Corporate social and ethical responsibility

There is an increasing emphasis within organizations and governments on support for a variety of ethical and environmental principles often subsumed within the broad heading ‘Corporate Social Responsibility’ (CSR)! In this chapter we review the various definitions that have been proposed and the attempts that have been made to apply the concept in various types of organization and various geographical locations.

The case both for and against CSR is examined as is the role of CSR within the various ‘schools’ of economic thought, which are reviewed further in Chapter 9. Case study materials are also presented to illustrate the issues involved when seeking to implement CSR policies in practice. Various reasons are proposed as to why there has been such an increase in profile for CSR, and empirical evidence is assessed as to the impacts when firms seek to put CSR principles into practice. Of course it is recognized that many of the concerns to provide improved conditions for the workforce, including regulations on the hours worked and age of employment, on housing conditions, and on minimum levels of education and healthcare, have long pre-dated the use of CSR as a concept! William Owen in Port Sunlight, Joshua Rowntree and John Cadbury are well known UK examples of reforming industrialists, as are Krupp in Germany, Carnegie and Duke in the USA. Their endeavours in the early 19th century and subsequently would undoubtedly be termed CSR in today’s use of that term!Later in the chapter we examine separately and in greater depth CSR-type issues under the specific headings of corporate responsibility and governance, ethical conformance and codes of conduct, and sustainability approaches by the responsible corporation. This chapter develops further some of the discussions on firm objectives and firm behaviour in Chapter 3, especially those objectives identified as ‘behavioural’!

Corporate Social Responsibility (CSR): definitions and themes

Some organizations refer explicitly to CSR initiatives; others prefer to use alternative phraseology.

Marks & Spencer recently used the phrase ‘Plan A’ to represent a set of 100 worthy targets to be achieved in the period 2008-13. Publishers have used titles for books, such as ‘Corporation Be Good’ or the ‘A to Z of Corporate Responsibility’. The phrase ‘Socially Responsible Investment’ (SRI) is also widely used, as are phrases such as ‘building a sustainable business’ or ‘corporate citizenship’.It will be useful at this point to explore further what exactly is meant by CSR or its many derivatives! Table 15.1 usefully reviews the definitions of CSR adopted by a range of governmental, nongovernmental, corporate and social enterprises as a useful starting point.

The various definitions of CSR can, arguably, be characterized as including one or more of the following four core characteristics.

1 Incorporating voluntary activities - i.e. those going beyond any legal or regulatory requirement (e.g. (i), (ii) and (vii) in Table 15.1).

2 Taking externalities into account - where ‘externalities’ refers to both the adverse (negative) or beneficial (positive) outcomes of actions by organizations for which they are neither charged (cost) or recompensed (revenue) in the market (e.g. (iii), (vi) and (viii)).

3 Taking multiple stakeholders into account - i.e. not just the profit concerns of owners (principals), such as shareholders, but the concerns of employees, customers, suppliers, distributors, and all others with a vested interest in the organisation (e.g. all (i)-(vi) inclusive, and (viii)).

4 Incorporating organizational value/mission statements - i.e. not only involving operational or practice-oriented activities, but core belief systems of the organization (e.g. (v), (vi)).

Stakeholder approach to CSR

As we note above, the majority of the definitions in Table 15.1 take ‘multiple stakeholders into account’.

It will be useful, therefore, to briefly review the stakeholder approach to CSR. In the view of Milton Friedman (see p. 307), the Nobel prize-winning economist, managers and directors (agents) have the duty and responsibility to always act in the best interests of the owners (principals), namely the shareholders in a public or private limited company.

However, stakeholder theory takes a much broader view of the responsibilities of managers and directors. The acknowledged initiator of the stakeholder view, R. E. Freeman, suggested the following definition:A stakeholder is any group or individual who can affect, or is affected by, the achievement of a corporation’s purpose (Freeman, 1984, p. vi).

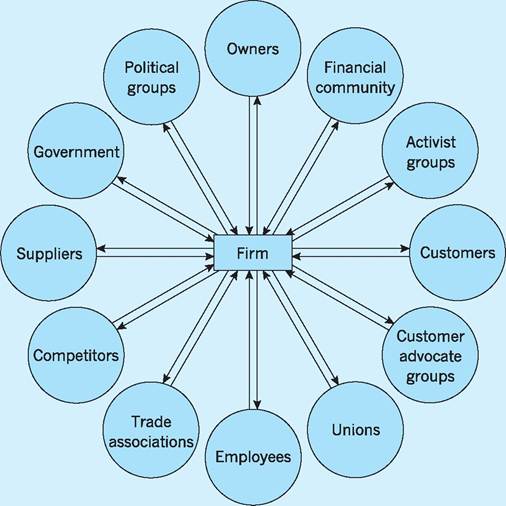

Arguably this definition helps more rigorously define the ‘S’ in ‘CSR’! In other words, instead of the vague ‘Social’ concept, we now focus more pragmatically on the groups or individuals in society who influence the companies’ activities or purposes, or who are impacted by those activities or purposes. Figure 15.1 outlines the various groups or individuals who might come within the stakeholder definition of a typical large corporation.

The ethical or moral dimension of stakeholder theory is the implication that if the company itself affects groups or individuals in seeking to achieve its goals, then these groups or individuals have a legitimate interest in the activities of that company. Of course, the extent of that interest is somewhat subjective - how do we weight the relative importance of the different stakeholders, whether in terms of the power they should be given to influence corporate policy or the significance we should give to the impacts of corporate policy on their wellbeing? In other words, while ‘stakeholder’ is arguably a more pragmatic concept than ‘social’, and an ethical case for the interests of such stakeholders in the activities of the company is more easily made, there is still a subjective issue as regards ‘weighting’ the importance of the various stakeholders in terms of both their permitted contribution to the decision-making processes and the relative valuation given to their ‘well-being’ when assessing the expected outcomes of different policy scenarios.

Table 15.1 Organizational definitions of CSR.

| Organization | Type of organization | Definition of CSR | Source | |

| (i) | UK government | Governmental organisation | ‘The voluntary actions that business can take, over and above compliance with minimum legal requirements, to address both its own competitive interests and the interests of wider society' | www.csr.gov.uk |

| (ii) | European | Governmental | ‘A concept whereby companies integrate | EC Green Paper, |

| Commission | organization | social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis' | 2001, Promoting a European Framework for Corporate Social Responsibility | |

| (iii) | Confederation of British Industry | Business association | ‘The acknowledgement by companies that they should be accountable not only for their financial performance, but for the impact of their activities on society and/or the environment' | www.cbi.org/uk/ |

| (iv) | World | Business | ‘The continuing commitment by business to | WBBCSD, 1999, |

| Business Council for Sustainable Development | association | behave ethically and contribute to economic development while improving the quality of life of the workforce and their families as well as of the local community and society at large' | ‘CSR: Meeting Changing Expectations' | |

| (v) | Gap Inc. | Corporation | ‘Being socially responsible means striving to incorporate our values and ethics into everything we do - from how we run our business, to how we treat our employees, to how we impact upon the communities where we live and work' | www.gapinc.com |

| (vi) | HSBC | Corporation | ‘Means managing our business responsibly and sensitively for long-term success. Our goal is not, and never has been profit at any cost because we know that tomorrow's success depends on the trust we build today' | |

| (vii) | Christian Aid | Non-governmental organization | ‘An entirely voluntary, corporate-led initiative to promote self-regulation at either national or international level' | ‘Behind the Mask: The Real Face of Corporate Social Responsibility', 2004 |

| (viii) | CSR Asia | Social enterprise | ‘A company's commitment to operating in an economically, socially and environmentally sustainable manner while balancing the interests of diverse stakeholders' | www.csr-asia.com |

| Source: Adapted from Crane etal. (2008), pp | 6-7. | |||

Fig. 15.1 Stakeholders in a large organization.

