Privatization and deregulation

Public ownership of industries is now in retreat throughout the world as governments privatize. Since the early 1980s the UK has provided a model of privatization which has been influential in policy-making, both in other industrial countries and in developing countries.

The collapse of the Soviet Union and the Eastern European Communist regimes has led to privatization programmes which totally dwarf those of the UK. This chapter summarizes the original case for nationalization and considers the arguments for and against privatization. There is also a discussion of the case for regulating the activities of the privatized companies as well as the contrary view in favour of less regulation (i.e. deregulation).I Nature and importance

Public (or state) ownership of industry in the UK has mainly been through public corporations, which are trading bodies whose chairpersons and board members are appointed by the Secretary of State concerned. These nationalized industries, as they are often called, are quite separate from government itself. They run their businesses without close supervision but within the constraints imposed by government policy. These constraints include limits to the amounts they can borrow and therefore invest and may also include limits to the wages and salaries they can offer. Not all public corporations are, however, nationalized industries. There are some public corporations, such as the BBC, which are not classed as nationalized industries.

Public ownership can also take the form of direct share ownership in private sector companies. So, for example, after the collapse of the DAF motor vehicle group in 1993, the Netherlands government provided 50% of the equity and loan capital for DAF Trucks NV which took over some of the failed group’s activities. In a similar way, the UK government held a majority holding in British Petroleum for many years prior to its complete privatization in 1987.

Privatization in the UK has reduced the number of nationalized industries to a mere handful of enterprises accounting for less than 2% of UK GDP, around 3% of investment and under 1.5% of employment. By contrast, in 1979 the then nationalized industries were a very significant part of the economy, producing 9% of GDP, being responsible for 11.5% of investment and employing 7.3% of all UK employees. The scale of the transfer of public sector businesses since 1979 to private ownership is further indicated in Table 8.1 below, which lists the businesses privatized by sector.

I Reasons for nationalization

Looking back from the perspective of the new millennium, the reader may well ask why the state ever became so heavily involved in the production of goods and services. Yet between the 1940s and the 1980s this was one of the most contentious issues in British politics, both between the major parties and within the Labour Party. The first post-war Labour government (1945-51) achieved a major programme of nationalization which was opposed by the Conservative Party at the time but broadly left in place by subsequent Conservative governments. The apparent consensus on the scale of the nationalized industries was, however, broken after 1979 as Conservative governments under Mrs Thatcher developed the policy of privatization. We now consider a range of arguments used in favour of nationalization.

Political

The political case for nationalization centred on the suggestion that private ownership of productive assets creates a concentration of power over resources which is intolerable in a democracy. Until 1995 the Labour Party appeared to embrace this idea in Clause 4 of its constitution which promised public ownership of the means of production, distribution and exchange. The founders of the Labour Party saw public ownership as a necessary step towards full-scale socialism and one which would aid economic planning. This developed into a policy of nationalizing the ‘commanding heights’ of the economy which the 1945 Labour government identified as the transport industries, the power industries and the iron and steel industries; the Post Office had always been state owned and at that time also included telephones.

There were always many in the Labour Party who were opposed to a literal interpretation of Clause 4 and saw that there were other means of regulating economic activity besides outright public ownership. By the 1990s, after the collapse of the Eastern European socialist economies, there were few remaining advocates of economic planning and the Labour Party abandoned the old Clause 4 by a large majority at a special conference in 1995.Post-war reconstruction

After the Second World War some industries, e.g. the railways, were extremely run-down, requiring large- scale investment and repair. For these, the provision of state finance through nationalization seemed a sensible solution. In other industries, e.g. steel, nationalization was a means of achieving reorganization so that economies of scale could be fully exploited. In still other industries, e.g. gas and electricity, reorganization was required to change the industry base from the local to the national.1 A different government might, of course, have used policy measures other than nationalization, such as grants and tax reliefs, to achieve these objectives.

The public interest

There are many situations where commercial criteria, with their focus on profitability, are at odds with a broader view of the public interest, and in such cases nationalization is one solution. For instance, the Post Office aims to make a profit overall, but in doing so makes losses on rural services which are subsidized by profits made elsewhere - a ‘cross-subsidy’ from one group of consumers to another. Some object to cross-subsidization, arguing that it interferes with the price mechanism in its role of resource allocation when some consumers pay less than the true cost of the services they buy, whilst others pay more than the true cost. However, in the case of the Post Office cross-subsidization seems reasonable, if only because we may all want to send letters to outlying areas from time to time, and all derive benefit from the existence of a full national postal service.

A private sector profit- orientated firm might not be prepared to undertake the loss-making Post Office services.State ownership may also be a means of promoting the public interest when entire businesses are about to collapse. The state has sometimes intervened to prevent liquidation, as in 1970 when the Conservative government decided to rescue Rolls-Royce rather than see the company liquidated. Prestige, strategic considerations, effects on employment and on the balance of payments all played a part in the argument, as the judgement of the market was rejected in favour of a broader view of the public interest. In the long run, the markets were proved wrong and the decision to intervene commercially correct, as the company is now a world leader in aero-engine technology and has been successfully returned to the private sector.

State monopoly

The ‘natural monopoly’ argument is often advanced in favour of nationalization of certain industries. Economies of scale in railways, water, electricity and gas industries are perhaps so great that the tendency towards monopoly can be termed ‘natural’. Competing provision of these services, with duplication of investment, would clearly be wasteful of resources. The theory of the firm suggests that monopolies may enjoy supernormal profits, charging higher prices and producing lower output than would a competitive industry with the same cost conditions. However, where there are sufficient economies of scale, the monopoly price could be lower and output higher than under competition (see Chapter 9). Monopoly might then be the preferred market form, especially if it can be regulated. Nationalization is one means of achieving such regulation.

Presence of externalities

Externalities occur when economic decisions create costs or benefits for people other than the decisiontaker; these are called social costs or social benefits (see Chapter 10, p. 190). For example, a firm producing textiles may emit industrial effluent, polluting nearby rivers and causing loss of amenity.

