Fixed Exchange Rates

Evaluate the strengths and weaknesses of different types of exchange rate systems.

FIGURE 13.11

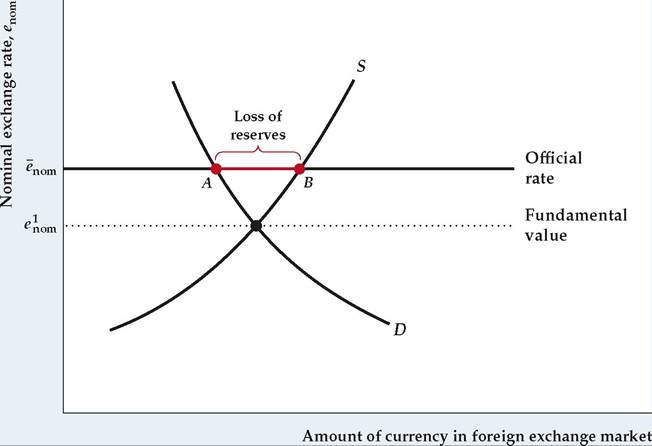

An overvalued exchange rate

The figure shows a situation in which the officially fixed nominal exchange rate, Fnom, is higher than the fundamental value of the exchange rate, e nom, as determined by supply and demand in the foreign exchange market.

In this situation the exchange rate is said to be overvalued. The country's central bank can maintain the exchange rate at the official rate by using its reserves to purchase its own currency in the foreign exchange market, in the amount of AB in each period. This loss of reserves also is referred to as the country's balance of payments deficit.The United States has had a flexible exchange rate since abandonment of the Bretton Woods system of fixed exchange rates during the early 1970s. However, fixed-exchange-rate systems—in which exchange rates are officially set by international agreement—have been important historically and are still used by many countries. Let's now consider fixed-exchange-rate systems and address two questions: (1) How does the use of a fixed-exchange-rate system affect an economy and macroeconomic policy? and (2) Ultimately, which is the better system, flexible or fixed exchange rates?

Fixing the Exchange Rate

In contrast to flexible-exchange-rate systems—where exchange rates are determined by supply and demand in foreign exchange markets—in a fixed-exchangerate system the value of the nominal exchange rate is officially set by the government, perhaps in consultation or agreement with other countries.[245]

A potential problem with fixed-exchange-rate systems is that the value of the exchange rate set by the government may not be the exchange rate determined by the supply and demand for currency. Figure 13.11 shows a situation in which the official exchange rate, Fnom, is higher than the fundamental value of the exchange rate, e Jiom, or the value that would be determined by free market forces without government intervention.

When an exchange rate is higher than its fundamental value, it is an overvalued exchange rate (often referred to as an overvalued currency).

How can a country deal with a situation in which its official exchange rate is different from the fundamental value of its exchange rate? There are several possible strategies: First, the country can simply change the official value of its exchange rate so that it equals, or is close to, its fundamental value. For example, in the case of overvaluation shown in Fig. 13.11, the country could simply devalue (lower) its nominal fixed exchange rate from enom to e Jom. However, although occasional devaluations or revaluations can be expected under fixed-exchange-rate systems, if a country continuously adjusts its exchange rate it might as well switch to a flexible-rate system.

Second, the government could restrict international transactions—for example, by limiting or taxing imports or financial outflows. Such policies reduce the supply of the domestic currency to the foreign exchange market, thus raising the fundamental value of the exchange rate toward its fixed value. Some countries go even further and prohibit people from trading the domestic currency for foreign currencies without government approval; a currency that can't be freely traded for other currencies is said to be an inconvertible currency. However, direct government intervention in international transactions has many economic costs, including reduced access to foreign goods and credit.

Third, the government itself may become a demander or supplier of its currency in the foreign exchange market, an approach used by most of the industrialized countries having fixed exchange rates. For example, in the case of overvaluation shown in Fig. 13.11, the supply of the country's currency to the foreign exchange market (point B) exceeds private demand for the currency (point A) at the official exchange rate by the amount AB.