I CSR: a growth phenomenon

Why has CSR in general, and these core characteristics in particular, become so important in the pronouncements and activities of so many organizations and their representatives in recent times? Here we examine some of the key reasons for the increased prominence of CSR, some of the reasons being somewhat ‘defensive’ in nature, i.e. seeking via CSR to avoid potential damage, but others being more ‘positive’ and proactive, i.e. seeking via CSR to increase potential benefits to the organization. We shall review both types of motive as we first examine the case for organizations supporting CSR initiatives.

Case for CSR

Here we review some of the arguments widely used to support the resurgence of interest in CSR which many analysts trace back to the 1950s, and to the US in particular.

There are a number of arguments which are advanced under the broad heading of ‘enlightened self-interest’ for the organizations concerned.Risk management: avoiding reputational damage

The experience of companies such as Enron, WorldCom, Global Crossing and Parmalat vividly portrays what can happen to companies and share prices when corporate scandals become the focus of 24/7 media coverage. Avoiding reputational damage by putting in place explicit codes of behaviour and reporting regularly on ethical and social activities to shareholders, often in annual ‘social responsibility’ reports, has become an expectation of the many analysts, credit rating agencies and non-governmental organizations closely scrutinizing multinational corporate behaviour especially! Organisations are increasingly expected to report on their non-financial as well as financial performance, especially given the awareness of shareholders of the impact of corporate disasters such as the explosion at the Bhopal pesticide factory in India, the oil spills of the Exxon Valdez in Alaska and more recently BP in the Gulf of Mexico, the exposure of Nike’s and Gap’s use of child labour, the resistance of pharmaceutical companies to providing cheaper generic antiretroviral treatments for HIV/AIDS, and so on. In this sense the development of CSR policies becomes an explicit element in ‘risk management’ used by organizations and their representatives in an effort to avoid incidents which might damage their reputation.

Revenue and profit enhancement

Here we review a less defensive and more proactive reason often advanced for the growth of CSR and which can be linked to a number of positive financial associations.

CSR is positively correlated with revenue/profit outcomes

It has often been suggested that firm behaviour which seeks to be more than usually ethical or to give considerable weight to environmental concerns must do so at the expense of profit. However, many firms are now seeing ethical and environmentally responsible behaviour as being in their own self-interest, with demand curves shifting to the right (increasing) the closer the alignment of products with positive social/ ethical initiatives.

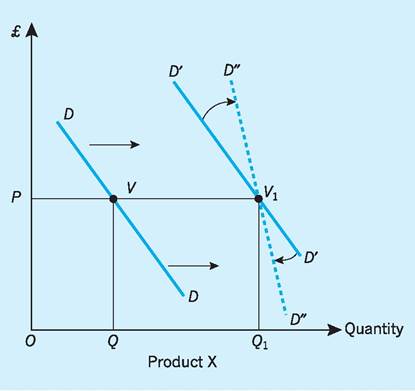

In Fig. 15.2 this is shown as a shift in the demand curve from D to D'. At any given price, consumers will purchase more of the product, raising total revenue at price P in the diagram from OPVQ to OPV1Q1. However, there is a further possible revenue-raising strategy that may now be possible! By creating a more positive ethical/environmental association with the product, CSR initiatives may also result in the demand curve pivoting from D' to D" in Fig. 15.2. The demand curve will now be less price-elastic, giving opportunities for the firm to raise prices and increase revenue, since demand falls by less than in proportion to the price rise.Firms are increasingly aware of the benefits of aligning themselves with ethical and ecological initiatives. Various ‘kitemarks’ exist for firms to certify that their product conforms to ethical standards in production, as for example ‘Rug-Mark’ for carpets and rugs, ‘Forest Stewardship Council’ mark (to certify wood derived from sustainable forestry extraction

Fig. 15.2 Demand increases and becomes less elastic with successful CSR campaign.

methods) and the ‘Fairtrade’ mark (guarantees a higher return to developing country producers).

Indeed, it was reported in 2010 that annual sales of Fairtrade food and drink in the UK have reached over £500m, having grown at over 40% per year over the past decade. It has expanded from one brand of coffee ten years ago to around 1,000 foodstuffs, including chocolate, fruit, vegetables, juices, snacks, wine, tea, sugar, honey and nuts. A Mori poll in 2010 found that two-thirds of UK consumers claim to be green or ethical and actively look to purchase products with an environmental/ethical association. At the sectoral level, many of the UK’s biggest retail names have joined the Ethical Trading Initiative (ETI) which brings together companies, trade unions and nongovernmental organizations in seeking to ensure that the products sold in their retail outlets have not been produced by ‘sweatshop’ labour working for next to nothing in hazardous conditions.

At the corporate level, Exxon Mobil seems to be an example of a company that has accepted the linkage between ethical/environmental practices and corporate profits. It announced in late 2003 that it had been holding discreet meetings with environmentalists and human rights groups worldwide in an effort to change its unfavourable image in these respects. The charm offensive has been linked to fears at Exxon’s Texas headquarters that a negative public image is threatening to damage its Esso petrol brand, which has faced ‘stop Esso' boycotts in the EU and elsewhere following its being linked to supporting the then US President Bush's boycott of the Kyoto agreement on protecting the climate.

An analysis by Geoff Heal (2008) of Columbia Business School indicated that as much as $1 out of every $9 under professional investment management now involves an element of SRI, so important do firms believe the linkage to be between this type of investment and financial outcomes of that investment.

DSM and TNT, the Dutch life sciences group and postal operator, respectively, joined a growing band of companies in February 2010 - predominantly from the Netherlands - that link part of the bonuses which senior management receive to sustainability, seen by them as an all-encompassing term that refers not only to the environment but to issues such as employee satisfaction and safety.

CSR is positively correlated with share price

At a more aggregative level, attempts are now being made to incorporate ethical/environmental considerations into formal stock exchange indices in the UK and other financial markets. A new FTSE 4 Good Index was launched in July 2001, using social and ethical criteria to rank corporate performance. All companies in three sectors were excluded, namely tobacco, weapons and nuclear power (representing 10% of all FTSE companies). Of the remaining companies, three criteria were applied for ranking purposes: environment, human rights and social issues. If a company ‘fails' in any one of these criteria, it is again excluded. Of the 757 companies in the FTSE All Share Index, only 288 companies have actually made it into the index. The FTSE itself has produced figures showing that if this new FTSE 4 Good Index had existed over the previous five years, it would actively have outperformed the more conventional stock exchange indices. The same has been found to be true for the Dow Jones Sustainability Group Index in the US. This is a similar ethical index introduced in the US in 1999. When backdated to 1993 it was found to have outperformed the Dow Jones Global Index by 46%.

Providing strategic direction

Porter and Kramer (2006) published a paper on how CSR could, if approached in a strategic way, help enhance an organization's competitive advantage over its rivals. The key element in their analysis is the suggestion that organizations embed CSR in their operational, global supply chain, investor relations and other strategies at every level, so that CSR becomes ‘part of the corporate DNA'. CSR then influences all decisions across the organization and gives the organization a competitive edge, thereby adding value.