In other words, society is forced to bear part of the cost of private industrial activity. Sometimes those who impose external or social costs in this way can be controlled by legislation (pollution controls, Clean Air Acts), or penalized through taxation. The parties affected might be compensated, using the revenue raised from taxing those firms creating social costs. On the other hand, firms creating external or social benefits may be rewarded by the receipt of subsidies. In other cases, nationalization is a possible solution. If the industry is run in the public interest, it might be expected that full account will be taken of any externalities. For instance, it can be argued that railways reduce road usage, creating social benefits by relieving urban congestion, pollution and traffic accidents. This was one aspect of the case for subsidizing British Rail through the passenger service obligation grant which, in the mid-1990s, amounted to around £1bn. The grant enabled British Rail to continue operating some lossmaking services. Nationalization is therefore one means of exercising public control over the use of subsidies when these are thought to be in the public interest.Improved industrial climate

There was hope after 1945 that the removal of private capital would improve labour relations in the industries concerned, promoting the feeling of coownership. The coal industry in particular had a bitter legacy of industrial relations. From nationalization until the strike of 1973, industrial relations in the coal industry, judged by days lost in disputes, seemed to have dramatically improved over pre-war days. Nevertheless, for the nationalized industries as a whole, it is fair to say that the hopes of the 1940s were not fulfilled, perhaps because the form of nationalization adopted in the UK did little to involve workers in the running of their industries. Participation in management, worker directors, genuine consultation and even an adequate flow of information to workers are no more common in the UK public sector than they are in the private sector.

Redistribution of wealth

Nationalization of private sector assets without compensation is a well-tried revolutionary means of changing the distribution of wealth in an inegalitarian society. Nationalization in the UK has not, unlike the Soviet Union in 1917, been used in this way; in the UK there has almost always been ‘fair’ compensation. Indeed, the compensation paid between 1945 and 1951 was criticized as over-generous, enabling shareholders to get their wealth out of industries which, in the main, had poor prospects (e.g. railways, coal) in order to buy new shareholdings in growth industries (e.g. chemicals, consumer durables). Once ‘fair’ compensation is accepted in principle in state acquisitions of private capital, then nationalization ceases to be a mechanism for redistribution of wealth.

An alternative to ‘fair’ compensation is confiscation. However, this would have serious consequences for UK capital markets. Ownership of assets in the UK would, in future, carry the additional risk of total loss by state confiscation, which could influence decisions to invest in new UK-based plant and equipment, and to buy UK shares. The ability of UK companies to invest and to raise finance might therefore be undermined. The transfer of assets might also prove inequitable, since shares are held by pension funds and insurance companies on behalf of millions of small savers who would then be penalized by confiscation.

I Privatization

Privatization means the transfer of assets or economic activity from the public sector to the private sector. As we noted earlier, privatization in the UK has reduced the number of nationalized industries in 2010 to a mere handful of enterprises accounting for less than 2% of UK GDP, around 3% of investment and under 1.5% of employment. Indeed the public ownership of industries is now in retreat throughout the world as governments privatize. However, privatization can often mean much more than denationalization. Sometimes the government has kept a substantial shareholding in privatized public corporations (initially 49.8% in BT), whereas in other cases a public corporation has been sold in its entirety (e.g. National Freight Corporation). Where public sector corporations and companies are not attractive propositions for complete privatization, profitable assets have been sold (e.g. Jaguar Cars from the then British Leyland and also British Rail Hotels). Yet again, many public sector activities have been opened up to market forces by inviting tenders, the cleaning of public buildings and local authority refuse collection being examples of former ‘in-house’ services which are now put out to tender. Private sector finance and operation of facilities and services is also now established in a vast array of public/private finance initiatives (PFI). In other words, the many aspects of privatization also involve aspects of deregulation, e.g. in allowing private companies to provide goods and services which could previously only (by law) be provided in the public sector.

Early privatizations, for example BT in 1984, were usually simple transfers of existing businesses to the private sector. Increasingly, privatizations have become much more complex, often being used to restructure industries by breaking up monopolies and establishing market-based relationships between the new companies. For example, the privatization of British Rail involved separating ownership of the track (Railtrack) from the train operating companies and also the train leasing companies. The train operating companies are in this case franchisees who have successfully tendered for contracts to operate trains for a specified period.

Market forces have also been introduced into the unlikely areas of social services, the health services and education - especially higher education. In health and social services this has involved the purchaser/ provider model in which, for example, doctors and ‘primary care groups’ have used their limited budgets to buy hospital services needed by their patients. Funds, and hence the use of resources, are then controlled by purchasers rather than by the providers. As a result, these purchasers have an incentive to use hospitals offering, in their judgement, the ‘best’ service as described by some combination of quality and value for money. (However, as we note in Chapter 13, the Labour government (1997-2010) sought to modify some of these market arrangements.) In higher education, the funding of universities has been closely linked to the numbers of students enrolling. It follows that any failure to enrol students, perhaps through offering unpopular courses, would drive a university into deficit and possible bankruptcy. Resources in this sector were previously allocated by administrators; now a market test is applied.

Table 8.1 shows the extent of privatization in the UK to 2010, in terms of both the number of businesses and their spread across major sectors of the economy. The total value of privatization receipts to the Treasury has been estimated at over £70bn. Clearly the scope for further privatization among the remaining nationalized industries is now limited as there are so few left, but there are many possibilities in the activities currently run by the Civil Service and Local Authorities.

The case for privatization

A commitment to privatize wherever possible became established in the Conservative Party during Mrs Thatcher’s first term. By 1982 the late Mr Nicholas Ridley, then Financial Secretary to the Treasury, expressed this commitment as follows:

It must be right to press ahead with the transfer of ownership from state to private ownership of as many public sector businesses as possible The introduction of competition

must be linked to a transfer of ownership to private citizens and away from the State. Real public ownership - that is ownership by people - must be and is our ultimate goal.

Mr Ridley made a case for privatization which focused on the traditional Conservative antipathy to the state. On this view, the transfer of economic activity from the public to the private sector is, in itself, a desirable objective. By the early 1980s privatization was also supported by adherents of ‘supplyside’ economics with its emphasis on free markets. Privatization would expose industries to market forces which would benefit consumers by giving them choice,

Table 8.1 Major privatizations: a sectoral breakdown.

Mining, Oil, Agriculture and Forestry

British Coal, British Petroleum, Britoil, Enterprise Oil

Land Settlement, Forestry Commission, Plant Breeding Institute

Electricity, Gas and Water

British Gas

National Power, PowerGen

Nuclear Electric

Northern Ireland Electric, Northern Ireland Generation (4 companies)

Scottish Hydro-Electric, Scottish Power

National Grid

Regional Electricity Distribution (12 companies)

Regional Water Holding Companies (10 companies)

Manufacturing, Science and Engineering

AEA Technology

British Aerospace, Short Bros, Rolls-Royce

British Shipbuilders, Harland and Wolff

British Rail Engineering

British Steel

British Sugar Corporation

Royal Ordnance

Jaguar, Rover Group

Amersham International

British Technology Group Holdings (ICL, Fairey,

Ferranti, Inmos)

Distribution, Hotels, Catering

British Rail Hotels

Transport and Communication

British Railways

National Freight, National and Local Bus Companies

Motorway Service Area Leases

Associated British Ports, Trust Ports, Sealink

British Airways, British Airports Authority (and other airports)

British Telecommunications, Cable and Wireless

Banking, Finance, etc.

