Beyond markets: critical approaches to microeconomics

As we saw in Chapter 3, the widely accepted assumption is that businesses follow maximizing objectives, whether profit, sales revenue or sales revenue, subject to a minimum profit constraint.

Although we reviewed a range of nonmaximizing or behavioural objectives, we paid little attention to the role of institutions in influencing the context in which both principals and agents (managers) take decisions. This chapter seeks to remedy that deficiency by reviewing the various ‘schools' of economic thought and the different perspectives these bring to the role of markets and prices in providing effective ‘signals' to both produces and consumers in allocating scarce resources amongst alternative uses.Defining ‘institutions' is by no means as obvious as it might appear! North (1990) defines ‘institutions' as including any form of constraints that have been devised by human beings to shape human interactions, whether formal (as in explicit laws and regulations) or informal (as in conventions and codes of behaviour). Such ‘institutions' can be created at a single point in time (e.g. US Constitution or UK Magna Carta) or can evolve over time as increasingly accepted norms of behaviour within a particular ‘community’. In other words, institutions are ‘rules of the game’, whether written or unwritten, but are NOT the same as organizations. Organizations are groups of individuals held together by some common purpose, whether in the spheres of economics (trade unions, employer federations, firms, co-operatives), education (schools, universities, training centres), politics (political parties, regulatory agencies, national/regional/local councils) or social endeavours (churches, sports/social clubs).

Institutions and organizations clearly interact, but the emphasis here is on the written and unwritten rules themselves, i.e. the institutional framework and its relevance to how markets and indeed economies evolve over time, and to how that framework impacts upon individual consumer and producer behaviour.

Of course, this institutional framework plays a key role in determining the types of organizations which evolve and how they operate and develop over time. Before examining the contribution and relevance of institutional perspectives to actual policy-making, it will help to review the approaches of the various ‘schools’ of economic thought as to the role of markets and governments in resource allocation. We look closely at the role of markets in neoclassical perspectives before applying some of the more recent institutional perspectives to real world phenomena which neoclassical approaches have found difficult to resolve, such as gift giving and quasi-internal markets.Classical and neoclassical perspectives on markets

Classical perspectives on the market

For the purposes of creating a benchmark against which the neoclassical and other perspectives on markets can be contrasted, we shall attempt to identify a classical position as to the nature and development of markets by examining the work of key figures within the so-called Classical School. It is widely acknowledged that the ‘economic science’ emerged as a separate branch of knowledge through the combined efforts of the French Physiocrats, Hume and other Scottish philosophers, and in particular with the publication of Adam Smith’s Wealth of Nations (1776). The emphasis within classical economic theory was on wealth creation and economic growth, and therefore on the study of the market mechanisms that might bring about these two objectives, seen as vital for the successful functioning of any society. In this context, terms such as laissez-faire, harmony, selfregulating systems, natural order were introduced into the economic, social and political narratives.

One of the purposes of Smith’s argument was to study the human propensities that incline mankind to a societal form of existence. Smith’s most characteristic ideas concerned the way that man is led by an ‘invisible hand’ to promote ends which were not part of his original intention, i.e.

the ‘unintended outcomes’ thesis. Whilst recognizing markets as the place where the propensity of human nature to barter or exchange is exerted, for Smith markets were seen in a broader context as a preferable alternative to government regulation in supporting wealth creation and economic growth.The Wealth of Nations (1776) arguably provided us with the first coherent treatment of the role of markets within an economic system. Although a staunch advocate of the free market, Adam Smith was not a slavish devotee of the unrivalled ‘power of the market’, and he never suggested that the state can or should be entirely replaced by markets. As Cairncross emphasized: ‘The market was allowed more scope and freedom but the state still determined the framework of law and regulation under which private initiative could be exercised to meet market requirements’ (Cairncross 1978, p. 113).

Smith’s way of describing market forces, the interaction between supply and demand, the formation or adjustment of prices and the sequential ‘movement’ towards equilibrium has shaped modern thinking on markets. Smith introduced two concepts which can be used to analyse price formation, the natural price (i.e. in modern terms the equilibrium price), and the market price (i.e. the actual price of a commodity which covers its production cost). Smith contends:

When the price of any commodity is neither more nor less than what is sufficient to pay the rent of the land, the wages of the labour, and the profits of the stock employed in raising, preparing, and bringing it to the market, according to their natural rates, the commodity is then sold for what may be called its natural price... The actual price at which any commodity is commonly sold is called its market price. It may either be above, or below, or exactly the same as its natural price (Smith A. 1776, p. 36).

The market price can be lower, higher or equal to the natural price which is determined by long- run, underlying structural factors.

By describing the mechanism of market adjustment, Smith engages his analysis with the process of partial equilibrium; this comparative statics method of comparing equilibrium states before and after the adjustments has been used by economists ever since. The argument is extremely simple: if the quantities supplied to the market are smaller than the ‘effectual demand’ for those commodities, not all individuals can actually buy the desired quantities. Some will be willing to pay a higher price than the natural price; as a consequence, depending on competition, the ‘market price’ will rise above the ‘natural price’. In a similar way, if the quantities supplied to the market are greater than effective demand, the ‘market price’ will fall. If the demand is equal to supply, the ‘market price’ will coincide with the ‘natural price’.Smith considers the ‘natural price’ to be a central price towards ‘which the prices of all commodities are continually gravitating’ (Smith 1776). Smith has employed the term ‘constant tendency’ to denote the outcome of economic forces in the economic system. The fluctuations of market prices are governed by wages, profits and rents, and by the stage of development within a society. These influence the circumstances of labour, economic activities, etc., and this position is a more dynamic conception of prices and competition than the one envisaged by neoclassical economics. Smith’s concept of ‘free competition’ amounts to an absence of restriction on the market and freedom of entry; similarly, monopoly means obstacles to entry, the exertion of power over the consumers through the market being under-stocked, thereby raising ‘market prices’ above ‘natural prices’. In conditions of ‘perfect liberty’, the sellers have the possibility to adapt their prices and may exit if the ‘market price’ is below the natural price in the long term.

In other words, Smith acknowledges the existence of monopolies and their tendency to ‘keep the market under-stocked’.

Ricardo (1817) and Mill (1863), in a similar way, defined monopoly as ‘inelastic supply’. With Ricardo, political economy took a major step towards using abstract models, in which the historical, institutional, social or philosophical perspectives were reduced to relatively unimportant issues. The ‘comparative statics’ approach, which did not go uncriticized, became the dominant methodology. The attractiveness of economics as a science, and the certain guarantee of empirical results similar to those to be found within natural science, undoubtedly had an influence upon Ricardo.In sum, therefore, the classical conception of markets can be described as constituting a belief in market systems as a mechanism for creating harmonious order in which individual actions motivated by self-interest are co-ordinated by the ‘invisible hand’ in order to achieve a common good. As the foremost prophet of competition, Smith did not conceive of a perfectly competitive market but advocated a less regulated as opposed to a government-regulated market in order to achieve an efficient allocation of resources.

Classical economists generally had an optimistic attitude towards the market. Of course, a notable exception to this position was Marx, who was sceptical about the merits of co-ordinating economic activities through the market given the nature and inequalities of private property rights. At the same time, and despite their preference towards laissez- faire, the market was certainly not regarded as a ‘perfect’ entity by classical economists!

Neoclassical perspectives on the market

The origins of neoclassical economics are to be found in the marginalist revolution of the 1870s with its shift in focus for microeconomics towards a concern with differential calculus, mathematical economics and the determination of relative prices. Such an approach flourished with the work of Jevons (1871) and was continued by Walras (1877), Edgeworth (1881) and Pareto, amongst others. On this foundation of mathematical precision, a whole analytical apparatus was developed as regards consumer and choice theory, indifference curves and exchange theory.

