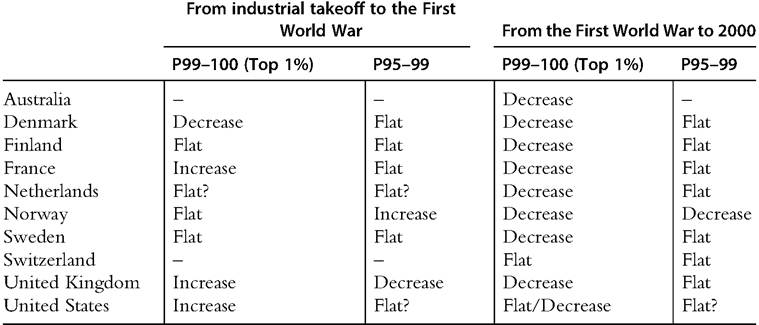

LONG-RUN TRENDS IN WEALTH INEQUALITY

It is fair to say that the majority of research on economic inequality has focused on incomes. Much less attention has been given to the role of wealth, which is unfortunate for a number of reasons.

As a determinant of people’s consumption possibilities, personal wealth is of first-order relevance. The classical Haig-Simons definition of income states that income is what we can consume while keeping our real wealth intact. Wealth can also determine which opportunities individuals have to make investments and pursue different occupations, especially in the presence of credit constraints. The interplay between the distribution of wealth and development is also central to many theories attempting to explain the cross-country differences in long term development.This section presents and discusses the existing research on the long-run evolution of wealth inequality. The ambition is to harmonize the outline with the previous section on the long-run trends in income inequality. We begin by presenting the core methods and data issues concerning how to measure wealth, wealth inequality, and how to tackle the specific challenges associated with studying historical trends. Thereafter we present ten country case studies for which we have sufficiently good data on wealth concentration for at least a century and in some cases from the beginning of each country’s industrialization.

Finally, we bring together the pieces of evidence into cross-country mappings of the trends, searching for common patterns that may help us address the overall questions about the relationship between economic development and inequality.

7.3.1 Data and Measurement

Despite the arguments for studying wealth and its distribution, the empirical literature on wealth inequality is still limited, particularly when it comes to the long-run perspective. Naturally, there are many reasons for this past neglect, but the problem of agreeing on a manageable definition of wealth and then the practical problems associated with measuring it empirically are most likely important.

Sources for studying wealth over time are of different sorts. In their investigation of the analysis of wealth distribution, Davies and Shorrocks (2000) pointed at the five most common sources of wealth data: wealth tax returns, estate tax returns (or probate records), investment income method (using capital income and some assumed or observed net rate of return), household surveys, and journalistic rich list. With respect to investigations of long-run patterns, perhaps the most consistent of these sources is estate records. They have existed for centuries with largely the same basic structure of assets and debts of the deceased individuals. Unfortunately, there are few compilations of estate records in most countries over time, which is why we still lack data on wealth distribution from this source. A few countries have presented tabulated sizes of estate records in relation to estate tax compilations. Wealth tax statistics is another common source, available in a fairly homogenous way in several countries over long periods of time. Here, however, the problems of what components are included in the tax base or how large share of the population that is covered in the statistics are more pressing problems. Surveys, finally, comprise a more recent source for wealth distribution evidence.

Historical evidence on wealth distribution data is primarily based on wealth and estate taxation statistics. These fiscal instruments have been used for centuries and offer consistent source materials. Authorities have often also been interested not only in collecting the revenues but also in calculating the size of each tax base as well as their respective size distribution. Of the historical evidence presented later, series from France, the United Kingdom, and, in part, the United States, all emanate from the estate tax and, specifically, samples of individual estate tax returns. U.S. wealth distribution data from the latter part of the twentieth century and the beginning of the twenty-first century are also available in household surveys.

Wealth distribution data from Denmark, the Netherlands, Norway, and Switzerland are all based on wealth tax statistics, in most cases as tabulated distributions published by each country’s tax authorities. For Finland and Sweden the bulk of the data come from both wealth tax statistics but there are some complementary observations from estate tax returns. For Australia, finally, observations come from estate tax data, wealth surveys, and even journalistic rich lists.7.3.1.1 The Wealth Holding Unit

The concept of wealth owner varies across the empirical studies covered in this chapter depending on the nature of the data source used. When wealth tax-based data are used (as in the Netherlands, Switzerland, and the Nordic countries), the most common unit of observation is households. For the most part, this means tax households where married couples (and their under-aged children) count as one, as do children 18 years or older living at home. Many of the survey-based wealth records from recent decades, however, define households as cost-based households, the major difference being that adult children living at home are now included in the parents’ household. When studying very long time spans, households sometimes also included servants, parents or grandparents, slaves, or unregistered immigrants. Shammas (1993) shows that the U.S. historical wealth concentration is sensitive for the treatment of these different subgroups into the reference tax population.[261] Estate tax data and probate inventories (used in France, the United Kingdom, and the United States) are instead based on (deceased) individuals.[262] [263] Most studies focus on adult individuals, thereby imposing a lower age cutoff normally between 15 and 25 years of age.5

To define wealth holding units consistently matters for the distributional estimates. As was pointed out earlier in the discussion of the distribution of incomes, individual-based data tend to (but must not) give rise to a more unequal wealth distribution than does the household-based data (Atkinson, 2007).

Roine and Waldenstrom (2009) compared shifts in Swedish top wealth shares using household and individual distributions finding no important differences, and Kopczuk and Saez (2004) reached the same conclusions in their analysis of U.S. wealth distribution trends.7.3.1.2 The Concept of Wealth

The definition of personal wealth that is most commonly used in studies of wealth distribution is net wealth, also called net worth or net marketable wealth. Net wealth consists of the sum of all nonhuman real and financial assets less debt. Real (or nonfinancial) assets primarily consist of housing and land, but they may also include durable consumption goods (see further the discussion later), for example, cars, boats, furniture, and also valuables such as antiquities, jewelry, and art. In the distant past, even items such as clothing and other semidurable consumption goods were often inherited (especially among the less wealthy) and may also be covered among the nonfinancial assets. Financial assets are cash, bank deposits, corporate stocks, bonds and other claims, and insurance savings, which today also include some parts of funded pension assets. Debts, finally, are the sum of housing mortgages and loans for consumption, investment, or education.