Girobank

and also lower prices as a result of efficiency gains within the privatized companies.

Supply-side benefits

The breaking of a state monopoly would, in this view, enable consumers to choose whichever company

produced the service they preferred. That company would then generate more profit and expand in response to consumer demand, whilst competitive pressure would be put on the company losing business to improve its service or go into liquidation. BT’s progressive reductions in telephone charges and Internet access charges in recent years have clearly been at least partly in response to competition. The pressure to meet consumer requirements should also improve internal efficiency (X efficiency) as changes can be justified to workers and managers by the need to respond to the market. The old public corporations had increasingly been seen as producer led, serving the interests of management and workers rather than those of consumers and shareholders (in this case taxpayers). Privatization introduces market pressures which help to stimulate a change of organizational culture.

Trade unions can be expected to discover that previous customs and work practices agreed when in the public sector are now challenged by privatization, as the stance taken by management changes from when the industry was nationalized, and thereby raises corporate efficiency. Similarly, competition in the product market will force moderation in wage demands and increased attention to manning levels, again raising efficiency. Privatization contributes in these various ways to the creation of ‘flexibility’ in labour markets, higher productivity and reduced unit labour costs.

The stock market provides a further market test for privatized companies. Poor performance in meeting consumer preferences or in utilizing assets should result in a share price which underperforms the rest of the market and undervalues the company’s assets, ultimately leaving it vulnerable to takeover by a company able to make better use of the assets. Supporters of privatization place more faith in these market forces than in the monitoring activities of Departments of State and Parliamentary Committees.

Wider share ownership

The Conservative Party in its drive towards privatization also emphasized wider share ownership. By 2010, share ownership in the UK had spread to 22% of the adult population, having been only 7% as recently as 1981. The total number of UK shareholders is about the same as the number of trade unionists. This increase in shareholding is largely due to privatization.

A new group of shareholders has been attracted and become participants in the ‘enterprise culture’. Additionally, 90% of the employees in the privatized companies have become shareholders in the companies they work for, at least initially. Worker share ownership is advocated as a means of involving workers more closely with their companies and achieving improved industrial relations. This has been taken further by selling companies to their managers (e.g. Leyland Bus in 1987) or to consortiums of managers and workers (e.g. National Freight in 1982). The latter is regarded as a highly successful example, profits having grown more than tenfold since privatization.

Reductions in PSBR

Privatization has also been seen as a way in which the public sector borrowing requirement (PSBR) (now PSNCR - see Chapter 18, p. 356) can be cut, at a stroke! The finance of external borrowing by the nationalized industries is regarded in accounting terms as being part of public expenditure, which then ceases when these industries become privately owned. Sale of assets or shares also increases government revenue, again reducing the PSBR in the year of the sale. Over the period 1979-2010 the Treasury gained £75bn from asset sales. Privatization made a very significant contribution to the budget surpluses of the late 1980s and to curbing the size of the budget deficits of the 1990s. Privatization proceeds reduced the PSBR as a proportion of GDP by more than 1.5% during the late 1980s, and by a still significant, if smaller, percentage in other years.

Managerial freedom

The activities of state-owned organizations are constrained by their relationship with the government. They lack financial freedom to raise investment capital externally because the government is concerned about restraining the growth of public expenditure (see Chapter 18). Privatization is then seen as increasing the prospects for raising investment capital, thereby increasing efficiency and lowering prices.

A further limitation on nationalized industries is the political near-impossibility of diversification. In many cases, this would be the sensible corporate response to poor market prospects, but it is not an option likely to be open to a nationalized concern. Since privatization, however, companies have been able to freely exploit market opportunities. So, for example, most of the regional electricity companies have become suppliers of gas as well as electricity.

The ‘globalization’ of economic activity also, in this view, leaves nationalized industries at a distinct disadvantage. For example, no private oil company would have followed the nationalized British Coal in confining its activities to one country where it happened to have reserves. This international perspective is an important reason why the Post Office management saw privatization as ‘the only (option) which offers us the freedom to fight off foreign competition’. In the postal services, increased competition has arisen from the Dutch Post Office, which has been privatized, and is expected from further liberalization of other national postal services expected within the European Single Market. The difficulties of an international strategy for nationalized industries are shown by the failure of the attempted Renault-Volvo merger in 1993. The then nationalized status of Renault contributed substantially to Swedish (Volvo) shareholder opposition to the merger.

Privatization, then, is seen by its supporters as a means of greatly improving economic performance.

The case against privatization

Privatization may be opposed for all the reasons that nationalization was originally undertaken (see above). Additionally, both the rationale of the policy and its implementation may be criticized.

Absence of competition

An essential aspect to the case for privatization is the creation of competitive market conditions. However, some state-owned industries have always faced stiff competition in their markets (for example, Post Office Parcelforce from DHL), so that privatization of these industries might be considered irrelevant on the basis of this ‘competitive market conditions’ argument.

The government also faces a dilemma as regards creating competitive market conditions when privatizing public utilities which are monopolies, namely that it has another, and potentially conflicting, objective which is to raise money for the Treasury. Breaking up state monopolies in order to increase competition reduces the market value of the share offer; monopolies are likely to be worth more as share offers because they reduce uncertainty for investors. Critics would say that the government has allowed the creation of competition to be secondary to creating attractive share issues which sell easily. The result has been the transfer of public utility monopolies intact to the private sector, creating instead private sector monopolies.

Nevertheless, competitive pressures are being applied to some of the previously public utility monopolies in their newly privatized form. For example, at the time of privatization, British Gas appeared to be a classic natural monopoly. Since then consistent pressure from the regulatory authorities has created competitive market conditions in the supply of gas to industry, to such an extent that by 2006 the British Gas share of the industrial market was below 30% and competitive supply had been extended to the domestic market for gas across the whole country. As regards BT, opportunities for new entrants created by rapid technological change have been even more significant in eroding the market dominance of BT. Cable TV companies can now provide highly competitive phone services using their fibre optic cable systems; additionally many large organizations have created their own phone networks and the Internet and digital TV are creating still further opportunities for communication.

