Firm objectives and firm behaviour

Economists have put forward various theories as to how firms behave in order to predict their reaction to events. At the heart of such theories is an assumption about firm objectives, the most usual being that the firm seeks to maximize profits.

The first part of the chapter examines a number of alternative objectives open to the firm. It begins with those of a maximizing type, namely profit, sales revenue and growth maximization, predicting firm price and output in each case. A number of nonmaximizing or behavioural objectives are then considered. The second part of the chapter reviews recent research into actual firm performance, and attempts to establish which objectives are most consistent with how firms actually operate. We see that although profit is important, careful consideration must be given to a number of other objectives if we are accurately to predict firm performance. The need for a perspective broader than profit is reinforced when we consider current management practice in devising the corporate plan.Chapter 15 (Corporate social and ethical responsibility) also reviews related aspects of firm objectives and firm behaviour.

I Firm objectives

The objectives of a firm can be grouped under two main headings: maximizing goals and non-maximizing goals. We shall see that marginal analysis is particularly important for maximizing goals. This is often confusing to the student who, rightly, assumes that few firms can have any detailed knowledge of marginal revenue or marginal cost. However, it should be remembered that marginal analysis does not pretend to describe how firms maximize profits or revenue. It simply tells us what the output and price must be if they do succeed in maximizing these items, whether by luck or by judgement.

Maximizing goals

Profit maximization

The profit-maximizing assumption is based on two premises: first, that owners are in control of the day- to-day management of the firm; second, that the main desire of owners is for higher profit.

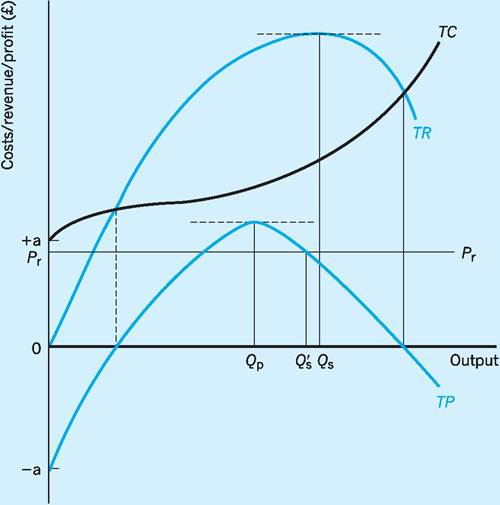

The case for profit maximization as ‘self-evident’ is, as we shall see, undermined if either of these premises fails to hold.Profit is maximized where marginal revenue (MR) equals marginal cost (MC), i.e. where the revenue raised from selling an extra unit is equal to the cost of producing that extra unit. In Fig. 3.1 total profit (TP) is a maximum at output Qp, where the vertical distance between total revenue (TR) and total cost (TC) is the greatest (TP = TR — TC). Had the marginal revenue and marginal cost curves been presented in Fig. 3.1, they would have intersected at output Qp.

To assume that it is the owners who control the firm neglects the fact that the dominant form of industrial organization is the public limited company (plc), which is usually run by managers rather than by owners. This may lead to conflict between the owners (shareholders) and the managers whenever the managers pursue goals which differ from those of the owners. This conflict is referred to as a type of principal-agent problem and emerges when the shareholders (principals) contract a second party, the managers (agents), to perform some tasks on their behalf. In return, the principals offer their agents some compensation (wage payments). However, because the principals are divorced from the day-to- day running of the business, the agents may be able to act as they themselves see fit. This independence of action may be due to their superior knowledge of the company as well as their ability to disguise their actions from the principals. Agents, therefore, may not always act in the manner desired by the principals. Indeed, it may be the agents’ goals which predominate. This has led to a number of managerial theories of firm behaviour, such as sales revenue maximization and growth maximization.

Fig. 3.1 Variation of output with firm objective.

Sales revenue maximization

Baumol (1959) has suggested that the manager- controlled firm is likely to have sales revenue maximization as its main goal rather than the profit maximization favoured by shareholders.

His argument is that the salaries of top managers, and other perks, are more closely correlated with sales revenue than with profits.Williamson’s (1963) managerial theory of the firm is similar to Baumol’s in stressing the growth of sales revenue as a major firm objective. However, it is broader based, with the manager seeking to increase satisfaction through the greater expenditure on both staff levels and projects made possible by higher sales revenue. Funds for greater expenditure can come from profits, external finance and sales revenue. In Williamson’s view, however, increased sales revenue is the easiest means of providing additional funds, since higher profits have in part to be distributed to shareholders, and new finance requires greater accountability. Baumol and Williamson are describing the same phenomenon, though in rather different terms.

If management seeks to maximize sales revenue without any thought to profit at all (pure sales revenue maximization) then this would lead to output Qs in Fig. 3.1. This last (Qsth) unit is neither raising nor lowering total revenue, i.e. its marginal revenue is zero.

Constrained sales revenue maximization

Both Baumol and Williamson recognize that some constraint on managers can be exercised by shareholders. Maximum sales revenue is usually considered to occur well above the level of output which generates maximum profits. The shareholders may demand at least a certain level of distributed profit, so that sales revenue can only be maximized subject to this constraint.

The difference a profit constraint makes to firm output is shown in Fig. 3.1. If Pr is the minimum profit required by shareholders, then Q's is the output which permits the highest total revenue whilst still meeting the profit constraint. Any output beyond Q's up to Qs would raise total revenue TR - the major objective - but reduce total profit TP below the minimum required (Pr).

Therefore Q's represents the constrained sales revenue maximizing output.So far we have assumed that the goals of owners (profits) have been in conflict with the goals of management (sales revenue). Marris (1964), however, believes that owners and managers have a common goal, namely maximum growth of the firm.

Growth maximization

Marris (1964) argues that the overriding goal which both managers and owners have in common is growth. Managers seek a growth in demand for the firm’s products or services, to raise power or status. Owners seek a growth in the capital value of the firm to increase personal wealth.