As already stated, our definition of wealth does not include peoples’ inherent or acquired skills, or human capital. This is a natural implication of the wealth definition set out at the beginning, which focuses on assets that are marketable and thus possible to sell or purchase at a market place.[264] Historically, such market for human wealth has existed, namely in association with slavery. In terms of aggregate wealth the total value of “slave assets” was somewhere between 15% and 30% of total national wealth (Piketty and Zucman, 2014, figure 11; Soltow, 1989, p. 180). According to Soltow (1989, p. 267), slaves were disproportionately held by the wealthy, and the inequality in slave ownership was almost three times as large as the inequality in land and dwellings.

Measuring net wealth is sensitive to the valuation of assets. Ideally assets should be valued at current market prices, net of taxes and transaction costs, the theoretical reason being the possibility to convert wealth to consumption. However, most estimates of historical inequality use data where assets are reported in tax-assessed values rather than in market values. Tax laws are typically designed to strike a balance between the revenue needs of government and tax collectability of tax authorities, and the rules regarding asset coverage or valuation criteria may thus not be aligned with what researchers would ideally like to have. But if the discrepancy across tax and market values is similar across the distribution—and historically we think that this was arguably often the case—the biasing effect of valuation on relative wealth shares should be small. Only a few studies have delved into these questions. Examples are the analyses of inequality trends in the United StateswhereWilliamsonandLindert (1980a,b) and WolffandMarley (1989) investigated whether tax-driven avoidance distorts the use of tax data for distributional analysis (and they generally found that it does not). Atkinson and Harrison (1978) examined how the valuation of taxed assets may influence inequality, for example, looking at life policies (table 4.6) and offshore assets (pp. 161f).[265] Roine and Waldenstrom (2009) studied the effect of valuation by using several alternative estimates of aggregate wealth (based on either tax or market values as well as including items that have not been taxable) and also different assumptions about the distribution of the difference between these alternative reference totals and the baseline specification. They found that there are some differences in the levels of wealth shares over the period, but that the trends in wealth concentration remain unchanged. Altogether, we believe that the comparability of the estimated shares presented in this chapter is good over time.

Some components are especially difficult in the analysis of personal wealth. Although some of them appear in the wealth data in several countries and time periods, their presence is associated with uncertainty concerning both valuation and conceptual adequacy. In the following we discuss three of the most important “problematic assets” and how they are typically treated in the historical sources. In the end, they do not, however, affect the main conclusions about the long-run inequality trends reported later.

(i) Pension and Social Security wealth is a composite term for the net present value of individuals’ entitlements to future private and public payments for pensions and other social outlays. These assets are for the most part not included in the historical inequality estimates. Conceptually, scholars have shown that expectations about future public pensions reduce the incentive to accumulate private wealth (see, e.g., Berg, 1983; Feldstein, 1976; Gale, 1998), and thus a comparison of private wealth across systems with differing public pension coverage may be misleading unless retirement wealth is accounted for. Researchers therefore sometimes add Social Security wealth to the net marketable wealth of households, yielding a concept often called augmented wealth. Studies of the concentration of augmented wealth typically find that it is substantially lower than the concentration of marketable wealth. For example, Wolff (2007) found that the Gini coefficient for the United States in 2001 dropped by a fifth when going from net worth to augmented wealth, and Frick and Grabka (2013) found a similar drop for Germany in 2007. The Inland Revenue in the United Kingdom presented for many years series of the distribution of marketable wealth (Series C) as well as wealth including public and private pension entitlements (Series E), exhibiting Gini coefficients that were about a third lower when including pensions.[266]

However, there are numerous problems associated with defining pension assets, or other “drawing rights” on the Social Security system, as private property, and until questions like those are fully settled we will not see a comprehensive treatment of pension and Social Security wealth alongside net marketable real and financial assets. The main issue is how to judge the fact that, on the one hand, not having the public system would have required an individual to save privately, thus decreasing consumption possibilities, but on the other hand, the “drawing rights” are not marketable wealth and cannot be converted freely into other consumption by the individual.[267]

(ii) Consumer durables are not always included in the wealth data, and when they are their valuation is difficult. First of all, this asset class is typically completely absent from wealth tax returns or administrative tax registers, primarily for evasion reasons. It is thus not part of the bulk of the distributional estimates examined in this chapter. However, insofar as data are based on probates or estate tax returns or household surveys, durables are more likely to be included because of smaller possibilities (and smaller incentives) to evade.[268] Atkinson and Harrison (1978, p. 43) noted that the valuation of consumer goods is difficult, and they often take too low values in estate data. In general, it is actually an open question whether consumer durables should at all be included in the household balance sheet. According to the System of National Account they should not because all consumed goods are assumed to depreciate within 1 year and therefore cannot contribute to any fixed asset formation.[269] However, many durables (e.g., cars, boats, and some electronic equipment) arguably last more than 1 year, and for this reason some countries (such as the United States) do include durable consumer goods in household balance sheets. Historically, consumption goods like china, furniture, and even clothing were important parts of household inventories and were inherited along with other assets. Waldenstrom (2014) estimated the household balance sheet of Swedish households since 1810, finding that durables represented between 10% and 20% of nonfinancial assets throughout the period up until today. Interestingly, durables grew more important in the middle of the twentieth century, which is related to the growth in earnings potential of increasingly educated middle-class households (Roine and Waldenstroom, 2009).