The technical and regulatory changes in the telecommunication and gas industries have benefited consumers but should not be confused with the issue of the desirability of privatization. Consumers might well feel that these desirable outcomes could have been achieved under public ownership. If so, critics might then argue that consumers could have experienced still greater benefit from technical innovation because, under privatization, lax regulatory regimes have allowed excessive levels of profit, to the benefit of shareholders and executives rather than consumers.

Presence of externalities

The rationale for privatization is at its weakest when externalities exist. Indeed the former nationalized industries contained many examples of such externalities, which was one of the reasons for their original public ownership. The now privatized rail companies are not able to charge road users for any benefits (e.g. less congestion) created by the lower levels of road traffic which rail services create. In the water industry there is a vested interest in encouraging consumption to increase turnover, even if this means the need to build new reservoirs with a consequent loss of land, disruption to everyday life and dramatically changed landscapes. In the case of the electricity industry, the competitive market among the generators has had nearly terminal implications for the coal industry. New contracts for coal supplies to the electricity generating companies have only been secured by British Coal at world prices, well below the prices previously agreed. As employment in mining has plummeted, the cost has been borne by society. Miners’ families and local communities have become much poorer, whilst public expenditure on unemployment and social security benefits has risen and tax revenues have been reduced by the rising unemployment. At a time of high unemployment, organizations which lower their private costs by making more workers redundant invariably create social costs (externalities). There is also the issue of the long-term strategic role of the coal industry. The German government has long recognized these wider aspects of industrial policy and has arranged a levy on electricity users to compensate the electricity generators for offering coal prices which are over three times the world price. German electricity prices in the first decade of the millennium were some 30-40% higher than those in the rest of Europe. The UK government has taken a contrary view and decided that the nuclear industry rather than the coal industry should be subsidized. In doing so it has, of course, departed from its free market philosophy and further endangered the coal industry by subsidizing a competitor.

Undervaluation of state assets

The extension of share ownership does not in itself attract much criticism. The issues which have provoked criticism include the pricing and the marketing of the shares. It is argued that valuable national assets have been sold at give-away prices. This criticism is made of both privately negotiated deals and the public share offers. An example of the former is the offer for Austin Rover made by British Aerospace in March 1988 which valued a company which has received a total of £2.9bn of public funds at only £150m and this on condition that the government wrote off £1.1bn of accumulated losses and injected a further £800m. The deal could be presented as giving away £650m and a company with net assets of more than £1.1bn. The generosity of the government’s approach was confirmed when the European Commission ruled that the £800m government injection of capital must be reduced to £572m, in the interests of fair competition in the EU motor market. The Commission also insisted that British Aerospace repay £44.4m which it received from the government as ‘sweeteners’ during the deal. The government’s prime objective was to return Rover to the private sector as quickly as possible in the belief that the benefits would soon outweigh any losses on the deal. There were also the provisos that the company remain under British ownership (see below) and that employment be maintained. These provisos severely restricted the number of potential buyers.

In most cases, public share offers have been heavily over-subscribed and large percentage profits have been made by successful applicants. Rolls-Royce shares, for example, were issued part paid at 85p on 20 May 1987 and moved to 147p by the close of business that day, a profit of 73% before dealing costs. British Telecom shares reached a premium of 86% on the first day. The electricity privatization has, to date, raised some £6.5bn, but the assets involved have a value of £28bn. Hardly surprisingly, the regional electricity company shares had a first-day premium of almost 60%, and those of the electricity generating companies a premium of almost 40%.

Underpriced issues have cost the Treasury substantial revenues and have also conditioned a new class of small shareholders to expect quick, risk-free capital gains. These expectations were encouraged by barrages of skilful advertising. Not surprisingly many of the new shareholders cashed in their windfall gains by selling their shares. As a result share ownership in the new companies quickly became more concentrated. For example, the 1.1 million BA shareholders at the flotation in February 1987 had reduced to 0.4 million by early October. Despite this, there is no doubt that there has been a considerable extension of share ownership, although the majority of shareholders have shares in only one company. In fact 54% of investors hold shares in only one company and only 17% have shares in more than four companies. Parker (1991) concludes that privatization has widened share ownership but not deepened it. Indeed, the institutional investors raised their proportion of shareholdings during the 1980s at the expense of the private investor, whose proportion of total shareholdings fell from 30% to 20% during this period.

Short-termism

The discipline of the capital markets may prove a very mixed blessing for some of the privatized companies if they become subject to the City’s alleged ‘short-termism’. The large investment fund managers are often criticized for taking a short-term view of prospects. This would be particularly inappropriate for the public utilities where both the gestation period for investment and the pay-back period tend to be lengthy. The freedom with which ownership of assets changes hands on the stock market is not always in the public interest. The acquisition of B Cal in 1987 by the newly privatized BA, for example, was investigated by the then Monopolies and Mergers Commission (MMC) and approved on condition that BA gave up some of the routes acquired. There was also concern at the 22% holding in BP which the Kuwait Investment Office acquired very cheaply in the aftermath of the 1987 stock market crash. The MMC ruled that the Kuwait holding be reduced to 11%. The limitations of privatization and excessive reliance on the markets was illustrated in 1994 by BMW’s takeover of the Rover Group from British Aerospace. The government had originally set a period of five years in which Rover could not be sold to a foreign buyer but, within a few months of the expiry of the limitation, the last British-controlled volume car producer was sold to the German company. Of course it is by no means clear that retaining national control of companies is a desirable objective. The takeover could arguably be welcomed as a benefit of European integration which will strengthen the European car industry. However, if national control is desired, as it was when British Aerospace bought Rover, then this is an example of the weakness of privatization as a substitute for industrial policy. The French government’s plan to retain a controlling majority interest in Renault after privatization illustrates an alternative approach, although the UK government would tend not to view such a compromise as a ‘privatization’.

Opportunity costs

The flow of funds into privatization offers has been diverted from other uses. It is reasonable to suppose that applicants for shares are using their savings rather than reducing their consumption. Large sums of money leave the building societies during privatizations, and other financial institutions are also deprived of funds. This raises the possibility that what is merely a restructuring and change of ownership of state industry may be reducing the availability of funds for other organizations which would use them for real capital investment. The effects of privatization issues on the financial markets are much the same as the effects of government borrowing, raising the same possibilities of ‘crowding out’.

