VALUATION THROUGH RESTRUCTURING POTENTIAL

A more subtle benefit of the Du Pont analysis is the insight it can provide into companies’ potential for enhancing value through corporate restructuring.

Whether initiated internally or imposed from outside, major revisions in operating and financial strategies can dramatically increase the price of a corporation’s common shares. The analysis illustrated in Exhibit 14.7 helps to identify the type of restructuring that can unlock hidden value in a particular instance. Some companies have the potential to raise their share prices by utilizing their assets more efficiently, whereas others can increase their value by increasing their financial leverage.3By way of background, corporate managers frequently find themselves at odds with stock market investors and speculators over issues of corporate policy. In general, managers prefer to maintain a certain amount of slack in their organizations, that is, a reserve capacity to deal with crises and opportunities. They tend to be less troubled than investors if their companies generate excess cash that remains on the balance sheet earning the modest returns available on low-risk, short-dated financial instruments. That cash may come in handy, they argue, if earnings and cash flow unexp ectedly turn down or if an outstanding acquisition opportunity suddenly presents itself. Investors and speculators, in contrast, prefer to see the cash used to repurchase stock or else returned to shareholders. Managers also tend to be more inclined than shareholders to believe that underperforming units can be rehabilitated. Their judgment is sometimes influenced by reluctance to admit that acquisitions in which they had a hand have worked out po orly.

Over the years, management-shareholder disputes over such operating- and financial-policy issues have featured a variety of tactics.

As far back as 1927 and 1928, pioneer securities analyst Benjamin Graham waged a successful campaign to persuade the management of Northern Pipeline to liquidate certain assets that were not essential to the company’s crude oil transportation business and distribute the proceeds to shareholders. Graham enlisted pivotal support for his effort from a major institutional holder, the Rockefeller Foundation. The outcome was unusual, as institutional investors generally sided with management, both at the time and for many years afterward. At most, institutions sold their shares if they became thoroughly dissatisfied with the way a company was being run. Trying to bring about change was not a widespread institutional practice, even in the 1980s. Therefore, management’s main adversaries in battles over corporate governance were aggressive financial operators. During the 1950s, these swashbucklers attracted considerable attention by pushing for strategic redirection through proxy battles. Their modus operandi consisted of striving to obtain majority control of the board through the election of directors at the annual meeting of shareholders.The 1970s brought the tactical shift to hostile takeovers, a type of transaction previously regarded as unsavory by the investment banks that acted as intermediaries in mergers and acquisitions. Hostile takeovers became especially prominent in the 1980s, fueled in part by the greatly increased availability of high-yield debt (informally referred to as “junk bond”) financing. High-yield bonds also financed scores of leveraged buyouts. LBO sponsors defended these controversial transactions in part by arguing that corporations could improve their long-run performance if they were taken private and thereby shielded from the public market’s insatiable demand for short-run profit increases.

In the 1990s, institutional investors finally began to understand the influence they could wield in corporate boardrooms by virtue of their vast share holdings.

Large institutional shareholders began to prod corporations to increase their share prices by such measures as streamlining operations, divesting unprofitable units, and using excess cash to repurchase shares. In some instances, where merely making their collective voice heard had no discernible effect, the institutions precipitated the ouster of senior management.The shareholder activism of the 1990s flourished in an environment of comparatively high price-earnings ratios. Additionally, the period was characterized by a backlash against the previous decade’s trend toward increased financial leverage. Conditions were not conducive to the sort of borrow-and-acquire transactions that drove much of the corporate restructurings of the 1980s.

In that era, the prototypical deal consisted of gaining control of a company by buying its stock at a depressed price, then adding a large amount of debt to the capital structure. Opportunities of this sort were abundant, not only because of low prevailing price-earnings ratios, but also because many corporations carried far less debt than their cash flows could support. At least in the early stages, before some raiders became overly aggressive in their financial forecast assumptions, it was feasible to extract value without creating undue bankruptcy risk, simply by increasing the ratio of debt to equity. The hostile takeover artists focused on the second factor in the Modified Du Pont Formula—financial leverage.

By releasing the potential embedded in a relatively debt-free balance sheet, the corporate raiders of the 1980s did more than pursue large profits. More important to the subject at hand (although not to the raiders), their activities seriously undermined the earnings multiple as a basis for valuing companies.

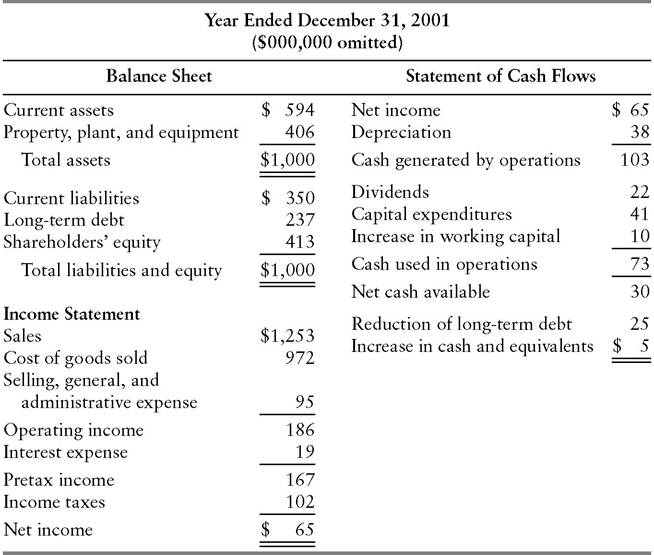

Consider the fictitious Sitting Duck Corporation (Exhibit 14.8).

