Bahrain

Fiscal profligacy, volatile economic trajectory and conditional Gulf support

| GDP | USD44.4bn (World ranking 94) |

| Population | 1.5mn (World ranking 154) |

| Form of state | Constitutional Monarchy |

| Head of government | Hamad bin Isa Al Khalifa |

| Next elections | 2026, Legislative |

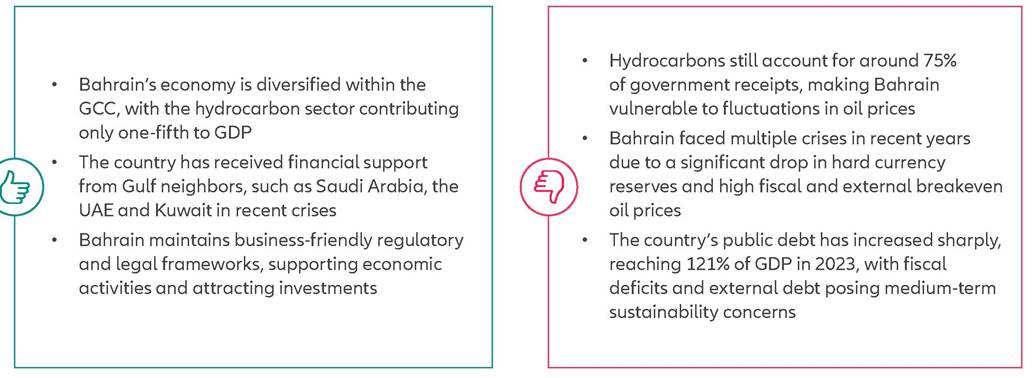

Strengths & weaknesses

Economic overview

Dire fiscal and external positions

The hydrocarbon sector is all-important for the Bahraini economy, even if the latter is diversified compared to that of fellow members of the GCC regional grouping.

The extraction of hydrocarbons accounts for approximately one-fifth of GDP (compared to more than one-third in Saudi Arabia, for example), but the related revenues represent around 75% of government receipts. Bahrain's fiscal and external breakeven oil prices are among the highest in the region, indicating the scarce ability to generate additional revenue through taxation or other means.As a result, Bahrain's fiscal and external vulnerabilities increased rapidly when oil prices collapsed between late 2014 and 2016. At the end of 2017, this caused a financial crisis as the fiscal and external deficits brought the central bank's FX reserves down to about USD1.6bn (import cover of just 0.8 months). In 2018, Saudi Arabia, the UAE and Kuwait agreed to provide a USD10bn financial support package to Bahrain.

Although not disclosed, the aid was conditioned on strict fiscal consolidation, which curtailed growth in the nonoil sector in the following years. At the start of 2019, Bahrain introduced a 5% value-added tax. Not yet recovered from the previous crisis, Bahrain's fiscal and external accounts were again hit by the double whammy of the global Covid-19 pandemic and the oil price slump of early 2020.In the medium term, Bahrain's public finances will remain a cause for serious concern. The government posted an average fiscal deficit of -14% of GDP in 2015-2021, which pushed up public debt from 44% of GDP in 2014 to 121% in 2023, in tandem with external debt surpassing 2.5 times the size of the Bahraini economy. We forecast another fiscal deficit in 2024, with public debt remaining unsustainably high. In contrast to the public and external debt levels, as well as compared to larger countries in the Gulf, Bahrain's sovereign wealth fund is small, estimated at USD18bn in 2023 (40% of GDP).

Overall, the country's debt position appears unsustainable in the medium term. However, we expect Bahrain's rich Gulf neighbors to continue to support it, if needed, to prevent larger concerns.

Still on an uncertain economic trajectory, but support from Gulf countries remains likely

Bahrain's recovery from the double shock of the global Covid-19 crisis and the drop in oil prices in 2020 began moderately in 2021, gathering pace in 2022, with growth averaging +2.7% and +4.2%, respectively. In 2021, authorities tightened lockdown measures again in response to a renewed and lasting surge in Covid-19 cases, despite the rapid vaccine rollout in the country. In 2023, real GDP growth moderated to an estimated +2.6%, due to lower oil and gas revenues and subdued services, especially in the tourism and transportation sectors. We expect these factors to remain in place in 2024, compounded with the resurgence of conflicts in the region, causing a further deceleration of economic growth to +1.8%.

Inflationary risks will remain low. Bahrain experienced only moderate price pressures in 2022, in contrast to many other emerging markets and advanced economies, with headline inflation reaching a peak of +4% in Q3 2022 and gradually easing thereafter. We forecast average annual consumer price inflation to be approximately +2% in 2024, up from an estimated +1.5% in 2023. Bahrain has a fixed exchange rate system, with the Bahraini dinar (BHD) pegged to the US dollar at BHD0.38:USD1. Pressures on the currency and speculation about unpegging rose as the country's dwindling FX reserves during the low-oil-price period in 2015-2017 triggered the financial crisis. However, as Saudi Arabia and some other GCC neighbors remain supportive, the risk of unpegging has declined. On the other hand, progress towards a full Gulf monetary union has been limited and we do not envisage the introduction of an effective GCC single currency in the next five years or so.

Work at the Sitra oil refinery will support GDP growth and keep the fiscal deficit in check once the project goes online. In 2024, public debt will remain well above 100% of GDP, putting pressure on the government as interest rates stay high. A substantial number of megaprojects are being bid on and may begin construction, such as the Bahrain Metro project and a road and rail bridge to connect Bahrain with Qatar. Work on the Bahrain Marina, which will eventually promote tourism, is also expected in 2024.

The political landscape remains tense amid a friendly environment for businesses

The political landscape will remain tense because of latent dissatisfaction with the Sunni Al Khalifa ruling family among the largely Shia population. A decision to re-establish relations with Iran may help reduce tensions in the context of a resurgence of conflicts across the Middle East, following events in Israel, the Gaza Strip and the Red Sea. The regulatory and legal frameworks are business-friendly, while weaknesses remain with regards to perceived corruption, judicial effectiveness and government integrity. Regarding environmental sustainability, Bahrain scores badly, owing to the absence of renewable electricity output, a high level of water stress and a very low recycling rate, ranking only 189th out of 210 economies in our proprietary Environmental Sustainability Index.