It is important to note, therefore, that it is through the growth of the firm that the goals of both managers and owners can be achieved. Also central to the analysis of Marris is the ratio of retained to distributed profits, i.e. the ‘retention ratio’. If managers distribute most of the profits (low retention ratio), shareholders will be content and the share price will be sufficiently high to deter takeover. However, if managers distribute less profit (high retention ratio), then the retained profit can be used for investment, stimulating the growth of the firm. In this case shareholders may be less content, and the share price lower, thereby increasing the risk of a takeover bid.

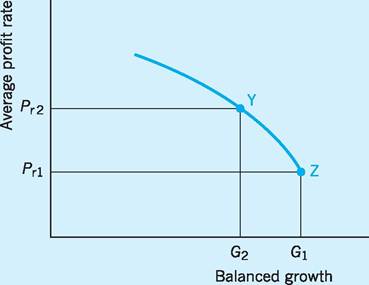

The major objective of the firm, with which both managers and shareholders are in accord, is then seen by Marris as maximizing the rate of growth of the firm’s demand and the firm’s capital (‘balanced growth’), subject to an acceptable retention ratio. Figure 3.2 shows the trade-off between higher balanced growth and the average profit rate.1

For ‘balanced growth’ to increase, more and more investment in capital projects must be undertaken.

Fig. 3.2 Trade-off between average profit and balanced growth.

Since the most profitable projects are undertaken first, any extra investment must be reducing the average profit rate.

Point Z is where the balanced growth rate is at a maximum (G1), with an implied retention ratio so high that all profitable investment projects have been pursued, giving an average profit rate Pr1. Risk avoidance by managers may, however, enforce a lower retention ratio with more profits distributed. Point Y is such a constrained growth-maximizing position (G2), with a lower retention ratio, lower investment and higher average profit (Pr2) than at point Z. How close the firm gets to its major objective, Z, will depend on how constrained management feels by the risk of disgruntled shareholders, or a takeover bid, should the retention ratio be kept at the high rates consistent with points near to Z.Non-maximizing goals

The traditional (owner control) and managerial (nonowner control) theories of the firm assume that a single goal will be pursued. The firm then attempts to achieve the highest value for that goal, whether profits, sales revenue or growth. The behaviouralist viewpoint is rather different, and sees the firm as an organization with various groups, workers, managers, shareholders, customers, etc., each of which has its own goal, or set of goals. The group which achieves prominence at any point of time may be able to guide the firm into promoting its goal set over time. This dominant group may then be replaced by another giving greater emphasis to a totally different goal set. The traditional and managerial theories which propose the maximization of a single goal are seen by behaviouralists as being remote from the organizational complexity of modern firms.

Satisficing

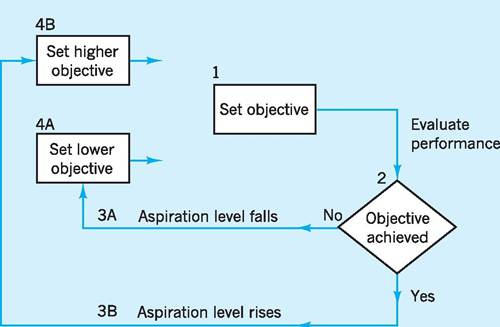

One of the earliest behavioural theories was that of Simon (1959) who suggested that in practice managers are unable to ascertain when a marginal point has been reached, such as maximum profit with marginal cost equal to marginal revenue. Consequently, managers set themselves minimum acceptable levels of achievement. Firms which are satisfied in achieving such limited objectives are said to ‘satisfice’ rather than ‘maximize’.

This is not to say that satisficing leads to some long-term performance which is less than would otherwise be achieved. The achievement of objectives has long been recognized as an incentive to improving performance and is the basis of the management technique known as management by objectives (MBO). Figure 3.3 illustrates how the attainment of initially limited objectives might lead to an improved long-term performance.At the starting point 1, the manager sets the objective and attempts to achieve it. If, after evaluation, it is found that the objective has been achieved, then this will lead to an increase in aspirational level (3B). A new and higher objective (4B) will then emerge. Thus, by setting achievable objectives, what might be an initial minimum target turns out to be a prelude to a series of higher targets, perhaps culminating in the achievement of some maximum target, or objective. If, on the other hand, the initial objective is not achieved, then aspirational levels are lowered (3A) until achievable objectives are set. Simon’s theory is one in which no single objective can be presumed to be the inevitable outcome of this organizational process. In fact, the final objective may, as we have seen, be far removed from the initial one.

Coalitions and goal formation

If a firm is ‘satisficing’, then who is being satisficed - and how? Cyert and March (1963) were rather more specific than Simon in identifying various groups or coalitions within an organization. A coalition is any group which, at a given moment, shares a consensus on the goals to be pursued.

Fig. 3.3 Development of aspiration levels through goal achievement.

Workers may form one coalition wanting good wages and work conditions and some job security; managers want power and prestige as well as high salaries; shareholders want high profits. These differing goals may well result in group conflict, e.g. higher wages for workers may mean lower profits for shareholders. The behavioural theory of Cyert and March, along with Simon, does not then view the firm as having one outstanding objective (e.g. profit maximization), but rather many, often conflicting, objectives.

It is not just internal groups which need to be satisfied. There is an increasing focus by leading organizations on stakeholders, i.e. the range of both internal and external groups which relate to that organization. Freeman (1984) defined stakeholders as ‘Any group or individual who can affect or is affected by the achievement of the organization’s objectives’. Cyert and March suggest that the aim of top management is to set goals which resolve conflict between opposing groups.

Contingency theory

The contingency theory of company behaviour suggests that the optimal solutions to organizational problems are derived from matching the internal structure and processes of the firm with its external environment. However, the external environment is constantly changing as industrial markets become more complex, so that the optimum strategy for a firm will change as the prevailing environmental influences change. The result of this is that firms may not have a single goal such as the maximization of profits or sales, but will have to vary their goals and strategies as the environment changes around them. Contingency theory helps us to understand why firms will not always be able to follow a single optimizing course through time.