Under conventional assumptions, and given a prevailing earnings multiple of 11 on similar companies, Sitting Duck’s equity will be valued at $715 million, about 1.7 times its book value of $413 million.EXHIBIT 14.8 Sitting Duck Corporation

Corporate raiders, however, would approach the valuation much differently. Their focus would not be on earnings, but on cash flow. After paying out approximately one-third of its earnings in dividends and more than offsetting depreciation through new expenditures for plant and equipment, Sitting Duck generated $30 million of cash in 2001. The incumbent management group used this cash to reduce an already conservative (36%) total-debt-to-total-capital ratio and to add to the company’s existing portfolio of marketable securities. To a takeover artist, a more appropriate use would be to finance a premium bid for the company.

The arithmetic goes as follows: Assume commercial banks are currently willing to lend to sound leveraged buyout projects that can demonstrate EBITDA coverage of 1.5 times. (The lenders do not care about the company’s book profits, but rather about its ability to repay debt. Cash generation is a key determinant of that ability.) Sitting Duck’s operating income of $186 million, with $38 million of depreciation added back, produces EBITDA of $224 million. The amount of interest that $224 million can cover by 1.5 times is $149 million, an increase of $130 million over Sitting Duck’s present interest expense. Assuming a blended borrowing cost of 13% on the LBO financing, a raider can add $1 billion of debt to the existing balance sheet. If prevailing lending standards require equity of at least 10% in the transaction, the raider must put up an additional $111 million, for a total capitalization of $1.1 billion.

By this arithmetic, the takeover artist can pay a premium of 55% ($1.111 billion ÷ $715 million = 1.55) over Sitting Duck’s present market capitalization. The purchase price equates to a multiple of 17 times earnings, rather than the 11X figure currently assigned by the market. The raider got to this number, however, through a measure of cash flow, rather than earnings. The EBITDA multiple of the bid is 5.0 times, a moderate level by the standards of LBO specialists. (As explained in Chapter 8, EBITDA is by no means the best measure of cash flow, but it can be fairly described as the standard in leveraged finance circles.)Stepping back from these calculations, one is bound to wonder whether the raider can truly expect to earn a high return on investment after paying 55% above the prevailing price for Sitting Duck’s shares. In actuality, many comparably high-priced takeovers of the 1980s proved quite remunerative for the equity investors. Some of the cycle’s early deals benefited from asset values that could not be discerned from even a thorough review of the financial statements. For example, companies owned real estate bought decades earlier and carried at historical cost. These assets were salable at substantially higher prices than their balance sheet values. Armed with such information, managers led buyouts of their own companies, knowing that they were not taking on inordinately large debt relative to the market value of the acquired assets. Naturally, transactions in which the managers had an informational advantage over the shareholders, who were in principle their ultimate employers, prompted complaints of conflicts of interest. As the LBO cycle of the 1980s progressed, boards of directors took greater care to arrange competitive auctions for their companies, lest they be accused of obtaining inadequate value for selling shareholders through “sweetheart” deals with management. The opportunities for LBO sponsors and management teams to buy companies on the cheap consequently diminished.

Purchasers could no longer be confident that the economic value of the acquired assets exceeded the amount of debt they were taking on. Many bonds connected with these late-cycle LBOs went into default in 1990 and 1991.Leveraged buyouts became a less prominent feature of the financial landscape during the 1990s. Transactions continued to occur, although with less highly leveraged capital structures than investors countenanced in the late 1980s. In future bear markets, when stocks again sell at depressed priceearnings multiples, investors will probably renew their focus on companies’ values as LBO candidates. Equity analysts will need to understand how those values are determined to assess the upside potential in stocks. In addition, lenders, bondholders, and purchasers of LBO equity can be expected to call on analysts of financial statements to judge the likelihood that particular deals will prove profitable. The answers will lie partly in ability of the companies to emulate the strategies employed by leveraged buyouts of the past that succeeded in paying off their debts and providing satisfactory risk- adjusted returns to their equity investors. Typically, the LBO world’s winners have achieved their gains through one or both of the following means:

1. Profit Margin Improvement. A leveraged buyout can bring about improved profitability for either of two reasons. First, a change in ownership results in a fresh look at the company’s operations. The newcomers typically have less sentimental attachment to product lines that are long on tradition but are no longer profitable. In addition, they can more easily take the emotionally difficult, but necessary, steps to restore competitiveness, such as reducing the work force and outsourcing production. Second, management may obtain a significantly enlarged stake in the firm’s success as the result of a buyout. In lieu of stock options that could leave them comfortably provided for in their retirement, senior and even middle-level executives may receive equity interests that can potentially make them immensely wealthy within a few years. The change in incentives can reduce managers’ zeal for maintaining slack in their operations and cause them instead to squeeze every possible dollar of profit out of their company’s assets. With an enhanced opportunity to participate in the benefits, the managers may crack down on unnecessary costs that they formerly tolerated and pursue potential new markets more aggressively than in the past. Regardless of how it comes about, however, improvement in profit margins means higher EBITDA. That, in turn, leads to a higher valuation and generates a profit for the LBO’s equity investors.

