Macroeconomic Policy in an Open Economy with Flexible Exchange Rates

Discuss the

A primary reason for developing the IS-LM model for the open economy is to determine how borrowing and trading links among countries affect fiscal and rr ł r ł < ■ C, C, C,

eTTects OT αo∣mestic monetary policies.

When exchange rates are flexible, the effects of macroeconomicmacroeconomic policy on domestic variables such as output and the real interest rate are largely

policies unchanged when foreign trade is added. However, adding foreign trade raises

two new questions: (1) How do fiscal and monetary policy affect a country's real exchange rate and net exports? and (2) How do the macroeconomic policies of one country affect the economies of other countries? With the open-economy IS-LM model, we can answer both questions.

To examine the international effects of various domestic macroeconomic policies, we proceed as follows:

1. We use the IS-LM diagram for the domestic economy to determine the effects of the policies on domestic output and the domestic real interest rate. This step is the same as in our analyses of closed economies in Chapters 9-11.

2. We apply the results of Section 13.2 (see in particular Summary table 16 and Summary table 17) to determine how changes in domestic output and the domestic real interest rate affect the exchange rate and net exports.

3. We use the IS-LM diagram for the foreign economy to determine the effects of the domestic policies on foreign output and the foreign real interest rate. Domestic policies that change the demand for the foreign country's net exports will shift the foreign IS curve.

A Fiscal Expansion

To consider the effects of fiscal policy in an open economy, let's look again at a temporary increase in domestic government purchases. In analyzing this policy change we use the classical version of the IS-LM model (with no misperceptions) but also discuss the results that would be obtained in the Keynesian framework.

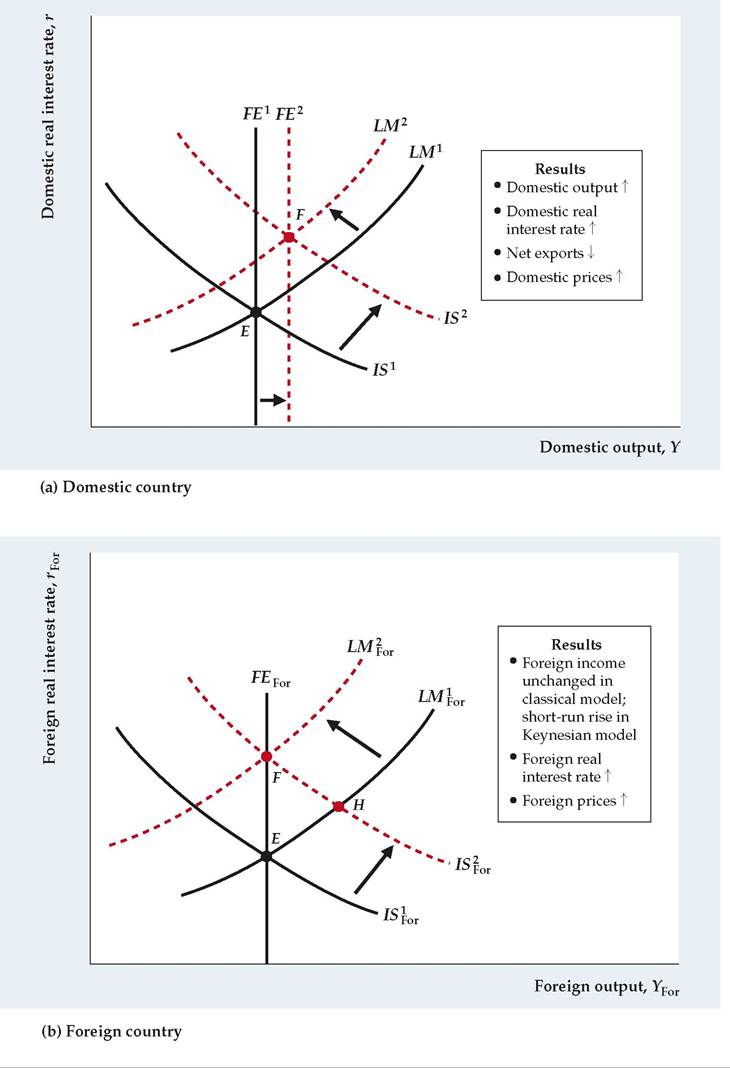

FIGUREJ3.9

Effects of an increase in domestic government purchases

(a) In the classical IS-LM model, an increase in domestic government purchases shifts the domestic IS curve up and to the right, from IS1 to IS 2. It also shifts the domestic FE line to the right, from FE1 to FE 2. Therefore domestic output and the domestic real interest rate both increase. These increases reduce net exports but have an ambiguous effect on the real exchange rate. The results are similar in the Keynesian model.