To summarize, the various behavioural theories look at the process of decision-making. They recognize that the ‘organization’ is not synonymous with the owner, nor with any other single influence, but rather that the firm has many objectives which relate to the many different groups acting within the organization. These objectives may be in conflict and so management will use a number of techniques in order to reduce that conflict. The behavioural approach has been criticized for its inability to yield precise predictions of firm activity in particular settings. However, where management processes are recognized, such as in strategic planning (see p. 55), then specific shortterm predictions can be made.

Does firm objective matter?

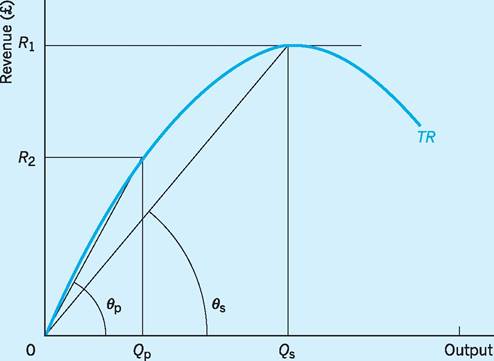

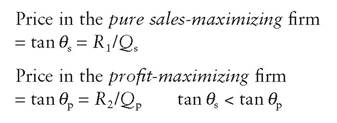

The economist is continually seeking to predict the output and price behaviour of the firm. Figure 3.1 indicates that firm output does indeed depend upon firm objective, with the profit-maximizing firm having a lower output than the sales-maximizing firm (pure and constrained). If we remember that price is

Fig. 3.4 Variation of price with firm objective.

average revenue (i.e. total revenue/total output) we can see from Fig. 3.4 that firm price will also vary with firm objective.

i.e. the price of the pure sales-maximizing firm is below that of the profit-maximizing firm.

It is clear that it really does matter what objective we assume for the firm, since both output and price depend on that objective. We turn now to firm performance to assess which of the objectives, if any, can be supported by how firms actually behave.

Firm behaviour

Ownership and control in practice

Profit maximization is usually based on the assumption that firms are owner-controlled, whereas sales and growth maximization usually assume that there is a separation between ownership and control. The acceptance of these alternative theories was helped by early research into the ownership of firms. Studies in the US by Berle and Means (1934), and by Larner in the 1960s, suggested that a substantial proportion of large firms (44% by Berle and Means and 85% by Larner) were manager-controlled rather than owner- controlled. Later research has, however, challenged the definition of ‘owner-control’ used in these early studies. Whereas Berle and Means assumed that owner-control is only present with a shareholding of more than 20% in a public limited company, Nyman and Silberston (1978) used a much lower figure of 5% after research had indicated that effective control could be exercised by owners with this level of shareholding. This would suggest that owner-control is far more extensive than previously thought. Leech and Leahy (1991) found that 91% of British public limited companies are owner-controlled using the 5% threshold figure, but only 34% are owner-controlled using a 20% threshold figure. Clearly the degree of ownership control is somewhat subjective, depending crucially on the threshold figure assigned to shareholding by owners in order to exercise effective control.

A further aspect of owner-control involves the role of financial institutions and pension funds. In 2006 they owned 43% of the capital of public companies in the UK (£796 billion of the total value of £1858b). Foreign investors owned a further 41% while individual share ownership has declined from 54% in the mid-1960s to 13% in 2006 (UK Shareholders Association 2007). Financial institutions are more likely than individuals to bring influence to bear on chief executives, being experienced in the channels of communication and sensitive to indices of firm performance. The effect of this influence is seen by many as moving the firm towards the profit-maximizing (owner-controlled) type of objective.

Profit

Profit maximization

In a major study, Shipley (1981) concluded that only 15.9% of his sample of 728 UK firms could be regarded as ‘true’ profit-maximizers. This conclusion was reached by cross-tabulating replies to two questions shown in Table 3.1.

Because answers to questionnaires can often be given loosely, Shipley considered as ‘true’ maximizers only those who claimed both to maximize profit (answered (a) to Question 1) and to regard profit as being of overriding importance (answered (d) to Question 2). Only 15.9% of all the firms replied with both 1(a) and 2(d), and were considered by Shipley as true profit-maximizers.

A similar study by Jobber and Hooley (1987) found that 40% of their sample of nearly 1,800 firms had profit maximization as their prime objective. In a study of 77 Scottish companies by Hornby (1994), 25% responded as ‘profit maximizers’ to the ‘Shipley test’. The percentage of satisficers was very similar in both studies (Shipley 52.3%, Hornby 51.9%).

Given the significance of the profit-maximizing assumption in economic analysis, these results may seem surprising. However, some consideration of the decision-making process may serve to explain these low figures for profit maximization. Firms in practice often rely on preset ‘hurdle’ rates of return for projects, with managers given some minimum rate of return as a criterion for project appraisal. As a result they may not consciously see themselves as profitmaximizers, since this phrase suggests marginal analysis. Yet in setting the hurdle rates, top management will be keenly aware of the marginal cost of funding, so that this approach may in some cases relate closely to profit maximization. In other words, the response of management to questionnaires may understate the true significance of the pursuit of profit.

Evidence from a recent study of ‘not for profit’ companies in the healthcare sector in the USA found that 79% of them displayed ‘for profit’ decisions that maximized the profit function rather than the utility function, i.e. the majority did not spend as much as they could have done to provide a higher level of resident care (Vitaliano 2003).

Profit as part of a ‘goal set'

Although few firms appear to set out specifically to maximize profit, profit is still seen (even in response to questionnaires) as an important factor in decisionmaking. In the Shipley study the firms were asked to list their principal goal in setting price. Target profit was easily the most frequently cited, with 73% of all firms regarding it as their principal goal. Even more firms (88%) included profit as at least part of their ‘goal set’.

Table 3.1 Sample of 728 firms.

All respondents (%)

| (1) | Does your firm try to achieve: (a) maximum profits? 47.7 (b) ‘satisfactory’ profits? 52.3 |

| (2) | Compared to your firm’s other leading objectives, is the achievement of a target profit... regarded as being: (a) of little importance? 2.1 (b) fairly important? 12.9 (c) very important? 58.9 (d) of overriding importance? 26.1 |

Those responding with both 1(a) and 2(d) 15.9

Source: Adapted from Shipley (1981).