As Fig. 15.3 illustrates, Porter and Kramer (2006) have identified two types of the CSR-Strategy relationship, i.e. responsive and strategic CSR. Responsive CSR is defined as being a reaction to various legal,

Fig. 15.3 Corporate involvement in society: a strategic approach.

Source: Porter and Kramer (2006). The link between competitive advantage and corporate social responsibility, Harvard Business Review, 84(12), p. 89.

Fig. 15.4 Putting ethical/environmental strategies into practice using the value chain.

Source: Porter and Kramer (2006). The link between competitive advantage and corporate social responsibility, Harvard Business Review, 84(12).

social or intrinsic pressures. The companies which practice responsive CSR ‘will gain an edge, but... any advantage is likely to be temporary’ (Porter and Kramer, 2006). Strategic CSR, on the other hand, goes beyond best practices, as ‘it is about choosing a unique position... arising in the product offering and the value chain.’ It provides gains through the synergy of consistently applied CSR and strategy, bringing competitive advantage and, at the same time, generating value for society.

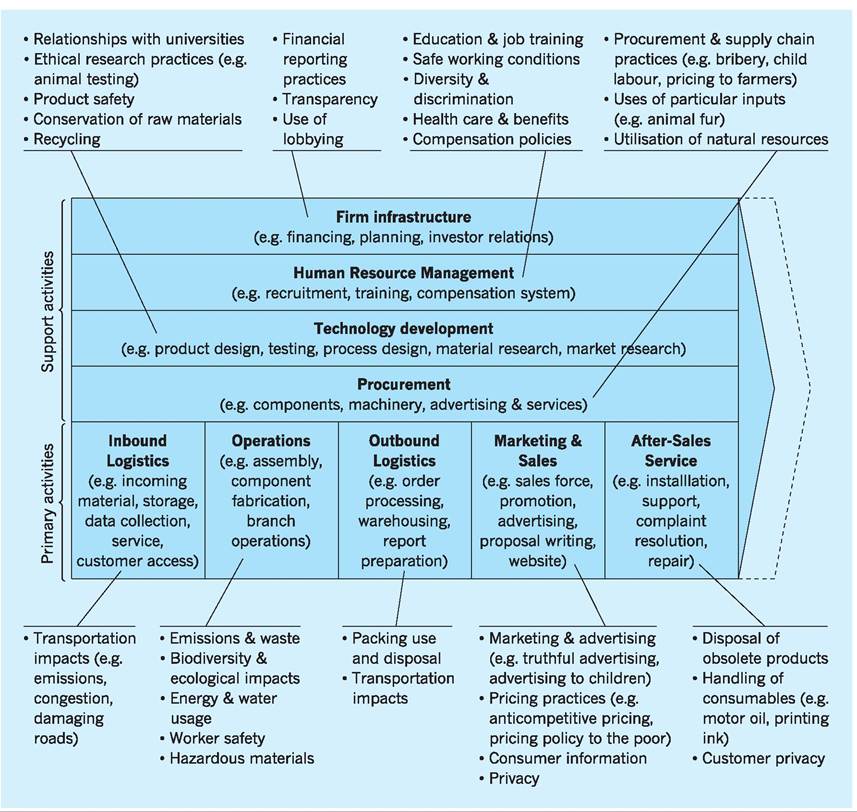

Porter and Kramer identify a range of potential policies associated with aspects of the organization’s value chain which might become a focus for policy action when using CSR in a strategic way. As Fig. 15.4 indicates, there are a wide range of CSR- related policy options that organizations might adopt if they are to strategically ‘brand’ and differentiate themselves in terms of their value chain.

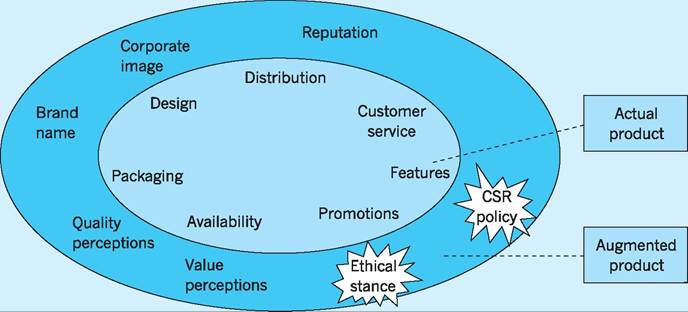

In fact, some organizations may so focus on CSR- related aspects that, in effect, they are developing an

Fig. 15.5 Augmented product and strategic CSR. Source: McDonald (2007), p. 275.

‘augmented product’ which has a perception amongst consumers that goes well beyond the realities of the actual product! In Fig. 15.5 the actual product has certain characteristics/features and an associated value chain. However, the explicit, strategic CSR emphasis creates an augmented product in consumer perception which is more closely aligned in many ways with those CSR features than with the actual product value chain itself! Such organizations instigate well-advertised, grand-scale initiatives, dedicating significant resources to ethical behaviour, and often try to engage the public in their projects. Companies in this position are likely to devise codes of conduct; establish procedures for the implementation and processes resulting from such values; and publish detailed triple bottom line reports. Also, many of them work closely with non-governmental organizations (NGOs) in a relevant field aiming to achieve a high level of transparency for their operations (e.g. Ecover).

The reality for Porter and Kramer and many other analysts is that CSR and organizational strategy are often only loosely and intermittently connected! In a global study in 2007, McKinsey consultants found a shortfall of over 25% between what respondents believe their organizations should do in terms of CSR and what they say their organization actually does! At the individual product level Toyota has been criticized for its strategic inconsistency in supporting ‘green’ sustainable transport with its Prius hybrid model, but at the same time joining other car companies in lobbying the US and other governments to resist imposing standards in terms of minimum miles/km per gallon/litre on fuel consumption in their vehicles.

CSR and the dynamic capabilities view

The so-called ‘dynamic capabilities view’ points to the sources of competitive advantage having less to do with the intrinsic capabilities of the traditional factor inputs (e.g. labour and capital) than with the ways in which these are engaged and deployed within the organization! The emphasis here is on the organizational and strategic routines by which managers modify, integrate and recombine their factor inputs and resources to generate new value-creating strategies. A number of authors (e.g. Teece et al. 1997; Petrick and Quinn 2001) have identified the approaches and policies of the organizations as regards social and ethical issues as sources of competitive advantage, as in the organizational approach to moral decision-making.

Case against CSR

Misuse of scarce resources

The main argument against CSR under this heading is the suggestion that managers do not have the moral right to waste valuable resources on social and related initiatives, as this is detrimental to the efficiency of the business, but should instead seek to use scarce resources to increase the company’s (and the owners’) profits. This view has been strongly advocated by critics of CSR such as Milton Friedman.

There is one and only one social responsibility of business - to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception or fraud (Friedman 1970, p. 126).

Writing some 30 years later Wolf reinforced this view of CSR as essentially misunderstanding the key function of business.

The role of well run companies is to make profits, not save the planet (Wolf 2000, p. 21).

However, as Fisher and Lovell (2009) point out, Friedman’s argument does allow for a form of corporate philanthropy where such activities can be shown to bring higher profitability and returns to owners than any alternative investment opportunities! However, Friedman would argue that such ‘calculative’ behaviour is nothing more than normal commercial investment appraisal as the motivation behind such calculations is explicitly financial and involves no ethical concern for the beneficiary (-ies) and therefore does not fall into the conventional domain of CSR!