(iii) Foreign wealth holdings have historically been sizeable in many countries, especially colonial powers such as France and the United Kingdom. In a recent investigation, Piketty and Zucman (2014, table A27) found that net foreign wealth represented between a 10th and a quarter of total national wealth in these two countries from the middle of the nineteenth century up to World War I. At the individual level, information about foreign assets such as foreign government stock and bonds and other real estate is most likely completely absent from domestic wealth tax returns, but should in principle be more visible in estate data. As noted by Atkinson and Harrison (1978, p. 161), however, overseas real estate was not taxable before 1962 and therefore not included in wealth inequality estimations before this year. In an attempt to gauge the importance of the acclaimed tax-driven capital flight from Sweden during the period from the 1970s to the 2000s, Roine and Waldenstroom (2009) used residual flows in the Balance of

Payments and Financial Accounts to estimate the aggregate offshore wealth held by residents. Assuming that this wealth was primarily held by the richest residents, the authors found that the top percentile wealth share rose from about 20% in the 2000s to over 30%, depending on assumptions about interest rates on foreign capital and whether to include the closely held corporations of superrich Swedes.[270] Also, without explicit reference to distributional aspects, Lane and Milesi-Feretti (2001, 2007) constructed estimates of the external wealth of nations since 1970. However, going further back we know very little about the role of offshore wealth in historical eras and can therefore not offer a consistent interpretation of their role for long-run inequality trends.

7.3.1.3 Measuring Historical Wealth Inequality

When we estimate the concentration of wealth, we use a similar methodology as when calculating top income shares. That is, we estimate the wealth share held by Variousfractions of the population by dividing the observed top wealth holdings for specific groups (fractiles) in the top by a reference total for all personal wealth in the economy. Just as in the case of historical income distribution data, the historical wealth distribution data often come in the form of tabulated distributions of grouped data. This means that we observe wealth holders and their net wealth divided into different wealth size classes. To get the exact wealth share accruing to certain fractiles in the top, such as the top percentile or the top decile, we use the Pareto interpolation technique described previously.

Using top wealth shares as measure of inequality has several advantages for our purposes.[271] Most historical sources of wealth data come from wealth and estate tax returns, and the group most consistently represented in these tax listings throughout history is the rich (i.e., where the wealth was), which makes them the most homogenously observed group over time. Moreover, wealth distributions are heavily skewed—much more so than income distributions—and top wealth holders have often held the vast majority of all personal wealth; between 70% and 90% before the Second World War and between 50% and 70% thereafter. Studying the top and its wealth therefore means that almost all personal wealth is being studied. Finally, most of the historical wealth inequality estimates constructed by past researchers come in the form of top wealth shares, especially as top wealth percentiles, and this measure is therefore the most appropriate to use for our purposes.

A specific challenge associated with estimating top wealth shares is the measuring of the reference total of net wealth ofthe whole population. Wealth tax data typically only cover the top households that have paid wealth tax, and researchers must therefore limit their observations to years when attempts to measure the corresponding total for the whole population have been made, for example, in censuses or special public investigations. In the case of Sweden, for example, there are years for which tabulated top wealth data exists, but there is no reliable information about the reference total wealth to be found. Estate data also have problems with constructing population measures but they are of a slightly different kind. Researchers here typically try to collect a sample of estates that is representative for the whole population, which thereby enables them to compute the relevant inequality measures using only the sample at hand. However, most of the time the estate data sources are themselves not fully representative for the population, mostly lacking information about people with low levels of personal wealth.[272]

The different wealth data sources also display the wealth distribution for different entities. Whereas wealth tax data and surveys reflect the distribution of the living population, estate tax data and probate inventories reflect the distribution of the deceased. Because those people who die during a year are not a representative sample of the living population (e.g., because the old are heavily overrepresented), these two distributions are not immediately comparable. The usual procedure used by researchers to make them comparable is by applying so-called mortality multipliers, which are inverse mortality rates for different age, sex, or social status groups.[273] In this way, the distribution of estates can be transformed so as to reflect the wealth distribution among the living population.

7.3.1.4 TaxAvoidanceandEvasion

As already noted, using data from administrative tax-based statistics to compute measures of wealth distribution gives rise to some problems relating to tax evasion and avoidance. But, as in the case of the income distribution, the extent to which such activities lead to errors in estimated wealth shares is, however, not clear. If noncompliance and tax planning is equally prevalent in all parts of the distribution—it may, of course, take very different forms—this affects the reported wealth levels but not the shares. The same goes for comparisons over time and across countries (see Section 7.2.1.5 for more on this). Unfortunately there is little systematic evidence on this. There are overviews, mainly concerned with personal income taxes, suggesting that, although avoidance and evasion activities are important in size, there are no clear results on the incidence of overall opportunities or on these activities becoming more or less important over time.[274]

Moreover, it is not clear whether to expect more or less avoidance and evasion in countries with higher tax rates. As the incentives to engage in avoidance and evasion become higher when taxes increase, so do the incentives for tax authorities to improve their control.[275] Regarding wealth and estate taxes it may seem plausible to think that estate tax data are more reliable because it is typically in the interest of the heirs to formally establish correct valuations of the estate.[276] At the same time tax planning aimed at avoiding the estate tax is an important industry in the United States and elsewhere. This may affect the reliability of the data. For wealth, tax data problems of underreporting are likely to be similar to those for income data, with items that are double reported being well captured, whereas other items are more difficult.

Finally, the use of tax havens may be a problem, and as we discussed earlier there are indications that substantial amounts have been hidden over the past decades (see for example, Johannessen and Zucman, 2014, and references therein). Given the large fixed costs related to advanced tax planning, it is likely that such activities are limited to the very top of the distribution. If this has become more important over the past decades— something that seems likely—then estimates of wealth concentration for recent periods may understate wealth holdings in the very top and not be directly comparable with estimates produced for earlier years in this century, in particular top wealth shares may be underestimated for recent decades.