Profit - long-term versus short-term

Long-term profit may be even more important than short-term profit in firm objectives. Senior managers are well aware that poor profitability in the long term may lead to their dismissal or the takeover of their firm, quite apart from an increased risk of insolvency. Indeed Shipley found that 59.7% of his sample gave priority to long-term profits, compared to only 20.6% giving priority to short-term profits. Shipley found long-term profit to be a significant influence in all sizes of company, though particularly in those of medium/large size. However, as international financial investors dominate the ownership of public companies, who can and do shift their investments to gain short-term profits, the narrative of short-term versus long-term continues to be played out in the financial world. It is not unusual to find the leader of a corporation or the head of a policy institute complaining of the short-term orientation of investors, and the damage that can cause to the sustainability of their organizations (e.g. Financial Times 2010).

Studies of the behaviour of firms in technologybased markets have provided further support for the emphasis on longer-term profit perspectives (Arthur 1996). Arthur suggests that when a technology reaches a certain critical mass of usage, then the market is ‘locked in’ and the only rational choice for new users is then to adopt the established technology. He cites Microsoft Windows as being a typical example of this, with the continued increase in use of Windows providing an example of a market system operating positive feedback. Arthur suggests that average (and marginal) revenues might even rise in technologybased markets as volume exceeds the ‘critical mass’ for that established technology, rather than decline as in standard theory. This phenomenon has often led to a strategy of giving away products reflecting new technologies at their introduction stage in order to create lock-in. The objective of this strategy for technology-based markets might arguably still be profit maximization, but only in the longer term.

Profit and reward structures

There has been a great deal of concern throughout the 1990s and in the first decade of the millennium that managers in large firms have paid too little regard to the interests of shareholders, especially as regards profit performance of the company. Indeed a number of celebrated cases in the press have focused on the apparent lack of any link between substantial rises in the pay and bonuses of chief executives and any improvements in company performances (see also Chapter 15, p. 314).

The majority of empirical studies have indeed found little relationship between the remuneration of top managers and the profit performance of their companies. In the UK, Storey et al. (1995) found no evidence of a link between the pay of top managers and the ratio of average pre-tax profits to total assets, with similar results for studies by Jensen and Murphy (1990) and Barkema and Gomez-Meija (1998) in the US. Table 3.2 confirms this picture, with not one of the 20 firms appearing in the 10 highest sales revenue and 10 highest profit rankings being in the list of the 10 highest paid Chief Executive Officers (CEOs). This apparent lack of a clear relationship between executive pay and company performance became an important issue during 2007-10 as the CEOs of various high-profile financial intermediaries and companies received large pay rises and special cash deals at the same time as company profits and share prices fell. Despite the economic recession, the chief executives of the FT100 companies have also benefited from average increases in the pay element of their remuneration packages by as much as 20%, while average pay settlements across all employees in UK firms only rose by 1.3% (Financial Times 2010).

However, the absence of any proven link between the profitability of a firm and the reward structures it offers to its CEO and other top managers does not necessarily mean that profit-related goals are unimportant. Firms increasingly offer top managers a total remuneration ‘package’ involving bonus payments and share options as well as salary. In this case higher firm profitability, and therefore dividend earnings per share, may help raise the share price and with it the value of the total remuneration package. Indeed Ezzamel and Watson (1998) have suggested that the total remuneration package offered to CEOs is directly related to the ‘going rate’ for corporate profitability. It may therefore be that top management have more incentives for seeking profit-related goals than might at first be apparent.

To summarize, therefore, although there may be no open admission to profit maximization, the strong

Table 3.2 The ten highest-ranked US corporations by sales revenue growth, profit growth and CEO remuneration 2010.

| Rank | Sales revenue maximizers1 | Profit maximizers2 | Highest paid CEOs3 |

| 1 | International Asset Holding | First Solar | Danaher |

| 2 | SXC Health Solutions | Sapient | Oracle |

| 3 | First Solar | International Asset Holdings | Chesapeake Energy |

| 4 | Olin | Fuel Systems Solutions | Occidental Petroleum |

| 5 | KapStone Paper and Packaging | Bucyrus International | Yum Brands |

| 6 | Sun Power | Sturm Ruger & Co | Gilead sciences |

| 7 | Life Partners Holdings | Salesforce.com | Celgene |

| 8 | Green Mountain Coffee Roasters | Thoratec | XTO Energy |

| 9 | Bucyrus International | Life Partners Holdings | Freeport Copper |

| 10 | Ebix | Kapstone Paper and Packaging | bgcolor=white>Nividia

1Revenue growth (latest 3 year annual average growth of revenue).

2Profit growth (latest 3 year annual average growth of earnings per share (EPS)).

3Remuneration includes salary, bonuses and stocks.

Sources: Adapted from Fortune (2010) 100 Fastest Growing Companies, 6 September; DeCarlo (2010a) Special Report: CEO Compensation, 28 April, Forbes.com; DeCarlo (2010b) Special Report: Global High Performers, 21 April, Forbes.com.

influence of owners on managed firms, the use of preset hurdle rates and the presence of profit- related reward structures may in the end lead to an objective, or set of objectives, closely akin to profit maximization.

Sales revenue

Sales revenue maximization

Baumol’s suggestion that management-controlled firms will wish to maximize sales revenue was based on the belief that the earnings of executives are more closely related to firm revenue than to firm profit. A number of studies have sought to test this belief. For example, in a study of 177 firms between 1985 and 1990, Conyon and Gregg (1994) found that the pay of top executives in large companies in the UK was most strongly related to relative sales growth (i.e. relative to competitors). They also found that it was only weakly related to a long-term performance measure (total shareholder returns) and not at all to current accounting profit. Furthermore, growth in sales resulting from takeovers was more highly rewarded than internal growth, despite the fact that such takeovers produced on average a lower return for shareholders and an increased liquidity risk. These findings are in line with other UK research (Gregg et al. 1993; Conyon and Leech 1994) and with a study of small UK companies by Conyon and Nicolitsas (1998) which also found sales growth to be closely correlated with the pay of top executives.