Indeed, through much of the twentieth century and to the present day, microeconomics has arguably continued to be dominated by marginalism and mathematical formulism.Neoclassical economics would typically claim that society is populated by individual agents whose behaviour is perfectly predictable and who can be regarded as acting ‘rationally’ and without reference to any institutional or social context. Only individuals exist and concepts such as class or society are merely ‘intellectual constructions’. The methodological individualism underpinning this neoclassical approach implies that change and the outcomes of human actions are best understood through the eyes of individual agents.

Shand (1984) defines such methodological individualism as an approach in which ‘all statements about groups are reducible to statements about the behaviour of the individuals composing those groups and their interactions’ (p. 4). Boland (2003) offers a similar definition: ‘Methodological individualism is the view that allows only individuals to be the decision-makers in any explanation of social phenomena’ (p. 31).

Methodological individualism therefore presupposes an explanation of institutions as an outcome of individual actions, in line with conventional assumptions. The central debate seems to be between theorists committed to such methodological individualism (i.e. the individual actors are the central elements in society and social structure is the result and consequence of the interaction of such individuals) and methodological holism (i.e. individual actors are socialized and institutions may be formed which constrain and shape individuals’ capacities and dispositions to act).

Some neoclassical economists have sought to allow for various types of market failure and the role of institutions. Williamson (1975), Coase (1937) and others have emphasized the importance of property rights, transaction costs and other institutional characteristics as influencing individual actors, but the neoclassical framework has arguably remained intact.

Whilst market failures of various kinds and institutional contexts are readily admitted by some neoclassical economists as challenging some of the mathematically oriented marginalist precision, advocates of ‘methodological individualism’ such as North (1990) would respond in the following way:

Although, I know of very few economists who really believe that the behavioural assumptions of economics accurately reflect human behaviour, they do (mostly) believe that such assumptions are useful for building models of market behaviour in economics and, though less useful, are still the best game in town for studying politics and the other social sciences (North 1990, p. 17).

At this point, it will be useful to illustrate some of the central tenets of the neoclassical approach to markets and the role of price as providing ‘signals’ to both consumers and producers to bring about stable and ‘efficient’ resource allocations. Insofar as we can identify a neoclassical approach to institutions, it presumes utility maximization at the level of the individual, stable preferences and the rejection of custom and tradition on the grounds that this might admit ignorance and irrationality. In this context, neoclassical economics is largely unable to deal with issues involving changes in economic and social institutions:

Neoclassical theory implies that economic behaviour is essentially non-habitual and non-routinised, involving rational calculation and marginal adjustments towards an optimum (Hodgson 1988, p. 130).

Consequently, habits and routines that are the product of unconscious decision-making have no place within the neoclassical schema, despite the obvious existence of such forms of decision-making within the real world.

Markets, prices and economic efficiency

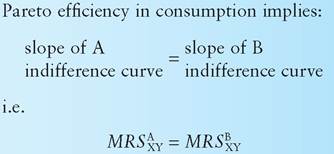

It may be useful at this point to explore the theoretical basis for the belief, particularly amongst neoclassical economists, that markets can coordinate the decisions of innumerable producers and consumers in such a way as to bring about an efficient allocation of resources. The key ‘signal’ available to markets for influencing producer and consumer decisions is, of course, market price. By way of illustration we shall focus on the role of prices in guiding consumer choices so that total utility (satisfaction) of consumers is maximized, with no single consumer able to add to his/her utility without at the same time some other consumer losing utility. This is the Pareto optimal resource allocation, and we return to it in more detail below (p. 170).

For simplicity, we shall begin our analysis by taking a two person and two product model, since by assuming a 2 ? 2 model we can make use of (two-dimensional) graphical analysis. We assume that consumers A and B are active in the market for two products X and Y and that their preferences are expressed by (ordinal) indifference curves which are smooth and convex to the origin. This implies diminishing marginal rates of substitution in consumption between the two products. Consumers are assumed to be independent, in that the consumption pattern of one does not affect the consumption pattern of the other, and to have perfect information as to the prices and qualities of the products traded.

Px = price of product X;

Py = price of product Y

Xa, Xb = quantity of product X purchased by consumers A and B respectively

Ya, Yb = quantities of product Y purchased by consumers A and B respectively

Pareto optimal resource allocation between consumers

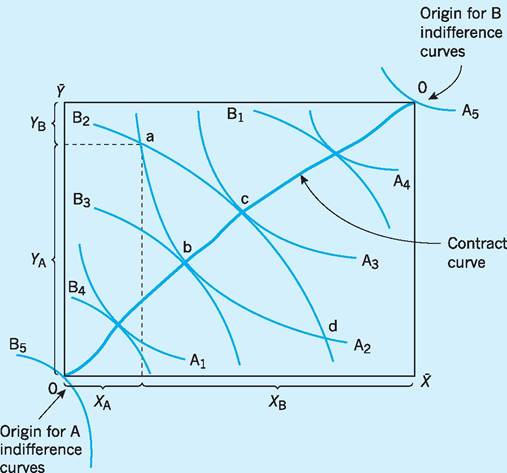

A Pareto-efficient (Pareto optimal) allocation of resources between consumers is said to occur when it is no longer possible to reallocate product outputs between consumers so as to make one consumer better off without at the same time making the other consumer worse off. We first consider what is involved in a Pareto-efficient distribution of products X and Y between our two consumers A and B using an Edgeworth-Bowley consumption box, then we see how prices can bring about such a resource allocation.

The Edgeworth-Bowley consumption box used in our analysis is shown in Fig. 9.1. The lengths of each side of the consumption box are determined by the amounts of products X and Y (X, Y) available for distribution between the two consumers A and B. The more of one product allocated to consumer A, the less is available for consumer B, and vice versa.

The indifference curves of consumer A are plotted with the south-west corner of the box as origin. Each A indifference curve is smooth and convex to this origin, and the furthest indifference curve from the origin (A5) corresponds to the highest level of utility available to A. In this case, all the output of products X and Y available in the economy is consumed by A (and none by B).

The opposite occurs for consumer B; it is as though we construct the same diagram for B then turn it upside down and superimpose it onto our diagram for A. The origin for B is now the north-east corner of the box. Each B indifference curve is smooth and convex to this origin and the furthest indifference curve from the origin (B5) corresponds to the highest level of utility available to B. In this case, all the output of products X and Y available in the economy is consumed by B (and none by A).

This time we use the Edgeworth-Bowley consumption box to identify those distributions of resources which are Pareto-efficient. Only certain distributions of the total product (X, Y) between

Fig. 9.1 Edgeworth-Bowley consumption box.

Source: Griffiths and Wall (2000) Intermediate Microeconomics, Financial Times/Prentice Hall.

consumers A and B are Pareto-efficient. Let us begin by considering the distribution at point ‘a’ in which Xa, Ya is the respective consumption of products X and Y by consumer A. Clearly this distribution is non- Pareto-efficient in the sense that we can redistribute output so as to make some better off and none worse off. For example, if we slide down the A2 indifference curve to point ‘b’, we distribute less product

Y to consumer A but more product X, keeping A’s utility constant (at A2). However, by distributing the residual output to consumer B (now more of product

Y and less of product X is available to consumer B than the combination Yb, Xb at ‘a’), we increase B’s utility (B3 > B2) at point ‘b’. If consumer B is better off and consumer A is no worse off at ‘b’ as compared to ‘a’, then clearly distribution ‘a’ is non-Pareto- efficient.

Note that B3 is the highest attainable indifference curve (furthest from the B origin) in the consumption box given that A remains on indifference curve A2. The distribution at point ‘b’ is clearly a tangency position between the respective A2 and B3 indifference curves and corresponds to a Pareto-efficient distribution of output. Any further redistribution of output along A2 in this direction will take us below and to the right of ‘b’ on A2 which will mean lower utility for consumer B. For example, at point ‘d’ we again have A2, B2 levels of utility for each consumer, and as we have seen B2 < B3.

It should be clear that only tangency positions between the respective indifference curves correspond to Pareto-efficient solutions. The line connecting these tangency positions is called the contract curve. It is therefore distributions of output along the contract curve which alone are Pareto-efficient in the consumption box. You might usefully consider why a redistribution of resources from ‘a’ to ‘c’ would also achieve a Pareto-efficient solution.