(b) Because the domestic country's exports are the foreign country's imports, and vice versa, the decrease in the domestic country's net exports is equivalent to a rise in the foreign country's net exports. This increase shifts the foreign IS curve up, from ISpor to ISpor. In the classical model, prices adjust rapidly, shifting the LM curve from LM 1or to

LM por. The new equilibrium is at point F, where the foreign real interest rate and price level are higher but foreign output is unchanged. In the Keynesian model, price stickiness would cause a temporary increase in foreign output at H before price adjustment restores general equilibrium at F. classical model the FE line shifts to the right, from FE1 to FE2. The reason for this shift is that the increase in government purchases raises present or future tax burdens; because higher taxes make workers poorer, they increase their labor supply, which raises full-employment output. The new equilibrium is represented by point F, the intersection of IS2 and FE2. The domestic price level rises, shifting the domestic LM curve up and to the left, from LM1 to LM2, until it passes through F. Comparing point F with point E reveals that the increase in government purchases increases both output, Y, and the real interest rate, r, in the domestic country. So far the analysis is identical to the classical analysis for a closed economy (Chapter 10).

Note also that fiscal expansion raises output and the real interest rate—the same results that we would get from the Keynesian model.Figure 13.9 shows two IS-LM diagrams, one for the domestic country (where the fiscal policy change is taking place) and one for the foreign country, representing the domestic country's major trading partners. Suppose that the original equilibrium is at point E in Fig. 13.9(a). As usual, the increase in government purchases shifts the domestic IS curve up and to the right, from IS1 to IS 2. In addition, in the

To examine the role of international trade, we first consider the effects on the exchange rate of the increases in domestic output and the domestic real interest rate. Recall that an increase in output, Y, causes domestic residents to demand more imports and thus to supply more currency to the foreign exchange market. The increase in domestic output therefore depreciates the exchange rate. However, the rise in the domestic real interest rate makes domestic assets more attractive, causing foreign savers to demand the domestic currency and domestic savers to supply less domestic currency to the foreign exchange market and causing the exchange rate to appreciate. The overall effect of the increase in government purchases on the exchange rate is ambiguous: We can't be sure whether the increase in government purchases will raise or lower the exchange rate.

The effect of the fiscal expansion on the country's net export demand isn't ambiguous. Recall that the increase in domestic output (which raises domestic consumers' demand for imports) and the increase in the real interest rate (which tends to appreciate the exchange rate) both cause net exports to fall. Thus the overall effect of the fiscal expansion clearly is to move the country's trade balance toward deficit. This result is consistent with the analysis of the "twin deficits" (the government budget deficit and the trade deficit) in Chapter 5.

In an interconnected world, the effects of macroeconomic policies in one country aren't limited to that country but also are felt abroad. Based on the analysis we've just finished, taking the extra step and finding out how the domestic fiscal expansion affects the economies of the domestic country's trading partners isn't difficult.

The effects of the domestic fiscal expansion on the rest of the world— represented by the foreign country IS-LM diagram in Fig. 13.9(b)—are transmitted through the change in net exports. Because the domestic country's imports are the foreign country's exports, and vice versa, the decline in net exports of the domestic country is equivalent to an increase in net exports for the foreign country. Thus the foreign country's IS curve shifts up, from ISFor to ISFor.

In the classical IS-LM model, the upward shift of the foreign IS curve doesn't affect foreign output; instead the price level rises immediately to restore general equilibrium (the LM curve shifts up from LM For to LM For). The foreign economy ends up at point F, with the real interest rate and the price level higher than they were initially.

If prices were sticky, as in the Keynesian model, the effects of the shift of the foreign country's IS curve would be slightly different. If prices don't adjust in the short run, the shift of the IS curve implies that the foreign economy would have temporarily higher output at the intersection of the IS and LM curves at point H in Fig. 13.9(b); only after firms adjust their prices would the economy arrive at point F. Otherwise, the implications of the classical and Keynesian analyses are the same.[244]

Therefore, in the open-economy versions of both the classical and Keynesian models, a temporary increase in government purchases raises domestic income and the domestic real interest rate, as in a closed economy. In addition, net exports fall; thus increased government purchases reduce, or crowd out, both investment and net exports. The effect on the real exchange rate is ambiguous: It can either rise or fall.