As well as a linkage between the growth of sales revenue and executive income, there is also general support for the contention that firm size is directly related to executive income. Studies by Gregg et al. (1993) and Rosen (1990) concur with much earlier studies, such as that of Meeks and Whittington (1975), who found that the larger the asset value of the company, the larger the executive salary.

What does seem clear from these various findings is that top management appears to be able to revise the rules for their own remuneration according to circumstance. Principals (shareholders) would appear to have little effective control over the remuneration of agents (management) in major public corporations where ownership and control are separated. This lack of control has led to a rise in shareholder activism, where investors intervene in the decisions of the Board, either through direct threat of disinvestment, or voting against executive remuneration, forcing or preventing mergers, or imposing corporate responsibility policies at Annual General Meetings or Extraordinary General Meetings.

Sales revenue as part of a ‘goal set'

The results of Shipley’s analysis tell us little about sales revenue maximization. Nevertheless, Shipley found that target sales revenue was the fourth-ranked principal pricing objective, and that nearly half the firms included sales revenue as at least part of their set of objectives. Larger companies cited sales revenue as an objective most frequently; one-seventh of companies with over 3,000 employees gave sales revenue as a principal goal compared to only one-fourteenth of all the firms. Since larger companies have greater separation between ownership and management control, this does lend some support to Baumol’s assertion. The importance of sales revenue as part of a set of policy objectives was reinforced by the study of 193 UK industrial distributors by Shipley and Bourdon (1990), which found that 88% of these companies included sales revenue as one of a number of objectives. However, we see below that the nature of planning in large organizations must also be considered and that this may temper our support for sales revenue being itself the major objective, at least in the long term.

Strategic planning and sales revenue

Current thinking on strategic planning would support the idea of short-term sales maximization, but only as a means to other ends (e.g. profitability or growth). Research in the mid-1970s by the US Strategic Planning Institute linked market share - seen here as a proxy for sales revenue - to profitability. These studies found that high market share had a significant and beneficial effect on both return on investment and cashflow, at least in the long term. However, in the short term the high investment and marketing expenditure needed to attain high market share reduces profitability and drains cashflow. Profit has to be sacrificed in the short term if high market share, and hence future high profits, are to be achieved in the long term. A recent meta-study (Armstrong and Green 2007) suggests that a deliberate strategy of buying market share through high advertising and reduced prices (for example) is detrimental to the profits of the business.

Constrained sales revenue maximization

The fact that 88% of all companies in Shipley’s original study included profit in their goal set indicates the relevance of the profit constraint to other objectives, including sales revenue. The later study by Shipley and Bourdon (1990) reached a similar conclusion, finding that 93% of the UK industrial distributors surveyed included profit in their goal set.

Growth

There are a number of reasons why firms should wish to grow, although in the 1990s the term ‘growth’ would appear to apply to asset value and market share rather than workforce. Marris (1964) suggests that managers seek to increase their status by increasing the ‘empire’ in which they work. Others would argue that although growth is an important company objective it is a means to an end, e.g. higher profit, rather than an end in itself as Marris would suggest.

When we examine the facts, however, there is little to indicate that faster growth really does mean higher profits. An analysis in 2007 of the top 10 highest- growth firms (percentage change in total assets) amongst the leading 100 UK plcs found that, ranked in terms of profitability (percentage profit margin), only Rio Tinto was ranked as both fast growing and highly profitable, i.e. being in the top 10 plcs on both measures. Indeed, the other nine high-growth plcs are low in the profitability rankings, with BP third in growth but only 53rd in profitability. This finding is in line with the results of a study by Whittington (1980) who found that profit levels did not increase as the firm grew in size. This lends some support to those, like Marris, who see growth as a separate objective to profit.

In fast-moving markets, such as high-technology electronics and pharmaceuticals, companies need flexibility to move rapidly to fill market niches. To achieve this, some firms are moving in quite the opposite direction to growth, i.e. they are ‘de-merging’. De-merging occurs when the firm splits into smaller units, each separately quoted on the Stock Exchange. For example, in 2010 Carphone Warehouse demerged its Talk Talk Telecoms (fixed line and broadband) subsidiary, Fiat de-merged its cars and engines from Iveco Trucks and Fosters de-merged its wine business from its beer business. Such de-merging is a clear sign that professional investors do not merely equate larger size to greater profit.

In a similar vein, Tom Peters, co-author of In Search of Excellence, says that ‘quality and flexibility

will be the hallmarks of the successful economy for the foreseeable future’. This premise leads to a view that size, with its inherent inflexibility and distance from the end-customer, is a disadvantage. Indeed, analysis by the Strategic Planning Institute (Buzzel and Gale 1987) shows an inverse relationship between market size and the rate of return on investment in the US. In market segments of less than $100m (£61m), the return on investment averaged 27% in their study; however, where firms operated in market segments of over $1bn (£610m), the return averaged only 11%. They found that organizations sought to reduce the disadvantages of size by restructuring, either by de-merging or by the creation of smaller, more dynamic Strategic Business Units (SBUs), which are able to meet the demands of the market more rapidly.

Despite the comments made above, a company which fails to grow over a period of time, even though its profits are relatively healthy, is in danger of becoming an ineffective innovator. Growth is important because it attracts good, young entrepreneurial talent, as dynamic firms such as Nokia, Goldman Sachs and L’Oreal have found. It also helps companies to attract new capital and to be innovative as regards new products and processes. The dynamics of the growth process depend on the interaction between a firm’s external environment (industry, markets and customers) and the internal environment of the company (resources and abilities). Table 3.3 shows four corporate growth paths with examples of companies which seem to have taken these paths.

Basically speaking, corporate renewal is a determinant of growth when companies use their current resources and abilities to expand their customer base. For example, Swatch succeeded in becoming dynamic once more as a result of greater attention to costs, product design and differentiation. Innovation is

Table 3.3 Patterns of corporate growth.