Fig. 9.2 Role of product prices in attaining contract curve (Pareto-efficient solutions). Source: Griffiths and Wall (2000) Intermediate Microeconomics, Financial Times/Prentice Hall.

Prices and Pareto efficiency in consumption

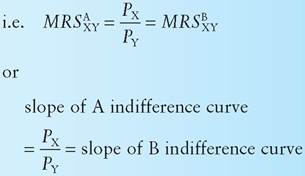

This Pareto efficiency condition in consumption involves the economy attaining an appropriate distribution of output (products X and Y) between consumers (A and B). We now consider how, under our earlier assumptions, prices can provide the signals to consumers to bring about contract-curve distributions of output between themselves.

The slope of a budget line in Fig. 9.2 is given by the ratio of product prices, PX/Py. Provided that consumers face the same price ratios on product markets (e.g. purchase outputs on perfectly competitive product markets) then they will be faced by budget lines of identical slope. To maximize utility consumers must seek the highest attainable indifference curves, given the constraints of income level (position of budget line) and product prices (slope of budget line). In Fig. 9.2(a), if M1 is the income level of consumer A, and PX/Py the ratio of product prices, then I2 is the highest level of utility attainable, where the budget line (M 1) just touches (is a tangent to) the indifference curve furthest from the origin. This implies consumer A purchasing the combination X1, Y1 of the respective products. Similarly in Fig. 9.2(b), if M 2 is the income level of consumer B, and PX/Py the ratio of product prices, then I3 is the highest level of utility attainable, where the budget line (TM2) is a tangent to the indifference curve furthest from the origin. This implies consumer B purchasing the product combination X2, Y2.

Without any conscious co-ordination between consumers, but simply by individually seeking their own utility maximizing solutions, the two consumers have achieved a contract-curve distribution of resources (here the allocation of products between consumers). Provided only that they face the same product price ratio (PX/Py), they will have equated the slopes of their respective indifference curves; i.e. they will be at a solution such as ‘b’ or ‘c’ in the earlier Fig. 9.1.

It is product prices which act as the signal to induce consumers to select distributions of products X and Y between themselves (resource allocations) which are Pareto-efficient.

The above analysis has been expressed in terms of product prices and consumers. However, the Edgeworth-Bowley production can be used to show how factor prices (wage rate w and interest rate r) can act as signals to profit-maximizing producers to allocate factor input (labour and capital equipment) between the two producers in a Pareto-efficient way.

General equilibrium and ‘efficiencies’

Whilst it was readily admitted that the ‘invisible hand’ in the form of price signals could result in equilibrium outcomes in single markets, there was a problem in extending this equilibrium yielding property of the price mechanism to all markets simultaneously! This became known as the problem of achieving a ‘general equilibrium’ solution across all product and factor markets simultaneously.

This issue of achieving a general equilibrium through the price mechanisms ‘clearing’ all markets simultaneously also became linked with the idea of ‘efficiency’, with the so-called ‘Pareto optimal’ resource allocation seen as a ‘holy grail’ in which resources (both products and factors) would be allocated in such a way that it would no longer be possible to redistribute an extra unit of resources to make one consumer or producer ‘better off’, without at the same time making some other consumer or producer ‘worse off ’. If you could redistribute resources to make someone better off without making anyone worse off, then clearly you should do so as total ‘welfare’ would then rise!

The subsequent work of Arrow and Debreu (1954) was seen by many as actually attaining this ‘holy grail’ by the autonomous actions of individuals guided by self-interest and market signals alone. Arrow and Debreu showed mathematically that if certain competitive conditions were present in markets, then individual agents (consumers and producers) would, without prompting, take self-interested decision in allocating resources such that a Pareto optimal efficiency condition would be inexorably attained. More specifically, Arrow and Debreu showed that, if certain conditions hold, then a set of prices will result across the product and factor markets such that aggregate supplies will match aggregate demands for every commodity. Nor would any overall ‘planner’ be needed to achieve this efficient ‘general equilibrium’. Self-interested decision-making by the individual ‘actors’, consumers seeking to maximize utility and producers seeking to maximize profit, will bring about this efficient general equilibrium, provided only that the appropriate market conditions hold! The task of governments then reduces to the minimalist one of ensuring the existence of such conditions - no other co-ordinating effort is required of governments!

However, these necessary conditions are by no means ‘trivial’! They required perfect product and factor markets, full and accurate information to all market participants, no externalities in consumption or production, maximizing behaviour by consumers and producers, convexity assumptions ensuring diminishing returns in consumption and production, amongst others. Of all the subsets of opinion within the neoclassical paradigm, the ‘Chicago School’ has often been identified as holding most closely to the use of unfettered markets in resource allocation.

Chicago School

Based around the University of Chicago, this ‘School’ is seen by many as the full embodiment of the neoclassical approach, with its resolute application of the assumptions of maximizing behaviour, market equilibria and stable preferences, in a world with few, if any, admitted ‘market failures’! Becker (1981) saw no limit to the areas in which ‘rational economic decisions’ using such microeconomic assumptions, could be usefully applied, as indicated by the following extract from his speech on receiving the Nobel prize for economics.

In the early stages of my work on crime, I was puzzled by why theft is socially harmful, since it appears merely to redistribute resources, usually from richer to poorer individuals. I resolved the puzzle by pointing out that criminals spend on weapons and on the value of their time in planning and carrying out their crimes and that such spending is socially unproductive (Becker 1981)

The emphasis here is on rational, self-interested calculations being the driving force behind all decision-making, and that ethical values such as ‘honesty’ will only be a market outcome if it can be shown to yield larger ‘payoffs’ to the various ‘actors’ than dishonesty.

Nor does the Chicago School even recognize the existence of ‘market failures’! Markets are seen as incapable of failing - and that whilst individuals and businesses may (falsely) perceive such failures - the ultimate outcome can still be modelled using the assumption of ‘rational expectations’, i.e. where consumers and businesses are assumed to behave ‘as if’ they had access to all available knowledge and are capable of making precise (marginalist) calculations on that basis!

The fundamental tenet of the Chicago School is that competitive markets have ‘efficiency properties’ that no other institutional system can possible attain! The Arrow-Debreu work on general equilibrium was seen by Chicago School adherents as the ultimate vindication of this perspective!

Role of the state in neoclassical economics

Whilst the degree to which ‘market failure’ is accepted as actually occurring varies widely amongst neoclassical economists, most accept that the rigorous conditions advocated for a spontaneous general and competitive equilibrium do not, in reality, exist. In other words we are often, in reality, in a ‘second best’ world where pragmatic policy-making has a role to play which might differ from the simple presumptions of a ‘first best’ model in which no market failures occur. Here we provide some insights into the (less extreme) neoclassical perspective that the state’s main role is to seek, wherever possible, to correct any market imperfections or failures which might distort the price signals given to consumers and producers and thereby prevent the market from co-ordinating decision-making and increasing economic ‘efficiency’!

Imperfect information

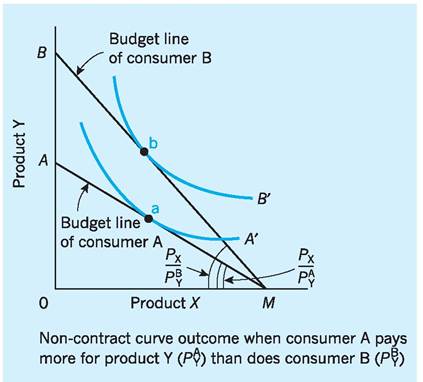

We can use our earlier analysis of prices and consumer behaviour to illustrate the typical neoclassical perspective as to the main role of the state being merely to ‘correct’ any deviation in the set of conditions necessary for general equilibrium. The policy prescription for government intervention in this case is to help restore ‘perfect information’ to market participants as to the true prices prevailing on product markets. Figure 9.3 shows how imperfect information in product markets means that prices would no longer be able to act as appropriate signals for bringing about a contract-curve (Pareto-efficient) solution in terms of the Edgeworth-Bowley consumption box. Remember how we noted (p. 170) that simply by maximizing their own utility subject to the product prices they faced and the incomes they possessed, consumers would equate the slopes of their respective indifference curves and bring about a contract-curve solution. In Fig. 9.3, however, the absence of such perfect information means that consumer A maximizes utility subject to a different set of product prices than those faced by consumer B.

