Free trade, regional trading blocs and protectionism

Protectionist measures are aimed at reducing the level of imports, either because of the ‘damage’ they cause to particular domestic industries, or because of their adverse effects on the balance of payments.

In this chapter we review critically the arguments in favour of free trade, and therefore against protectionism. We examine the international institutions which have been created to foster trade, particularly the General Agreement on Tariffs and Trade (GATT) and the World Trade Organization (WTO), and then note the measures available to countries wishing to pursue a protectionist strategy. The extent to which such measures have been used within both the European Union (EU) and the UK is considered, together with their alleged benefits and costs. We also consider the shift in trading patterns towards regional blocs and assess the implications of this development.Free trade

Free trade was given impetus by ‘The Theory of Comparative Advantage’, outlined by Ricardo in the nineteenth century. Essentially, Ricardo sought to extend Adam Smith’s principle of the division of labour to a global scale, with each country specializing in those goods which it could produce most efficiently. Even if one country was more efficient than another country in the production of all goods, Ricardo showed that it could still gain by specializing in those goods in which its relative efficiency was greatest. It was said to have a comparative advantage in such goods. This would raise total world output above the level it would otherwise be, with the benefits shared via trade between the two countries. The degree of benefit to any one country after specialization and trade would depend upon the terms of trade, i.e. the ratio of export to import prices.

The use of protectionist measures, such as tariffs, may distort the comparative cost ratios, by raising import prices and encouraging the domestic production of goods that could otherwise have been imported rather more cheaply.

In addition to disrupting the efficient allocation of domestic resources, such protectionist measures are likely to reduce international specialization and to lead to a less efficient allocation of world resources.Figure 26.1 shows that free trade could, in theory, bring welfare benefits to an economy previously protected. Suppose the industry is initially completely protected. The price Pd will then be determined by the interaction of domestic supply (S-Sh) and domestic demand (D-Dh). The government now decides to remove these barriers and to allow foreign competition. For simplicity, we assume a perfectly elastic ‘world’ supply curve Pw- C, giving a total supply curve (domestic and world) of SAC. Domestic price will then be forced down to the world level, Pw, with domestic demand being OQ3 at this price. To meet this domestic demand, OQ2 will be supplied from domestic sources, with Q2Q3 supplied from the rest of the world (i.e. imported). The consumer surplus, which is the difference between what consumers are prepared to pay and what they have to pay, has risen from DBPd to DCPw. The producer surplus, which is the difference between the price the producer receives and the minimum necessary to induce production, has fallen from PdBS to PwAS. The gain in consumer

id="Picutre 228" class="lazyload" data-src="/files/uch_group77/uch_pgroup315/uch_uch7347/image/image217.jpg">

Fig. 26.1 Free trade versus no trade.

surplus outweighs the loss in producer surplus by the area ABC, which could then be regarded as the net gain in economic welfare as a result of free trade replacing protectionism.

Critics of free trade suggest that a number of drawbacks may outweigh the net gain shown above:

■ The theory is based on a ‘full employment’ model and fails to appreciate the problems raised by chronic unemployment. For instance, in Fig. 26.1 if domestic supply falls from OQ1 to OQ2 as a result of the removal of tariffs, then the reduced output may lead to unemployment.

The welfare loss associated with this may more than offset the net welfare gain (area ABC) noted above.■ It fails to analyse how the gains that arise from trade will be distributed. In practice, the stronger economies, through their economic power, have often been able to extract the greater benefits.

■ It assumes a purely competitive model of industry. If, in fact, industry includes both large and small firms, then area ABC may not represent net gain. For instance, a higher proportion of the remaining domestic output OQ2 in Fig. 26.1 may now be in the hands of a monopoly. This growth in importance of monopoly could be construed as a welfare loss to be set against the area of net gain, ABC.

In practice a number of organizations have tried to encourage free trade in the post-war period.

General Agreement on Tariffs and Trade (GATT)/World Trade Organization (WTO)

The General Agreement on Tariffs and Trade (GATT) was signed in 1947 by 23 industrialized nations including the US, Canada, France and the Benelux countries. Its successor, the World Trade Organization (WTO), was established in 1995 and now has 153 members. China was the latest high-profile recruit, joining in 2001, although the newest member is Cape Verde. WTO members in total account for more than 97% of the value of world trade. The objectives of the WTO are essentially the same as GATT’s: that is, to reduce tariffs and other barriers to trade and to eliminate discrimination in trade. But the WTO is much more than GATT. Although the latter still provides the principal rulebook for trade in goods, the WTO has broadened out the agreement to also include services (the General Agreement on Trade in Services) and intellectual property such as copyright, trademarks and patents (the Agreement on Trade Related Aspects of Intellectual Property, also known as TRIPS).

Since the GATT was signed there have been eight rounds of negotiations paving the way for considerable cuts in the level of tariffs being applied.

In 1947 the average tariff in the industrialized world stood at some 40%, but the figure has now dropped in 2010 to around 5%. The ‘Kennedy round’ of negotiations in the 1960s was particularly effective, cutting tariffs by around one-third. The ‘Tokyo round’ in the latter part of the 1970s resulted in further reductions of a similar magnitude.An important series of multilateral negotiations, known as the Uruguay round, was completed in December 1993. This proved to be a particularly complex and ambitious round of negotiations. It consisted of 28 accords designed to extend fair trade rules to agriculture, services, textiles, intellectual property rights and foreign investment. It was agreed to make further cuts in tariffs on industrial products, to eliminate tariffs entirely in 11 sectors and to substantially reduce the level of farm subsidies. Non-tariff barriers were to be converted into the more viable tariff barriers (Greenaway 1994). Significantly, the most recent series of negotiations, known as the Doha round, begun in 2001 has proved to be even more protracted than the Uruguay round and yet to reach any sort of agreement. A key issue is the vexed subject of agricultural liberalization, with neither the US nor the EU willing to make sufficient concessions in terms of the removal of subsidies to their farmers. We will return to this subject later. In addition, middle-income countries such as Brazil and India are proving reluctant to open their markets for industrial goods until in return there is more on offer from the richer countries.