Exploiting

| Corporate renewal | Innovation | Expanding capabilities | external opportunities |

| Swatch | Nokia | Glaxo | Merck |

| L’Oreal | Hewlett-Packard | Volkswagen | Bertelsmann |

| Disney | Canon | BP | Merrill Lynch |

| Lloyds | Goldman Sachs | Compaq | Wal-Mart |

an important determinant of growth, as companies like Nokia can attest. The company moved from one which operated across different industries to one which increasingly concentrated on communication systems. It focused more clearly on cellular phones by increasing investment in R&D and increasing its manufacturing capabilities. Some companies grow by expanding their capabilities through merger, as was the case with Glaxo and Wellcome. The synergy of two pharmaceutical companies (which had strong R&D capabilities and complementary areas of expertise) meant that the new company, Glaxo Wellcome, could produce an array of new products. Finally, exploiting external opportunities involves companies utilizing the benefits of growth in order to exploit external opportunities, such as new markets. For example, in the 1990s, Merck, the giant US pharmaceutical company, acquired Medco, a firm that ran a network of 48,000 pharmacies in the US. Through Medco’s direct sales links, Merck was able to control distribution and sell its goods direct to patients.

As we can see from the above examples, growth is still an important strategic variable because it acts as a catalyst to firms that want to become leaders in their respective fields. Firms that stand still often die, so that corporate growth provides the way for firms to ensure their long-term survival.

Non-maximizing behaviour

We have seen that the non-maximizing or behavioural theories concentrate on how firms actually operate within the constraints imposed by organizational structure and firm environment. Recent evidence on management practice broadly supports the behavioural contention, namely that it is unhelpful to seek a single firm objective as a guide to actual firm behaviour. This support, however, comes from a rather different type of analysis, that of portfolio planning.

Work in the US by the Boston Consulting Group on the relationship between market share and industry growth gave rise to an approach to corporate planning known as ‘portfolio planning’. Firms, especially the larger ones, can be viewed as having a collection or ‘portfolio’ of different products at different stages in the product life cycle. If a product is at an early stage in its life cycle, it will require a large investment in marketing and product development in order to achieve future levels of high profitability. At the same time another product may have ‘matured’ and, already possessing a good share of the market, be providing high profits and substantial cashflow.

The usual strategy in portfolio planning is to attempt to balance the portfolio so that existing profitable products are providing the funds necessary to raise new products to maturity. This approach has become a classic part of strategic decision-making.

If a firm is using the portfolio approach in its planning then it may be impossible to predict the firm’s behaviour for individual products or market sections on the basis of a single firm objective. This is because the goals of the firm will change for a given product or market sector depending on the relative position of that product or market sector within the overall portfolio. Portfolio planning, along with other behavioural theories, suggests that no single objective is likely to be useful in explaining actual firm behaviour, at least in specific cases.

The non-maximizing behaviour of large companies can be seen clearly in the approach taken by some large companies (Griffiths 2000). For example, between 1997 and 2000 Cadbury Schweppes, the chocolate and confectionery multinational, explained its objectives in terms of ‘Managing for Value’ (MFV). To meet the MFV criterion the company stressed the importance of:

■ increasing earnings per share by at least 10% every year;

■ generating £150m of free cashflow every year;

■ doubling the value of shareholders’ investment in the next four years;

■ competing in the world’s growth markets by effective internal investment and by value-enhancing acquisitions;

■ developing market share by introducing innovations in product development, packaging and routes to market;

■ increasing commitment to value creation in managers and employees through incentive schemes and share ownership;

■ investing in key areas of air emissions, water, energy and solid waste.

From the above list it is clear that the first three preoccupations are related to the profit objectives while the third and fourth relate to company growth and market share. In addition the final two objectives encompass both human resource and environmental issues.

A multiple and longer-term perspective is also evident in the response of some companies to the 2008-10 recession. For many firms a skilled workforce (talent) is a fundamental resource which is not easy to replace. So when salary costs had to be cut to survive, firms found innovative ways to do this, such as offering pay cuts and sabbaticals, with guaranteed re-employment, rather than making people redundant. Such a move is neither profit maximizing nor growth maximizing in the short term; the motive is survival.

In this context, it can be seen that maximizing a single corporate goal seems unrealistic in the dynamic world of multinationals.

Firm behaviour, firm objective and market structure

Whatever the firm objective, price-setting behaviour will vary with market structure (see also Chapter 6). We initially assume a profit-maximizing objective and note that price-setting behaviour will vary depending on the type of market structure.

Price and market structure

Given a profit-maximizing objective the price charged may still vary depending on the type of market structure within which the firm operates. This is well illustrated by a comparison between the extreme market forms of perfect competition and pure monopoly.

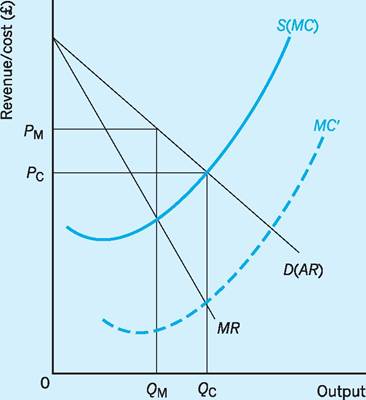

Perfect competition versus pure monopoly

Under perfect competition, price is determined for the industry (and for the firm) by the intersection of demand and supply, at Pc in Fig. 3.5. As the reader familiar with the theory of the firm will know, the supply curve, S, of the perfectly competitive industry is also the marginal cost (MC) curve of the industry. Suppose now that the industry is taken over by a single firm (‘pure monopoly’), and that costs are initially unchanged. It follows that the marginal cost curve remains in the same position; also that the demand curve for the perfectly competitive industry becomes the demand (and average revenue (AR)) curve for the monopolist. The marginal revenue (MR)

Fig. 3.5 Price under perfect competition and monopoly.

curve must then lie inside the negatively sloped AR curve. The profit-maximizing price for the monopolist is Pm, corresponding to output Qm where MC = MR. Price is higher under monopoly than under perfect competition (and quantity, Qm, is lower). This is the so-called ‘classical’ case against monopoly.