To maintain the value of the currency at the official rate, the government could buy back its own currency in the amount AB in each period.Usually, these currency purchases are made by the nation's central bank, using official reserve assets. Recall (Chapter 5) that official reserve assets are assets other than domestic money or securities that can be used to make international payments (examples are gold, foreign bank deposits, or special assets created by international agencies such as the International Monetary Fund). During the gold standard period, for example, gold was the basic form of official reserve asset, and central banks offered to exchange gold for their own currencies at a fixed price. If Fig. 13.11 represented a gold-standard country, AB would represent the amount of gold the central bank would have to use to buy back its currency in each period to equalize the quantities of its currency supplied and demanded at the official exchange rate. Recall also that the decline in a country's official reserve assets during a year equals its balance of payments deficit. Thus amount AB measures the reserves the central bank must use to support the currency and corresponds to the country's balance of payments deficit.

Although a central bank can maintain an overvalued exchange rate for a time by offering to buy back its own currency at a fixed price, it can't do so forever because it has only a limited supply of official reserve assets. During the gold standard period, for example, central banks did not own unlimited amounts of gold. Attempting to support an overvalued currency for a long period of time would have exhausted a central bank's limited gold reserves, leaving the country no choice but to devalue its currency.

A central bank's attempts to support an overvalued currency can be ended quickly and dramatically by a speculative run. A speculative run, also called a speculative attack, occurs when financial investors begin to fear that an overvalued currency may soon be devalued, reducing the value of assets denominated in that

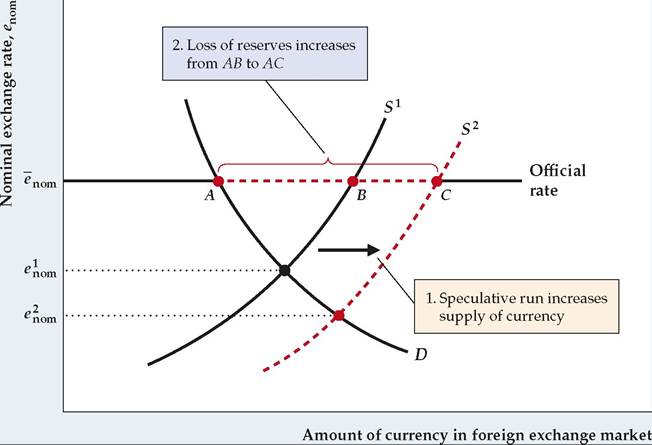

FIGUREJ3.12

A speculative run on an overvalued currency

Initially, the supply curve of the domestic currency is S1, and to maintain the fixed exchange rate, the central bank must use amount AB of its reserves each period to purchase its own currency in the foreign exchange market.

A speculative run occurs when holders of domestic assets begin to fear a devaluation, which would reduce the values of their assets (measured in terms of foreign currency). Panicky sales of domestic-currency assets lead to more domestic currency being supplied to the foreign exchange market, which shifts the supply curve of the domestic currency to the right, from S1 to S2. The central bank must now purchase its currency and lose reserves in the amount AC. This more rapid loss of reserves may force the central bank to stop supporting the overvalued currency and to devalue it, confirming the market's expectations.

currency relative to assets denominated in other currencies. To avoid losses, financial investors frantically sell assets denominated in the overvalued currency. The panicky sales of domestic assets associated with a speculative run on a currency shift the supply curve for that currency sharply to the right (see Figure 13.12), increasing the gap between the quantities supplied and demanded of the currency from amount AB to amount AC. This widening gap increases the rate at which the central bank has to spend its official reserve assets to maintain the overvalued exchange rate, speeding devaluation and confirming the financial investors' expectations.

Without strong restrictions on international trade and finance (themselves economically costly), we conclude that an overvalued exchange rate isn't sustainable for long. If the exchange rate is overvalued, the country must either devalue its currency or make some policy change to raise the fundamental value of the exchange rate. We show in the next section that the basic tool for changing the fundamental value of the exchange rate is monetary policy.