GATT itself, the accord on services and intellectual property and the codes on government procurement and anti-dumping have now been placed under the umbrella of the WTO. Trade disputes between member states are settled in this arena by a streamlined disputes procedure with the provision for appeals and binding arbitration. Since its creation in January 1995, more than half the cases brought before the WTO have involved the US and the EU, whilst around one-quarter have involved developing countries.

Trade disputes which go to arbitration still tend to be fairly lengthy affairs, as can be seen from the case of the importation of polyethylene retail bags from Thailand into the US. Although the complaint was lodged by Thailand in November 2008, it was not until March 2010 that the US informed the WTO that it would implement the recommendations of the body. Moreover, it took a further six-month period before it actually began to do so, meaning all in all, close to two years from start to finish.Although the aim of the WTO is to reduce tariff barriers, there are a number of circumstances in which a country will be allowed to maintain such barriers. Article 6 of the original GATT permits retaliatory sanctions if ‘dumping’ can be proven. Article 18 also provides a number of ‘escape clauses’ for the newly industrializing economies, allowing some protection of both infant industries and of their balance of payments. Article 19 permits any country to abstain from a general tariff cut in situations where rising imports may seriously damage domestic production. Articles 21-25 are concerned with the protection of the national interest, permitting restrictions to be placed on imported products which might affect the nation’s security.

Aside from tariff cuts, the WTO/GATT has made efforts to eliminate discrimination in trade by use of the ‘most-favoured nation’ (MFN) principle. This means that each member country has to treat each of its fellow members equally; any trading advantage granted by one country to another must be accorded to all other member states. The MFN clause is so important that it was actually the first article of the original GATT. It has also been incorporated in the GATS (Article 2) and the TRIPS (Article 4). Some exceptions are allowed from MFN, for example when a free trade area has been established by a specific group of countries. In general, however, the MFN means that no discrimination is permitted in trade relations.

One indication that there is growing understanding of the benefits of free trade is the sharp drop in the number disputes coming before the WTO.

In total, WTO members initiated an average of 41 new disputes per year during 1995 to 2000, but this falls to an average of just half this total between 2001 and 2009. The drop is almost entirely due to the US and EU launching fewer cases. Developing countries’ use of the disputes process has been steadier and provides some evidence of their commitment to the multilateral rules-based WTO system.I Trade and the world economy

The rapid growth of world trade over the past 100 years or so reflects the fact that nations have become more interrelated as they have attempted to gain the benefits of freer trade. One way of measuring this increasing integration is to compare the relative growth of world trade and world output, as seen in Table 26.1.

Table 26.1 shows that the growth rate of world merchandise exports (Trade) has exceeded the growth of world output (GDP) in five of the six periods, clearly suggesting an acceleration of global integration through trade. The only exception to this pattern occurred during 1913-50 when two world wars and a major world depression led to economic depression and the emergence of protectionist trade policies. The post-Second World War period (1950-73) saw an unprecedented growth of world trade which far outstripped the growth of world production. This period of freer trade reflected the desire to reduce the high protective tariffs introduced during the inter-war period as a means of increasing post-war prosperity for all countries. The founding of the GATT in 1947 was a positive step in this direction. Since 1991 it is significant that a more profound move towards globalization of the world economy has seen a further acceleration in the average growth rate of exports. In this regard, it is noteworthy that developing and newly industrializing countries have achieved the fastest expansion of trade. With an average annual rise of close to 10%, their share of world trade has increased from 24 to 40%.

It may be useful to enquire at this stage whether the expanding role of world trade seen in Table 26.1 was accompanied by an increase in the share of that trade conducted on a regional basis. It would seem natural that nations would tend to trade more with their immediate neighbours in the first instance, thereby raising the share of world trade occurring between nations within a specific geographical region. This tendency towards intra-regional trade can be seen in Table 26.2.

From Table 26.2 it can be seen that the share of intra-regional trade grew most rapidly in Western Europe between 1948 and 1996. However, between 1996 and 2004, North America saw the most rapid growth in intra-regional trade. In the most recent period, it is the Middle East and Latin America that have enjoyed the biggest gains in intra-regional trade. It is also clear from Table 26.2 that intra-regional

Table 26.1 Growth in world GDP and merchandise trade, 1870-2009 (average annual % change).

Table 26.2 Shares of intra-regional trade in total trade, 1928-2009 (% of each region's total trade in goods occurring between nations located in that region).

| 1928 | 1938 | 1948 | 1968 | 1979 | 1996 | 2004 | 2009 | |

| Western Europe | 50.7 | 48.8 | 41.8 | 63.0 | 66.2 | 68.3 | 73.8 | 72.2 |

| CIS | 20.7 | 19.2 | ||||||

| North America | 25.0 | 22.4 | 27.1 | 36.8 | 29.9 | 36.0 | 56.0 | 48.0 |

| Latin America | 11.1 | 17.7 | 17.7 | 18.7 | 20.2 | 21.2 | 23.2 | 26.1 |

| Asia | 45.5 | 66.4 | 38.9 | 36.6 | 41.0 | 51.9 | 50.3 | 51.6 |

| Africa | 10.3 | 8.8 | 8.4 | 9.1 | 5.6 | 9.2 | 9.9 | 11.7 |

| Middle East | 5.0 | 3.6 | 20.3 | 8.7 | 6.4 | 7.4 | 5.6 | 15.5 |

Source: WTO (2010a) Annual Report, and previous editions.

trading is not a new phenomenon and that geographically adjacent nations in many areas of the world have been trading with each other for many decades.

