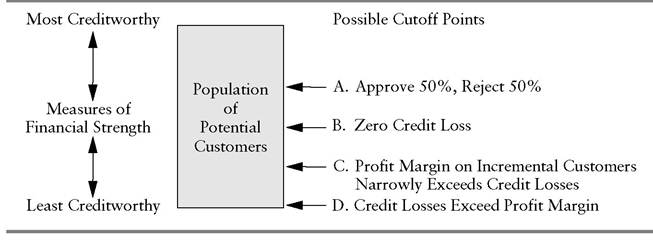

Consider, to begin with, the very term “credit approval process.” As the name implies, the vendor’s bias is toward extending rather than refusing credit. Up to a point, this is as it should be. In Exhibit 1.3, “neutral” Cutoff Point A, where half of all applicants are approved and half are refused, represents an unnecessarily high credit standard. Any company employing it would turn away many potential customers who posed almost no threat of delinquency. Even Cutoff Point B, which allows more business to be written but produces no credit losses, is less than optimal. Credit managers who seek to maximize profits aim for Cutoff Point C. It represents a level of credit extension at which losses on receivables occur but are slightly more than offset by the profits derived from incremental customers.

To achieve this optimal result, a credit analyst must approve a certain number of accounts that will eventually fail to pay. In effect, the analyst is required to make “mistakes” that could be avoided by rigorously obeying

EXHIBIT 1.3 The Bias toward Favorable Credit Evaluations

the conclusions derived from the study of applicants’ financial statements.

The company makes up the cost of such mistakes by avoiding mistakes of the opposite type (rejecting potential customers who will not fail to pay).Trading off one type of error for another is thoroughly rational and consistent with sound analysis, so long as the objective is truly to maximize profits. There is always a danger, however, that the company will instead maximize sales at the expense of profits. That is, the credit manager may bias the system even further, to Cutoff Point D in Exhibit 1.3. Such a problem is bound to arise if the company’s salespeople are paid on commission and their compensation is not tightly linked to the collection experience of their customers. The rational response to that sort of incentive system is to pressure credit analysts to approve applicants whose financial statements cry out for rejection.

A similar tension between the desire to book revenues and the need to make sound credit decisions exists in commercial lending. At a bank or a finance company, an analyst of financial statements may be confronted by special pleading on behalf of a loyal, long-established client that is under allegedly temporary strain. Alternatively, the lending officer may argue that a loan request ought to be approved, despite substandard financial ratios, on the grounds that the applicant is a young, struggling company with the potential to grow into a major client. Requests for exceptions to established credit policies are likely to increase in both number and fervor during periods of slack demand for loans.

When considering pleas of mitigating circumstances, the credit analyst should certainly take into account pertinent qualitative factors that the financial statements fail to capture. At the same time, the analyst must bear in mind that qualitative credit considerations come in two flavors, favorable and unfavorable.

It is also imperative to remember that the cold, hard statistics show that companies in the “temporarily” impaired and start-up categories have a higher-than-average propensity to default on their debt.Every high-risk company seeking a loan can make a plausible soft case for overriding the financial ratios. In aggregate, though, a large percentage of such borrowers will fail, proving that many of their seemingly valid qualitative arguments were specious. This unsentimental truth was driven home by a massive 1989-1991 wave of defaults on high-yield bonds that had been marketed on the strength of supposedly valuable assets not reflected on the issuers’ balance sheets. Bond investors had been told that the bold dreams and ambitions of management would suffice to keep the companies solvent. Another large default wave in 2001 involved early-stage telecommunications ventures for which there was scarcely any financial data from which to calculate ratios. The rationale advanced for lending to these nascent companies was the supposedly limitless demand for services made possible by miraculous new technology.

To be sure, defaults also occur among companies that satisfy established quantitative standards. The difference is that analysts can test financial ratios against a historical record to determine their reliability as predictors of bankruptcy (see Chapter 13). No comparable testing is feasible for the highly idiosyncratic, qualitative factors that weakly capitalized companies cite when applying for loans. Analysts are therefore on more solid ground when they rely primarily on the numbers than when they try to discriminate among companies’ soft arguments.

More on the topic THE IMPORTANCE OF BEING SKEPTICAL:

- appendix : BARTLEY’S CRITIQUE OF POPPER

- The Balanced-Budget Multiplier

- Mathematical Economist

- SIMILARITIES BETWEEN CONFLICT RESOLUTION AND HUMAN RIGHTS

- The Theory of Income Determination

- Why Macroeconomists Disagree

- HISTORICAL AND PRESUPPOSITION ARGUMENTS FOR THE EXISTENCE OF A TOE