7.3.2 Evidence on Long-Run Trends in Wealth Inequality

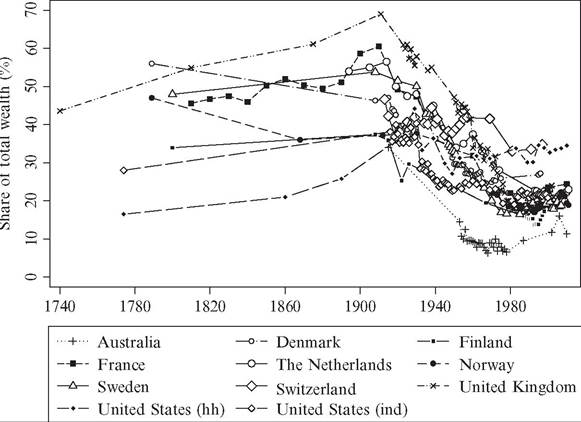

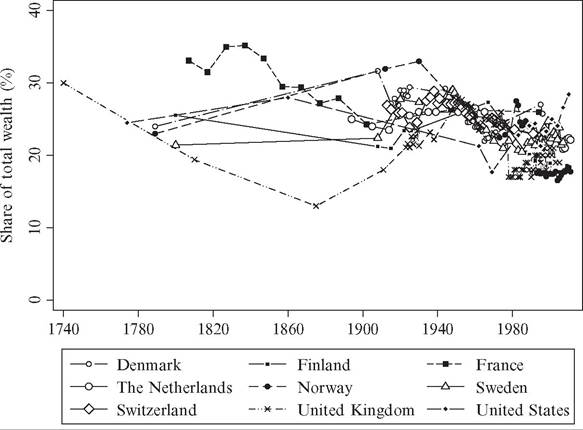

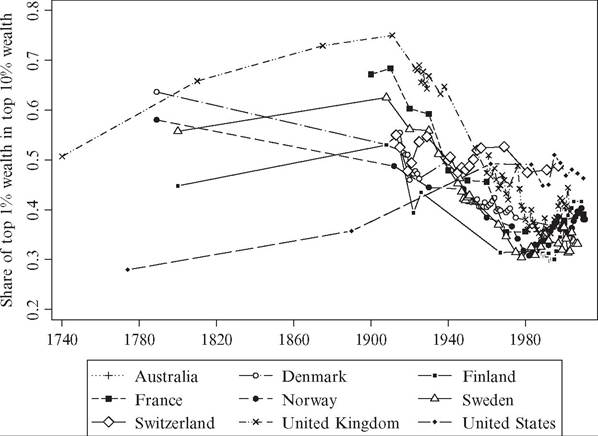

In this section we present evidence on the evolution of wealth inequality in 10 Western countries. The length and detail of the series vary but in most cases the first observations are from around 1800 and with relatively frequent observations throughout the whole of the twentieth century. The relatively small number of countries for which we have data allows us to delve a little deeper into each country case, examining the specificities associated with national histories as well as the structure of historical wealth distribution evidence. After going through the country cases, we compile the series and study to what extent there are common patterns over time. Note that we focus on the twentieth and twenty-first centuries in the country-specific figures in order to ease inspection of the trends in this era, whereas in the figures compiling several countries (Figures 7.19—7.21) we show the full set of observations stretching back to the nineteenth and eighteenth centuries.[277]

7.3.2.1 Country-Specific Evidence

7.3.2.1.1 Australia

A recent investigation of Australian wealth concentration since the beginning of the twentieth century is the one by Katic and Leigh (2013). The authors estimate top wealth shares using three different sources: estate tax returns, household surveys, and journalistic rich lists. The main emphasis is put on the first two, but the very recent trends can also be studied by putting the rich lists into context.

The earliest observation comes from a war wealth survey conducted in 1915 by the Commonwealth Bureau of Census and Statistics. From the 1950s up until the 1970s, tabulated estate tax returns were collected and adjusted by using inverse mortality multipliers adjusted for age, sex, and social status. From the 1980s onward, the authors again used wealth surveys, conducted by different entities, but complemented them by annual observations of wealth share of the superrich Australians published in the Australian magazine Business Review Weekly.

A common theme in all these sources is that they are not extensive in terms of coverage of wealth holders. With a few exceptions, only the very richest citizens are covered, and for this reason the only long-run time series coming out of the historical evidence are the wealth share of the top 1 and top 0.5 percentiles.

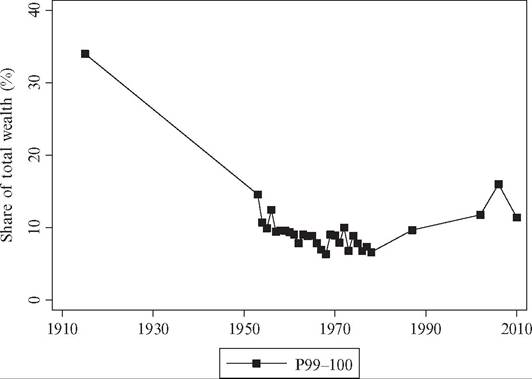

Figure 7.9 shows the trend in the Australian top wealth percentile share between 1915 and 2008. The share falls from almost 35% of total wealth during the First World War down to less than 15% in the early 1950s. Due to the lack of observations in between these dates, we cannot tell whether the fall came as a consequence of the immediate post-WWI turmoil, the crisis impact during the GreatDepression of the 1930s, or the dramatic events during the Second World War and its aftermath. From the 1950s onward, the top percentile share has hovered at around a level of 10-15% of total wealth. Internationally, this is a very low wealth share, actually the lowest of all countries covered in this chapter. At this point, the reasons for the low Australian share have not been studied in detail.