The contribution of privatization to reducing the PSBR has been widely criticized as ‘selling the family silver’. The sales involve profitable assets and, after privatization, the Exchequer loses the flow of returns from them. Schwartz and Lopes (1993) have pointed out that the sale price of assets should equal the net present value of expected future returns on them. If this were the case, then the ‘family silver’ argument would lose some of its power and rest on the use to which the proceeds were put - that is consumption or investment. However, most privatization issues in the UK have been underpriced in the view of the markets (see above).

Burden on taxpayers

A final criticism of privatization is a moral one, that the public are being sold shares which, as taxpayers, they already collectively own. The purchasers of the shares benefit from the dividends paid by the new profit-seeking enterprises, at the expense of taxpayers as a group. Those taxpayers who do not buy the shares, perhaps because they have no spare cash, are effectively dispossessed.

Regulation of privatized companies

The privatization of public utility companies with ‘natural’ monopolies creates the possibility that the companies might abuse their monopoly power. In these cases, UK privatizations have offered reassurance to the public in the form of regulatory offices for each privatized utility, for example OFTEL for telecommunications and OFWAT for the water industry. Where privatized companies such as Rover and British Airways are returned to competitive markets, arguably there is no need for specific regulation beyond the normal activities of the Office of Fair Trading (OFT) and the Competition Commission (CC). If a privatized company finds its regulator’s stipulations unacceptable, then it may appeal to the Competition Commission.

Objectives of regulators

Regulators have two fundamental objectives. Firstly, they attempt to create the constraints and stimuli which companies would experience in a competitive market environment. For example, companies in competitive markets must bear in mind what their competitors are doing when setting their prices and are under competitive pressure to improve their service to consumers in order to gain market share. Regulation can simulate the effects of a competitive market by setting price caps and performance standards. Secondly, regulators have the longer-term objective of encouraging actual competition by easing the entry of new producers and by preventing privatized monopoly power maintaining barriers to entry. An ideal is the creation of markets sufficiently competitive to make regulation unnecessary. The market for telecommunication services has moved substantially in this direction, so much so that in July 2006 OFTEL announced that it would no longer apply a price cap for BT-provided services, since the market was now so competitive that such a price cap was unnecessary.

Problems facing regulators

Regulators have an unenviable role as they try to create the constraints and stimuli of a competitive market. Essentially they are arbitrating between the interests of consumers and producers. Other things being equal, attempts by regulators to achieve improvements in service levels will cause increases in costs and so lower profits, whilst price caps on services with price-inelastic demand will also reduce profits by preventing the regulated industries raising prices and therefore revenue. Lower profits, and the expectation of lower profits, have immediate implications for dividend distributions to shareholders and so for share prices. At this point other things are unlikely to remain equal. The privatized company subject to a price cap may well look for ways of lowering costs to allow profits to be at least maintained, or perhaps raised. In most organizations, there are economies to be gained by reducing staffing levels, and the utility companies have dramatically reduced their numbers of employees. Investment in new technology may also enable unit costs to be lowered so that profits are greater than they otherwise would have been.

Establishing a price cap

In deciding on a price cap, the regulator has in mind some ‘satisfactory’ rate of profit on the value of assets employed. A key issue is then the valuation of the assets. If the basis of valuation is historical, using the market value at privatization plus an estimate of investment since that date, then the company will face a stricter price cap than if current market valuations are used for assets. This is because historical valuations will usually be much smaller than the current valuations and so will justify much smaller total profits and therefore lower prices to achieve that profit.

Price caps are often associated with job losses. In an economy with less than full employment it may then be argued that such cost savings in the privatized companies are only achieved at the expense of extra public expenditure on welfare benefit. However, a counter-argument is that lower public utility prices benefit all consumers, with lower costs of production across the economy stimulating output and creating employment.

It may be over-simplistic to assume that privatized companies will invariably respond to a price cap by cutting costs as much as possible in order to maximize profits over the medium-term period of the price cap. The planning period in public utilities is likely to be much longer than the four or five years of a regulator’s price review period. If a company meets its price cap and service requirements by making excessively large efficiency savings so that its profits and share price grow quicker than the average for large companies, then there will be great public pressure on the regulator to be much tougher next time. The goals of regulated companies probably include avoiding the long-term regulatory regime becoming too ‘tight’. At the same time, the regulator may depend on the company for a great deal of the information needed for the task of regulation. So there is the possibility of the regulator’s independence being compromised, which has been called ‘capture’ of the regulator. Clearly the relationship between regulator and regulated company is complex, so that simple predictions of action and reaction are difficult to make.

Costs of regulation

Whilst regulation should produce clear benefits for the consumers of each privatized company, there are inevitable costs involved in running regulatory offices and also costs for the regulated company which has to supply information and present its case to the regulator. It is likely that companies will go further than this and try to anticipate the regulator’s activities, so incurring further costs. It is not at all clear that having separate regulatory offices for each industry is a cost-effective arrangement. Concentration of all regulation in one agency might be more efficient and lead to more consistency in the treatment of different industries. It would also enable a consideration of the implications of decisions in one industry on competitive conditions in other industries. OFTEL, for example, has sought to increase competition in the rapidly changing telecommunications market by forcing BT to allow cable TV companies favourable access to its transmission networks. Yet these cable companies themselves have monopoly power in their own markets!

Differences in the regulatory regimes have certainly contributed to the astonishing difference between the weak share performance of the gas and telecommunications industries and the strong share performance of the water and electricity industries which have outperformed the FTSE 100 index by 60% and 101% respectively. High returns in the stock market are usually associated with risk. However, neither the water industry nor electricity can be viewed as risky; indeed, they would normally be seen as unspectacular but steady income generators rather than as growth stocks.

I Regulation and deregulation

Regulation

Regulation may be defined as the various rules set by governments or their agencies which seek to control the operations of firms. We have already discussed the role of the regulators for the privatized industries who themselves are part of this broad regulatory process.

Regulation is one of the mechanisms available to governments when dealing with the problem of ‘market failure’. Of course, market failure can take many forms although, as Stewart (1997) points out, four broad categories can usefully be identified.

1 Asymmetric information. Here the providers may have information not available to the purchasers. For example, in recent cases involving the misselling of pensions the companies involved were found to have withheld information from purchasers. Stricter regulation of the sector has been the government’s response to this situation.

2 Externalities. In the case of negative externalities, regulations may be used to bring private costs more closely into line with social costs (as with environmental taxes) or to restrict social costs to a given level (as with environmental standards).