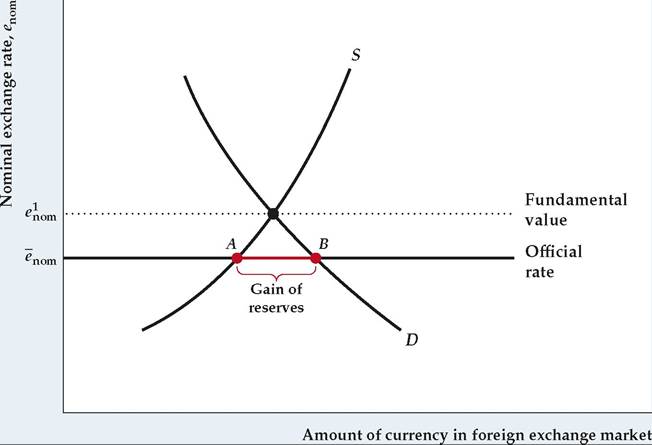

We've focused on overvaluation, but an exchange rate also could be undervalued. As illustrated in Figure 13.13, an undervalued exchange rate (or undervalued currency) exists if the officially fixed value is less than the value determined by supply and demand in the foreign exchange market.

In this case, instead of buying its own currency, the central bank sells its currency to the foreign exchange market and accumulates reserves in the amount AB each period. With no limit to the quantity of reserve assets (gold, for example) a central bank could accumulate, an undervalued exchange rate could apparently be maintained indefinitely. However, a country with an undervalued exchange rate can accumulate reserves only at the expense of trading partners who have overvalued exchange rates and are therefore losing reserves. Because the country's trading partners can't continue to lose reserves indefinitely, eventually they may put political pressure on the country to bring the fundamental value of its exchange rate back in line with the official rate.FIGUREJ3.13

An undervalued exchange rate

The exchange rate is undervalued when the officially determined nominal exchange rate, Fnom, is less than the fundamental value of the exchange rate as determined by supply and demand in the foreign exchange market, e nom. To maintain the exchange rate at its official level, the central bank must supply its own currency to the foreign exchange market in the amount AB each period, thereby accumulating foreign reserves.

Monetary Policy and the Fixed Exchange Rate

Suppose that a country wants to eliminate currency overvaluation by raising the fundamental value of its nominal exchange rate until it equals the fixed value of the exchange rate. How can it achieve this goal? Economists have long recognized that the best way for a country to do so is through contraction of its money supply.

To demonstrate why a monetary contraction raises the fundamental value of the nominal exchange rate, we first rewrite Eq. (13.1), which defined the relationship of the real and nominal exchange rates:

Equation (13.6) states that, for any foreign price level, PFor, the nominal exchange rate, e nom, is proportional to the real exchange rate, e, and inversely proportional to the domestic price level, P.

In our earlier discussion of monetary policy in the Keynesian model with flexible exchange rates, we showed that a monetary contraction causes the real exchange rate to appreciate in the short run by reducing domestic output and increasing the real interest rate. Because short-run domestic and foreign price levels are fixed in the Keynesian model, Eq. (13.6) indicates that the short-run appreciation of the real exchange rate also implies a short-run appreciation of the nominal exchange rate. In the long run money is neutral; hence a monetary contraction has no effect on the real exchange rate, but it does cause the domestic price level to fall. In the long run the domestic price level, P, falls but the real exchange rate, e, is unaffected, so Eq. (13.6) implies that the nominal exchange rate rises (appreciates) both in the long run and the short run. Thus in both the short and long runs a monetary contraction increases the fundamental value of the nominal exchange rate, or