7.3.2.1.2 Denmark

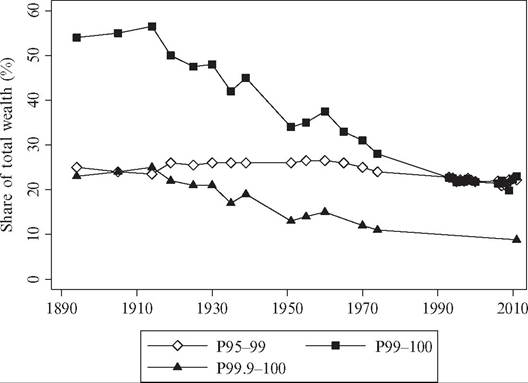

For Denmark, historical wealth concentration data exists from as early as 1789 and then more frequently during the twentieth century. The earliest observation comes from a comprehensive national wealth tax assessment in 1789, from which Soltow (1981a-c) collected a large individual sample of the gross wealth of households.[278] The next observation, however, comes over a century later at the time of the introduction of the modern

Figure 7.9 Wealth concentration in Australia, 1915-2010. Source: See the Appendix for details about sources and data.

wealth tax. For 1908-1925, Zeuthen (1928) lists tabulated wealth distributions (number of households and their wealth sums in different wealth size classes) for Danish households, adjusted to include those households with no taxable wealth. Similar tabulated wealth tax-based data are published in Bjerke (1956) for 1939, 1944, and 1949 and in various official statistical publications of Statistics Denmark for a few years thereafter until the wealth tax was abolished in 1997.[279]

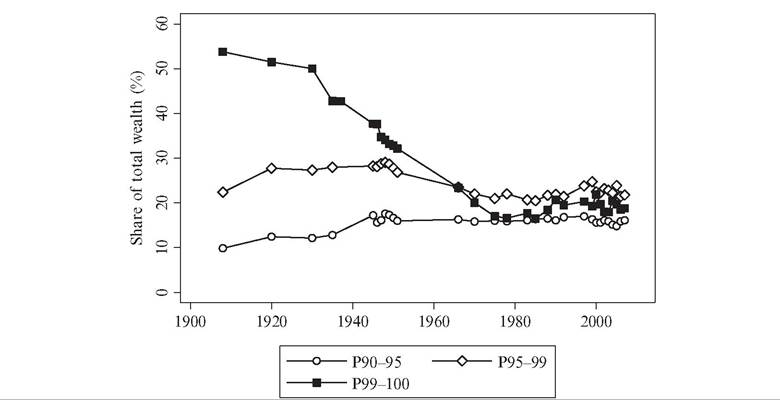

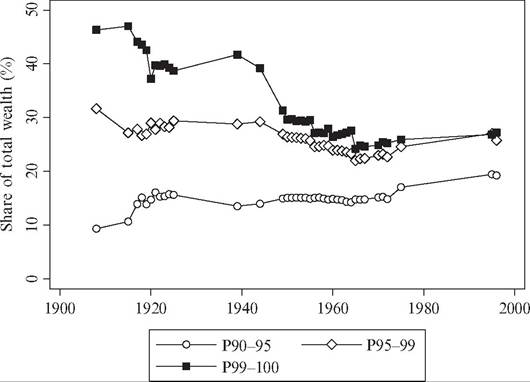

Figure 7.10 shows the wealth shares of groups within the top decile between 1908 and 1996, while Figures 7.19 and 7.20 show the trends back to 1789. The lowest four percentiles (P90-95) exhibit a flat trend up to 1908 and thereafter double their share from 10% to 20% over the twentieth century. The next four percentiles (P95-99) lie constant between 25% and 30% of total wealth over the entire period, whereas the top percentile (P99-100) decreases significantly over the entire period, with particularly marked decreases after the two world wars. When looking at the very top of the distribution, the top 0.1 percentile (P99.9-100), there is no decrease at all up to 1915, but instead there is a dramatic drop by almost two-thirds of the wealth share between 1915 and 1925. Overall, the Danish wealth concentration decreased over the course of industrialization, and this continued throughout the twentieth century, although the development was not uniform at all times and across all groups.

Figure 7.10 Wealth concentration in Denmark, 1908-1996. Source: See the Appendix for details about sources and data.

One way to understand the wealth compression of the Danish industrialization is to compare the identities of the Danish top wealth holders before and after the late nineteenth century. The dominant groups in the top of the wealth distribution in 1789 were owners oflarge agricultural estates. Soltow (1981a-c, p. 126) cited a historical source saying that “some 300 Danish landlords owned about 90 percent of the Danish soil.” By contrast, in 1925, the group with the largest private fortunes was the brokers (Veksellerere) although landlords (Godsejere, Proprietarerog Storforpagterere) were still wealthy, both groups having more than 50 times larger average wealth than the country average.[280]

The drops in top wealth shares after the two world wars were partly associated with the sharply progressive wartime wealth taxes.[281] According to Bjerke (1956, p. 140), however, the fall after the Second World War was also largely due to new routines in the collection and valuation of wealth information of the tax authorities, which in particular made middleclass wealth more visible. Toward the end of the century, the wealth concentration continued declining up to the 1980s, largely due to increased share of the relatively equally distributed house-ownership in the total portfolio (Lavindkomstkommissionen, 1979, Chapter 5), but thereafter started to increase up to the mid-1990s.

7.3.2.1.3 Finland

Finland is another Nordic country for which wealth distribution data exist since the agrarian era and during most of the twentieth century. The country’s industrialization came relatively late, in the interwar period, and even around the Second World War Finland was a predominantly agrarian economy focusing on forest industry and smallscale agriculture. Politically Finland was part of Sweden up until 1809, after which it came under Russian rule until 1917 when Finland ultimately gained independence (Eloranta et al., 2006).

