Firms and the Creation of Vacancies

The creation of a new job occurs when a prospective employer and a prospective employee agree to an employment contract. Of course, before this happens, the potential employer has to create a vacancy and search for an employee, and the prospective employee has to be unemployed and looking for a new job.

All this involves time and costs and is described by the matching function.Assume that the instantaneous value of the product of a job is constant and equal to p > 0. The instantaneous cost of a vacant post to a prospective employer is equal to pc, where 0 < c < 1. During the search period, the employer faces a probability q(θ) of finding a a suitable employee, which is independent of the employer’s actions.

The number of vacancies is endogenous and is determined by profit maximization. Any firm can create a vacancy and search for employees. Profit maximization with free entry means that the expected profit from the marginal vacancy should be equal to zero. Otherwise, firms would continue to create vacancies.

18.3.1 The Present Value of Net Expected Profits from an Existing Job

Denote by J the present value of net expected profits from an existing job. The instantaneous gross profit from a job for a firm is equal to the difference p−w, where w is the real wage. However, at every instant, there is an exogenous constant probability λ of the job ending and the firm losing the present value of net expected profits from the job. Thus, the instantaneous expected net profit from a job is equal to

Assuming a perfect capital market and an infinite horizon, the present value of this expected net profit is equal to

where r is the real interest rate, which is assumed exogenous and constant.5

From (18.10), the present value J of a job for the employer must satisfy the Bellman equation

Thus, from (18.11), the instantaneous net opportunity cost of a job rJ must be equal to the instantaneous net expected profit from the job, which implies the condition

For a positive net present value of expected profits from an existing job, the real wage will be less than productivity, both because of the interest costs of maintaining a job and the positive probability of termination of the job.

Thus, the wedge between productivity and the real wage must reflect these capital and insurance costs.18.3.2 The Present Value of Net Expected Profits from a Vacancy and the Creation of Vacancies

Denote by V the present value of expected profits from a job vacancy. The instantaneous net expected profit from a vacancy is equal to the probability of filling the vacancy, and earning the difference between the present value of a job and the present value of the vacancy, minus the instantaneous maintenance cost of the vacancy pc:

Assuming a perfect capital market and an infinite time horizon, the present value of expected net profits from a vacancy V is defined by

Thus, from (18.14), V must satisfy the Bellman equation

A vacancy is an asset for the firm. In a perfect capital market, the instantaneous expected net yield of this asset, q(J − V) − pc, will be equal to its expected opportunity cost, which is equal to rV.

18.3.3 Free Entry and the Job Creation Condition

In equilibrium with free creation of vacancies (free entry), all profit opportunities by creating new vacancies will be exploited, and the expected profits from the creation of an additional vacancy will be equal to zero. So in equilibrium with free entry, V = 0. Thus from (18.15), we have that

which is an important prediction of this model. In equilibrium with free entry, the present value of a job will be equal to the expected cost of hiring an employee. This is equal to the instantaneous cost pc of maintaining a vacancy times the expected duration of the vacancy (which is 1/q(θ)).

Thus, competition for the creation of vacancies and free entry reduces the present value of profits from a job to the level of the expected cost of hiring a worker.Equations (18.16) and (18.12) imply that the marginal job must satisfy

Equation (18.17) is the second key equation of this model and can be called the job creation condition. The firm will only hire a worker and create a new job if the real wage is smaller than or equal to the productivity of the worker, minus the marginal hiring cost, which is defined as

The marginal hiring cost is equal to the gross opportunity cost of maintaining a job. It is the opportunity cost of the expected net present value of profits from the job, which, because of free entry, is equal to the expected cost of hiring an employee. The higher is labor market tightness θ, and the higher is c, the higher will be the marginal hiring cost, because the expected duration and the cost of a vacancy will be greater.

For this model, (18.17) corresponds to the usual condition for hiring in competitive models without hiring costs, which is none other than the real wage must be equal to (marginal) productivity. One can confirm this by setting the cost c of maintaining a vacancy equal to zero. In this case, the real wage is equal to average and marginal productivity p. In the general case, where maintaining a vacancy is costly, the firm will only hire a new worker if the marginal cost of maintaining the vacancy is recouped.

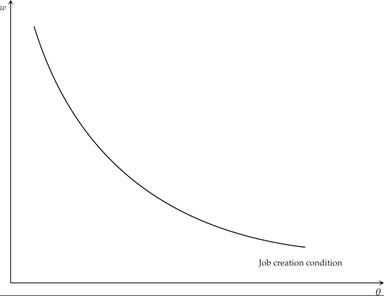

The job creation condition implies a negative relation between labor market tightness and the real wage. The higher is labor market tightness, the higher will be the expected duration of a vacancy and the marginal cost of maintaining a vacancy. Thus, the real wage that the firm would be prepared to pay, relative to productivity, will be lower. The job creation condition is depicted in figure 18.2. It is negatively sloped and convex to the origin because of the properties of the matching function.

Figure 18.2 The job creation condition.

18.4