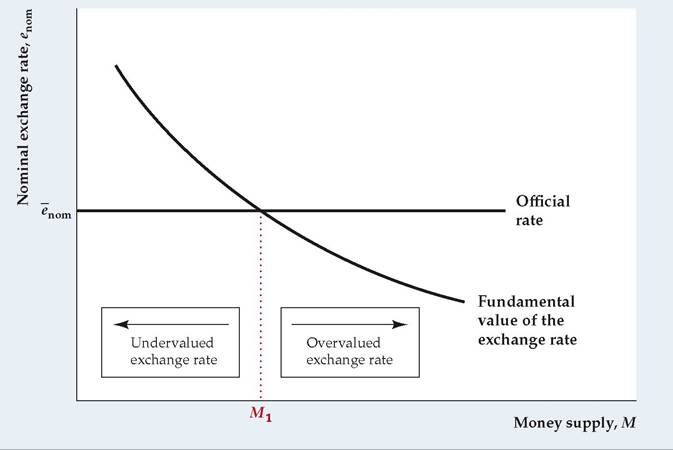

FIGUREJ3.14

Determination of the money supply under fixed exchange rates The downward-sloping fundamental value curve shows that a higher domestic money supply causes a lower fundamental value of the exchange rate. The horizontal line shows the officially fixed nominal exchange rate. Only when the country's money supply equals M1 does the fundamental value of the exchange rate equal the official rate. If the central bank increased the money supply above M1, the exchange rate would become overvalued. A money supply below M1 would result in an undervalued currency.

the value of the nominal exchange rate determined by supply and demand in the foreign exchange market.[246] Conversely, a monetary easing reduces the fundamental value of the nominal exchange rate in both the short run and long run.

Figure 13.14 illustrates the relationship between the nominal exchange rate and the money supply in a country with a fixed exchange rate.[247] The downward-sloping curve shows the relationship of the money supply to the fundamental value of the nominal exchange rate. This curve slopes downward because, other factors being equal, an increase in the money supply reduces the fundamental value of the nominal exchange rate. The horizontal line in Fig. 13.14 is the officially determined exchange rate. M1 on the horizontal axis is the value of the money supply that equalizes the fundamental value of the exchange rate and its officially fixed value. If the money supply is more than M1, the country has an overvaluation problem (the fundamental value of the exchange rate is below the official value), and if the money supply is less than M1, the country has an undervaluation problem.

Figure 13.14 suggests that, in a fixed-exchange-rate system, individual countries typically are not free to expand their money supplies to try to raise output and employment. Instead, the money supply is governed by the condition that the official and fundamental values of the exchange rate be the same. If the country represented in Fig. 13.14 wanted to expand its money supply to fight a recession, for example, it could do so only by creating an overvaluation problem (most likely

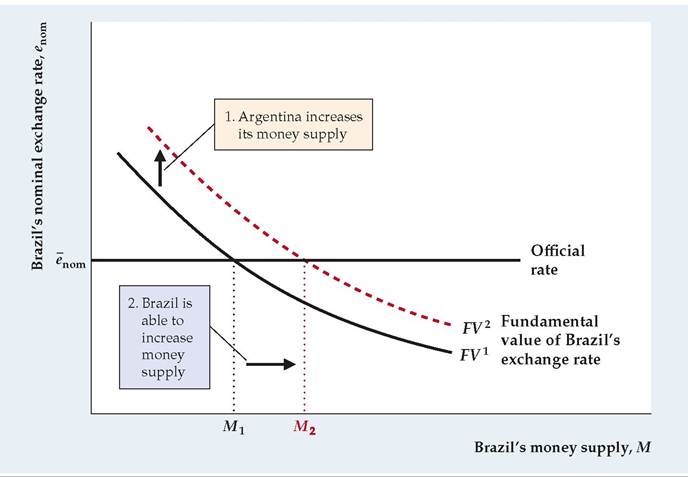

FIGUREJ3.15

Coordinated monetary expansion

Initially, the fundamental value of Brazil's exchange rate is shown by FV1, and the money supply level consistent with the official exchange rate is M1. If Brazil raises its money supply to M 2, the fundamental value of its exchange rate would fall below the official fixed rate, and Brazil's currency would be overvalued.

