Fiscal Policy Shocks in the Classical Model

Discuss the effects of fiscal policy shocks in the classical model.

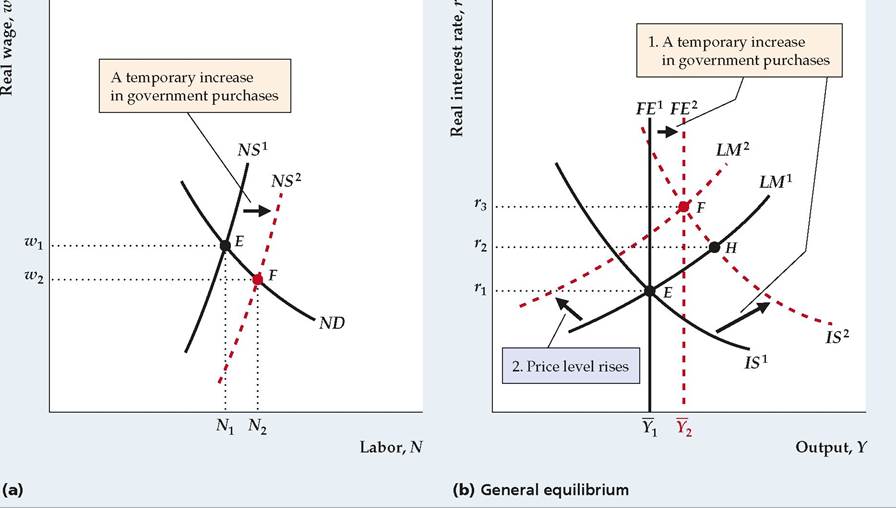

Let's consider what happens when the government purchases more goods, as it would, for example, when the country is at war.

(Think of the increase in government purchases as temporary. Analytical Problem 2 at the end of the chapter asks you to work out what happens if the increase in government purchases is permanent.)Figure 10.4 illustrates the effects of an increase in government purchases in the classical IS-LM model. Before the fiscal policy change, the economy's general equilibrium is represented by point E in both (a) and (b). To follow what happens after purchases rise, we start with the labor market in Fig. 10.4(a). The change in fiscal policy doesn't affect the production function or the marginal product of labor (the MPN curve), so the labor demand curve doesn't shift.

FiGUREJO. 4

Effects of a temporary increase in government purchases

Initial equilibrium is at point E in both (a) and (b).

(a) A temporary increase in government purchases raises workers' current or future taxes. Because workers feel poorer, they supply more labor and the labor supply curve shifts to the right, from NS1 to NS2. The shift in the labor supply curve reduces the real wage and increases employment, as indicated by point F.

(b) The increase in employment raises full-employment output and shifts the FE line to the right, from FE1 to FE2. The increase in government purchases also reduces desired national saving and shifts the IS curve up and to the right, from IS1 to IS2. Because the intersection of IS2 and LM1 is to the right of FE2, the aggregate quantity of output demanded is higher than the full-employment level of output, Y2, so the price level rises.

The rise in the price level reduces the real money supply and shifts the LM curve up and to the left, from LM1 to LM2, until the new general equilibrium is reached at point F. The effect of the increase in government purchases is to increase output, the real interest rate, and the price level.However, classical economists argue that an increase in government purchases will affect labor supply by reducing workers' wealth. People are made less wealthy because, if the government increases the amount of the nation's output that it takes for military purposes, less output will be left for private consumption and investment. This negative impact of increased government purchases on private wealth is most obvious if the government pays for its increased military spending by raising current taxes.[174] However, even if the government doesn't raise current taxes to pay for the extra military spending and borrows the funds it needs, taxes will still have to be raised in the future to pay the principal and interest on this extra government borrowing. So, whether or not taxes are currently raised, under the classical assumption that output is always at its full-employment level, an increase in government military spending effectively makes people poorer.

In Chapter 3 we showed that a decrease in wealth increases labor supply because someone who is poorer can afford less leisure. Thus according to the classical analysis, an increase in government purchases—which makes people financially worse off—should lead to an increase in aggregate labor supply.[175] The increase in government purchases causes the labor supply curve to shift to the right, from NS1 to NS2 in Fig. 10.4(a). Following the shift of the labor supply curve, the equilibrium in the labor market shifts from point E to point F, with employment increasing and the real wage decreasing.[176]

The effects of the increase in government purchases in the classical IS-LM framework are shown in Fig.

10.4(b). First, note that, because equilibrium employment increases, full-employment output, Y, also increases. Thus the FE line shifts to the right, from FE1 to FE2.In addition to shifting the FE line to the right, the fiscal policy change shifts the IS curve. Recall that, at any level of output, a temporary increase in government purchases reduces desired national saving and raises the real interest rate that clears the goods market. Thus the IS curve shifts up and to the right, from IS1 to IS2. (See also Summary table 12 in Chapter 9.) The LM curve isn't directly affected by the change in fiscal policy.