3 Public goods. Regulation may be required if such goods are to be provided at all. The idea of a public ‘good’ (which may, of course, be a service) is that it has the characteristics of being nonexcludable and non-exhaustible, at least in the ‘pure’ case. Non-excludable refers to the difficulty of excluding those who do not wish to pay for the ‘good’ (e.g. police or defence); non-exhaustible refers to the fact that the marginal cost of providing an extra unit of the ‘good’ is effectively zero (e.g. an extra person covered by the police or defence forces). The non-excludable condition prevents a private market developing, since it is difficult to make ‘free riders’ actually pay for the public good. The non-exhaustible condition implies that any price that is charged should, for allocative efficiency (see Chapter 5, p. 89), equal marginal cost and therefore be zero. Private markets guided by the profit motive are hardly in the business of charging zero prices! Both conditions imply that the ‘good’ is best supplied by the public sector at zero price, using general tax revenue to fund provision (in the ‘pure’ public good case).

4 Monopoly. Regulation may be required to prevent the abuse of monopoly power. In Chapter 5 we considered a variety of regulations implemented by the Office of Fair Trading. Figure 5.2 (p. 90) was used to show that regulations involving the Competition Commission may be used to prevent or modify certain proposed mergers which are arguably against the public interest (e.g. where gains in ‘productive efficiency’ are more than offset by losses in ‘allocative efficiency’).

The forms of regulation are too innumerable to capture in a few headings. The various rules can involve the application of maximum or minimum prices, the imposition of various types of standards, taxes, quotas, procedures, directives, etc., whether issued by national bodies (e.g. the UK government or its agencies) or international bodies (e.g. the EU Commission, the World Trade Organization, etc.).

Although a strict classification of the numerous types of regulation would seem improbable, McKenzie (1998) makes a useful distinction:

■ regulations aimed at protecting the consumer from the consequences of market failure;

■ regulations aimed at preventing the market failure from happening in the first place.

In terms of the Financial Sector, the Deposit Guarantee Directive of the EU is of the former type. This protects customers of accredited EU banks by restoring at least 90% of any losses up to £12,000 which might result from the failure of a particular bank. In part, this is a response to asymmetric information, since customers do not have the information to evaluate the credit-worthiness of a particular bank, and might not be able to interpret that information even if it were available.

The Capital Adequacy Directive of the EU is of the latter type. This seeks to prevent market failure (such as a bank collapse) by directly relating the value of the capital a bank must hold to the riskiness of its business. The idea here is that the greater the value of capital available to a bank, the larger the buffer stock which it can use to absorb any losses. Various elements of the Capital Adequacy Directive force the banks to increase their capital base if the riskiness of their portfolio (indicated by various statistical measures) is deemed to have increased. In part, this is in response to the potential for negative externalities in this sector. One bank failure can invariably lead to a ‘domino effect’ and risk system collapse with incalculable consequences for the sector as a whole.

In these ways, the regulatory system for EU financial markets is seeking to provide a framework within which greater competition between banks can occur, while at the same time addressing the fact that greater competition can increase the risks of bank failure. It is seeking both to protect consumers should any mishap occur and at the same time to prevent such a mishap actually occurring.

Overall, we can say that those who support any or all of these forms of regulation, in whatever sector of the economy, usually do so in the belief that they improve the allocation of resources in situations characterized by one or more types of market failure.

Deregulation

Deregulation may be defined as efforts to remove the various rules set by governments or their agencies which seek to control the operation of firms.

One of the major arguments in favour of deregulation involves ‘public interest theory’. The suggestion here is that regulations should be removed whenever it can be shown that this will remove or reduce the ‘deadweight loss’ typically shown to result from various types of market interference.

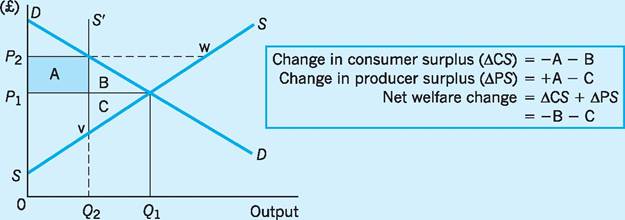

Figure 8.1 can be used to show how a particular market regulation, here a quota scheme, can result in a ‘deadweight loss’. In this analysis, economic welfare is defined as consumer surplus plus producer surplus.

Fig. 8.1 Welfare loss with a quota scheme 0Q2 raising price (P2) above the market clearing level P1.

The consumer surplus is the amount consumers are willing to pay over and above the amount they need to pay; the producer surplus is the amount producers receive over and above the amount they need for them to supply the product.

In Fig. 8.1 we start with an initial demand curve DD and supply curve SS giving market equilibrium price P1 and quantity Q1. However, the regulation here is that should the market price fall below a particular level P2, then the government is directed to intervene. It is required to use a quota arrangement to prevent market price from falling below, P2; in other words P2 is a minimum price which is set by regulation at a level which is above the free market price P1. In terms of Fig. 8.1, if the quota is set at Q2, then the effective supply curve becomes SvS', since no more than Q2 can be supplied whatever the price. The result is to raise the ‘equilibrium’ price to P2 and reduce the ‘equilibrium’ quantity to Q2. However, the quota regulation has resulted in a loss of economic welfare equivalent to the area B plus area C. The reduction in output from Q1 to Q2 means a loss of area B in consumer surplus and loss of area C in producer surplus. However, the higher price results in a gain of area A in producer surplus which exactly offsets the loss of area A in consumer surplus. This means that the net welfare change is negative, i.e. there is a ‘deadweight loss’ of area B + area C.

‘Public interest theory’ is therefore suggesting that deregulation should occur whenever the net welfare change of removing regulations is deemed to be positive. In terms of Fig. 8.1, it might be argued that removing the regulation whereby the government (or its agent) seeks to keep price artificially high at P2 will give a net welfare change which is positive, namely a net gain of area B + area C. In other words, allowing the free market equilibrium price P1 and quantity Q1 to prevail restores the previous deadweight loss via regulation. Put another way, public interest theory is suggesting that deregulation should occur whenever the outcome is a net welfare gain, so that those who gain can, at least potentially, more than compensate those who lose.

Of course, a similar analysis can be carried out in terms of other types of regulation incurring a deadweight loss vis-a-vis the free market equilibrium. In Chapter 27 we show how the operation of price support schemes using central purchasing arrangements by the Common Agricultural Policy of the EU can incur deadweight loss, when intervention prices are set above the world market price for certain agricultural products.