An increase in Argentina's money supply would depreciate the fundamental value of Argentina's exchange rate and appreciate the fundamental value of Brazil's exchange rate. The curve showing the fundamental value of Brazil's exchange rate shifts up, from FV1 to FV2. Brazil can now increase its money supply to M 2 without creating an overvaluation problem.

leading to a future devaluation) or by devaluing its currency immediately. Under fixed exchange rates, then, a central bank cannot use monetary policy to pursue macroeconomic stabilization goals.

Although one member of a group of countries in a fixed-exchange-rate system generally isn't free to use monetary policy by itself, the group as a whole may be able to do so, if the members coordinate their policies. For example, suppose that Argentina and Brazil have a fixed exchange rate between their two currencies and that, because of a recession in both countries, both want to expand their money supplies. If Brazil attempts a monetary expansion on its own, from M1 to M 2 in Figure 13.15, its exchange rate will become overvalued (its fundamental value, at the intersection of M 2 and FV1, would be lower than the official exchange rate). As a result, the central bank of Brazil would lose reserves, ultimately forcing Brazil to undo its attempted expansion.

Suppose, however, that Argentina goes ahead with its own money supply expansion. If Brazil 's money supply remains constant, an increase in Argentina's money supply reduces the fundamental value of Argentina's (nominal) exchange rate, which is equivalent to raising the fundamental value of Brazil's exchange rate at any level of its money supply, as shown in Fig. 13.15. The fundamental value curve in Fig. 13.15 shifts up, from FV1 to FV2. Now Brazil can expand its money supply, from M1 to M 2, without creating an overvaluation problem (the fundamental value of the Brazilian exchange rate at the intersection of M 2 and FV2 is the same as the official exchange rate). Thus, if Argentina and Brazil cooperate by changing their money supplies in the same proportion, both countries can achieve their stabilization goals without either country experiencing overvaluation. This example shows that fixed exchange rates are most likely to work well when the countries in the system have similar macroeconomic goals, face similar shocks, and can cooperate on monetary policies.

Fixed Versus Flexible Exchange Rates

We have discussed the overvaluation and undervaluation problems that can arise in fixed-exchange-rate systems. However, flexible-exchange-rate systems have problems of their own, primarily the volatility of exchange rates, which introduces uncertainty for people and businesses in their transactions with other countries. Each type of system has its problems, so which is preferable?

Proponents of fixed-exchange-rate systems stress two major benefits. First, relative to a situation in which exchange rates fluctuate continuously, fixed exchange rates (if they are stable and not subject to frequent changes or speculative crises) may make trading goods and assets among countries easier and less costly. Thus a system of fixed rates may promote economic and financial integration and improve economic efficiency. Second, fixed exchange rates may improve monetary policy "discipline," in the sense that countries with fixed exchange rates typically are less able to carry out highly expansionary monetary policies; the result may be lower inflation in the long run.

The other side of the monetary discipline argument is that fixed exchange rates take away a country's ability to use monetary policy flexibly to deal with recessions.[248] This inability is particularly serious if the different countries in the fixed-exchange-rate system have different policy goals and face different types of economic shocks. Thus, for instance, one country may want to expand its money supply to fight a recession while another country does not want to increase its money supply. This divergence in monetary policies between the two countries would put downward pressure on the exchange rate of the country that increases its money supply, and thus would strain the fixed exchange rate between the two countries.

Which system is better depends on the circumstances. Fixed exchange rates among a group of countries are useful when large benefits can be gained from increased trade and integration and when the countries in the system coordinate their monetary policies closely. Countries that value the ability to use monetary policy independently—perhaps because they face different macroeconomic shocks than other countries or hold different views about the relative costs of unemployment and inflation—should use a floating exchange rate.