Suppose consumer A is less aware (perhaps via less search activity) of the availability of a cheaper source of product Y than is consumer B, so that consumer A faces a higher price for Y and therefore a lower product price ratio (Px∕Py) than does consumer B. This implies a flatter budget line (AM) for consumer A than for B. Clearly from Fig. 9.3 we can see that in maximizing utility by equating their respective

Fig. 9.3 Imperfect information as to prices and market failure.

Source: Griffiths and Wall (2000) Intermediate Microeconomics, Financial Times/Prentice Hall.

Note: For diagrammatic simplicity we assume a given income for consumers A and B.

budget lines with the highest attainable indifference curves, consumers A and B are in a non-contractcurve situation. In other words, imperfect information as to product prices means that price signals fail to bring about a (first best) Pareto-efficient allocation of resources in product markets as regards consumers (via exchange).

Figure 9.3 is drawn on the assumption that both consumers have identical incomes, but differential access to information as regards the price of Y. This simplifying assumption results in the respective consumer budget lines having the same intercept on the horizontal axis (i.e. M). It also helps to illustrate the welfare loss to the consumer possessing imperfect information. For example, if consumer A were to receive the same product price information as consumer B, then his/her budget line would pivot from AM to BM and he/she would be able to attain a higher indifference curve (such as B').

Institutionalist perspectives on markets

The aim of this section is to assess the contribution of the Institutionalist School to the development of the theory of markets and prices. Here we will focus on the basic contribution of this ‘school’ to the understanding of markets, and to the process of price formation, reviewing the work of the authors who represent the ‘core’ of institutional economics such as Veblen (1899), Ayres (1951), Commons (1931) and Mitchell (1927). In addition, we shall also explore later thinkers who have written in this tradition such as Galbraith (1952), Means (1962) and more recently Hodgson (1988).

In order to arrive at an institutionalist conception of markets, it is necessary to examine key themes within institutionalist writing that are pertinent to their views on the nature and operation of markets. It is broadly accepted that the use of the term institutionalism as a school of economic thought was first proposed in 1919 by Walter Hamilton in a paper presented at the Thirty-first Annual Meeting of the American Economic Association. Hamilton identified the concern of institutionalism as ‘the customs and conventions, or, if you please, the arrangements, which determine the nature of our economic system’. Hamilton went on to argue that economic theory should be based upon an acceptable theory of human behaviour, grounded in a modern theory of psychology.

Although a number of economic and social theorists are identified as having an interest in institutional approaches to economics (e.g. the German Historical School, Marx and Menger), Veblen is widely credited with being the founder of institutional analysis, and he criticized the dominant neoclassical concept of the individual whose preferences are exogenously given and the failure of neoclassical economics to recognize the importance of the role of institutions as embodying tradition, customs and habitual behaviour. According to Veblen (1899, p. 373), ‘economics is helplessly behind the times, and unable to handle its subject matter in a way which entitles it to stand as a modern science’. The main reason for this situation lies in a ‘faulty conception of human nature’, which is static and hedonistic (i.e. seen as passive and inert). Veblen considered that economics should study the processes of human behaviour rather than assuming that pleasure and pain, utility and satisfaction are the ‘real drivers’ behind human behaviour.

Veblen further suggested that where a habitual way of thinking and acting becomes a persistent element in the culture of a group or society, then it takes on the concrete form of an ‘institution’, i.e. a settled habit of thought common to all individuals and that this will then influence individual behaviour. Formal and informal ‘institutions’ and organizations from the past can always be found in the present. Such ‘institutions’ and organizations are capable of changing but also of enduring through time, a view endorsed by both Veblen and Ayres.

Commons (1931, p. 648) reinforced this emphasis on institutions rather than individuals, seeing an institution as a ‘collective action in control, liberation and expansion of individual action’. They determine what an individual can or cannot do; and they can establish positive and negative freedoms or liberties as regards individual actions. An institution ‘indicates what individuals can, must or may do or not do, enforced by collective sanctions’ (Commons 1931, p. 649), with the sanctions on individual behaviour resulting from ‘disobeying’ the accepted norms of behaviour having important economic, ethical and legal implications.

The analysis of markets as particular ‘institutions’ governed by certain ‘working rules’ in the form of legal, economical and cultural conventions and norms has been implicitly present in the Institutionalist School. We say implicit because despite extensively discussing the classical and neoclassical conception of exchange, value, market and prices, they have neither provided an alternative systematic approach to market analysis, nor set out the theoretical and methodological consequences of seeing markets as specific historical and cultural institutions. More recently, the analysis of markets as social institutions has been considered by Hodgson:

We shall here define the market as a set of social institutions in which a large number of commodity exchanges of a specific type regularly take place, and to some extent are facilitated and structured by those institutions. Exchange, as defined above, involves contractual agreement and the exchange of property rights, and the market consists in part of mechanisms to structure, organize, and legitimate these activities. Markets, in short, are organized and institutionalized exchange (Hodgson 1988, p. 174).

Portraying markets as a diverse body of ‘institutions’ and organizations makes us consider issues such as the values and norms embedded in these institutions and organizations (e.g. in the stock market), or in the associated legal structures (e.g. legal rules which govern contractual interactions). In this institutionalist perspective, market processes evolve and market forces, such as expectations or conventions on prices and legal rules, adapt and change. To many, the fall of the Berlin Wall finally emphasized that markets as institutions have proved to be the most successful form of human organization - a line of argument that falls within the central premise of Francis Fukuyama’s End of History (1992).

Hodgson (1988) attempts to outline a number of theoretical implications that can be derived from the institutional approach to markets.

■ The institutional view of markets argues against the classical view of markets as being a natural order and an aggregation of subjective preferences in an institutional vacuum; instead, all exchanges take place and interact within an institutional context.

■ The institutional view advocates the endogenous nature of institutions, with institutions playing a central role in economic development and economic analysis, rather than being exogenous to such development and analysis.

■ Markets are a means for transmitting information and knowledge, but they also have a transformational role, shaping individual behaviour, beliefs, preferences or cognitive processes.

■ Markets are specific, cultural institutions, reflecting historical and locational contexts and not a universal and uniform context for human interaction.

These considerations provide a powerful critique of the mainstream neoclassical conception of markets, and arguably constitute an emerging paradigm which differs from the static, non-evolutionary and individualistic character of previous economic doctrines.

Whilst not easily falling within the remit of any single approach, it may be appropriate to reflect on the tenets of the Austrian School under the institutionalist rather than the neoclassical perspective.

Austrian School

The origins of the Austrian approach can be found in the ideas of Menger (1871), although his work also emerged as part of the marginalist movement on which neoclassicism was grounded. Whilst Menger’s intention was not to build any particular school of thought, his focus and methodologies clearly exerted considerable influence on the research agenda of those theorists who followed and became known as representatives of the so-called ‘Austrian School’, including Hayek (1948), von Mises (1949) and Schumpeter (1908, 1991) amongst others. As Boettke and Leeson (2003) state, the contributions initiated by Hayek and von Mises in the 1940s have been slowly transformed into a heterodox, alternative perspective to mainstream economics.

Attempting to identify the essential characteristics of the Austrian School is not an easy task. According to Shand (1984), one of the biggest differences between the Austrian method and the neoclassical one is subjectivism, i.e. its emphasis upon individual choices and actions as inherently problematic to predict, and which cannot be presupposed as ‘given’ and therefore are not capable of being modelled and measured by mathematics or econometrics. Austrian School adherents therefore have ‘doubts’ about the validity and importance of much empirical work in economics.