Friedman criticizes the traditional arguments in favour of CSR from at least three perspectives.

1 Economic. Friedman argues that companies are responsible for using shareholders’ funds in profitable ways and in legally acceptable ways, nothing more! Friedman points out that focusing on charities and schools and engaging in corporate philanthropy distorts allocative efficiency as it ‘takes management’s eye off the ball’, namely securing higher profits for owner-shareholders.

2 Ethics and political philosophy. Friedman insists that it is inappropriate for corporations to use shareholders’ funds to support good causes since ‘any such donations can only come at the expense of lower dividends, higher prices or lower wages (or a combination of all three)’. Friedman asked the rhetorical question ‘how can it be ethical that a corporation should act first as unpaid tax collector (i.e. levying a ‘tax’ on the shareholders/customers and/or employees) and then as unaccountable benefactor?’ In the view of Friedman it is the responsibility of publically elected representatives at national or local levels to levy real taxes and in due course be accountable to the electorate, both for the taxes themselves and for the uses to which they are put. In other words, if the tax revenues are used to provide financial support to charities or for other welfare or social services, then in a democratic state the electorate can confirm or withhold its support for such taxes and their uses at the ballot box. Only publically elected representatives of the people or private individuals acting voluntarily have, in Friedman’s view, the right to make financial donations of this type.

3 Philosophical. In Friedman’s view businesses cannot have responsibilities, because they are not real people, they are social constructs dependent on legal definitions and legal protections for their existence. Only individuals can have responsibilities, not corporations.

We now turn our attention to organizational responses to the rather broad CSR definitions and issues already outlined. We first focus on corporate responsibility in the increasingly high profile area of sustainability policies and approaches, then on broader areas of appropriate ethical behaviour, before turning our attention to the internal management and supervision of such policies via the corporate governance framework and various codes of conduct.

Corporate responsibility

The term ‘corporate responsibility’ is increasingly in use, the omission of ‘social’ being seen by many as a recognition that the responsibilities of corporations extend over a still broader range of issues, especially those involving environmental and ethical concerns.

Environmental and ecological responsibilities

In today’s global economy a number of driving forces are arguably raising environmental concerns to the forefront of corporate policy debate, which is the

focus of this section - a broader, less corporate review of environmental issues and policies is undertaken in Chapter 10.

■ Environmentally conscious consumers. Consumer awareness of environmental issues is creating a market for ‘green products’. Patagonia, a Californiabased producer of recreational clothing, has developed a loyal base of high-income customers partly because its brand identity includes a commitment to conservation. ‘Every day we take steps to lighten our footprint and do less harm.’ A similar successful approach has been used by Timberland (‘our love for the outdoors is matched by our passion for confronting global warming’) and the Body Shop. Consumers have long claimed to be more virtuous than they are. Retailers called it the ‘30:3 phenomenon’ - 30% of purchasers told pollsters that they thought about workers’ rights, animal welfare and the state of the planet when they decided what to buy, but sales figures showed that only 3% of them acted on those thoughts. Now, however, retailers are behaving as if consumers mean it. A Mori poll found that two-thirds of UK consumers claimed to be ‘green’ or ethical and actively look to purchase products with an environmental/ethical association. We noted earlier that annual sales of Fairtrade food and drink in Britain had reached over £500m in 2010, having grown at over 40% per year over the past decade. In the UK, J. Sainsbury is selling only bananas with the Fairtrade label, which guarantees a decent income to the grower. Marks & Spencer is stocking only Fairtrade coffee and tea and is buying a third of the world’s supply of Fairtrade cotton. In the US, Dunkin’ Donuts has decided to sell only Fairtrade espresso coffee in its North American and European outlets. Wal-Mart has devoted itself to a range of ‘sustainability’ projects.

■ Environmentally and credit-risk-conscious producers. International businesses are increasingly aware that failure to manage environmental risk factors effectively can lead to adverse publicity, lost revenue and profit and perhaps even more seriously a reduction in their official credit rating, making it more difficult and costly (e.g. higher interest rates) to finance future investment plans. BP has found that the Gulf of Mexico oil-spill in April 2010 cost it $10bn in clean-up operations, $1bn in compensation to those individuals and businesses directly affected, $70bn in market capitalization via a 50% fall in its share price in the following six months. All this does not even include ongoing litigation for breaches in health and safety regulations prior to the explosion and oil spill, and loss of reputation and of ‘preferred bidder’ status in many ongoing bids for new exploration in the US and elsewhere.

A 2010 Populus poll of energy consumers in the UK found that their choice of energy supplier was significantly influenced by the following factors:

■ how hard the supplier is working to use resources effectively and reduce waste;

■ level of supplier investment in renewable energy;

■ the extent to which the supplier is helping me to become more environmentally efficient;

■ how hard the supplier is working to address climate change;

■ the supplier’s approach to biodiversity.

The above five factors were all in the top seven factors identified by consumers as ‘important’ when choosing an energy supplier, all scored over 3 on a scale from 0 (completely unimportant) to 5 (very important indeed), and all had increased their scores (by around 10%) since the previous Populus survey in 2008.

■ Environmentally conscious governments. Businesses have a further reason for considering the environmental impacts of their activities, namely the scrutiny of host governments. Where production of a product causes environmental damage, it is likely that this will result in the imposition of taxes or regulations by government. In the EU, strict new regulations on maximum emissions of greenhouse gases by vehicles are forcing car manufacturers to change engine/chassis designs and sizes to comply with the new regulatory environment. For example, a legally binding EU regulation of a maximum emission of 130 grams of CO2 per kilometre driven by new cars comes into force in 2015. As we note below, in 2008 the US and EU governments made it a criminal offence to import illegal timber, given environmental concerns involving deforestation.

Environmental sustainability

‘Sustainable’ and ‘sustainability’ are now key trigger words in the world of advertising for positive, emotive images associated with words such as ‘green’, ‘wholesome’, ‘goodness’, ‘justice’, ‘environment’, amongst others. They are used in a sophisticated manner to sell cars, nappies, holidays and even lifestyles. Sustainability sells - how has this come about and what exactly are we being encouraged to buy?

As long ago as 1987, a United Nations report entitled Our Common Future provided the most widely used definition of sustainable development: ‘development which meets the needs of the present without compromising the ability of future generations to meet their own needs’ (World Commission on Environment and Development, 1987). Of course, there have been many different views as to how this definition should affect individual, corporate and government actions, though one theme that has been constant in most views is that of ‘intergenerational equity’, i.e. where the development process seeks to minimize any adverse impacts on future generations. These clearly include avoiding adverse environmental impacts such as excessive resource depletion today reducing the stock of resources available for future use, or levels of pollution emission and waste disposal today beyond the ability of the environment to absorb them, thereby imposing long-term damage on future generations.

Forests and deforestation provides a useful case study, illustrating how environmental and ecological dilemmas impact on corporate interests and activities.

Forestry and corporate responsibility

The vital contribution of forests to a sustainable global environment has long been recognized, especially their ability to give out oxygen and absorb and store carbon. Of course, destroying forests for wood, for increased plantation or cattle rearing works in reverse - with around half the dry weight of a tree consisting of stored carbon, much of which is released into the atmosphere when trees are burned or left to rot. In fact, around half the earth’s total forest area has been cleared by man-made interventions in the past 10,000 years, and today continued deforestation contributes some 15-17% of the world’s annual emissions of carbon dioxide (CO2). Of course, forest clearance does still more damage than this, with the loss of plant sources of many modern medicines and animal species, as well as threatening the habitats and livelihoods of some 400 million of the world’s poorest people, and resulting in increased flooding as bare hillsides fail to absorb rainfall as effectively as in the past.