In the foreign economy the real interest rate and the price level rise. In the Keynesian version of the model, foreign output also rises, but only in the short run.A Monetary Contraction

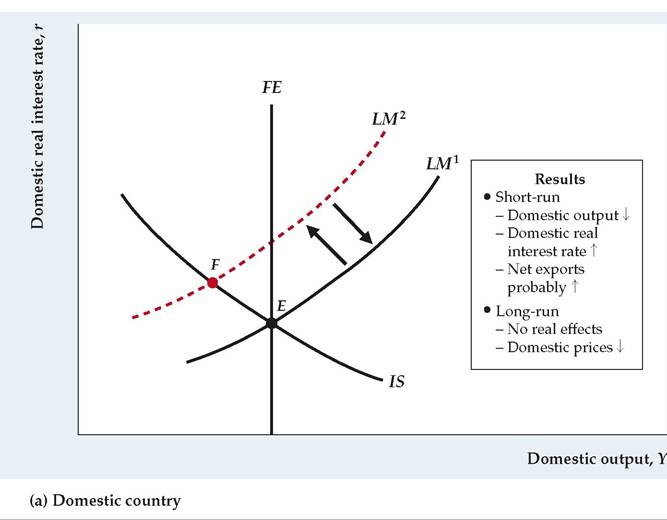

We can also use the open-economy IS-LM model to study the effects of monetary policy when exchange rates are flexible. For the Keynesian version of the IS-LM model we analyze the effects of a drop in the money supply in both the short and long run. Because the effects of monetary policy are the same in the basic classical model (without misperceptions) and the long-run Keynesian model, our analysis applies to the classical model as well.

Short-Run Effects on the Domestic and Foreign Economies. The effects of a monetary contraction are shown in Figure 13.10, which shows IS-LM diagrams corresponding to both the domestic and foreign countries. Suppose that the initial equilibrium is represented by point E and that a decrease in the money supply shifts the domestic LM curve up and to the left, from LM1 to LM2, in Fig. 13.10(a). In the Keynesian model, the price level is rigid in the short run, so the short-run equilibrium is at point F, the intersection of the IS and LM2 curves. Comparing points F and E reveals that in the short run domestic output falls and the domestic real interest rate rises. This result is the same as for the closed economy.

After the monetary contraction, the exchange rate appreciates in the short run, for two reasons. First, the drop in domestic income reduces the domestic demand for imports, leading domestic consumers to demand less foreign currency to buy imported goods. Second, the rise in the domestic real interest rate makes domestic assets relatively more attractive to foreign and domestic savers, increasing foreign savers' demand for the domestic currency and reducing domestic savers' supply of domestic currency to the foreign exchange market.

What happens to the country's net exports? Here there are two competing effects: (1) The drop in domestic income created by the monetary contraction reduces the domestic demand for foreign goods and thus tends to increase the country's net exports; but (2) the rise in the real interest rate, which leads to exchange rate appreciation, tends to reduce net exports.