As a caveat, analysts must watch out for improvements in reported profit margins that represent nothing more than reductions in investment spending. Following an LBO, a company can report an immediate improvement in earnings by cutting back expenditures on advertising and research and development. Even though the accounting rules do not permit these items to be capitalized, the outlays provide benefits in future periods. Sharply reducing such outlays, or delaying capital expenditures to conserve cash, can impair a company’s future competitiveness, making the increase in current-period earnings illusory. Invariably, LBO organizers either deny that such cutbacks will occur or maintain that before the buyout, the company was plowing more into these categories than the associated benefits justified. In light of the high LBO failure rate of 1980s-vintage LBOs in 1990 and 1991, however, a prudent analyst will be skeptical about such arguments. Today’s profit improvement may be a precursor of tomorrow’s bankruptcy by a company that has economized its way to an uncompetitive state.

Regrettably, the income statement may provide too little detail to determine whether specific kinds of investment spending have been curtailed. Analysts must therefore query industry sources for evidence regarding the adequacy of the company’s investment spending. If the company’s customers report a drop in the quality of service following a leveraged buyout, it may indicate that important sales support functions have been eviscerated. Earnings may rise in the short run, but suffer in the only slightly long term as customers switch to other providers.

2. Asset Sales. As a function of the stock market’s primary focus on earnings, a company’s market capitalization may be far less than the aggregate value of its assets. For example, a subsidiary that contributes little to net income, but generates substantial cash flow from depreciation, has potentially large value in the private market. In that realm, the unit would be priced on a multiple of EBITDA. Alternatively, a subsidiary might be unprofitable only because its scale is insufficient. A competitor might be willing to buy the unit and consolidate it with its own operations. The result would be higher combined earnings than the two operations were able to generate independently. An LBO sponsor who spies this sort of opportunity within a company may invest a small amount of equity and borrow the greater part of the purchase price, then liquidate the low-net-income operations to repay the borrowings. If carried out as planned, the asset sales will leave the acquirer debt-free and in possession of the remainder of the company, that is, the operations that previously contributed almost all of the net income. In the P/E-multiple-oriented stock market, that portion of the company will be worth as much as the entire company was previously. The LBO sponsor may then cash out by taking it public again. After all the dust has settled, the sponsor should have cleared more than enough to cover the premium paid to original shareholders who sold into the buyout.

Unrealized earnings potential and EBITDA multiples are by no means the only valuation factors that come into play in corporate governance controversies. Proponents of policy changes in pursuit of enhanced shareholder value sometimes focus on the values of specific assets identified in the financial statements. For example, oil companies disclose the size of their reserves in their annual reports. Because energy companies frequently buy and sell reserves, and because the prices of larger transactions are widely reported, current market valuations are always readily at hand. If recent sales of reserves in the ground have occurred at prices that equate to $10 a barrel, then a company with 25 million barrels of reserves could theoretically liquidate those assets for $250 million.4 It may be that the sum of $250 million and a P/E-multiple-based price for the company’s refining, marketing, and transportation assets substantially exceeds the company’s current market capitalization. If so, the “unrecognized” value of the oil reserves can be the basis of an alternative method of evaluating the company’s stock.

Would-be corporate restructurers also seek unrecognized value in other types of minerals, real estate, and long-term investments unrelated to a company’s core business. Methods of realizing the value of such an asset include:

■ Selling the asset for cash.

■ Placing it in a separate subsidiary, then taking a portion of the subsidiary public to establish a market value for the company’s residual interest.

■ Placing the asset in a master limited partnership, interests in which are distributed to shareholders.

The key message to take away from this overview of valuation via restructuring potential is that a focus on price-earnings multiples, the best- known form of fundamental analysis, is not the investor’s sole alternative to relying on technicians’ stock charts. There are in fact several approaches to fundamental analysis. A solid understanding of financial statements is essential to all of them, even though factors outside the financial statements also play a role in fundamental valuation.

More on the topic VALUATION THROUGH RESTRUCTURING POTENTIAL:

- Potential Conflict of Interest Situations and the Codes

- 8 The Agriculture EIA Regulations – Rural Land Projects

- POTENTIAL CONFLICT RESOLUTION ROLES FOR FAITH-BASED ACTORS

- Other Forms of Exploitation in the Small-to-Medium-sized Cooperative

- Scaling Worker Cooperatives as an Economic Justice Tool for Communities in Crises

- AN OVERVIEW OF PERSUASION THEORY AND RESEARCH