The increasing emphasis of the media on such environmental issues has, of course, increased pressures on corporations and governments to advance more ‘responsible’ approaches to forests and their many products and uses. A UN supported organization ‘The Economics of Ecosystems and Biodiversity’ (TEEB) has estimated that negative externalities from forest loss and degradation cost between $2trillion and $4.5trillion each year!

The prominence given to the important role of forests in ‘sustainability’-related concerns is providing both positive and negative incentives for corporations to adopt policies consistent with increased environmental responsibility.

■ Positive incentives. On the positive side, governments and environmental agencies are providing incentives of various kinds to encourage a more responsible corporate attitude towards forestry. For example, agricultural companies and farmers are benefitting from incentives in the form of Payments for Ecosystem Services (PES) to reforest agricultural land - in China farmers in the vicinity of the Yangzi River are paid $450 a year per reforested hectare, in an attempt to lessen flooding damage. Costa Rica offers $45-163 per reforested hectare

■ Negative incentives. On the negative side, failure to support sustainable forestry can result in serious damage to corporate profitability. Nestle has been targeted by Greenpeace with negative blogs and adverts exposing links between the production of chocolate for Kit Kat bars and associated deforestation in Indonesia; around half of the forest areas cleared for crops in Indonesia are used for oil palms, mainly for chocolate production. The impact of such negative publicity was deemed so severe by Nestle that it ceased buying palm oil from its main Indonesian supplier, Sinar Mas, and promised to remove from its supply chain any producer of palm oil linked to deforestation.

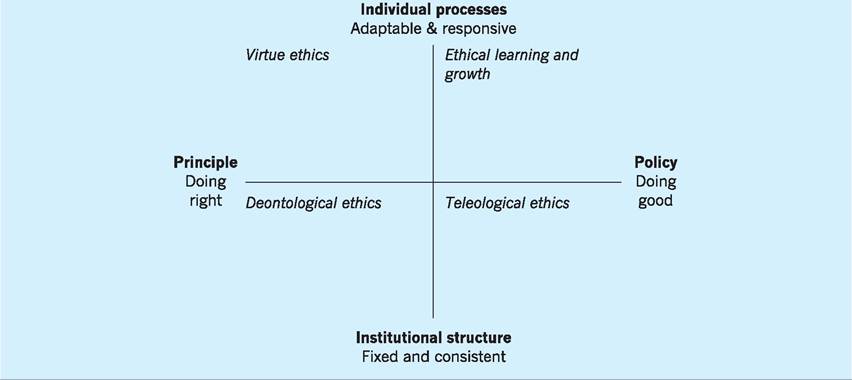

Fig. 15.6 A framework for ethical theories. Source: Adapted from Fisher and Lovell (2009).

Ethical responsibilities and codes of conduct

Over time a wide range of ethical theories has developed, with individuals and groups supporting or challenging them! Figure 15.6 gives a broad ‘map’ of the range of ethical theories available and it may be useful at this point to define the terms on the horizontal and vertical axes, before turning briefly to the ethical theories themselves.

Horizontal axis

■ Principles - standards to be observed, seen as desirable in terms of fairness/justice or some other moral dimension in their own right, irrespective of the outcome of following those principles. This approach is sometimes referred to as a ‘duties’ view of ethical behaviour - things to be done (or avoided) because they are intrinsically right or wrong.

■ Policies - approaches that achieve measurable outcomes which are regarded as improvements on the original situations. This approach is sometimes referred to as a ‘consequential’ view of ethical behaviour - things to be done (or avoided) because they will have consequences which result in an overall net benefit or loss.

Along this horizontal axis, some ethical theories are seen as focusing primarily on the ‘rightness’ of some action or approach or on the ‘outcome’ of that action or approach in terms of making a net overall improvement for the individual or group.

Vertical axis

■ Individual processes - approaches that emphasize the responsibilities of individuals to develop/ improve themselves or the group(s) to which they belong.

■ Institutional structure - approaches that emphasize the importance of establishing institutions and structures that exist and operate independently of the individuals who devise them, but which determine the key principles which underpin ethical considerations.

Of course any such diagram is over simplistic, but it does give us a useful starting point to consider various ethical theories in the context of our previous discussions.

■ Virtue ethics. This broadly corresponds to theories which emphasize individuals having the responsibility to respond to the question ‘What would a virtuous person do in this situation?’ Plato is often associated with this approach, identifying the four virtues of wisdom, courage, self-control and justice. His follower, Aristotle, identified key personal qualities associated with achieving these virtues, especially ‘justice’, namely liberality (especially as regards money), truthfulness, patience, magnanimity. These virtues and personal qualities were seen as desirable ends in their own right, whatever the outcomes of practising them!

■ Deontological ethics. While the emphasis is still on universal principles to be followed because of their intrinsic ‘rightness’, irrespective of outcomes, there is a recognition that individuals act within a social and institutional context which gives them a sense of shared identify and commitment to the values of their group. Kantian ethics come under this heading, with actions to be guided by universal principles and deemed morally acceptable only if carried out as a duty, rather than in expectation of any reward or reciprocity. Kant used the term ‘categorical imperative’ to refer to principles that must be obeyed, with no exceptions.

■ Ethical learning and growth. Located in the topright quadrant of Fig. 15.6, the emphasis here is on ethical behaviour being tested by outcomes but ones that are based on individual morality, and cannot be imposed by institutional decree (e.g. codes of conduct). Ethical behaviour can only be encouraged indirectly from this perspective by providing learning experiences from which individuals derive their own ethical codes of behaviour.

■ Teleological ethics. These are again outcome- oriented ethical theories, but which see institutions as necessary to achieve these desirable ethical outcomes. The term ‘teleological’ means that the rightness or goodness of an action is not intrinsic to that action, but must be judged on the merits of its outcomes. Utilitarianism is often placed under this heading, with the emphasis here on institutions or organizations seeking to achieve the greatest good of the greatest number: ‘The greatest happiness of the greatest number is the foundation of morals and legislation’ (Bentham 1843, p. 142). In this sense, utilitarianism is a calculated approach to ethics, with the costs and benefits of institutional actions assumed to be capable of valuation and ranking.

CSR perspectives and ethical frameworks

Perspectives

■ Friedman perspectives. In terms of our earlier analysis, Friedman’s view on businesses (not individuals) having the primary responsibility of achieving profit, and their having no right to engage in distracting philanthropy would locate his perspective in the bottom - left quadrant of Fig. 15.6, i.e. ‘Deontological ethics’. His emphasis is on the ‘rightness’ of a shareholder focus by the business and on the business as an ‘institutional’ and social construct, dependent on legal definitions and legal protections for its existence (Friedman 1970, p. 126). However, the variant of Friedman’s position which emphasizes investigating the profit- related outcomes of philanthropy, rather than the intentions behind it, would arguably justify placing his approach into the bottom right quadrant, i.e. ‘Teleological ethics’, with the outcome of philanthropy or gift giving to be judged in terms of outcomes rather than ‘rightness’.