Regional trading arrangements (RTAs)

As we have noted above, the resumption of rapid growth in world trade after the Second World War was tied up with the desire for the resumption of multilateral trade under the auspices of the GATT. However, this movement towards free trade was accompanied by a parallel movement towards the formation of regional trading blocs centred on the EU, North and South America, and East Asia. We noted in Table 26.2 that intra-regional trading is not a new phenomenon and has been active for at least a century or more. However, what is new involves the fact that the nations of a given region have begun to create more formal and comprehensive trading and economic links with each other. By 2010 there were more than 280 RTAs in force, many of which had been established over the previous decade.

There are four types of regional trading arrangements:

1 free trade areas, where member countries reduce or abolish restrictions on trade between each other while maintaining their individual protectionist measures against non-members;

2 customs unions, where, as well as liberalizing trade amongst members, a common external tariff is established to protect the group from imports from any non-members;

3 common markets, where the customs union is extended to movements of factors of production as well as products;

4 economic union, where national economic policies are also harmonized within the common market.

Three features have characterized post-war regional integration.

1 Regional integration has been primarily centred in Western Europe. More than half of all the RTAs established have involved West European countries, with many of the more recent agreements with the EU involving the Central and Eastern European countries.

2 Only a relatively small number of regional agreements have been concluded by developing countries although this is now changing. This is mainly due to continuing competition between these countries involving trade in similar products (e.g. primary products) together with the difficulty of achieving the political stability in some developing countries which is so vital to trade.

3 The type of economic integration between the parties to agreements has varied quite significantly. Most of the notifications made to GATT have involved free trade areas, with the number of customs unions agreement being much smaller.

Table 26.3 provides examples of different types of regional trading arrangements across the globe. For example, the most advanced form of trading bloc is the EU which originated as a customs union but moved towards the common market type of

Table 26.3 Regional Trading Arrangements (RTAs): intra-regional export shares (%).

| 1990 | 1995 | 2004 | 2009 | |

| NAFTA | 42.6 | 46.1 | 56.0 | 47.9 |

| EU | 64.9 | 64.0 | 68.5 | 66.7 |

| MERCOSUR | 8.9 | 20.5 | 12.5 | 15.2 |

| ASEAN | 20.1 | 25.5 | 25.0 | 24.8 |

| ANDEAN | 4.2 | 12.2 | 7.7 | 7.7 |

Source: WTO (2010b) International Trade Statistics.

arrangement in the 1990s, the majority of members effectively progressing into a type of economic union with the advent of the euro and its related financial arrangements on 1 January 1999. At the start of 2010 the EU consisted of 27 nations with a combined population of over 490 million and accounted for about 38% of world trade. In August 1993 the North American Free Trade Agreement (NAFTA) was signed between the US, Canada and Mexico, having grown out of an earlier Canadian-US Free Trade Agreement (CUFTA). NAFTA, as the name implies, is a free trade arrangement covering a population of 372 million and accounting for around 20% of world trade.

MERCOSUR was established in South America in 1991, evolving out of the Latin American Free Trade Area, the four initial members being Argentina, Brazil, Paraguay and Uruguay. It developed into a partial customs union in 1995 when it imposed a common external tariff covering 85% of total products imported.

In Asia and the Pacific, the rather ‘loose’ Association of South East Asian Nations (ASEAN) with a population of 300 million was formed in August 1967. In 1991 they agreed to form an ASEAN Free Trade Area (AFTA) by the year 2003. A Common External Preference Tariff (CEPT) came into force in 1994 as a formal tariff-cutting mechanism for achieving free trade in all goods except agricultural products, natural resources and services. One of the latest arrangements initiated covers ASEAN, Australia and New Zealand. This came into force at the start of 2010 and has the explicit goal of liberalizing and facilitating trade within the area.

RTAs have also featured in trade liberalization in Africa over the past decade. The Common Market for Eastern and Southern Africa (COMESA) is the largest RTA in geographic terms, with some 19 members. It is a free trade area which was established in the mid-1990s, has eliminated customs tariffs and is working on the elimination of quantitative restrictions and other non-tariff barriers. In central and eastern Europe, a free trade area was established in the early 1990s (CEFTA), although the three founding members, Poland, Hungary and Czechoslovakia (now the Czech Republic and Slovakia), have since left to join the EU. The remaining members are Albania, Bosnia and Herzegovina, Croatia, Macedonia, Moldova, Montenegro and UKMIK/ Kosovo.

From the above examples it is possible to see that trading blocs have adopted various types of arrangements depending on their specific circumstances. Table 26.3 shows the share of intra-regional exports of each specific bloc as a percentage of the total exports of that bloc. For example, in 2009 the exports of EU members to each other comprised around two-thirds of total EU exports. A significant shift towards intra-regional exports took place in Europe, North and Central America, and Asia between 1960 and 1970, but since that time the tend has moderated.

The completion of the Uruguay round in December 1993 served as a step forward in the cause of multilateral trade. However, frustration with the slow progress of the Doha round, and increasing frictions over the level of currencies (fuelled by a depreciating dollar and the renminbi peg), have reinforced concerns that regional trading blocs may begin to look inwards and behave more like ‘regional fortresses’. Thus, the trading blocs we have been discussing above have begun to be seen as initiators of a ‘new regionalism’, leading to potential problems for interbloc trade. Those who favour the regional approach argue that the setting up of trading blocs can enable individual countries to purchase products at lower prices because tariff walls between the member countries have been removed; this is the trade creation effect. They also argue that regional trading arrangements help to harmonize tax policies and product standards, while also helping to reduce political conflicts. Others argue that where the world is already organized into trading blocs, negotiations in favour of free trade are more likely to be successful between, say, three large and influential trading blocs than between a large number of individual countries with little power to bargain successfully for tariff reductions.