Currency Unions

An alternative to fixing exchange rates is for a group of countries to form a currency union, under which they agree to share a common currency. Members of a currency union also typically cooperate economically and politically. The agreement among the original thirteen colonies, enshrined in the U.S. Constitution, to abandon their individual currencies and create a single currency, is an early example of a currency union. The Application "European Monetary Unification," discusses a contemporary currency union.

An effective currency union usually requires more than just cooperation of national central banks. For a currency union to work, the common monetary policy must be controlled by a single institution. Because countries are typically reluctant to give up their own currencies and monetary policies, currency unions have been rare. However, if politically feasible, a currency union has at least two advantages over fixed exchange rates. First, the costs of trading goods and assets among countries are even lower with a single currency than under fixed exchange rates. Second, if national currencies are eliminated in favor of the common currency, speculative attacks on the national currencies obviously can no longer occur.

However, a currency union shares the major disadvantage of a fixed-exchangerate system: It requires all of its members to pursue a common monetary policy. Thus, if one member of a currency union is in a recession while another is concerned about inflation, the common monetary policy can't deal with both countries' problems simultaneously. In contrast, under flexible exchange rates, each country could set its own monetary policy independently.

Under what circumstances does forming a currency union make economic sense? Economist Robert Mundell of Columbia University defined an optimum currency area as any geographic region for which the benefits of having a common currency exceed the costs.[249] So, to put the question another way, why might one region be an optimum currency area while another is not?

Researchers have identified four general criteria that help determine whether a group of countries (or other political units) forms an optimum currency area:

1. Countries within an optimum currency area trade extensively with each other (and may hope for even further economic integration). A common currency makes trade across borders easier and is therefore most beneficial when trade is extensive.

2. Countries within an optimum currency area should have similar business cycle patterns. Because a common currency forces countries to have the same monetary policy, conflicts are minimized if booms and recessions in the various countries are closely linked and tend to occur at about the same time.

Even if countries have similar business cycle patterns, those patterns won't be exactly the same. Countries in an optimum currency area therefore need other ways to collectively adjust to economic shocks. The need for economic flexibility is reflected in the third and fourth criteria for an optimum currency area:

3. Countries within an optimum currency area will have high levels of capital and labor mobility; in other words, there are few barriers to flows of investment or of workers across borders. With high levels of mobility, resources can flow to countries within the optimum currency area where their marginal products are highest from regions where their marginal products are lowest; and

4. The fiscal systems within an optimum currency area will allow for the possibility of fiscal transfers, through which the countries or regions within the optimum currency area who are doing relatively better can help countries or regions that are doing worse (and which do not have the possibility of using an independent monetary policy to address their problems).

Application

Is Either the United States or Europe an Optimum Currency Area?

Based on our discussion of an optimum currency area, a natural question to ask is whether either the United States or Europe meets the criteria proposed by Mundell to qualify as an optimum currency area. All 50 states in the United States use the dollar, whereas 19 European countries share the use of the euro. But should they?

The United States has had a common currency since Alexander Hamilton integrated our fiscal and monetary systems. Looking at the evidence, it appears that the United States meets all four criteria for being an optimum currency area. Trade across states is quite extensive. Business cycles tend to hit the country as a whole, although there can be significant differences among states or regions. For example, in the recent recession the states—the "sand states"[250]—that had bigger increases in house prices before the recession tended to do worse as those prices collapsed. Capital and labor mobility are quite high as well. There are extensive fiscal transfers. Taxpayers in rich states indirectly subsidize poor states, as there is much less federal government spending in rich states than they pay in federal taxes. For example, in 2005 federal spending in Mississippi, which had the lowest per-capita income in the country, was $2.02 per $1 of federal taxes paid, and federal spending in Connecticut, which had the highest per-capita income in the country, was just $0.69 per $1 of federal taxes paid.[251] Also, the federal government rather than the states is responsible for Social Security, Medicare, and defense spending.