Some of the key areas in which the Austrian School adopts a dissenting voice to neoclassical economics involve the principles underlying the treatment of economic behaviour and institutions. As Vaughan (1999) emphasises, ‘the key to economic order in Hayek’s later writings is found in the role he sees for institutions as repositories of social learning’ (Vaughan 1999, p. 130). Institutions are social arrangements that seem to possess a ‘wisdom of their own’ and, although not designed intentionally, they are the outcome of human action aimed at individual purposes. The most controversial statement came from Hayek in the context of the cultural transmission of rules: a spontaneous system of rules will be more efficient precisely because natural selection determines which rules and institutions are appropriate. Society progresses, in Hayek’s view, by continually adapting to the rules emerging in new circumstances. Underlying both Menger’s and Hayek’s institutional theory seems to be the ‘actioninformation loop’, i.e. institutions transmit information and signals to individuals, whose actions both reinforce the goal set of institutions but also have the potential to change that goal set over time. One of the criticisms levelled at Hayek’s view of human action and adaptation was called ‘the self-referential inconsistency’: ‘He (Hayek) sees human action as governed by general rules that people have not chosen; they are just adopted. Nowhere in his analysis is there apparently any room for free will; human behaviour is mostly outside human control’ (Shand 1984, p. 10).

Gift giving and trust

The institutionalist approach to markets would seem better attuned to explaining increasingly important phenomena in modern societies, including altruism in the form of gift giving and trust, as compared to more market-oriented paradigms. Neoclassical views tend to regard the market as primarily an exchange mechanism, guided by the prices of products or factors of production, by the self-interest of utility-maximizing consumers or profit-seeking producers, and by the initial endowments of income or resources to the respective market participants. Motives such as altruism, which is the basis of gift giving or trust, have proved difficult for the fundamentally exchange-oriented perspective of the market mechanism to explain or predict. However, our institutional perspective has permitted new insights into gift giving and other, non-exchange related actions by market-participants.

Markets have always exhibited a wider economic and social role than that prescribed by the conventional view of markets as simply exchange mechanisms. Economists, anthropologists and historians have been inclined to suggest that the spheres of the market and gift giving are in complete opposition, with many adopting the conventional linear image of historical development in which market relations systematically displace gift relations as economic systems ‘mature’ (Hicks 1969). The analysis below challenges this conventional view, using giving as an example. ‘To give’ implies to transfer or to deliver voluntarily to another person something over which you have control or property rights. We define gift as a transfer motivated by altruism. The magic of gift is altered once there is an expectation of returning the gift. Accordingly, a gift may be thought of as a transfer, either material or non-material, between individuals, from an individual to a group, from a group to an individual, or from a group to another group. As we can see in modern economics, the role of gift giving is increasingly prominent in the form of the high-profile foundations of Bill Gates, Warren Buffett, Bill Clinton and others, or by the gifts given by millions of private citizens in remitting income back home, or in the gifts given as a response to disaster appeals, or in numerous other ways. Such gift giving is an increasingly important part of economic and social life.

However, within economic theory, there is a long tradition of assuming that human behaviour is inherently selfish. This is manifest in the conventional economists’ preoccupation with individual optimizing behaviour. One argument for retaining self-interest as the behavioural baseline in economic analysis derives from Adam Smith’s concept of the invisible hand, taken much further by neoclassical economists, resulting in the claim that ‘efficient’ resource allocation can best be achieved via competitive interactions among self-interested individuals (Collard 1978). Theorems on efficiency attainment via self-interested behaviour in competitive markets yielding a Pareto- optimal general equilibrium tend to be based on denying any role to altruistic goals or preferences. Yet contemporary game theory (see Chapter 6) has shown a wide range of circumstances in which competitive markets do not yield optimal allocations. An efficient market may require cooperative behaviour and trust.

However, not all economists are convinced that economic analysis would be advanced by including gift giving and altruism as part of our understanding of a market-based system. Becker (1981), for instance, has argued that altruism can be present in families or households, but is not a market characteristic. Becker argues that since members of the family maximize the utility of the oikos (the household), altruism is nothing but family-oriented self-interest. Even when economists such as Akerlof (1984) apply a model of gift exchange to examine the relationship between workers and firms as part of the process of wage determination in the labour market, his analysis closely resembles a form of reciprocity rather than gift (in the sense used here). In the neoclassical approach espoused by Akerlof (1984), there is no advantage to pay a higher wage than the marketclearing wage. In a gift economy, which functions on norms related to gift, there is the perception that benefits may occur by producers paying a higher wage, sellers accepting lower prices or buyers agreeing to pay higher prices in order to maintain a relationship.

Recent studies in economics have revisited the self-interest axiom. Studies such as charitable giving and intergenerational transfers (e.g. Andreoni 1989, 1990), voting (e.g. Mueller 1989, 1997), and voluntary tax-paying (Meier 2006) have argued that such actions cannot only be explained by using the selfishness paradigm. Rather the reciprocity model has gained status especially in experimental economics and the theory of games (Kolm 1984, 2000; Fehr and Schmidt 1999; Fehr and Gachter 2000). Meier (2006), who has made some valuable contributions to the theory of pro-social behaviour (i.e. behaviour that systematically deviates from self-interest), has argued that despite previous findings, contributions to public goods are possible without government intervention, and institutions need to be designed to foster and encourage pro-social behaviour. For a pro-social behaviour, the institutional environment in which people decide to contribute time and money to public goods is crucial and can influence intrinsic motivation to behave pro-socially. Meier (2006) concludes:

The good news is that the prospect of people behaving pro-socially does not look so gloomy as is often predicted by economic theory. People deviate systematically from the self-interest hypothesis by contributing money and time to public goods. The bad news is that they do not always do so. In certain situations, people are not willing to contribute to a good cause and hence the public good is not provided in a socially optimal amount (Meier 2006, p. 135).

and

The good news that people behave pro-socially is bad news for orthodox economists, who are reluctant to accept that standard economic theory is limited and sometimes purely wrong in predicting behaviour (Meier 2006, p. 138).

What has been less discussed within the literature is the persistence of earlier non-market forms of transfers and exchanges into modern times. Different forms of exchange such as reciprocity, redistribution and market exchange were certainly present (although in a different guise to those existing within modern society) in pre-modern economies. In modern times, the persistence of some non-market exchanges suggests that the potential co-existence of markets and gift is not simply a historical relic. For example, reciprocity and gift giving have been identified as important components within the workplace (e.g. Akerlof 1984). The current systems of organ and blood donation based upon altruistic acts have supplanted the failed market mechanisms previously put in place to regulate the allocation of these scarce resources (Titmuss 1970: 205). Gift transfers are to be found in many spheres, including organ donations, charity and philanthropic contributions, bequests and so on, with the voluntary character of these personal relationships (Godbout 1998) deciding what is left at the level of the individual and what at the level of market and state, with the co-existence of market and gift being seen as a contribution to social order and social harmony. As Elster points out (1989: 287) ‘altruism, envy, social norms and self-interest all contribute, in complex, interacting ways to order, stability and cooperation.’

Institutional pluralism or heterodox perspectives

Political economy as constructed by Smith and others perceives selfish behaviour, mediated via the mechanism of the market, as the process by which social harmony emerges within societies. Markets based upon self-interested forms of exchange are then constructed as the central arena within which economic activity emerges and takes place. Meier (2006), however, argues that pro-social behaviour also contributes to social harmony and contends that it is more important to examine the institutional context within which pro-social behaviour emerges and is fostered. If we conceive of markets and gift as being the product of the institutional context from which they spring, then this places ‘institutions’ such as values and norms as the central feature of economic activity, rather than the market. The economy then becomes a multi-faceted mixture of economic and social institutions for which a pluralistic or heterodox outlook is required, both in terms of recognizing the importance of different institutions and organizations and for coping with the diversity that results.