On the other hand, the critics of regionalism warn that regional trading blocs have, historically, tended to be inward looking, as in the 1930s when discriminatory trade blocs were formed to impose tariffs on non-members. Some also argue that member countries may suffer from being inside a regional bloc because they then have to buy products from within the bloc, when cheaper sources are often available from outside, i.e. the trade diversion effect. Further, it is argued that regionalism threatens to erode support for multilateralism in that business groups within a regional bloc will find it easier to obtain protectionist (trade diversionary) deals via preferential pacts than they would in the world of non-discriminatory trade practices favoured by GATT. Finally, it is argued that regionalism will move the world away from free trade due to the increasing tendency for members of a regional group to resort to the use of non-tariff barriers (VERs, anti-dumping duties, etc.) when experiencing a surge of imports from other countries inside the group. Such devices, all part of the new protectionism, can then easily be used by individual countries against non-members from other regional groups.

Many studies have been made as to the trade and welfare effects of such regional blocs both on ‘internal’ participants and on countries outside the bloc.

■ Analyses of the customs union formed between the original six members of the European Community (EC) have shown that trade creation exceeded trade diversion in the case of manufactures (Lloyd 1992; Srinivasan et al. 1993), but that the reverse was true in the case of trade in agricultural products - leaving the overall effect unclear.

■ Studies of EFTA suggest that trade creation just outweighed trade diversion (Lloyd 1992).

■ Studies for CUFTA suggest positive benefits for Canada but negligible benefits for the US, while trade with third countries declined (Primo Braga et al. 1994).

■ For NAFTA, estimates indicate some net trade creation with small trade effects for third countries (Reinert et al. 1994).

■ Research by Prusa and Teh in 2010 shows antidumping cases within RTAs have dropped by between 33 and 55%. However, they found that there has been a 10-30% increase in the number of anti-dumping actions over the same period against countries that are not part of the trading bloc.

The various studies noted above can only give a general idea of the net effects as they do not measure accurately the potential stimulus to third countries resulting from any higher rate of economic growth in the bloc being studied.

What then can be done to make sure that regionalism and multilateralism (general free trade) can coexist? First, it has been suggested that article 24 of GATT which sets the rules for regional arrangements could be modified to allow only customs unions (i.e. regions which require a common external tariff) and to prohibit free trade areas which allow countries to retain a variety of national tariffs against other countries. If this were done, the more liberal members of the region would then be able to force down the overall regional tariff level, which could then be ‘locked in’ under GATT rules and prevented from being subsequently raised. Second, in order to fight the ‘new protectionism’, GATT articles 6 (antidumping) and 19 (VER) could be strengthened to minimize the use of non-tariff barriers against countries outside the regional arrangement (IMF 1993).

Protectionism

Methods of protection

There are a number of methods which individual countries or regional trading blocs can use to restrict the level of imports into the home market.

Tariff

A tariff is, in effect, a tax levied on imported goods, usually with the intention of raising the price of imports and thereby discouraging their purchase. Additionally, it is a source of revenue for the government. Tariffs can be of two types: lump sum, or specific, with the tariff a fixed amount per unit; and ad valorem, or percentage, with the tariff a variable amount per unit.

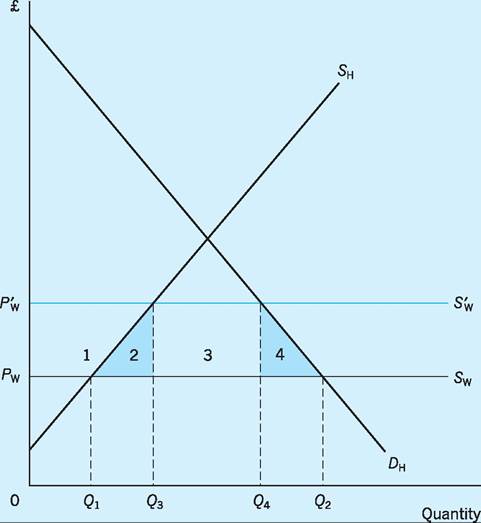

To examine the effect of a tariff, it helps to simplify Fig. 26.2 if we again assume a perfectly elastic world supply of the good Sw at the going world price Pw, which implies that any amount of the good can be imported into the UK without there being a change in the world price. In the absence of a tariff the domestic price would be set by the world price, Pw in

Fig. 26.2 The effect of a tariff.

Fig. 26.2. At this price, domestic demand Dh will be OQ2 though domestic supply Sh will be only 0Q1. The excess demand, Q2 - Q1, will be satisfied by importing the good.

If the government now decides to restrict the level of import penetration, it could impose a tariff of, say, Pw - PW. A tariff always shifts a supply curve vertically upwards by the amount of the tariff, so that in this case the world supply curve shifts vertically upwards from Sw to SW. This would raise the domestic price to SW which is above the world price Pw. This higher price will reduce the domestic demand for the good to 0Q4, whilst simultaneously encouraging domestic supply to expand to 0Q3. Imports will be reduced to Q4 - Q3. Domestic consumer surplus will decline as a result of the tariff by the area 1 + 2 + 3 + 4, though domestic producer surplus will rise by area 1, and the government will gain tax revenue of (PW - Pw) + (Q4 - Q3) (i.e. area 3). These gains would be inadequate to compensate consumers for their loss in welfare, yielding a net welfare loss of area 2 + 4 as a result of imposing a tariff.

The UK was extensively protected by tariffs until the 1850s. These were progressively dismantled in an era of free trade that lasted until the First World War. The first significant reintroduction of tariffs occurred in 1915 with the ‘McKenna duties’, a 33.3% ad valorem tax on luxuries such as motor cars, watches, clocks, etc. They were designed to discourage unnecessary imports in order to save foreign exchange, and thereby free shipping space for the war effort. In 1921, the Safeguarding of Industry Act extended protection to key industries. This was followed in 1932 by the Import Duties Act, which provided a comprehensive range of protection; a 20% ad valorem duty on manufactured goods in general, but 33.3% on articles such as bicycles and chemicals, and 15% on certain industrial raw materials and semi-manufactures.