The empirical difficulties of placing a money value on changes in consumer surplus and producer surplus should not, of course, be underestimated. In terms of Fig. 8.1, it involves accurate estimates of both the demand and supply (or cost) curves facing the firm or industry. Issues of ‘weighting’ must also be considered, for example whether a £1 gain of producer surplus is the same in welfare terms as a £1 loss of consumer surplus. Certainly, such a ‘one for one’ weighting was used in Fig. 8.1, with +A gain of producer surplus under the quota regarded as exactly offsetting the -A loss of consumer surplus previously earned under the initial free market situation. Some might argue that a given monetary value to consumers should be given a greater ‘weight’ in terms of economic welfare than a similar monetary value received by producers!

Whether deregulation will yield a net welfare gain or loss (i.e. be in, or against, the public interest) clearly involves both theoretical and empirical aspects, and may need to be considered on a case-by-case basis. Certainly, deregulation is gathering momentum in the major industrialized economies. For example, it has been estimated that in 1977 some 17% of US GNP was derived from the output of fully regulated industries, whereas that figure has declined to around 5% of GNP in current times. Winston (1993), in a wide- ranging study of the impacts of deregulation across the US industrial and service sectors, found substantial net gains to have resulted from deregulatory activity. For instance, in the US airlines sector he estimated the net benefit of the elimination of all regulations on air fares in 1983 to have been in the range of $4.3bn to $6.5bn over a 10-year period.

Interestingly, empirical estimates of the impact of deregulation have had the greatest difficulty in placing monetary values on predicted or actual changes in the quality of goods or services. For example, predictions as to the likely impact of deregulation on the mean and variance of travel times for passengers and freight in the transport sector have been noticeable by their absence from empirical studies or their inaccuracy when compared with eventual outcomes.

Our earlier discussion in Chapter 5 (pp. 89-91) reinforced this point about the difficulty of evaluating the net welfare change from deregulation. It showed how ‘public interest theory’ may often have to weigh the gains in terms of ‘productive efficiency’ against

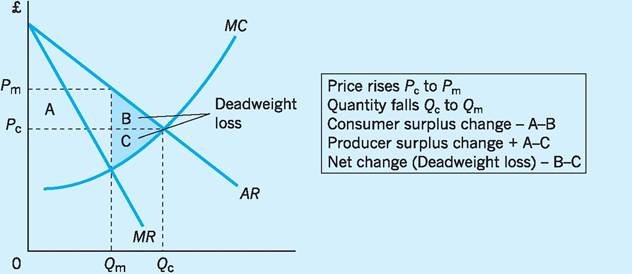

Fig. 8.2 Deadweight loss as a result of monopoly power raising equilibrium price (Pc to Pm) and lowering equilibrium output (Qc to Qm).

Source: Griffiths and Wall (2000) Intermediate Microeconomics, Financial Times/Prentice Hall.

the losses in terms of ‘allocative efficiency’ when trying to evaluate whether a regulation (e.g. restricting a proposed merger) is, or is not, operating in the overall public interest.

Regulating a deregulated monopoly

In the real world, the outcomes of deregulation may not be to recapture all the ‘deadweight loss’ resulting from the previous monopoly situation. This is especially true when a monopoly or oligopoly industry is deregulated, but when a return to a highly competitive industry characterized by numerous small firms is unrealistic! This has, in fact, been the case with most privatizations/deregulations of the previous nationalized industries, with the post-privatization situation often still involving a high degree of market dominance by a relatively small number of large firms.

It is in this type of situation that regulators, using price caps, may be able to release some, if not all, of the ‘deadweight loss’ previously present when the industry was nationalized or under monopoly control.

Deregulating the monopoly industry: no regulator required

If the classical case against monopoly does hold (Chapter 3, p. 58), namely higher price and lower output than in the perfectly competitive equilibrium, then Fig. 8.2 can be used to indicate the ‘deadweight loss’ from removing monopoly power. As compared to the competitive price/output equilibrium (Pc/Qc), the higher monopoly price (Pm) results in the loss of area A and area B (consumer surplus) by discouraging some consumers from purchasing at this higher price. At the same time, the producers who are still able to find a market in which to sell at the higher price gain area A of producers’ surplus, but those unable to sell at this price lose area C, giving an overall change of +A - C in terms of producers’ surplus.

The net change (deadweight loss) in aggregate consumer and producer surplus of the monopoly situation as compared to the competitive market outcome is therefore:

-A - B + A - C = -B - C.

Deregulating the monopoly industry: regulator required

In a simple model, removing the monopoly power by privatization/deregulation will then restore the deadweight loss B + C and thereby raise economic welfare. However, in reality the industry may, post- privatization/deregulation, not in fact move in the direction of a competitive industry but retain much of its previous monopoly/oligopoly characteristics, i.e. still be dominated by a few large firms. It is in such a context that using a regulator to oversee the now deregulated industry, and setting a price cap, may help ensure that at least some of the deadweight loss from the original monopoly situation is recovered2.

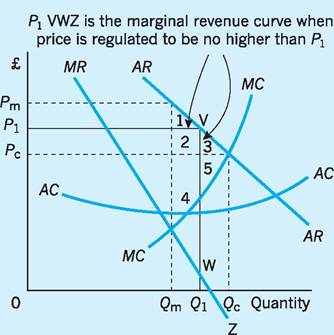

Suppose a regulator is appointed in such a situation and imposes a price ceiling, P1, for the monopoly in Fig. 8.3. The firm can now charge no more than P1, so that the effective average revenue curve is the horizontal line P1V up to output Q1. For output levels up to Q1 the marginal revenue curve will be identical to the average revenue curve (P1V). Of course, for output levels beyond Q1 the original average and marginal revenue curves still apply since the firm is permitted to charge less than P1 if it desires to reach those output levels. Effectively the marginal revenue curve is in two segments, P1V and WZ, with VW a line of discontinuity connecting these two segments.

In Fig. 8.3 the profit maximizing solution (MC = MR) will now be output Q1 at price P1 for the regulated monopolist. Comparing Fig. 8.3 with Fig. 8.2 it should be readily apparent that the area of deadweight loss under the regulated monopoly is smaller than that under the unregulated monopoly.

■ Unregulated monopoly: Deadweight loss = 1 + 2 + 3 + 4 + 5.

■ Regulated monopoly (P1 as price ceiling): Deadweight loss = 1 + 2 + 4.

Clearly, a reduction of area 3 + 5 of deadweight loss is achieved by price regulation in this case.