Economic diversity, or plurality, should be a theme common to any discussions on past and current economic systems. Diversity occurs over time and space and different institutional arrangements create distinct market logics. The institutional settings, the state, the market, and other socio-economic institutions interact with one another to create different national economic processes. The kind of diversity that is relevant here is not reducible to a unique, universal model of development. Take the case of China: it is commonly viewed as an economy and society that is striving towards a system led by the market. Yet China has particular forms of institutionalized behaviour, both formal and informal, such as the network of gifts or guanxi. These institutional arrangements are not deviations from a universal market norm, but rather behaviours that deserve to be analysed in their own right. Such elements of diversity have often been viewed by neoclassical economists as temporary outcomes of the transition phases from one development stage to another. The strong counter-argument of institutionalists is that diversity should be perceived as a permanent attribute of economic and social development over time. Norms, institutions and rules emerge, develop, change and breakdown continuously. Our investigation of economic systems should not be limited to a single market-oriented dimension and the role and place of gift and institutional behaviour in modern economic systems should be acknowledged. This more pluralist or heterodox view of economic development is taken further in Chapter 29.

Irrationality assumptions

Analysts of organizational behaviour are increasingly emphasizing non-rational and behaviourally oriented decision-making, rather than the ‘rational economic agents’ of the Neoclassical schools:

We are finally beginning to understand that irrationality is the real invisible hand that drives human decision making................................................. cognition biases

often prevent people from making rational decisions, despite their best efforts (Ariely 2009).

The integration of economics with psychological and sociological approaches is resulting in an increasing challenge to the fundamental neoclassical assumption of markets populated by rational economic agents!

The experimental work of Ernst Fehr involving ‘the trust game’ usefully illustrates the importance of trust and other psychological traits in actual decision-making.

The Trust Game

A group of Swiss researchers led by Ernst Fehr conducted an experiment now known as ‘the trust game with revenge' that reveals a lot about the motivation for vengeance. It goes something like this: You and an anonymous partner are each given $10, and you get to make the first move. You must decide whether to send your money over to your partner or keep it for yourself. If you keep it, each of you gets your $10 and the game is over. If you send it, the experimenters quadruple the amount to $40 - so now your partner has $50.

The obvious question is: why would you give away your $10 in the first place? The answer is that you hope you can trust your partner when he makes the next move. He can choose either to keep the $50 - leaving you with nothing - or send $25 back to you, so that you share equally in the spoils.

If your partner is acting rationally and in his own best interest he would never send you the $25. Knowing this, and acting equally rationally, you would never send him the money to start with. It follows that you will do nothing and go home! The good news is that people are more trusting and reciprocating than standard economic theory would have us believe. In the experiment, many people gave away their $10, and many partners reciprocated by sending $25 back.

But the Swiss game didn't end there. If your partner chose to keep the $50, the experimenter would give you an opportunity in the next phase of the game to use some of your own money to punish him. For every dollar you spend, your greedy partner loses $2. So if you decided to spend $25, your partner would lose all his winnings. You might think that people who had just lost some money would be unwilling to lose even more just to ‘get their own back'. Seated comfortably right now, you might not be able to appreciate these feelings, but most of the people who were given the opportunity exacted severe revenge on their greedy partners.

This finding was not the most interesting part of the study, however. While the participants were making their decisions, their brains were being scanned by positron emissions tomography (PET). The experimenters saw activity in the striatum, the part of the brain associated with experiencing reward. In other words, the decision to punish the greedy partners appeared to be related to a feeling of pleasure. What's more, those who had a high level of striatum activation punished their partners to a greater degree. This suggests that the desire for revenge, even when it costs us something and is fully irrational (you have no idea who this other person is, and you will never meet him again), has biological underpinnings.

Ariely 2009, p. 83

Quasi-markets

The influence of written and unwritten ‘rules of the game’ (institutions) and of organizations on actual market behaviour are clear when we examine the so- called ‘internal’ or ‘quasi’-markets that have developed in particular economies at particular points in time. In the UK, the ‘internal’ market and associated ‘rules’ which have developed within the organization known as the National Health Service (NHS) provides a useful illustration of the institutional, as opposed to the neoclassical approach to markets.

Creating an internal (quasi-)market in the National Health Service (NHS)

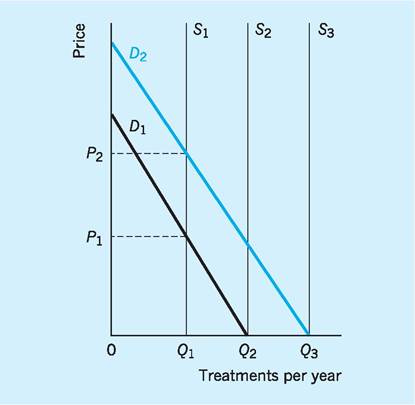

The contemporary structure and developments in the health care sector are reviewed in some detail in Chapter 12 and will be seen to embody key elements of the narrative below. The mandate of the NHS is to provide health care services according to need, free at the point of delivery. It was, and continues to be, financed from central government tax revenues via the Consolidated Fund. Some 80% of funding is via these tax revenues with another 14% via a proportion of the National Insurance contributions of employers and employees, with only around 4% of NHS receipts currently funded via charges for prescriptions, dental services, etc. The consequence for resource allocation of providing health care services

Fig. 9.4 Demand and supply of healthcare.

essentially free at the point of delivery can be discussed using Fig. 9.4.

We assume demand for health care services to be downward sloping with respect to price, i.e. people demand fewer treatments per time period if price rises. If a market were established with demand D1 and a short-run supply S1 (here perfectly inelastic supply), then a price P1 would be established with an equilibrium number of treatments demanded and supplied per year of Q1. If demand now increases to D2, then price adjusts in the market, rising to P2 to allocate the unchanged Q1.

However, the NHS does not operate by price adjustment but by quantity adjustment (since service is free at the point of treatment); with the initial demand D1, at a zero price 0Q2 treatments are demanded. This requires the supply curve of treatments to shift rightwards to S2 if the NHS is to satisfy this demand. If demand now rises to D2, supply must further increase to S3, since no price adjustment is permitted, otherwise Q3 - Q2 patients would be untreated, leading to a rise in waiting lists. It is clear that by relying mainly on quantity adjustment, the NHS must either allocate more resources to health care in the face of increased demand or accept a rise in waiting lists.

In April 1991 the then Conservative government introduced major changes into the UK health care market. The responsibility for purchasing health care was to be separated from the responsibility for providing it. According to the White Paper preceding the 1991 reforms, the health service reforms were intended to achieve two objectives, namely: to give patients, wherever they live in the UK, better health care and greater choice of the services available; to give greater satisfaction and rewards for those working in the NHS who successfully respond to local needs and preferences.

These objectives were to be accomplished by the implementation of a number of key measures.

1 Increased delegation of responsibilities from central to local levels, for example the delegation of functions from Regions to Districts, and from Districts to individual hospitals.

2 Certain of the larger hospitals were invited to apply to become NHS Hospital Trusts. Trust status would permit the hospital increased freedom of action in terms of local pay settlements, easier access to borrowing, more choice in deciding upon output mix (e.g. types of speciality) and new opportunities to retain profit. There would then be hospitals managed directly by the District Health Authority (DHA) and hospitals with NHS Trust status.

3 All hospitals in the future were to be free to offer their services, at agreed prices, to any DHA in the UK, and to the private sector. Previously hospitals within a given area normally treated only patients originating from within that area.

4 A facility was to be provided for the larger general practices to hold and operate their own budgets, for the purchase of services directly from hospitals and to cover drug prescribing costs. This meant the creation of a new category of General Practitioner Fund Holders (GPFH). For smaller practices the general practitioners (GPs) could combine to form various types of commissioning groups, purchasing on behalf of individual GPs within such groups.