Since the Second World War, the UK, along with others, has moved away from the protectionist doctrine of the inter-war period. We have already seen that considerable reductions in tariffs took place under the auspices of GATT. However, for the UK, entrance into the EU in 1973 has had a dual effect. Although tariffs on industrial products have been eliminated between member countries, permitting free trade, at the same time a Common External Tariff (CET) has been imposed on industrial trade with all non-member countries, with import tariffs varying by product. For example, whilst the average tariff on industrial imports into the EU is 3.5%, the tariff on shoes is as high as 17%. In contrast, most mineral imports carry a zero rate of duty.

Non-tariff barriers

During the 1990s many quantitative restrictions on trade were gradually replaced by tariffs. Exceptions do, however, remain with significant non-tariff barriers affecting trade in textiles and clothing. There are a number of different types of non-tariff barriers.

Quotas

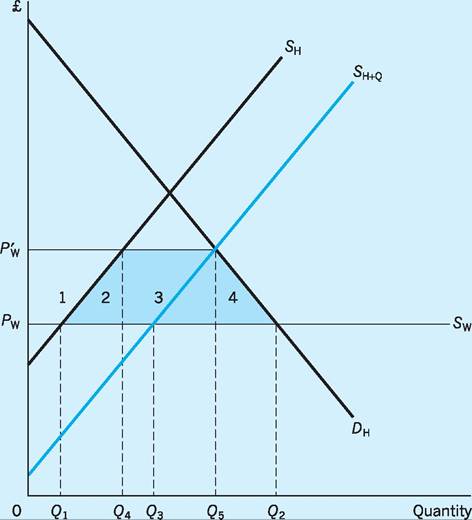

A quota is a physical limit on the amount of an imported good that may be sold in a country in a given period. Its effects are examined in Fig. 26.3. As in the case of a tariff, we assume for simplicity that the world supply curve is perfectly elastic at Pw. Once again, if there is free trade, the domestic price will be set by the world price, Pw. Domestic production would initially be 0Q1 though demand would be considerably higher at 0Q2. This excess would be satisfied by importing the amount Q2 - Q1 of the particular good.

If the government were now to decide that it wanted to limit the level of imports to, say, Q3 - Q1, it could impose a quota to this effect. The total supply curve to the UK market now becomes the domestic supply curve, ⅛, plus the fixed quota permitted from abroad, Q. The new domestic price rises from Pw to PW which in turn reduces domestic demand from 0Q2 to 0Q5. Domestic supply will expand to 0Q4, with imports reduced to the quota level Q3 - Q1 (= Q5 - Q4).

As in the case of the tariff, the imposition of a quota will involve a loss in consumer surplus (i.e. area 1 + 2 + 3 + 4). However, in contrast to the tariff, the only area of welfare gain will be the producer surplus of area 1, since the government receives no increase in tax revenue from the quota. This leaves area 2 + 3 + 4 as the net loss of economic welfare. For any given price rise, the welfare loss is then greater for a quota than for a tariff.1 Import quotas are still used on a whole range of products. They may be applied either unilaterally or as a result of negotiated agreements between the two parties. For instance, the EU has the authority to negotiate quota agreements on behalf of member states, including the UK, and does so on a whole range of products.

Fig. 26.3 The effect of a quota.

One of the most significant quota arrangements, which has now been phased out, was the Multi-Fibre Agreement (MFA). This came into effect in 1974 and controlled the import of textiles from the newly industrialized countries. A major aim of the MFA was to provide greater scope for newly industrialized countries to increase their share of world trade in textile products whilst at the same time maintaining some stability for textile production in the developed economies. The MFA was phased out at the beginning of 2005, but one of the interesting consequences of this was that some of the exporters of textiles suffered in the wake of this development. Lesotho, Swaziland and Madagascar all found themselves unprepared for a more competitive environment. Textile exports fell by almost one-fifth over the following two years as companies based elsewhere were no longer restricted by quotas.

An UNCTAD study (World Bank 1986) concluded that the complete liberalization of trade barriers would bring substantial benefits for developing countries. It was suggested that their total export of clothing would rise by around 135% while textile exports could grow by some 80%. A number of more recent analyses carried out by the World Bank have put the potential gains at an even greater level. These figures seem to indicate quite clearly that the export quotas work against the interest of the producers rather than the consumers. But there is an argument that the developing countries actually benefited through the MFA arrangement. This is because, it is asserted, they received what may be termed quota rents, i.e. higher prices than would be guaranteed through a free market.

Looking back to Fig. 26.3, this benefit would amount to area 3. However research into this by Balassa and Michalopoulos (1985) estimated that the value of lost output to the US exceeds the quota rent by nine times and to the EU by a factor of seven.

Subsidies

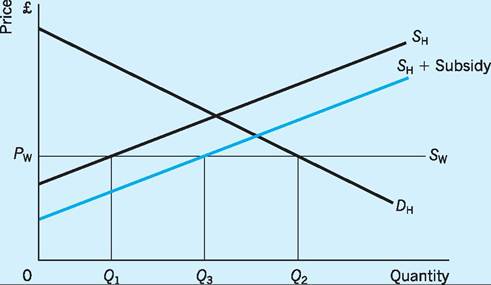

The first two forms of protection we have described have both been designed to restrict the volume of imports directly. An alternative policy is to provide a subsidy to domestic producers so as to improve their competitiveness in both the home and world markets. The effect of this is demonstrated in Fig. 26.4.