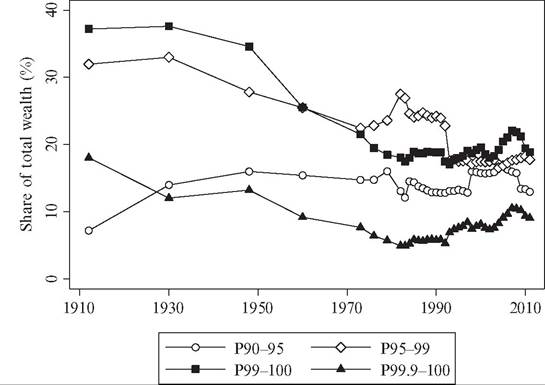

Our estimates of the Finnish historical wealth distribution are essentially based on wealth tax statistics.[282] The earliest known observation of wealth distribution in Finland is 1800, coming from a wealth tax assessment levied in Sweden and Finland. Jutikkala (1953) and Soltow (1980) examined this assessment collecting a representative sample of the gross wealth of almost 2000 male household heads. The taxed households represented about one-third of the population, whereas the other two-thirds were exempt because they lacked a sufficient amount of personal taxable wealth. The next set of estimates comes from estate data in 1907-1909, 1914, and 1915 compiled and published by Statistics Finland.[283] We compute top wealth shares of the deceased but adjust these with respect to the likely difference between top wealth shares of the deceased and living populations using observed differentials in Sweden around the same time. [284] For the early twentieth century, we use Soltow’s (1980) estimates from wealth tax assessments in 1922, 1926, and 1967. All these samples include adjustments for the share of the population without wealth on which no wealth tax was levied. Finally, we have wealth tax tabulations for the period 1987-2005 using net marketable wealth data retrieved directly from Statistics Finland.[285]

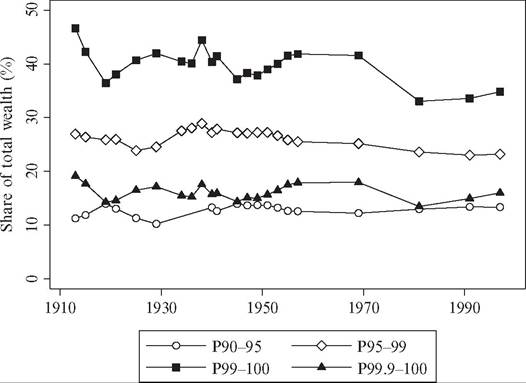

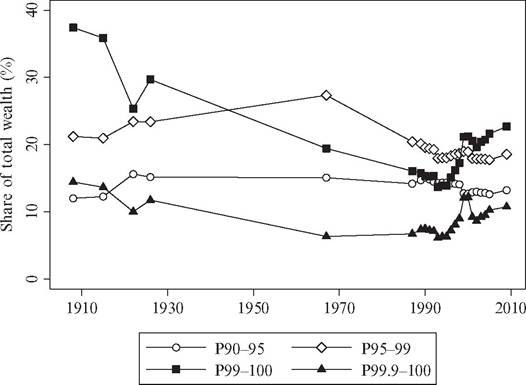

Figure 7.11 presents the evolution of wealth concentration in Finland from 1908 up to 2005, and Figures 7.19 and 7.20 show the trends back to 1800. The top decile held 46% of domestic net wealth in 1800, and its share peaked at 70% in 1909. Over the period the Finnish top percentile share exhibits an inverse-U shape, setting out at a relatively low share in 1800, which was doubled a century later in the years preceding the First World

Figure 7.11 Wealth concentration in Finland, 1908-2009. Source: See the Appendix for details about sources and data.

War. The 1920s saw a strong reduction in the top percentile share, possibly due to the civil war taking place at this time. Later on during the twentieth century, the top percentile’s share decreased further, reaching a global low in around 1990 when its share was less than 14% of total personal wealth. However, after this Finland experienced the IT-boom, led by the immense success of mobile phone producer Nokia, and the top percentile share increased swiftly during the 1990s and 2000s, reaching a level of 22% in 2005 (Eloranta et al., 2006). As for the rest of the top decile, the Finnish pattern is similar to that of most other countries studied here. The next four percentiles (P95-99) also experienced an inverse-U pattern, but peaked later, in the 1960s, after which its share started to decrease. The bottom half of the top decile hovered around 10-15% of total wealth.

Overall, the historical wealth concentration in Finland follows a pattern that looks very much like an inverse-U. The share of total wealth held by the rich (in the top percentile) increased during the nineteenth century and decreased during the twentieth century. The upper middle class (the rest of the top decile), however, did not change their relative position much during the two centuries covered. Also notable is the relatively low level of wealth concentration in Finland, especially in the year 1800 but also during the twentieth century.

7.3.2.1.4 France

The long-run evolution of French wealth inequality is particularly interesting to study given France’s important role for Europe’s economic and political development. Piketty et al. (2006), and later adjusted by Piketty (2014), presented new data on wealth concentration for Paris and France over almost 200 years from the Napoleonic era up to today. No previous study on any country has produced such long homogenous time series, offering complete coverage of wealth inequality overindustrialization. The French wealth data comes from estate sizes collected in relation to an estate tax established in 1791 and maintained for more than two centuries. For every 10th year during 1807-1902, the authors manually collected all estate tax returns recorded in the city of Paris—Paris was chosen both for practical reasons but also because it hosted a dispro- portionally large share of the wealthy in France. Using summary statistics on the national level for the estate tax returns, the top Paris wealth shares were “extrapolated” to the national level. For the post-1902 period, tabulated estate size distributions published by French tax authorities were used.