Note that the internal market established in 1991 was not a private market in the normal sense. It was not the patients who were to make the purchasing decisions, as they do in the case of US health care, for example; rather it was the DHAs and the GPs who were to have the spending power, allocated to them from the Regional Health Authority (RHA) or, as in the case of the GP Commissioning Groups, allocated to them from the DHA. On the basis of this budget allocation, the purchaser can then effect a health treatment on behalf of the patient in any one of three ways. Treatment may be purchased first, from a (managed) hospital administered by a DHA; second, from a hospital with Trust status; or third, from a private sector hospital, i.e. one totally outside the NHS.

The Conservative government argued in 1991 that the introduction of competition on the supply-side would encourage efficiency. Providers competing for contracts with purchasers would have to be efficient or face a possible loss of business. Purchasers, because they had finite budgets, would have incentives to seek out efficient providers. The government also argued that this system would increase patient choice. Table 9.1 outlines this separation of purchasers and providers, which is also very much a part of health care reforms in 2010 as we note in Chapter 12.

Table 9.1 Purchasers and providers of health care.

| Purchasers | Providers |

| District Health Authority | NHS Trust hospitals |

| (DHA) | |

| GP Fund Holders (GPFH) | District managed hospitals |

| GP Commissioning Groups | |

| Private patients | Private hospitals |

However, the efficiency benefits claimed for this internal (quasi-)market in health care depend upon the ‘signals’ or incentives given to both providers and purchasers and the nature of their likely response to such signals. We now consider this in more detail: first, the incentives to purchasers; second, the incentives to providers.

Incentives to purchasers

District Health Authority (DHA)

As purchasers, districts were to be responsible for assessing the health care needs of their populations, prioritizing needs, developing contracting arrangements for the services they wish to purchase, and monitoring provider performance. They received a budget, which was a function of the number and age of the persons for whom they were responsible.

The incentives for increased efficiency facing DHAs were, however, rather limited. There were no direct sanctions for failing to meet the needs of their consumers. Managers were not rewarded on the basis of health care outcomes and so were not directly rewarded for doing what the new system intended them to do. It was relatively costly for districts to gather information about the outcomes of care from different providers since they had no direct contact with patients. This high cost of acquiring information meant that at the margin, districts probably undercollected such information.

General Practitioner Fund Holders (GPFH)

Alongside districts, the 1991 reforms gave larger general practices (providers of primary care) the opportunity to become fund holders and to assume a purchasing role. The financing for this role came from top-slicing part of the budget of the DHA in which the fund holding practice was located. Fund holders were free to place contracts with whichever hospitals they wished, and in some cases to substitute their own services for existing ones, e.g. they could now offer minor surgical procedures directly.

GP fund holders had more discretion than nonfund-holding GPs about how and when their patients were treated. They had better access than the DHAs to information about the outcomes of care from different providers, since they saw patients both before and after treatment. The costs of gathering information were therefore lower and, in this respect, fund holders were likely to be more efficient than DHAs in acting as consumers’ agents.

Competition on the purchasing side between agents rather than individuals may arguably have given purchasers the incentive to be more responsive to patient needs. However, it may also have increased the risk of ‘cream skimming’. This is because each purchasing agent - DHA, GPFH or Commissioning Group of smaller GPs - receives a sum of money per person for whom they were responsible, adjusted for age. General Practitioner Fund Holders were, as we have noted, in a good position to identify directly any ‘bad risks’, i.e. patients who were likely to require recurrent health care. They could then reject these ‘bad risks’ from their list of patients, thereby reducing costs. In contrast the DHAs had to treat all patients, so that the pool of patients available to them may have become over-represented by those deemed ‘bad risks’ (i.e. adverse selection). Many saw the risks of a two-tier system developing in which healthier patients would receive priority treatment from GP fund holders.

Incentives to providers

The providers were to be the NHS managed hospitals, NHS trust hospitals and private hospitals. The difference between the first two, the directly managed hospitals under DHA control and the trust hospitals responsible to the Department of Health, was mainly in terms of the greater contractual freedom of the latter. Trust hospitals could set their own pay scales, and decide themselves on the quantity and mix of factor inputs and types of specialism they offered (output mix).

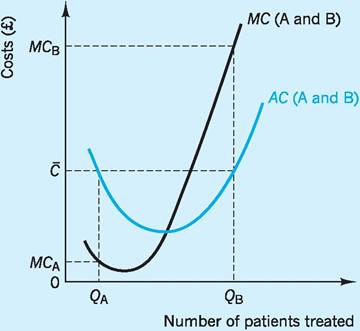

Neither managed nor trust hospitals could make a profit on their services. Prices had to be based on average cost, with no cross-subsidies or price discrimination. However, this average cost pricing policy could itself lead to inefficiencies. In Fig. 9.5 we assume, for simplicity, that two hospitals, A and B, have identical average and marginal cost curves. We can see that although each hospital treats a different number of patients, they each have the same average cost in a situation where Qa treatments take place in hospital A and Qb treatments take place in hospital B, and therefore both hospitals charge the same price according to the earlier directive on average cost pricing. However, an efficient allocation of resources (patients) would be one which allowed hospital A to charge a lower price than B, since scale economies are

Fig. 9.5 Problems with average cost pricing.

still potentially available to A which would reduce average costs with extra treatments (unlike hospital B where average costs would increase with extra treatments). This lower price would then attract patients to hospital A which can provide treatment at a lower (average) cost than hospital B. Therefore the regulation insisting on average cost pricing did not permit the (quasi-)market for health care to send appropriate signals to patients. Resource allocation would then be inefficient where patients (or their agents) chose the identically priced hospital B rather than A. (Note that a marginal cost pricing principle would be more appropriate here - since MCa at Qa < MCb at Qb.)

Put another way, the internal market was not structured in such a way as to allow profit signals on particular activities to guide resource allocation. Even if such profit signals had existed, the fact that all three types of provider (including even the private hospitals) may not have followed a clear profit-maximizing objective might have deflected them from reacting ‘appropriately’ to the profit signals. It is sometimes argued that the publicly owned managed and trust hospitals are dominated by senior managers or medical staff who seek ‘breakeven’ targets, rather than maximum profits. Such non-profit-maximizing objectives may even extend to private hospitals, some of which have charitable status. It can hardly be surprising if non-profit-maximizing hospitals fail to respond to profit-related signals in ways predicted by economic theory, even when such profit signals are transmitted in the market!

Another criticism of the operation of the internal market was that funds did not always follow the patient immediately, the result being that the efficient providers have sometimes been unable to treat more patients even when the demand has been there, since they have run out of funds. As a result, treatments have had to cease in some ‘efficient’ hospitals once their initial targets have been met.

Characteristics of an internal market and health care provision

It may be that certain aspects of the 1991 reforms establishing an internal market were unlikely to succeed because of intrinsic characteristics of the market for health care provision. For example, competition is likely to yield efficiency gains only where excess capacity exists in a market. This is hardly the case in health care provision where almost all indicators point to under-supply (i.e. excess demand). In a case of under-supply in a pure market, price will allocate the restricted supply amongst the competing consumers (see Fig. 9.4). In a quasi-market, where regulations of various kinds are imposed which prevent a ‘pure’ price adjustment, an element of rationing may be inevitable. Arguably, it may then be better to use certain ‘objective’ means of rationing rather than consumer purchasing power or the arbitrary judgements of the service providers.

A number of other problems were seen, by critics, as likely to prevent the internal market from making a significant contribution to the improvement of health care.

Asymmetry of information

When the provider and purchaser were one and the same, as with the DHAs before 1991, the quality of health care provision could be monitored through internal channels. However, they became separated after the creation of the internal market in 1991, the problem then being that while the providers may be aware of any diminution in quality of service, the purchasers may not. This asymmetry of information between seller and buyer is a classic instance of ‘market failure’ which may lead to an inefficient allocation of resources, with purchasers paying more than the competitive price for any given quality of service.