Our intention here is merely to point out that price will tend to differ for profit-maximizing firms depending on the type of market within which they operate. In our comparison of extreme market forms, the final outcome for price may or may not be higher under monopoly than under competition. It is in part an empirical question. If economies of scale were sufficient to lower the MC curve below MC' in Fig. 3.5, then the monopoly price would be below that of perfect competition. Price will, however, except by coincidence, be different under these two market forms, as it would under other market forms, such as monopolistic competition or oligopoly.

Price and firm objective

So far we have assumed that the firm with a single objective, i.e. profit maximization, will charge different prices in different types of market structure. If there are other objectives then there will tend to be a still wider range of possibilities for price. We saw in Fig. 3.4 (p. 51) that a sales-maximizing objective would usually lead to a lower price than would a profit-maximizing objective. The situation becomes even more complicated when we examine behavioural or non-maximizing objectives, as these yield not a unique price, but a range of price outcomes for any given market structure. Clearly firm price depends also on firm objective.

Price, market structure and firm objective

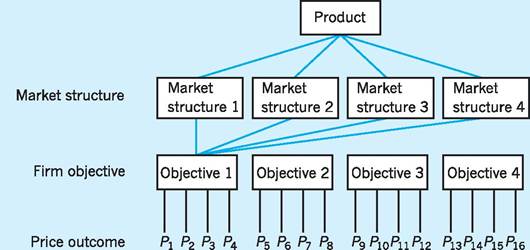

Price thus depends on both market structure and firm objective. Since there are many possible combinations of these, any given product or service can experience a wide array of possible prices.

From Fig. 3.6 we see that the four market structures can lead to at least four different price outcomes (P1-P4) for objective 1. A further four prices (P5-P8) might result from objective 2, and so on, giving at least 16 prices2 for the four market structures and the four firm objectives. To derive guidelines for pricesetting from theory, which will have general validity, is clearly a daunting if not impossible task.

Fig. 3.6 Market structure, firm objective and price.

Conclusion

The traditional theory of the firm assumes that its sole objective is to maximize profit. The managerial theories assume that where ownership and control of the organization are separated, the objective which guides the firm will be that which the management sets. This is usually thought to be maximization of either sales revenue or growth. It is important to know which, if any, of the maximizing objectives are being pursued, since firm output and price will be different for each objective. Behavioural theory tends to oppose the idea of the firm seeking to maximize any objective. For instance, top management may seek to hold the various stakeholder groups in balance by adopting a set of minimum targets. Even where a single group with a clear objective does become dominant within the firm, others with alternative objectives may soon replace it.

In practice, profit maximization in the long term still appears to be important. Sales revenue seems quite important as a short-term goal, though even here a profit target may still be part of the goal set. The prominence of the profit target may be an indication that ownership is not as divorced from the control of large firms as may once have been thought. One reason why sales revenue may be pursued in the short term is found in an analysis of current strategic planning techniques, which link short-term sales revenue to long-term profit. Sales revenue may therefore be useful for explaining short-term firm behaviour, but with profit crucial for long-term behaviour. Those who, like Marris, argue that growth is a separate objective from profit find some support in the lack of any clear relationship between growth and profitability. Growth may also be a means of securing greater stability for the firm. It may reduce internal conflict, by being an objective around which both owner-shareholders and managers can agree, and possibly reduces the risk of takeover. Also large firms experience, if not higher profits, then less variable profits (Whittington 1980; Schmalensee 1989). A widely used technique in the management of larger firms, portfolio planning, would seem to support the behaviouralist view, that no single objective will usefully help predict firm behaviour in a given market.

Key points

■ Separation between ownership by shareholders (principals) and control by managers (agents) makes profit maximization less likely.

■ Maximization of sales revenue or asset growth (as well as profit) must be considered in manager-led firms.

■ The objectives pursued by the firm will influence the firm’s price and output decisions.

■ Different groupings (coalitions) may be dominant within a firm at different points of time. Firm objectives may therefore change as the coalitions in effective control change.

■ Organizational structure may result in non-maximizing behaviour; e.g. the presence of diverse stakeholders may induce the firm to set minimum targets for a range of variables as a means of reducing conflict.

■ Shipley’s seminal work (supported by later studies) found less than 16% of the firms studied to be ‘true’ profit maximizers.

■ However, Shipley found that 88% of firms included profit as part of their ‘goal set’.

■ Separation between ownership and control receives empirical support, though small ‘threshold’ levels of shareholdings may still secure effective control in modern plcs.

■ Profit remains a useful predictor of long-term firm behaviour, though sales revenue may be better in predicting shortterm firm behaviour.

■ Profit maximization may not be acknowledged as a goal by many firms, yet in setting ‘hurdle rates’ senior managers may implicitly be following such an objective.

■ Profitability and executive pay appear to be largely unrelated, suggesting that other managerial objectives might be given priority (sales revenue, growth, etc.). However, total remuneration ‘packages’ for top executives may be linked to profitability, helping to align the interests of managers more closely to the interests of shareholders.

■ Portfolio planning points to a variety of ever-changing objectives guiding firm activity rather than any single objective.

■ Firm behaviour in specific areas, e.g. price setting, will be influenced by a combination of firm objective and market structure.

Now try the self-check questions for this chapter on the Companion Website. You will also find useful links to relevant websites.

Notes

1 Average profit rate is total profit divided by total capital employed.

2 For instance, it is assumed in Fig. 3.6 that the four firm objectives are of the maximizing type, with only a single price outcome for each objective. Equally, Fig. 3.6 assumes that for each objective and market structure there is a single price outcome covering both short- and long-run time periods. If either of these assumptions is relaxed, there might be more than 16 different price outcomes from our figure.

References and further reading

Armstrong, J. S. and K. C. Green (2007) Competitor-oriented objectives: the myth of market share, International Journal of Business, 12(1): 117-36.

Arthur, W. B. (1996) Increasing returns and the new world of business, Harvard Business Review, 74(4): 100-9.