Fig. 8.3 Price regulation of monopoly: P1 as the price ceiling set by the regulator.

Source: Griffiths and Wall (2000) Intermediate Microeconomics, Financial Times/Prentice Hall.

Indeed, if the price ceiling were set still lower, at the competitive price Pc, then the profit-maximizing solution (MC = MR) for the regulated monopoly would now be Pc∕Qc with zero deadweight loss.

Without the regulator and the price cap at P1, there would be the risk that the original privatization/ deregulation would have had little or no impact in terms of removing the original deadweight loss, as this is ‘recaptured’ by the now privatized large com- pany/companies.

Conclusion

Despite the advance of privatization, there remains a strong case for some form of government intervention in selected industries, for example to protect the public interest, prevent abuse of monopoly power and compensate for externalities. It does not, however, follow that nationalization is the best form of government intervention. The extent of privatization since 1979 has radically changed the role of the state in the UK economy and makes it very unlikely that there will ever again be the range of state industries which existed at that date. Indeed, there is now a worldwide shift of policy in favour of privatizing state-owned assets. The performance of both state-owned and privatized industry is difficult to evaluate. It has not been convincingly demonstrated that the form of ownership of an organization is the most important influence on its performance. Of much greater importance would seem to be the degree of competition and the effectiveness of regulatory bodies. Certainly, greater powers are being given to many of the regulators of the previously nationalized industries in an attempt to prevent the abuse of monopoly power by the now privatized utilities. Regulators may impose price caps and use other devices to prevent consumers being ‘exploited’ in monopoly-type situations. They may also seek to open markets to additional competition by encouraging new entrants. Nevertheless, there is also a counter-movement which seeks to remove regulations where these are thought to operate against the public interest. Such attempts at deregulation are widespread, though it should not be forgotten that the reason many regulations exist is to protect consumers from the adverse consequences of various types of ‘market failure’.

Key points

■ In 1979 the nationalized industries produced some 9% of GDP, 12% of investment and 7% of total employment. However, by 2010 their contribution was much smaller, only around 2% of GDP, 3% of investment and 2% of total employment.

■ Privatization is the transfer of assets or economic activity from the public sector to the private sector.

■ The term ‘privatization’ is often used to cover many situations: the outright sale of state-owned assets, part-sale, joint public/ private ventures, market testing, contracting out of central/local government services, etc.

■ The case for privatization includes allegedly greater productive efficiency (lower costs) via the introduction of market pressures. These are seen as creating more flexibility in labour markets, higher productivity and reduced unit labour costs. More widespread share ownership, a lower PSBR (PSNCR), easier access to investment capital, greater scope for diversification and the absence of civil service oversight are often quoted as ‘advantages’ of privatization.

■ The case against privatization includes suggestions that state monopolies have often merely been replaced by private monopolies, with little benefit to consumers, especially in the case of the public utilities. The loss of scale economies (e.g. ‘natural monopolies’), the inability to deal effectively with externalities, undervaluation of state assets, the subsequent concentration of share ownership and ‘short-termism’ of the city are often quoted as disadvantages of privatization.

■ Regulators have been appointed for a number of public utilities in an attempt to simulate the effects of competition (e.g. limits to price increases and to profits), when there is little competition in reality.

■ Other regulations are widely used in all economic sectors in order to protect consumers from ‘market failure’ and to prevent such failures actually occurring.

■ There is considerable momentum behind removing regulations (i.e. deregulation) where this can be shown to be in the ‘public interest’. However, evaluating the welfare change from deregulation is a complex exercise.

■ In some cases, e.g. where deregulation still results in large firms playing a dominant role in the industry, the appointment of a regulator may help to remove at least some of the deadweight loss under the previous nationalized industry or monopoly type situation.

Now try the self-check questions for this chapter on the Companion Website. You will also find useful links to relevant websites.

Notes

1 For example, the transition from private to public ownership meant the takeover of some 550 separate local concerns in the electricity industry and over 1,000 local concerns in the gas industry.

2 Of course, to the extent that the ‘classical case’ against monopoly of higher price and lower output does not hold (see Chapter 3, p. 58) then no such deadweight loss need occur.

References and further reading

Bishop, M., Kay, J. and Mayer, C. (1994) Privatization and Economic Performance, Oxford, Oxford University Press.

Crew, M. and Parker, D. (2008) Developments in the economics of Privatization and Regulation, Cheltenham, Edward Elgar.

Gerard, R. (2008) Privatisation: Successes and Failures, Columbia, University Press Group. Griffiths, A. and Wall, S. (2000) Intermediate Microeconomics, Harlow, Financial Times/ Prentice Hall.

Helm, D. (1994) British utility regulation theory, practice and reform, Oxford Review of Economic Policy, 10(3): 17-39.

Humphreys, I. and Francis, G. (2002) Airport privatisation, British Economy Survey, Spring, 51-6.

Ingham, A. (2003) Rail privatisation revisited, Economic Review, February.

Lipczynski, J., Wilson, J. and Goddard, J. (2009) Industrial Organisation: Competition, Strategy, Policy (3rd edn), Harlow, Financial Times/ Prentice Hall.

McKenzie, G. (1998) Financial regulation and the European Union, Economic Review, April.

McWilliams, D. and Pragnell, M. (1996) Who will miss the PSBR? Financial Times, 30 September.

Menard, I. and Ghertman, M. (2010) Regulation, Deregulation, Reregulation Institutional Perspectives, Cheltenham, Edward Elgar.

Myers, D. (1998) The Private Finance Initiative - a progress report, Economic Review, April, 28-31. Oxford Review of Economic Policy (1997) Competition in regulated industries, 13(1), Spring.

Parker, D. (1991) Privatization ten years on: a critical analysis of its rationale and results, Economics, Winter.

Schwartz, G. and Lopes, P. S. (1993) Privatization: expectations, trade-offs and results, Finance and Development, June, 14-17. Sherman, R. (2007) Market Regulation, Harlow, Financial Times/Prentice Hall.

Stewart, G. (1997) Why regulate?, Economic Review, September.

Wilson, J. (1994) Competitive tendering and UK public services, Economic Review, April, 1-5.

Winston, C. (1993) Economic deregulation, Journal of Economic Literature, 31(September): 1263-89.

More on the topic Privatization and deregulation:

- Privatization and deregulation

- Theory of the firm

- International economics

- Concluding remarks

- WHEREOF ONE CANNOT SPEAK, THEREOF ONE MUST BE SILENT14

- Methods of integration