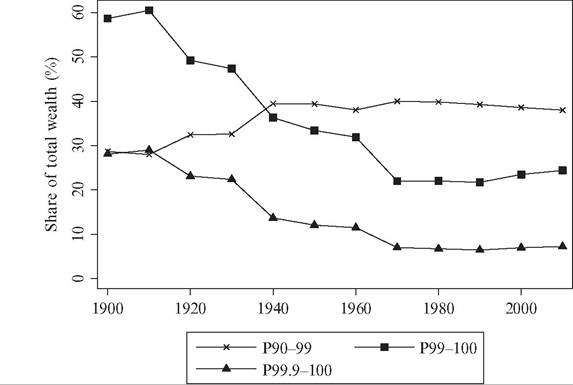

Figure 7.12 shows the evolution of the wealth shares for some fractiles within the top wealth decile in France since 1900, while Figures 7.19 and 7.20 show the trends beginning in the early nineteenth century. The estimates are from the population of deceased, that is, directly from the estate tax returns, but comparisons with the equivalent wealth shares for the distribution of the living population (computed using estate multipliers) reveal practically identical trends and levels.[286] The figures show that wealth

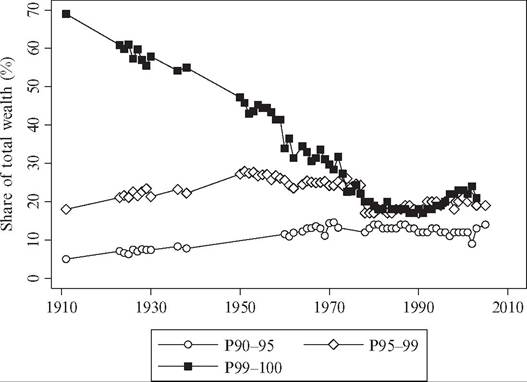

Figure 7.12 Wealth concentration in France, 1900-2010. Source: See the Appendix for details about sources and data.

concentration increased significantly for the top 1 and 0.1 percentiles over the nineteenth century, first slowly up to the 1870s then more quickly until its peak at the eve of the First World War. By contrast, the two lower groups in the top decile are much less volatile during the period. The bottom half (P90-95) held about 9% of total wealth until the First World War when its share started to increase slowly until it had doubled by the 1980s. The next 4% (P95-99) stayed put on a level around 27% of total wealth throughout the period. These patterns suggest that the French industrialization, which took off around midcentury, greatly affected personal wealth. It did so already after a couple of decades, but only in the absolute top. This conclusion is further supported by two other observations. First, the composition of top wealth went from being dominated by real estate assets (mainly land and palaces) in the first half of the century to being dominated by financial assets (cash, stocks, and bonds), which were supposedly held by successful industrialists and their financiers. Second, over the same period the share of aristocrats among top wealth holders decreased from about 40% to about 10%.[287] [288] From the First World War to the end of the Second World War, top wealth shares declined sharply, which according to Piketty (2003) is directly linked to the shocks to top capital holdings that inflation, bankruptcies, and destructions meant. The postwar era was quieter with regard to changes in the wealth concentration, although its decline continued most likely in relation to the increase of progressive taxation (Piketty et al., 2006).

7.3.2.1.4 TheNetherlands

The Netherlands represents and interesting point of reference to the analysis of long-run trends in wealth inequality among Western economies. Although the Netherlands did not industrialize in the traditional sense until the middle of the nineteenth century, its economy was already developed due to its role in the expansion of global trade that started already in the sixteenth century. According to van Zanden (1998b), this may explain the apparent lack of increase in inequality following the Industrial Revolution. Although inequality grew during the preindustrial era due to high growth rates but stagnant real incomes, industrialization did not only boost fortunes of the wealthy but there was also an increased demand for all kinds of labor, skilled as well as unskilled.

The previous literature on historical wealth inequality in the Netherlands is relatively rich. Soltow (1998) and Vermaas et al. (1998) present a series of estimates of inherited wealth and housing inequality in different Dutch regions from the beginning of the nineteenth century. Unfortunately, defining a trend over the nineteenth century appears to be difficult. The only comparable information between 1808, 1880, and 1908 comes from inheritance tax records that cover inheritances to distant heirs, that is, not spouses and children. The data indicates a slight increase in inequality.

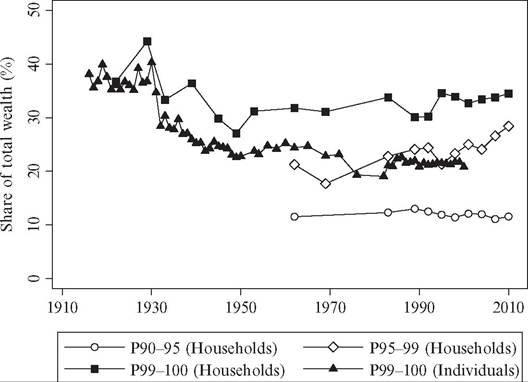

The most comprehensive longitudinal data are offered by the wealth tax statistics, which allow for an estimation of top wealth shares since 1894. The primary source of these observations is Wilterdink (1984), which presented a detailed account of the top vintile and groups within it for selected years between 1894 and 1974. The estimates stem from wealth tax records, showing the distribution among wealth tax units (mainly individuals), whereas the recent wealth survey data show the distribution among households. For the most recent years, Statistics Netherlands has compiled wealth-tax based distributions for the periods 1993-2000 and 2006-2011.[289]

Figure 7.13 shows the top wealth shares of the Netherlands from this year up to 2011. Wealth concentration was a high and stable around the turn of the century 1900. Thereafter the top percentile wealth share started decreasing. Both Wilterdink (1984) and van Zanden (1998a) highlighted the role of the geopolitical events, and these are clearly seen in the falls in top percentile shares during the two world wars and the depression of the 1930s. However, the researchers also emphasized the role of governmental redistribution, in particular the imposition of heavy wealth taxes after 1946 to finance the reconstruction after the war.

Figure 7.13 Wealth concentration in the Netherlands, 1894-2011. Sources: See the Appendix for details about sources and data.