Barkema, H. G. and Gomez-Meija, L. R. (1998) Managerial compensation and firm performance, Academy of Management Journal, 41(2): 135-46.

Barreto I. (2010) Dynamic capabilities: a review of past research and an agenda for the future, Journal of Management, 36(1): 256-80.

Bau, F., and Dowling, M. (2007) An empirical study of reward and incentive systems in German enterpreneurial firms, Schmalenbach Business Review, 59(April): 160-75.

Baumol, W. J. (1959) Business Behaviour, Value and Growth, New York, Macmillan.

Berle, A. A. and Means, G. C. (1934) The Modern Corporation and Private Property, New York, Macmillan.

Buzzel, R. and Gale, B. (1987) The PIMS Principles: Linking Strategy to Performance, New York, Free Press.

Canals, J. (2001) How to think about corporate growth, European Management Journal, 19(6): 587-98.

Conyon, M. and Gregg, P. (1994) Pay at the top: a study of the sensitivity of top director remuneration to company specific shocks, National Institute Economic Review, 149(1): 83-92.

Conyon, M. and Leech, D. (1994) Executive compensation, corporate performance and ownership structure, Oxford Bulletin of Economics and Statistics, 56: 229-47.

Conyon, M. J. and Nicolitsas, D. (1998) Does the market for top executives work? CEO pay and turnover in small UK companies, Small Business Economics, 11(2): 145-54.

Crossan, K. and Lange, T. (2006) Business as usual? Ambitions of profit maximisation and the theory of the firm, Journal of Interdisciplinary Economics, 17(3): 313-26.

Cyert, R. M. and March, J. G. (1963) A Behavioural Theory of the Firm, New York, Prentice Hall.

DeCarlo, S. (2010a) Special Report: CEO Compensation, 28 April, New York, Forbes.com. DeCarlo, S. (2010b) Special Report: Global High Performers, 21 April, New York, Forbes.com. Ezzamel, M. and Watson, R. (1998) Market compensation earnings and the bidding-up of executive cash compensation: evidence from the United Kingdom, Academy of Management Journal, 41(2): 358-96.

Financial Times (1998) Shares in the action, 27 April.

Financial Times (2010) The facts about boardroom pay speak for themselves (letter from Steve Tatton, Editor, IDS Executive Compensation Review), 3 November.

Fisher, C. and Lovell, A. (2009) Business Ethics and Values: Individual, Corporate and International Perspectives (3rd edn), Harlow, Financial Times/Prentice Hall.

Fortune (2010) 100 Fastest Growing Companies, 6 September.

Freeman, R. E. (1984) Strategic Management: A Stakeholder Approach, Boston MA, Pitman.

Gregg, P., Machin, S. and Szymanski, S. (1993) The disappearing relationship between directors’ pay and corporate performance, British Journal of Industrial Relations, 31: 1-9.

Griffiths, A. (2000) Corporate objectives, risk taking and the market: the case of Cadbury Schweppes, British Economy Survey, 29(2): 45-51. Henderson, B. (1970) Intuitive strategy, Perspectives, 96, Boston MA, The Boston Consulting Group.

Hornby, W. (1994) The Theory of the Firm Revisited: a Scottish Perspective, Aberdeen, Aberdeen Business School.

Jensen, M. C. and Murphy, K. J. (1990) Performance pay and top management incentives, Journal of Political Economy, 98 (April): 225-65. Jobber, D. and Hooley, G. (1987) Pricing behaviour in UK manufacturing and service industries, Managerial and Decision Economics, 8: 167-77.

Leech, D. and Leahy, J. (1991) Ownership structure, control type classifications and the performance of large British companies, Economic Journal, 101(409): 1418-37.

Main, B. G. M. (1991) Top executive pay and performance, Management and Decision Economics, 12: 219-29.

Marris, R. (1964) The Economic Theory of Managerial Capitalism, New York, Free Press, Glencoe.

Meeks, G. and Whittington, G. (1975) Directors’ pay, growth and profitability, Journal of Industrial Economics, 24(1): 1-14.

Nyman, S. and Silberston, A. (1978) The ownership and control of industry, Oxford Economic Papers, 30(1): 74-101.

Peters, T. and Waterman, R. (1982) In Search of Excellence, New York, Harper & Row.

Porter, M. and Kramer, M. (2011) Creating shared value, Harvard Business Review, 89(1): 2-17.

Ramaswamy, V. and Gouillart, F. (2010) Building the co-creative enterprise, Harvard Business Review, 88(10): 100-109.

Rosen, S. (1990) Contracts and the market for executives, NBER Working Paper 3542, Cambridge MA, National Bureau of Economic Research.

RSA (1994) Tomorrow’s Company Inquiry, London, Royal Society for the Encouragement of Arts, Manufacturers and Commerce. Schmalensee, R. (1989) Intra-industry profitability in the US, Journal of Industrial Economics, 36(4): 212-36.

Shipley, D. and Bourdon, E. (1990) Distributor pricing in very competitive markets, Industrial Marketing Management, 19(3): 215-44.

Shipley, D. D. (1981) Primary objectives in British manufacturing industry, Journal of Industrial Economics, 29(4): 429-43.

Simon, H. A. (1959) Theories of decision making in economics, American Economic Review, 69(3): 253-83.

Stern, S. (2010) Outsider in a hurry to shake up Unilever, Financial Times, 4 April.

Storey, D., Watson, R. and Wynarczyk, P. (1995) The remuneration of non-owner managers in UK unquoted and unlisted securities market enterprises, Small Business Economics, 7(1): 1-13.

Vitaliano, D. F. (2003) Do not-for-profit firms maximize profit? The Quarterly Review of Economics and Finance, 43(1): 75-87.

Watson Wyatt Worldwide (2009) Executive Pay Practices Around the World. London.

Whittington, G. (1980) The profitability and size of United Kingdom companies, Journal of Industrial Economics, 28(4): 335-52.

Williamson, O. E. (1963) Managerial discretion and business behaviour, American Economic Review, 53(December): 1032-1057.