Once again, we assume that the world supply curve is perfectly elastic at Pw. Under conditions of free trade, the domestic price is set by the world price at Pw. Domestic production is initially 0Q1 with imports satisfying the excess level of demand which amounts to Q2 - Q1. The effect of a general subsidy to an industry would be to shift the supply curve of domestic producers to the right. The domestic price will remain unchanged, but domestic production will rise to 0Q3 with imports reduced to Q2Q3. If, however, the subsidy is provided solely for exporters, the impact on the domestic market could be quite different- The incentive to export may encourage more domestic production to be switched from the home market to the overseas markets which, in turn, could result in an increased volume of imports to satisfy the unchanged level of domestic demand

Fig. 26.4 The effect of a general subsidy.

Subsidies continue to be widely employed in agriculture alongside other forms of protection- The US and the Cairns group of farm exporters, which includes Australia, Canada and Brazil, is pushing for a liberalization of trade in agricultural products- For example, producer support grant in the OECD area for agriculture still accounted for around $350bn in 2009 with the EU accounting for the largest share of this expenditure (36%) followed by Japan (24%). However, it is noteworthy that the US ranked third in the league table (20%) in terms of providing support for its farmers- Anti-subsidy cases brought before the WTO hit a peak in 1999 with 41 complaints, before falling to as few as six complaints in 2005-

Currency manipulation

The US Treasury stopped short of labelling China a currency manipulator in its latest assessment conducted during 2010. Nevertheless, it continues to argue that the extremely low level of the renminbi is an impediment to free trade and is a key factor explaining the huge bilateral trade imbalance between the two nations, and an impediment to a global economic recovery in the wake of the fall-out from the credit crunch- Indeed, this has become an even bigger issue as the Chinese currency has become more competitive against other emerging market currencies- Morgan Stanley suggested in the middle of 2010 that the Chinese currency would need to rise by at least 15% to bring it closer to ‘fair value'. A cheap currency can have significant implications for trade patterns, particularly if it is managed centrally and is thus unable to appreciate sufficiently to reflect market forces. In some ways, this ‘currency manipulation' strategy may be viewed as another form of protectionism.

Exchange controls

A system of exchange controls was in force in the UK from the outbreak of the Second World War until 1979 when, in order to allow the free flow of capital, they were abolished. They enabled the government to limit the availability of foreign currencies and so curtail excessive imports; for instance, holding a foreign- currency bank account had required Bank of England permission. Exchange controls could also be employed to discourage speculation and investment abroad.

Safety, technological and environmental standards These are often imposed in the knowledge that certain imported goods will be unable to meet the requirements. The UK government used such standards to prevent imports of French turkeys and ultraheat-treated (UHT) milk. Ostensibly the ban on French turkeys was to prevent ‘Newcastle disease', a form of fowl pest found in Europe, reaching the UK. The European Court ruled, however, that the ban was merely an excuse to prevent the free flow of imports. In the mid-1990s Germany effectively blocked imports of traffic cones from a UK manufacturer while it ‘upgraded' its testing requirements no fewer than 12 times. The cones passed the test each time, but the German authorities refused to issue approval certificates or to publish their standards. Eventually, pressure from the UK led to the standard for cones being published which allowed sales of cones to Germany to proceed. The US, meanwhile, banned shrimp imports from countries that fish using ‘Turtle Excluder Devices', a ban that included fish from India. While the policy may appear to have an environmental motive, it was also a form of discrimination. Significantly, it was applied to all Indian exports, whether farmed (as the bulk of shrimps are) or caught in the ocean. A more pertinent issue relates to genetically modified foods. The EU has effectively banned the import of GM products, much to the irritation of the US amongst others. GM crops now account for 75% of the US annual output of soya beans, 71% of its cotton and 34% of its corn. The WTO rules do allow countries to regulate imports on health and environmental grounds, but any restraints must be based on ‘sufficient scientific evidence'. In the case of GM foods, this is a point of dispute.

Time-consuming formalities

In 1990, the EU alleged that ‘excessive invoicing requirements' required by US importing authorities had hampered exports from member countries to the US. In Asia these problems abound. For example, Indonesian customs officials take at least a week to process imports, and this often involves considerable administrative and capital costs for many companies. A similar problem in China can lead to two or three weeks' delay.

Table 26.4 Anti-dumping cases initiated.

Public sector contracts

Governments often give preference to domestic firms in the issuing of public contracts, despite EU directives requiring member governments to advertise such contracts. A number of Australian states have continued to give price preferences of up to 20% to domestic bidders for public contracts in the latter half of the 1990s. Public contracts are actually placed outside the country of origin in only 1% of cases.

Labour standards

This is not an area currently subject to WTO rules and disciplines, but some countries do believe the issue should be examined as a first step towards bringing the matter of core labour standards within the WTO framework. However, many developing and some developed nations contend that the issue has no place within the WTO framework and see it as little more than a smokescreen for protectionism by the more developed economies from low-wage competition. Areas of particular concern include the issues of child labour and slave labour, but the broader issue of setting minimum labour standards is where opinion tends to diverge. The issue is a bone of contention in the current Doha round of negotiations.

The case for protection

A number of arguments have been used to justify the application of both tariff and non-tariff barriers:

■ to prevent dumping;

■ to protect infant industries;

■ to protect strategically important industries.

Dumping occurs where a good is sold in an overseas market at a price below the real cost of production. Under Article 6 of the GATT, the WTO allows retaliatory sanctions to be applied if it can be shown that the dumping materially affected the domestic industry. As well as using the WTO, countries within the EU can refer cases of alleged dumping for investigation by the European Commission. The Commission is then able to recommend the appropriate course of action, which may range from ‘no action’ where dumping is found not to have taken place, to either obtaining an ‘undertaking’ of no further dumping, or imposing a tariff.

Table 26.4 indicates a decline in anti-dumping cases initiated by the WTO in recent years. This is particularly encouraging in view of the severity of the recession that followed the onset of the credit crunch in many large economies.