The new IS curve, IS2, the initial LM curve, LM1, and the new FE line, FE2, have no common point of intersection. For general equilibrium to be restored, prices must adjust, shifting the LM curve until it passes through the intersection of IS2 and FE2 (point F). Will prices rise or fall? The answer to this question is ambiguous because the fiscal policy change has increased both the aggregate demand for goods (by reducing desired saving and shifting the IS curve up and to the right) and the full-employment level of output (by increasing labor supply and shifting the FE line to the right). If we assume that the effect on labor supply and full-employment output of the increase in government purchases isn't too large (probably a reasonable assumption), after the fiscal policy change the

aggregate quantity of goods demanded is likely to exceed full-employment output. In Fig. 10.4(b) the aggregate quantity of goods demanded (point H at the intersection of IS2 and LM1) exceeds full-employment output, Y2. Thus the price level must rise, shifting the LM curve up and to the left and causing the economy to return to general equilibrium at F. At F both output and the real interest rate are higher than at the initial equilibrium point, E.

Therefore the increase in government purchases increases output, employment, the real interest rate, and the price level.

Because the increase in employment is the result of an increase in labor supply rather than an increase in labor demand, real wages fall when government purchases rise. Because of diminishing marginal productivity of labor, the increase in employment also implies a decline in average labor productivity when government purchases rise.That fiscal shocks play some role in business cycles seems reasonable, which is itself justification for including them in the model. However, including fiscal shocks along with productivity shocks in the RBC model has the additional advantage of improving the match between model and data. We previously noted that government purchases are procyclical, which is consistent with the preceding analysis. Another advantage of adding fiscal shocks to a model that also contains productivity shocks is that it improves the model's ability to explain the behavior of labor productivity.

Refer back to Fig. 10.2 to recall a weakness of the RBC model with only productivity shocks: It predicts that average labor productivity and GNP are highly correlated. In fact, RBC theory predicts a correlation that is more than twice the actual correlation. However, as we have just shown, a classical business cycle model with shocks to government purchases predicts a negative correlation between labor productivity and GNP because a positive shock to government purchases raises output but lowers average productivity. A classical business cycle model that includes both shocks to productivity and shocks to government purchases can match the empirically observed correlation of productivity and GNP well, without reducing the fit of the model in other respects.[177] Thus adding fiscal shocks to the real business cycle model seems to improve its ability to explain the actual behavior of the economy.

Should Fiscal Policy Be Used to Dampen the Cycle? Our analysis shows that changes in government purchases can have real effects on the economy. Changes in the tax laws can also have real effects on the economy in the classical model, although these effects are more complicated and depend mainly on the nature of the tax, the type of income or revenue that is taxed, and so on.

Potentially, then, changes in fiscal policy could be used to offset cyclical fluctuations and stabilize output and employment; for example, the government could increase its purchases during recessions. This observation leads to the second of the two questions posed in the introduction to the chapter: Should policymakers use fiscal policy to smooth business cycle fluctuations?Recall that classical economists generally oppose active attempts to dampen cyclical fluctuations because of Adam Smith's invisible-hand argument that free markets produce efficient outcomes without government intervention. The classical view holds that prices and wages adjust fairly rapidly to bring the economy into general equilibrium, allowing little scope for the government to improve the macroeconomy's response to economic disturbances. Therefore, although in principle fiscal policy could be used to fight recessions and reduce output fluctuations, classical economists advise against using this approach. Instead, classicals argue that not interfering in the economy's adjustment to disturbances is better.

This skepticism about the value of active antirecessionary policies does not mean that classical economists don't regard recessions as a serious problem. If an adverse productivity shock causes a recession, for example, real wages, employment, and output all fall, which means that many people experience economic hardship. But would offsetting the recession by, for example, increasing government purchases help? In the classical analysis, a rise in government purchases increases output by raising the amount of labor supplied, and the amount of labor supplied is increased by making workers poorer (as a result of higher current or future taxes). Thus under the classical assumption that the economy is always in general equilibrium, increasing government purchases for the sole purpose of increasing output and employment makes people worse off rather than better off. Classical economists conclude that government purchases should be increased only if the benefits of the expanded government program—in terms of improved military security or public services, for example—exceed the costs to taxpayers.

Classicals apply this criterion for useful government spending—that the benefits should exceed the costs—whether or not the economy is currently in recession.So far we have assumed that, because fiscal policy affects the equilibrium levels of employment and output, the government is capable of using fiscal policy to achieve the levels of employment and output it chooses. However, a variety of lags in the process may prevent fiscal policy from being effective. It may take time to realize that policy is needed, known as the recognition lag. The lawmaking process can lead to a legislative lag between the time that a fiscal policy change is proposed and the time that it is enacted. Additional lags occur in implementing the new policies (implementation lag) and in the response of the economy to the policy changes (impact lag). Because of these lags, fiscal policy changes contemplated today should be based on where the economy will be several quarters in the future; unfortunately, forecasting the future of the economy is an inexact art at best.[178] Beyond the problems of forecasting, policymakers also face uncertainties about how and by how much to modify their policies to get the desired output and employment effects. Classical economists cite these practical difficulties as another reason for not using fiscal policy to fight recessions.

10.3