What about Europe? As in the United States, there is much trade within Europe. However, recently we have seen recessions hit Spain, Italy, and Greece much harder than Germany. Labor and capital are legally free to move between countries but language and cultural barriers mean that workers are less mobile. For example, workers are less likely to move from Greece to Germany than from Illinois to Texas. Fiscal transfers in Europe occur but are much more limited than in the United States because each country retains control of its own spending and taxation decisions. Thus Europe is less obviously an optimum currency area than the United States is, and a number of economists (such as Milton Friedman) pointed this out in advance of European monetary unification (see the Application "European Monetary Unification," for more on this topic).

Some of the problems of the euro predicted by the theory of optimum currency areas seem to have occurred. There were large differences in the recessions in different countries. For example, Germany's unemployment rate peaked at 8% in 2009, whereas the unemployment rate in the remaining countries using the euro averaged more than 14% as recently as 2013. As a result, Germany resisted aggressive monetary policy by the European Central Bank because it was not appropriate for Germany, which meant that monetary policy was too tight for other countries after the financial crisis. Countries such as Greece, Portugal, Ireland, Spain, and Italy all had major fiscal problems that prevented them from using fiscal policy as a substitute for monetary policy. Germany did not need and did not want more expansionary fiscal policy, and so fiscal policy in the euro zone was also relatively tight. The high unemployment rates persisted in many other countries, such as Spain, where the unemployment rate in June 2015 was 22.5% for all workers and 49.2% for young workers (younger than age 25). Thus labor mobility evidently did not do much to help reduce unemployment.

Although the United Kingdom was not part of the euro currency union, it did belong to the European Union (EU), in which the countries in Europe agreed to a number of common practices for immigration, open borders between each other, zero tariffs, and many common rules for business firms. In 2016, voters in the United Kingdom voted to leave the European Union. The consequences were significant because of the trade integration that had occurred between the UK and EU as well as the integration of businesses across the region. In completing its exit from the European Union in 2018, the UK was required to pay a significant penalty for leaving the union, and many businesses (especially in the banking sector) moved people out of London and into other parts of Europe. UK voters wanted out of the union because they thought the gains from increased trade with the rest of Europe did not exceed the costs that came from subscribing to rules on immigration and labor markets that were determined by the EU and not the UK. The withdrawal from the EU was not significant enough, however, to cause recessions in either the UK or the EU. But the withdrawal of the UK from the EU heightened worries about what might happen to the euro currency area if a country withdrew from using the euro currency.

These stresses in Europe have raised the question of whether the euro zone will survive. Even if it survives, will any of the countries that currently use the euro discontinue their use of the euro? One reason to think the euro will survive is the political motivations behind the euro project, especially the desire to enhance European political cooperation and integration. Another reason is that the transition back to individual currencies would be technically complicated and risky. How would new currencies be introduced? What would be done about existing contracts written in euros? So the future of the euro remains an open question.

Application

European Monetary Unification

In December 1991 at a summit meeting in Maastricht in the Netherlands, the member countries of the European Community (EC) adopted the Treaty on European Union, usually called the Maastricht Treaty. This treaty took effect in November 1993, after being ratified (with some resistance) by popular votes in the member countries. The motivation for the treaty was both economic and political. European countries felt that greater economic and political cooperation would lead to faster economic growth and help end the nationalism that contributed to World Wars I and II. One of the most important provisions of the treaty was that those member countries meeting certain criteria (including the achievement of low inflation rates and small government budget deficits) would adopt a common currency, to be called the euro. The common currency came into being on January 1, 1999. Eleven countries, with a collective population and GDP similar to those of the United States, joined the new currency union.19

The common monetary policy for the euro countries is determined by the Governing Council of the European Central Bank (ECB), a multinational institution located in Frankfurt, Germany. The Council includes six members of an Executive Board, appointed through a collective decision of the member countries, plus the governors of the national central banks of the member countries. Except through their representation on the Council, the national central banks, such as Germany's Bundesbank and the Bank of France, gave up their power to make monetary policy for their countries.