The US has consistently been one of the main initiators of anti-dumping investigations. Canada, India and the EU have also initiated numerous actions. The main targets of anti-dumping probes have been the EU, China, Taiwan and India, although it is interesting that China has itself taken advantage of this mechanism in recent years. The sectors where antidumping measures are most widely applied include chemical products and base metals, in particular steel. In 2010, the US imposed anti-dumping measures on warm water shrimps from Vietnam while China put in place restrictions on flat rolled electrical steel from the US.

The use of protection in order to establish new industries is widely accepted, particularly in the case of developing countries. Article 18 of GATT explicitly allows such protection. An infant industry is likely to have a relatively high cost structure in the short run, and in the absence of protective measures may find it difficult to compete with the established overseas industries already benefiting from scale economies. The EU has used this argument to justify protection of its developing high-technology industries.

The protection of industries for strategic reasons is widely practised in both the UK and the EU, and is not necessarily contrary to GATT rules (Article 2). The protection of the UK steel industry has in the past been justified on this basis, and the EU has used a similar argument to protect agricultural production throughout the Community under the guise of the CAP. In the Uruguay round of GATT, the developing countries used this argument in seeking to resist calls for the liberalization of trade in the service sector. This has been one of the few sectors recording strong growth in recent years and is still a highly ‘regulated’ sector in most countries.

Criticisms of protectionism

Retaliation

A major drawback to the imposition of protectionist measures is the possibility of retaliation. For example, in 2007 the EU initiated an anti-dumping investigation over Chinese fastener exports and imposed new duties of up to 85% in January 2009. China responded by initiating its own anti-dumping investigation over EU exports of a different variety of fastener and it imposed new 25% tariffs. Other examples include the WTO approving $4bn worth of trade sanctions to be applied by the EU in response to tax breaks being given by the US government to multinationals such as Boeing and Microsoft and to the imposition of steel tariffs in the US. In most cases, the threat of retaliation has been sufficient to produce a compromise, but there is always a danger that a full-blown trade war could result from retaliatory actions.

Misallocation of resources

We saw in Figs 26.1-26.3 that protectionism can erode some of the welfare benefits of free trade. For instance, Fig. 26.2 showed that a tariff (and Fig. 26.3 a quota) raises domestic supply at the expense of imports. If the domestic producers cannot make such products as cheaply as overseas producers, then one could argue that encouraging high-cost domestic production is a misallocation of international resources.

A related criticism also suggests that protectionism leads to resource misallocation on an international scale, but this time concerns the multinational. We saw in Chapter 7 that multinationals are the fastest- growing type of business unit in Western economies, and that they are increasingly adopting strategies which locate particular stages of the production process in (to them) appropriate parts of the world. Protectionism may disrupt the flow of goods from one stage of the production process to another, and in this sense inhibit global specialization.

A number of studies have been carried out in recent years on the impact of protectionism on the global economy. The most recent report produced by the OECD (2006) suggests that a 50% cut in agricultural support and a similar percentage reduction in applied tariffs would boost global GDP by $44bn. Almost two-thirds of the gain would accrue to the farming industry. Other studies generate even more positive outcomes. For example, a World Bank analysis (2005) concluded that if all trade protection were to be eliminated then the global welfare gain would amount to $278bn, with $173bn resulting from removing agricultural subsidies. Meanwhile a group of economists led by Robert Stern estimates that lowering services barriers by one-third under the Doha Development Agenda would raise developing countries’ incomes by around $60bn.

Fair trade as well as free trade

We noted earlier that the failure to advance the Doha trade round is in part a function of the reluctance of the rich economies to make sufficient concessions in terms of reducing their own array of protectionist measures. This is rather ironic since the OECD study (2006) referred to above shows that over 90% of the estimated benefit from the reform of agricultural policies goes to the OECD countries themselves.

The uneven outcome of trade negotiations prior to the current Doha round is reflected in the fact that tariff levels in the advanced industrial countries against the developing world are four times higher than against the developed countries. Indeed, as Joseph Stiglitz (2006) points out, the last round of successful trade negotiations, namely the Uruguay round, actually left the poorer countries worse off. While the developing countries were forced to open up their markets, the advanced economies continued to protect agriculture and to maintain barriers against key products from the developing world.

I Conclusion

The current Doha round of trade negotiations is struggling to make very much headway, with attempts to extend the range of goods and services covered under the auspices of the WTO proving difficult. There is clearly a need for the developed economies to make greater concessions and for all countries to recognize that free trade creates many more ‘winners’ than ‘losers’, with developed countries themselves benefiting most from reducing their own protectionist barriers.

For the time being, the volume of world trade is continuing to grow. But with the global economy struggling to cope with the legacy of the credit crunch, the risk remains of a retreat towards protectionism. This may conceivably at least initially take the form of competitive currency devaluations, but it could spread beyond that when such a move fails to solve the underlying issues. Unless there is a renewed recognition of the worldwide costs of protection, lobbies in various countries may still succeed in curbing the growth of international specialization and trade in a misleading attempt to revive economic fortunes.

Key points

■ In a competitive, full employment framework, free trade can be shown to yield a net welfare gain vis-a-vis various protectionist alternatives.

■ In the more realistic situation of ‘market failures’, the existence of monopoly power, unemployment, etc. may offset (in part or in whole) these welfare gains.

■ The General Agreement on Tariffs and Trade (GATT) established in 1947, and its successor the World Trade Organization (WTO), seek to reduce tariffs and other barriers to trade, and to eliminate discrimination in trade.

■ The GATT/WTO have had some success, cutting the average tariff in the industrialized world from 40% in 1947 to less than 5% in 2010.

■ Since 1870, the growth of trade has exceeded the growth of world GDP in all but the period between the First and Second World Wars.

■ Intra-regional trade (i.e. trade within a region) has grown substantially in recent decades. For example, around three- quarters of all Western European trade occurs between countries in Western Europe.