High transaction costs

The main means by which purchasers seek to gain assurances as to the price and quality of provision is by the issuing of contracts, which may of necessity be rather detailed. Drawing up such contracts takes time and money, as does the whole tendering process between rival providers and the eventual requirements for issuing and processing invoices and other documents between contracting parties. These transaction costs may absorb some or all of any efficiency gains via the internal market. Before the creation of the internal market some 5% of total health care spending in the UK involved administrative costs; there were fears that the internal market might raise this figure nearer to the 20% of total health care spending involving the various transaction costs commonly experienced in the US.

Non-contestable markets

To avoid excessive transaction costs, there may be the incentive for individual providers and purchasers to develop long-term relationships in response to the creation of an internal market. The billing and invoicing system of the respective parties might then be simplified and made compatible, as might other aspects of provision. Familiarity and convenience may then serve to make it difficult for potential new entrants to secure existing contracts when these are due for renewal. This lack of opportunity for new entrants may permit existing providers in the internal market to be less efficient than is technically feasible, as a result of the long-term relationships established between providers and purchasers. In other words, these long-term relationships may make the internal health care market less contestable (by new entrants) than hitherto.

Monopoly provision

Some districts and regions within the internal market may be too small, in themselves, to support more than one (or perhaps even one) ‘efficient’ service provider. This may be the case where significant economies of scale are available in respect of various types of treatment, giving large hospitals a cost advantage. Significant travel costs (transport, time and convenience) may then deter patients (or their agents) from undermining the higher cost provision in these local monopoly cases by seeking treatment in other regions and districts.

Key points

■ The role of the market is viewed in different ways by the various ‘schools’ of economic thought.

■ Classical economists tended to emphasise the co-ordinating role of prices in markets, whilst recognizing market imperfections (e.g. monopoly). Such economists saw the market system as also providing a mechanism for channelling self-interest into decisions which are consistent with achieving ‘harmonious order’ and furthering the common good!

■ Neoclassical economists tend to focus on a marginalist approach to decisionmaking within markets, with differential calculus and other mathematical foundations used to predict resource allocating decisions by rational economic agents. ‘Methodological individualism’ underpins this approach, with individuals acting rationally seen as the central element in society, and institutional arrangements merely an outcome of these individual actions.

■ In the neoclassical perspective, ‘prices’ convey sufficient information to bring about ‘Pareto Optimum’ resource allocations. Individual actors need only maximize their own self-interest, subject to the ‘signals’ they receive from the product and factor markets, and the outcomes will be such that no one can be made better off by further resource reallocation without someone else being made worse off!

■ Should ‘market failures’ occur, these are to be corrected, in the neoclassical view, by simple ‘rules’ based on competitive market characteristics, e.g. remove monopolies, improve information, set prices equal to marginal costs of provision, etc.

■ The ‘general equilibrium’ approach of Arrow-Debreu showed that, subject to competitive market conditions, a market system can itself generate relative prices capable of clearing all markets simultaneously, with no need for any external intervention.

■ Institutional or heterodox economists challenge the neoclassical emphasis on individual actors. They see institutions, especially the written and unwritten rules and norms within various communities and organizations, as playing a key role in resource allocation outcomes. Individual consumer and producer behaviour is seen, from this perspective, as directly influenced by the institutional context in which the respective actors operate.

■ The institutional or heterodox perspective is seen as better able to deal with issues of gift giving and trust and with other expressions of observed ‘selfless’ behaviour, seen as non-rational in the neoclassical perspective.

■ Quasi- or internal markets are a further example of institutional contexts playing a key role in actual decision-making. These quasi- or internal markets are often characterized by ‘market failure’ which are intrinsic to the ways in which they were established, e.g. asymmetry of information via the purchaser/provider structure of health care.

Now try the self-check questions for this chapter on the Companion Website. You will also find useful links to relevant websites.

References and further reading

Akerlof, G. A. (1984) An Economic Theorists Book of Tales, Cambridge, Cambridge University Press.

Andreoni, J. (1989) Giving with impure altruism: applications to charity and Ricardian equivalence, Journal of Political Economy, 97(6): 1447-58.

Andreoni, J. (1990) Impure altruism and donations to public goods: a theory of warmglow giving, Journal of Political Economy, 97(3): 1147-58.

Ariely, D. (2009) The end of rational economics, Harvard Business Review, July-August, Special Edition.

Arrow, K. and Debreu, G. (1954) Existence of an equilibrium for a competitive economy, Econometrica, 22(3): 265-90.

Ayres, C. (1951) The co-ordinates of institutionalism, American Economic Review, 41(May): 47-55.

Becker, G. (1981) A Treatise on the Family, Cambridge MA, Harvard University Press.

Boettke, P. J. and Leeson, P. (2003) The Austrian School of Economics, 1950-2000, in Samuels, W. J., Biddle, J. E. and Davis, J. B. (eds), A Companion to the History of Economic Thought, Oxford, Blackwell, 445-53.

Boettke, P. J., Coyne, C. and Leeson, P. (2005) The Many Faces of the Market, Working Paper, Fairfax, VA, George Mason University.

Boland, L. A. (2003) The Foundations of Economic Method: A Popperian Perspective (2nd edn), London, Routledge.

Cairncross, A. (1978) The market and the state, in T. Wilson and A. Skinner (eds), The Market and the State: Essays in Honour of Adam Smith, Oxford, Oxford University Press, 113-34. Chakravorti, B. (2010) Finding competitive advantage in adversity, Harvard Business Review, November, 102-8.

Coase, R. (1937) The nature of the firm, Economica, 4(16): 386-405.

Collard, D. (1978) Altruism and Economy, Oxford, Martin Robertson.

Commons, J. R. (1931) Institutional economics, The American Economic Review, 21(4): 648-57.

Edgeworth, F. (1881) Mathematical Physics, New York, Kegan Paul.

Elster, J. (1989) The Cement of Society: A Study of Social Order, Cambridge, Cambridge University Press.

Fehr, E. and Gachter, S. (2000) Fairness and retaliation: the economics of reciprocity, Journal of Economic Perspectives, 14(3): 159-81.

Fehr, E. and Schmidt, K. M. (1999) A theory of fairness, competition and cooperation, Quarterly Journal of Economics, 114, 817-68.

Fukuyama, F. (1992) The End of History and the Last Man, New York, The Free Press.

Galbraith, J. (1952) American Capitalism: the Concept of Countervailing Power, Boston MA, Houghton Mifflin.

Godbout, J. T. (1998) The World of the Gift, Montreal, McGill-Queen’s University Press. Griffiths, A. and Wall, S. (2000) Intermediate Microeconomics, Harlow, Financial Times/ Prentice Hall.

Hayek, von F. (1948) Economics and knowledge, in Individualism and Economic Order, London, Routledge, 33-56.

Hicks, J. (1969) A Theory of Economic History, Oxford, Oxford University Press.

Hodgson, G. M. (1988) Economics and Institutions: A Manifesto for a Modern Institutional Economics, Cambridge, Polity Press. Jevons, W. (1871) The Theory of Political Economy, Basingstoke, Macmillan.

Kaletsky, A. (2010) Capitalism 4.0: The Birth of a New Economy, London, Bloomsbury.

Kay, J. (2004) The Truth about Markets, London, Penguin.

Kolm, S.-C. (1984) La Bonne Economie. La Reciprocite Generale, Paris, Presses Universitaires de France.

Kolm, S.-C. (2000) The theory of reciprocity, giving and altruism, in Ythier, J. M., Kolm, S.-C. and Gerard-Varet, S.-A. (eds), The Economics of Reciprocity, Giving and Altruism, Basingstoke, Macmillan, 1-44.

Means, G. (1962) Pricing Power and the Public Interest, New York, Harper and Brothers.

Meier, S. (2006) The Economics of Non-Selfish Behavior, Cheltenham, Edward Elgar.

Menger, C. (1950[1871]) Principles of Economics, Glencoe, II, Free Press.

Mill, J. S. (1863) Utilitarianism, London, John Murray.

Mises, von L. (1949) Human Action, Auburn AL, Ludwig von Mises Institute.

Mitchell, W. (1927) Business Cycles: The Problem and its Setting, Cambridge MA, National Bureau of Economic Research.