Although the European Central Bank was set up to be similar to the Federal Reserve in the United States, two important differences remain. First, U.S. banks are supervised by the Federal Reserve and other U.S. government banking regulators, whereas in Europe each individual country supervised its own banks until recently. Second, in the United States, a single federal government engages in fiscal policy, determining taxes and government spending; in Europe each of the 19 countries runs its own fiscal policy and there is no central control. Both of these differences became important as the euro system went through a series of crises that began in 2008.20 One major improvement in the European banking system occurred in late 2014, when the European Central Bank was given regulatory authority over the largest banks in Europe.

The financial crisis that struck the United States beginning in 2008 had a strong impact all over the world, including Europe. Banks in both the United States and Europe lost large sums when their holdings of mortgage-related securities declined in value. Both the Federal Reserve in the United States and the European Central Bank responded to the crisis by reducing interest rates sharply and by increasing funds available to the economy. However, the two central banks differed in their handling of banks. In the United States, banks first received injections of capital from the U.S. government and later were required to raise additional capital from the private sector because the U.S. government and the Federal Reserve could issue regulations that covered every U.S. bank. However, banks in Europe were not recapitalized and remained weak because the European Central Bank had no control over the banking system, and national governments provided loans to banks in their own countries but did not require them to increase their capital. Because banks in many countries in Europe were weak, they did not lend very much. As a result, the economies of these countries did not grow very fast; thus the financial crisis directly led to a slowdown of the economies in Europe.

19Eight additional countries have subsequently joined the union, so now 19 countries have adopted the euro.

20For a broad overview of the problems in Europe, see Martin S. Feldstein, “The Euro and European Economic Conditions," National Bureau of Economic Research Working Paper No. 17617, November 2011; Jay C. Shambaugh, “The Euro's Three Crises," Brookings Papers on Economic Activity, Spring 2012, online at www.brookings.edu/bpea-articles/the-euros-three-crises/; and Philip R. Lane, “The European Sovereign Debt Crisis," Journal of Economic Perspectives, Summer 2012, pp. 49-68.

(continued)

When the euro monetary union was begun, the countries in the union were required to keep their government deficits smaller than 3% of their GDP. However, beginning in the mid-2000s, a number of the European countries began to violate the deficit requirement and run deficits larger than 3% of GDP. At first, financial markets ignored the growing deficits of these countries, but by spring 2010 investors began to recognize the danger that some countries (especially Greece, Spain, and Italy) might not be able to repay their loans. Interest rates began to rise in those countries relative to interest rates on bonds in the rest of Europe. As more information about the fiscal policy in various European countries was revealed, investors became concerned and began withdrawing funds from those countries. In addition, weaknesses at banks in those countries led to a downward spiral: the government had to provide loans to the weak banks, which in turn meant a higher government budget deficit, which caused interest rates to rise, which caused the banks to weaken further, and so on. In addition, many of the banks in Europe own bonds issued by countries that might not repay them, so a default in those countries would exacerbate the problems at banks. Thus the banking problems and the government deficit problems are intertwined.

Some countries in Europe, especially Germany, had low debt and relatively stronger banks, so their economies performed relatively well and they ran current account surpluses. Other countries had severe problems in their banks and have issued too much government debt; their interest rates rose and they ran current account deficits. If the countries were not tied together with the same currency, the exchange rate could adjust to help bring about balance: for example, the German currency could rise in value relative to the Greek currency, changing relative prices of goods, and helping to restore equilibrium. But because they share a common currency, the exchange rate cannot adjust.

►

More on the topic Fixed Exchange Rates:

- KEY TERMS

- Oman

- NUMERICAL PROBLEMS

- Are Financial Markets Efficient?

- Glossary

- Price Stickiness

- Abel A.B., Bernanke B., Croushore D.. Macroeconomics. 10th Edition, Global Edition. — Pearson,2021. — 690 pp., 2021

- The Conduct of Monetary Policy: Rules Versus Discretion

- The ‘Invisible Hand’ in the Game Theoretic Approach and the Limit of Computability

- Bahrain