■ Various types of regional trading arrangement have promoted this trend. Free Trade Areas, Customs Unions (which have an external tariff barrier), Common Markets (in which factors of production can also freely move) and Economic Unions (with harmonization of member policies) have all been used to this end.

■ Various types of protection have been used by countries, including tariffs, quotas, currency manipulation, subsidies, exchange controls and a range of restrictions involving technological standards, safety, etc.

■ Arguments often advanced in favour of protectionist policies include the prevention of dumping, the protection of infant industries and the protection of strategically important industries.

■ Arguments against protectionist policies include retaliation and a misallocation of resources on both a national and international scale, leading to welfare loss.

Now try the self-check questions for this chapter on the Companion Website. You will also find useful links to relevant websites.

Note

1 It could, however, be argued that the welfare loss is overestimated by this analysis. Area 3, though no longer received by the government as tax revenue, may still be received by importers.

Although paying only Pw to the foreign suppliers, the importers now receive PW when selling Q5 - Q4 on the domestic market.

References and further reading

Balassa, B. and Michaelopoulos, M. (1985) Liberalizing World Trade, Development Policy Issues Series Report VPERS4, Washington DC, World Bank.

Barrell, R. E. and Pain, N. (1999) Trade restraints and Japanese direct investment flows, European Economic Review, 43(1): 29-45.

Bayard, T. O. and Elliot, K. A. (1994) Reciprocity and Retaliation in US Trade Policy, Washington DC, Institute for International Economics.

Benassy-Quere, A. and Coeure, B. (2010) Economic Policy, New York, Oxford University Press.

Bhagwati, J. (1992) Regionalism and multilateralism: an overview, Discussion Paper No. 603, New York, Columbia University. Booth, P. and Wellings, R. (2009) Globalization and Free Trade, Cheltenham, Edward Elgar. Boughton, J. and Lombardi, D. (2009) Finance, Development and the IMF, Oxford, Oxford University Press.

Bown Chad, P. (2010) The WTO dispute settlement system would survive without Doha, VOX, 19 June.

De Melo, J. and Panagariya, A. (1992) The new regionalism, Finance and Development, December, 37-40.

Dicken, P. (2011) Global Shift: Reshaping the Global Economic Map in the 21st Century (6th edn), London, Sage Publications.

Fontaine Thomson (2007) End of quotas hits African textiles, IMF Survey Magazine, July 5. Giavazzi, F. and Blanchard, O. (2010) Macroeconomics: A European Perspective, Harlow, Financial Times/Prentice Hall.

Greenaway, D. (1994) The Uruguay Round of trade negotiations, Economic Review, 12, November.

Grimwade, N. (1996) Anti-dumping policy after the Uruguay Round, National Institute Economics Review, February, 98-105.

Hanson, D. (2010) Limits to Free Trade: NonTariff Barriers in the European Union, Japan and United States, Cheltenham, Edward Elgar. IMF (1993) World Economic Outlook 1993, Washington DC, International Monetary Fund. Krugman, P. and Obstfeld, M. (2010) International Economics: Theory and Policy, Harlow, Financial Times/Prentice Hall.

Lloyd, P. J. (1992) Regionalisation and world trade, OECD Economic Studies, No. 18, Paris, Organisation for Economic Cooperation and Development.

OECD (2006) Agricultural Policy and Trade Reform: Potential Effects at Global, National and Household Levels, Paris, Organisation for Economic Cooperation and Development. Panagariya, A. (1999) The regionalism debate: an overview, The World Economy, 22(4): 477-511. Primo Braga, C. A., Safadi, R. and Yeats, A. (1994) NAFTA’s Implications for East Asian Exports, Policy Working Paper No. 1351, Washington DC, World Bank.

Prusa, T. J. and Teh, R. (2010) Protection Reduction and Diversion: PTAs and the Incidence of Anti-dumping Disputes, NBER Working Paper No. 16276, Cambridge MA, National Bureau of Economic Research.

Reinert, K. A., Roland-Holst, D. W. and Shiells,

C. R. (1994) A general equilibrium analysis of North American regional integration, in Francois,

J. F. and Shiells, C. R. (eds), Modelling Trade Policy: Applied General Equilibrium Analysis of a North American Free Trade Area, Cambridge, Cambridge University Press.

Schefer, K. N. (2010) Social Regulation in the WTO: Trade Policy and International Legal Development, Cheltenham, Edward Elgar. Smith, F. (2009) Agriculture and the WTO, Cheltenham, Edward Elgar.

Srinivasan, T. N., Whalley, J. and Wooton, I. (1993) Measuring the effects of regionalism on trade and welfare, in Anderson, K. and Blackhurst, R. (eds), Regional Integration, Hemel Hempstead, Harvester Wheatsheaf. Stiglitz, J. (2006) Social justice and global trade, Far Eastern Economic Review, March, 18-22. UNCTAD (2010a) Trade and Development Report 2010: Employment, Globalization and Development, New York and Geneva, United Nations Conference on Trade and Development. UNCTAD (2010b) World Investment Report 2010: Investing in a Low Carbon Economy, New York and Geneva, United Nations Conference on Trade and Development.

UNDP (2010) Human Development Report 2010: The Real Wealth of Nations: Pathways to Human Development, New York, United Nations Development Programme.

Vanston, N. (1993) What price regional integration? OECD Observer, No. 181, 4-7. World Bank (1986) World Development Report 1986, Washington DC.

World Bank (2005) Global Monitoring Report, Washington DC.

World Bank (2010) World Development Report 2010: Development and Climate

Change. Washington DC.

WTO (2008) 10 Benefits of the WTO Trading System, Geneva, World Trade Organization. WTO (2010a) Annual Report, Geneva, World Trade Organization.

WTO (2010b) International Trade Statistics, Geneva, World Trade Organization.

Yannopoulos, G. N. (1990) Foreign direct investment and European direct investment: the evidence from the formative years of the European Community, Journal of Common Market Studies, 23(3): 235-59.