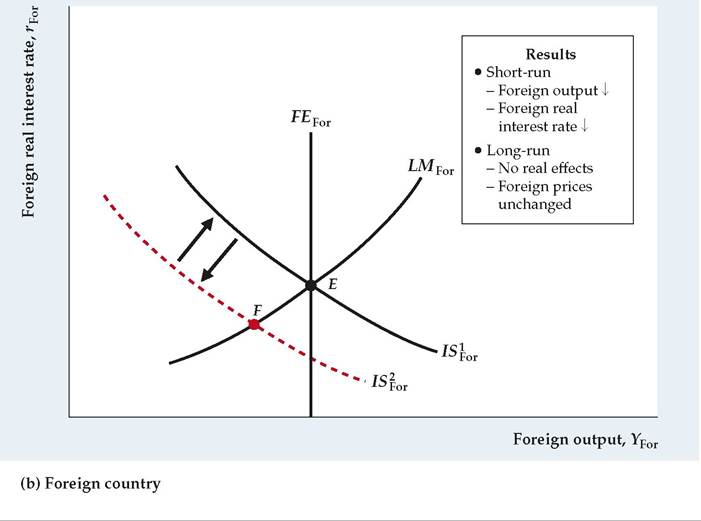

The theory doesn't indicate for certain which way net exports will change. In our earlier discussion of the J curve, however, we noted that the effects of changes in the real exchange rate on net exports may be weak in the short run. Based on that analysis, we assume that in the short run exchange rate effects on net exports are weaker than the effects of changes in domestic income so that overall the country's net exports will increase.The next question is: How does the domestic monetary contraction affect the economies of the country's trading partners? The effects on the typical foreign economy are illustrated by Fig. 13.10(b). If the domestic country's net exports are increased by the monetary contraction, the foreign country's net exports must

FIGURE 13.10

Effects of a decrease in the domestic money supply

(a) A decrease in the domestic money supply shifts the domestic LM curve up, from LM1 to LM 2. The short-run equilibrium in the Keynesian model is at point F, the intersection of the IS and LM 2 curves. The decline in the money supply reduces domestic output and increases the domestic real interest rate. The drop in domestic output and the rise in the real interest rate cause the real exchange rate to appreciate. The effect on net exports is potentially ambiguous; if we assume that the effect on net exports of the drop in domestic income is stronger than the effect of the appreciation of the exchange rate, net exports increase as domestic residents demand fewer goods from abroad.

(b) Because the domestic country's net exports increase, the foreign country's net exports fall and the foreign IS curve shifts down, from IS⅛or to ISpor. Thus output and the real interest rate fall in the foreign country in the short run. In the long run domestic prices fall and both economies return to equilibrium at point E. Thus in the long run money is neutral.

decrease because the domestic country's exports are the foreign country's imports. Thus the IS curve of the foreign country shifts down and to the left, from ISjor to IS2or. The short-run equilibrium is at point F, where the ISjor and LMFor curves intersect. Output in the foreign country declines, and the foreign real interest rate falls.

These results show that a domestic monetary contraction also leads to a recession abroad. This transmission of recession occurs because the decline in domestic output also reduces domestic demand for foreign goods. The appreciation of the domestic real exchange rate works in the opposite direction by making foreign goods relatively cheaper, which tends to increase the net exports of the foreign country. However, we have assumed that the negative effect of declining domestic income on the foreign country's net exports is stronger than the positive effect of the appreciating domestic exchange rate. Thus a domestic monetary contraction leads to a recession in both the foreign country and the domestic country.

Long-Run Effects on the Domestic and Foreign Economies. In the long run after a monetary contraction, wages and prices decline in the domestic country, as firms find themselves selling less output than they desire. The domestic country's LM curve returns to its initial position, LM1 in Fig. 13.10(a), so that money is neutral in the long run. As all real variables in the domestic economy return to their original levels, the real exchange rate and the domestic demand for foreign goods also return to their original levels. As a result, the foreign country's IS curve shifts back to its initial position, ISjor in Fig. 13.10(b), and the foreign country's economy also returns to its initial equilibrium point, E. At E, all foreign macroeconomic variables (including the price level) are at their original levels. Hence in the long run the change in the domestic money supply doesn't affect any real variables, either domestically or abroad. In particular, the real exchange rate and net exports aren't affected by the monetary contraction in the long run.

Although monetary neutrality holds in the long run in the Keynesian model, it holds immediately in the basic classical model. So, in the basic classical model, monetary policy changes have no effect on real exchange rates or trade flows; they affect only the price level. In a monetary contraction, the domestic price level will fall (the foreign price level doesn't change).

Although money can't affect the real exchange rate in the long run, it does affect the nominal exchange rate by changing the domestic price level. (This is one case where the responses of the real and nominal exchange rates to a change in macroeconomic conditions differ.) As we have shown, the long-run neutrality of money implies that a 10% decrease in the nominal money supply will decrease the domestic price level by 10%. Note that Eq. (13.1) implies that the nominal exchange rate, enom, equals ePjor∕P, where e is the real exchange rate, Pjor is the foreign price level, and P is the domestic price level. Because the real exchange rate, e, and the foreign price level, Pjor, are unchanged in the long run by a domestic monetary contraction, the 10% drop in the domestic price level, P, raises the nominal exchange rate, e nom, by (approximately) 10%. Thus a monetary contraction reduces the domestic price level and appreciates the nominal exchange rate by the same percentage as the drop in money supply.

13.5