■ Stakeholder perspectives. The broader stakeholder perspective was reviewed earlier (p. 300) and might be more readily located on the right-hand side of Fig. 15.6 with its emphasis on balancing the outcomes of corporate actions amongst the various ‘interested parties’ within the organization. Of course, it could be located in the topright quadrant under ‘Ethical learning and growth’ should the emphasis be on individual behaviour conforming to these stakeholder principles. Here the focus would be on developing an ‘atmosphere’ conducive to moral behaviour at an individual level within the organization. However, should the emphasis be on institutional behaviour being aligned with a stakeholder approach, as in the case of organizational codes of conduct, then it might more accurately be located in the bottom-right quadrant under ‘teleological ethics’.

It is to these ‘codes of conduct’ that we now turn our attention.

Fig. 15.7 Codes of conduct and ethical frameworks. Source: Fisher and Lovell (2009), p. 388.

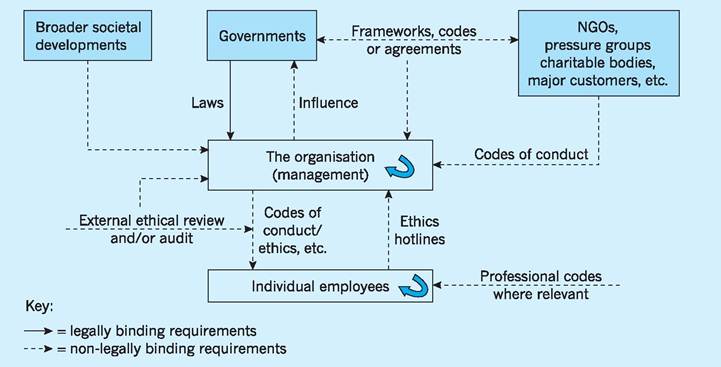

Codes of conduct

As Fig. 15.7 indicates, some of the pressures for organizations to exhibit ethical and socially responsible behaviour stem directly from the explicit legal environment in which the organization operates. The only continuous and unbroken line in Fig. 15.7 indicates the legally binding (mandatory) requirements as regards ‘corporate’ behaviour imposed on the organization by national and supra-national (e.g. EU) governmental bodies. The broken lines represent the many ethical frameworks and codes of conduct which, while technically voluntary, provide important constraints and contexts for organizational behaviour.

Non-governmental organizations such as Greenpeace, Friends of the Earth, International Baby Food Action Network and other charities and pressure groups will contrast organizational performance against agreed or proposed codes of conduct and ethical frameworks. The codes of conduct the organization itself may impose (usually these are ‘top-down’ initiatives!) on its own employees and operations will often be an attempt to regularize processes and steer behaviours to align the outcomes of organizational performance more closely with the external pressures and expectations from governments, NGOs and the broader society.

The ‘ethics hotlines’ in Fig. 15.7 include mechanisms for employees to raise concerns about current behaviours and practices - giving organizations themselves early warning of possible problems as well as providing avenues for expressing concerns which might otherwise result in ‘whistleblowing’ to a more critical external audience.

Table 15.2 provides a useful summary of some of the advantages and disadvantages of using codes of conduct. Of course, the operation of these codes of conduct can be reviewed annually or periodically by external ethical audits. In addition, a variety of ‘informal’ mechanism can be used to support such codes in seeking to influence organizational values and behaviour, including reward systems, training, storytelling, recruitment and selection policies and processes, ethics officers, etc.

Codes of conduct versus codes of ethics

Whilst these terms are sometimes used interchangeably, codes of conduct tend to be a more prescriptive set of rules or instructions as regards employee behaviour. They identify specific actions that must be undertaken or avoided! Codes of ethics tend to be more general and to emphasize attitudes and characteristics (honesty, diversity, loyalty, integrity, etc.) to be exhibited, rather than actions to be taken/ avoided.

Table 15.2 Codes of conduct: advantages and disadvantages.

Advantages

Disadvantages

Reduces the need for governmental regulation or intervention

Limits the potential damages awarded when the organization can be seen by the court to have an explicit policy even when not followed by individual employees

Enhances trust, customer loyalty and reputation

Creates benchmarks against which the organization’s practices can be compared

Creates pressure from internal and external stakeholders to follow through on commitments by formalizing and publishing commitments

Creates potential for competitive advantage

Flexible, can be uniquely adapted to that organization

Creates order and structure in standards and procedures acceptable to the organization when operating globally

Allows stakeholders influence in decision-making

Relatively inexpensive

Cannot enforce full implementation as voluntary codes Lack rigorous mechanisms to ensure accountability Often written as broad philosophical statements therefore hard to measure

Those adopting are often already leaders in CSR issues in those sectors

Often unknown to majority of employees

Such codes tend to be over-represented in industries and sectors with high visibility and with a focus on brand image or reputation and large environmental or social impacts (often business to customer products) Often do not include complaints processes or whistleblower protections

I Corporate governance

Corporate governance refers to the various arrangements within an organization which provide both authority and accountability in its operations. In other words, it refers to a wide range of formal structures, procedures and regulations governing the means by which decisions are made, communicated and operationalized within an organization. The earlier debate in Chapter 3 on the separation between ownership and control via the rise of public and private limited companies and associated principalagent issues is certainly relevant here, as is the whole set of formal legal, accounting and other regulations relevant to different categories of company and to the ways in which decisions are made, communicated and enforced (see Chapter 2).

The many corporate scandals over the centuries have tended to result in legislation and regulations seeking to clarify the respective responsibilities of corporations and their shareholders. The ‘Bubble Act’ of 1719 was an attempt to protect future shareholders from the distortions and misleading pronouncements of the Board of the South Sea company which had led to financial ruin for so many investors.

Before reviewing some major developments in corporate governance in the UK and US, it may be useful to note that the term can be used in a context much wider than the usual one involving financial and regulatory aspects only. For example, Sir Adrian Cadbury made the following statement in his submission to the World Banks’ 1999 Report on Corporate Governance:

Corporate governance is concerned with holding the balance between economic and social goals and between individual and community goals...... The aim is to align as

nearly as possible the interests of individuals, corporations and society (Sir Adrian Cadbury, reporting to the King Committee on Corporate Governance 2002, p. 6).

We first check out developments towards such ambitious aims for corporate governance in the high-profile area of executive remuneration.

Corporate governance and executive remuneration

We have already reviewed (Chapter 3, p. 53) executive pay in the context of the principal-agent problem. In Europe 84% of companies place decisions about executive pay in the hands of their compensation, or remuneration, committee, according to a survey Executive Compensation by consultants, Hewitt, Bacon and Woodrow (Thomas 2009). So, ultimately it is remuneration committees that are as responsible as anyone when executive pay appears to bear scant relationship to corporate performance. Pension and Investment Research Consultants (PIRC), the UK corporate governance watchdog, regularly reports that the pay of executive directors at FTSE 100 companies has spiralled high above inflation.

The rapid rise in executive pay, when the companies themselves have been performing modestly at best, has created widespread criticism from shareholders and others. Stock options have been a particular source of criticism - the practice whereby senior executives have been given the ‘option’ of buying company shares at a heavily discounted price (i.e. lower than the market price) and then selling them at a profit should they succeed in raising the share price above an agreed target. Often, exercising these options has given far more income to executives than their basic salaries.

Table 15.3 provides a useful review of Chief Executive Officer (CEO) remuneration packages around the world (Watson Wyatt Worldwide 2009). In the US some 60% of total CEO compensation is in the form of incentive plans (stock options, etc.), with only 23% of such compensation derived from basic salary and a further 17% from cash bonuses.