7.3.2.1.5 Norway

Data on Norwegian wealth concentration come mostly from various kinds of wealth taxation. Overall, these data are perhaps the most uncertain presented in the entire chapter, and the estimates of top wealth shares presented in this chapter must therefore be interpreted cautiously. The first observation is from 1789, when the wealth tax assessment that also was launched in Denmark came into place (the two countries were in a political union at this time). As in Denmark, both real and financial assets were subject to taxation, including land, houses or farms, factories, livestock, mills, shop inventories, and financial instruments. Debts were not deducted, and hence the wealth concept is gross wealth.[290] Our second observation is from 1868, when the Norwegian government launched a national wealth tax assessment. Mohn (1873) presents totals for wealth and households and a tabulation of the wealth held by the top 0.27% (P99.73-100) of all households, including a detailed listing of the 15 overall largest fortunes.[291] For 1912, we use wealth tax returns from the taxation of 1913-1914 (exempting financial wealth) which are presented in tabulated form in Statistics Norway (1915b).[292] Similarly, for 1930 we use tabulated wealth distributions (number of wealth holders in wealth classes along with totals for wealth and tax units) presented in Statistics Norway (1934).

From 1948 onward, we use the tabulation of wealth holders and wealth sums in classes of net wealth published annually in the Statistical Yearbook of Statistics Norway. In the early 1980s the wealth statistics started being reporting for individual taxpayers instead of, as before, for households. To keep our series as consistent as possible, we attempted to convert the post-1982 observations from reflecting the individual distribution to reflect the household distribution using a listing of both types by Statistics Norway for the year of 1979.[293]

For the period since 1993, we use tabulated wealth distributions published on the Statistics Norway’s Web site.[294] Somewhat ironically, the uncertainty about these data is perhaps largest because both asset coverage and valuations are highly problematic. For example, tax-assessed values of housing are heavily discounted and represent on average no more than a fifth of their true market value, with the discount being larger for more expensive dwellings (Epland and Kirkeberg, 2012). For this reason, household net tax- assessed wealth is negative for practically every Norwegian household. Furthermore, it is not obvious that the distributional trends in tax-assessed net assets are the same as those in market-valued assets if there are also trends in market-to-tax values of dwellings.

To shed some additional light on these matters, we refer to what we see as the most reliable estimate of the Norwegian net wealth distribution presented by Epland and Kirkeberg (2012). This investigation brings together a rich microdata material for 2009, carefully estimates market-valued assets and liabilities, and computes wealth inequality estimates. The study finds that the top wealth decile held about 53% and the top percentile about 21% of all net wealth (Epland and Kirkeberg, 2012, table 8). Interestingly, although the aforementioned tax-based tabulations of net wealth made no sense, the distribution of gross wealth seems less off the chart, producing for 2009 top shares of 54% for the top decile and 26% for the top percentile. For this reason, we use the time series pattern offered by the tabulated gross wealth of Statistics Norway and scale down the wealth shares to match the Epland-Kirkeberg reference level of2009.

Altogether, the Norwegian long-run wealth concentration estimates are thus highly problematic in several respects. Looking at the overall trend in wealth concentration, however, it appears to be relatively robust to variations in some of our assumptions, and it does not deviate much from the long-run inequality trends observed in other countries.

Figure 7.14 presents the trends in Norwegian wealth concentration between 1912 and 2002, while the trends back to 1789 are shown in Figures 7.19 and 7.20. The top wealth decile is broken up into the bottom 5% (P90-95) of wealth holders, the next 4% (P95-99), the top percentile, as well as the top 0.1 percentile. Norway’s top wealth holders experienced quite different trends in their relative positions over the period. As for the bottom 5% of the top decile, its share decreases between 1789 and 1912 and then jumps up sharply between 1912 and 1930 to land on a fairly stable (though slowly declining) level thereafter. The wealth share of the next 4% exhibits an inverse-U shaped pattern, increasing sometime in the nineteenth century (we do not know exactly when due

Figure 7.14 Wealth concentration in Norway, 1912-2011. Sources: See the Appendix for details about sources and data.

to a lack of data), peaking in 1930 and then declining almost monotonically over the rest of the twentieth century. Finally, the share of the top wealth percentile decreases significantly between 1789 and 1868, both years predating Norway’s industrialization period. The share then goes up to slightly in 1912 only to start decreasing again. The most dramatic falls occur in the postwar period, with the top percentile dropping from 34.6% to 17.5% during 1948—1983 and the top 0.1 percentile going from 13.2% to 5.7% over the same period. In the 1990s, there is a rapid recovery, which may be related to the oil fortunes being built up in recent times and to the rise in world stock markets prices that also produced a rise in the top income shares over this period (Aaberge and Atkinson, 2010). The sizeable increase between 1997 and 1998 can also be explained by a change in the Norwegian tax laws specifying an increase in the assessed values of corporate stock on personal tax returns.[295]

Despite the somewhat disparate trends among Norway’s top wealth holders and underlying problems with the Norwegian wealth tax-based data series, the evidence presented in Figures 7.14, 7.19, and 7.20 nonetheless corresponds relatively well with what one could expect given the economic and political history of Norway over this period. The Norwegian economy was badly hit by the economic crisis after the Napoleonic wars, and there was a shift in the political power from the great landlords and landed nobility to a class of civil servants.[296] When merchant shipping expanded in the world after 1850, Norwegian shipowners and manufacturers experienced a tremendous economic boost. When looking at the average wealth of various occupations in 1868 listed in Mohn (1873: 24), the four richest groups were manufacturers (having 160 times the country average household wealth), merchants (124 times), shipowners (96 times), and civil servants (87 times). Half a century later, in 1930, a similar comparison between the wealth of top occupations groups and the country average was made (Statistics Norway, 1934, p. 6), and only shipowners had kept the distance to the rest of the population (having 119 times the country average wealth), whereas merchants (22 times) and manufacturers (19 times) had lost wealth relative to the average.

87

7.3.2.1.6 Sweden