Table 15.3 Structure of CEO remuneration packages around the world.

| Country | Base salary (%) | Cash bonus (%) | Incentive plan compensation (%) |

| US | 23 | 17 | 60 |

| Brazil | 27 | 41 | 32 |

| Germany | 39 | 47 | 14 |

| UK | 40 | 38 | 22 |

| France | 44 | 25 | 31 |

| Ireland | 44 | 43 | 13 |

| Hong Kong | 51 | 19 | 30 |

| Netherlands | 51 | 28 | 21 |

| Belgium | 52 | 26 | 22 |

| Italy | 52 | 29 | 19 |

| Japan | 71 | 12 | 17 |

Note: Companies with revenues between $1bn and $3bn.

Source: Watson Wyatt Worldwide (2009) Executive pay practices around the world.

The situation is, however, reversed in Japan with 71% of CEO compensation consisting of basic salary, 12% cash bonuses and only 17% via incentive plans. EU countries tend to be somewhere in between these two extremes.

Table 15.4 broadly supports the suggestion that the most important sources of executive remuneration lie outside the base salary. For the five executives with the highest total remuneration package among the FTSE 100 in 2010, it is clear that the base salary is one of the least important sources of executive remuneration. The highest share of the total

Table 15.4 Top five earners in the FTSE 100 2009/10.

| Company | Name/role | Base salary | Cash bonus | Benefits and other | Share incentives | Total remuneration |

| Reckitt Benckiser | Chief executive | £0.99m | £3.52m | £0.083m | £88.00m | £92.59m |

| Berkeley Group Holdings | Executive director | £0.75m | £0.75m | £0.156m | £34.71m | £36.37m |

| Xstrata | Chief executive | £1.31m | £1.31m | £0.314m | £22.58m | £25.51m |

| Icap | Chief executive | £0.36m | £1.50m | £0.669m | £21.80m | £24.33m |

| BG Group | Chief executive | £1.14m | £1.13m | £0.005m | £20.77m | £23.06m |

| Source: Various. | ||||||

Table 15.5 CEO compensation in the FTSE 100.

| Year | Average CEO | Average employee earnings (£) | Multiple |

| 1998 | 1,012,380 | 21,540 | 47 |

| 1999 | 1,235,401 | 20,939 | 59 |

| 2000 | 1,684,900 | 24,070 | 70 |

| 2001 | 1,812,750 | 24,170 | 75 |

| 2002 | 2,587,474 | 24,182 | 107 |

| 2003 | 2,773,904 | 24,767 | 112 |

| 2004 | 3,121,435 | 25,955 | 119 |

| 2005 | 3,312,285 | 27,254 | 121 |

| 2006 | 3,339,421 | 30,828 | 107 |

| 2007 | 3,935,820 | 25,677 | 151 |

| 2008 | 3,950,642 | 30,994 | 128 |

| 2009 | 3,710,440 | 32,521 | 115 |

remuneration package accounted for by the base salary was 5.1%.

Size of executives’ compensation

Of course it is not just variations in the sources of executive remuneration that are often in focus, but also in the absolute totals of such compensation.

Totals of executive compensation

Thomas (2009) concluded, having reviewed various global CEO pay surveys, that the US paid by far the largest remuneration packages to executives. Citing work by Towers Perrin, he demonstrates that total CEO pay in Germany is some 51% of that to be expected in comparable companies in the US, with a still lower figure of 44% from Sweden and 21% for China.

Table 15.5 shows the average CEO compensation across the FTSE 100 companies over the period 19982009, the average employee earnings across those companies and the multiple between the two. Clearly the general trend has been one whereby the multiple is rising, though with some reduction in the recessionary period 2007-2009. However, the change from a situation whereby the average CEO salary of FTSE 100 companies was 47 times the average employee salary in 1998 but 115 times that salary in 2009.

Arguably, excessive executive pay is even more widespread in the US. For example, the gap between the earnings of ordinary Americans and top executives has grown far wider in the past 25 years. A statistic commonly quoted by the labour group AFL- CIO shows that a chief executive made $42 for every dollar earned by one of his or her blue-collar workers in 1980. Today, chief executives were earning $531 for every dollar taken home by a typical worker.

Executive pay and remuneration committees

So who sits on the remuneration committee which decides the executive remuneration schemes? In the UK the Combined Code of corporate governance states that members should be drawn ‘exclusively’ from non-executives due to the potential for conflicts of interest. By and large, this is so. However, says PIRC, some 14% of FTSE 100 companies continue to include executives on their remuneration committees.

Lessons for corporate governance

Over the past decade or so a number of major ‘corporate scandals’ have brought issues of corporate governance and accountability to public prominence.

Corporate scandals

Corporate scandals, such as those at Enron, WorldCom and Global Crossing in the US, have become well known in the past few years. However, such problems are by no means confined to the US, as the case of the Italian dairy company, Parmalat, clearly indicates. In little more than a fortnight in December 2003, the Italian dairy conglomerate became engulfed in Europe’s biggest financial fraud as some ˆ10-13bn were found to have disappeared from its accounts. Deloitte, Parmalat’s chief auditor, did not do its own checks on some big bank accounts at one of the Italian dairy group’s subsidiaries that turned out to be fakes. As a result, in December 2003, a major scandal broke after the disclosure that Bonlat, a Parmalat subsidiary in the Cayman Islands, did not have accounts worth almost ˆ4bn (£2.8bn) at Bank of America (B of A). Eventually, this ‘lost’ money was found to be three times greater. Bonlat’s auditor was Grant Thornton and B of A told it in January 2004 that a document purportedly showing accounts with cash and securities worth ˆ3.95bn was fake. Deloitte, one of the big four global accounting firms, allegedly did not make independent checks on the authenticity of Bonlat’s supposed accounts with B of A, believing it was entitled to rely on Grant Thornton’s work on Bonlat, rather than do its own checks, and such an arrangement was permitted by Italian law and regulators. Even though the division of work between Deloitte, as chief auditor, and Grant Thornton, as auditor to Parmalat’s subsidiaries, was allegedly agreed with the company and notified to Consob, Italy’s chief financial regulator, the deficiencies in such regulation became only too apparent with the eventual collapse and prosecution of those involved.

These high-profile company collapses, together with shareholder concerns as to the often ‘excessive’ remuneration packages of company directors in poorly performing companies, have resulted in changes in the rules of corporate governance in recent years. These have involved changes in both internal and external practices, as for example in the companies’ dealings with auditors and accountants.

Higgs Committee: UK

In the UK the Higgs Committee in 2002 has sought to improve corporate governance in the wake of the bitter experiences for shareholders and investors from the collapse of a number of high-profile companies. The Higgs proposals include the following.

■ At least 50% of a company’s board should consist of independent non-executive directors.

■ Rigorous, formal and transparent procedures should be adopted when recruiting new directors to a board.

■ Roles of Chairman and Chief Executive of a company should be separate.

■ No individual should be appointed to a second chairmanship of a FTSE 100 company.

Sarbanes-Oxley Act: US

In the US the Sarbanes-Oxley Act in 2002 was introduced following major collapses of companies such as Enron, Worldcom and Global Crossing and was also directed at strengthening corporate governance.

■ If officers of a company are proved to have intentionally filed false accounts, they can be sent to jail for up to 20 years and fined $5m.

■ Executives will have to forfeit bonuses if their accounts have to be restated.

■ A ban on company loans to its directors and executives.

■ Protection for corporate whistleblowers.

■ Audit committees to be made up entirely of independent people.

■ Disclosure of all off-balance-sheet transactions.

Other suggestions for improving corporate governance have included the European Commission seeking to ensure that group auditors take responsibility for all aspects of companies’ accounts. It is therefore considering requiring each EU member state to set up US-style accounting oversight boards. The OECD has also drafted a revision of its principles on corporate governance, including calls for shareholders to be able to submit questions to auditors, who should be seen as accountable to shareholders and not to management, as seems too often to have been the case. The draft proposals also call on boards to protect whistleblowers.

Conclusion

CSR clearly involves a range of activities and approaches. Whilst CSR definitions vary, at least four characteristics tend to be included: a voluntary element, an inclusion of ‘externalities, reference to multiple stakeholders and reference to the organization’s core values/mission.

The case for CSR often refers to the organization’s need to manage risk and, in particular, to avoid reputational damage. The various stakeholders are all too aware of the adverse impacts of well-publicized environmental or ethical ‘lapses’ on dividends and the share price, via lost sales and/or paying expensive damages. More positively, such stakeholders are increasingly aware of the benefits from well-publicized proactive CSR initiatives! Being positively associated with ethical or environmental causes is increasingly recognized as important in capturing consumer loyalty, both of existing consumers (making the demand curve less price-elastic) and in attracting new consumers (shifting the demand curve to the right). The former causes the demand curve to pivot and become steeper, increasing options to raise price and revenue given the enhanced commitment of consumers to the organization’s product, irrespective of price charged. The latter causes an increase in demand, with more consumers now willing to purchase the product at any given price.

Of course, higher revenue is a key element in securing higher profit (revenue minus cost), giving greater scope for higher dividend payouts to shareholders and higher share price as market sentiment shifts in favour of these shares giving a higher profit. CSR can also be seen as conveying strategic benefits for organizations with ‘responsive’ and ‘strategic’ CSR identified by Porter and Kramer, the former being more reactive to events and the latter more proactive in terms of market positioning.

Critics of CSR, such as Friedman, point to the primacy of owner/shareholder interests and profit outcomes as of first importance. For businesses to spend money on CSR initiatives is seen by Freidman as a type of ‘tax’ on shareholders for activities more properly the domain of elected governments and their representatives. In any case, to Friedman it is inconceivable that a legal entity such as a business should have ‘responsibilities’, which in his view can only be assigned to individuals.

Environmental, as much as ethical, responsibilities are becoming more prominent in a world where ‘sustainability’ is a high-profile concept in all walks of life. Ethical theories can be categorized in a framework which is useful in emphasizing whether principle or outcome, individual or institutional responsibilities, are the key characteristics of a particular ethical approach.

The role of codes of conduct within organizations is reviewed, as are a number of legal requirements for corporate governance in various countries. We note that in response to various corporate scandals, a number of ‘requirements’, both formal and informal, are now expected of organizations as regards the arrangements which provide both authority and accountability. A particular area, executive remuneration, is reviewed in some detail and the absence of effective restraints on CEO and other senior executive remuneration is noted.

Key points

■ Corporate Social Responsibility (CSR) has at least four core characteristics: voluntary; recognizes externalities; considers multiple stakeholders; reflects organizational value/mission statements.

■ The stakeholder approach helps focus the ‘social’ in CSR on specific interest groups rather than the vague concept of ‘society’.

■ CSR has positive linkages with revenue, profit, share price and strategic direction.

■ CSR is criticized by some as a misuse of scarce resources resulting in a neglect of the ‘rightful’ interests of shareholders, namely profit.

■ The Friedman approach to CSR can be most readily located in the ‘Deontolog- ical ethics’ category, with an emphasis on ‘principles’ and institutions whilst the stakeholder perspective fits more clearly in the ‘Ethical learning and growth’ category, with an emphasis on outcomes (policies) and individuals or groups of individuals.

■ Codes of conduct are increasingly used within organizations to secure advantages such as limiting potential legal damages, reducing the need for legal regulations and establishing a positive organizational ‘brand’ image. Disadvantages include non-compulsion and a tendency to be ‘loose’ and lacking specificity.

■ Corporate governance, i.e. the formal and informal arrangements within an organization giving clarity to authority and accountability, is very much at the forefront of contemporary debate, as governments and organizations seek to avoid recent corporate scandals.

■ Executive remuneration remains an area where corporate governance approaches seem unable to curb widely viewed excesses.

■ The Higgs Committee recommendations in the UK and Sarbanes Oxley Act in the US are attempts to ‘tighten’ approaches to corporate governance in the respective countries.

Now try the self-check questions for this chapter on the Companion Website. You will also find useful links to relevant websites.

References and futher reading

Bentham, J. (1994) ‘The Commonplace Book’ in The Works of Jeremy Bentham,Vol. X, ed. Bowring, J., Bristol, Thoemnes Press. Original edition (1843), Edinburgh, Tait.

Berry, L., Mirabito, A. and Baun, W. (2010) What’s the hard return on employee wellness programmes? Harvard Business Review, December.

Boeger, N., Murray, R. and Villiers, C. (2008) Perspectives on Corporate Social Responsibility, Cheltenham, Edward Elgar.

Crane, A., Matten, D. and Spence, L. (2008) Corporate Social Responsibility: Readings and Cases in a Global Context, London, Routledge. Fisher, C. and Lovell, A. (2009) Business Ethics and Values: Individual, Corporate and International Perspectives (3rd edn), Harlow, Financial Times/Prentice Hall.

Freeman, E. (1984) Strategic Management: a Stakeholder Approach, Harlow, Pitman Friedman, M. (1970) The social responsibility of business is to increase its profits, The New York Times Magazine, 33(September): 122-6.

Heal, G. (2008) When Principles Pay: Corporate Social Responsibility and the Bottom Line, New York, Columbia University Press.

Horrigan, B. (2010) Corporate Social Responsibility in the 21st Century: Debates, Models and Practices Across Government, Law and Business, Cheltenham, Edward Elgar. McDonald, M. (2007) Marketing Plans: How to Prepare Them, How to Use Them (6th edn), Oxford, Butterworth-Heinemann.

Petrick, J. and Quinn, J. (2001) The challenge of leadership accountability for integrity capacity as a strategic asset, Journal of Business Ethics, 34(3-4): 331-43.

Porter, M. and Kramer, M. (2006) The link between competitive advantage and corporate social responsibility, Harvard Business Review, 84(12): 78-92.

Porter, M. and Kramer, M. (2011) Creating shared value, Harvard Business Review, January-February, 62-77.

Ramaswamy, V. and Gouillart, F. (2010) Building the co-creative enterprise, Harvard Business Review, October.

Teece, D., Pisano, G. and Shuen, A. (1997), Dynamic capabilities and strategic management, Strategic Management Journal, 18(7): 509-33.

Thomas, R. (2009) International Executive Pay: Current Practices and Future Trends, Vanderbilt Law Economic Research

Paper No. 08-26, Nashville TN, Vanderbilt University.

Watson Wyatt Worldwide (2009) Executive pay practices around the world. London: Watson Wyatt.

World Commission on Environment and Development (WCED) (1987) Our Common Future, New York, Oxford University Press. Wolf, M. (2000) Sleepwalking with the enemy: CSR distorts the market by deflecting business from its primary role of profit generation, Financial Times, May 16.