Azerbaijan

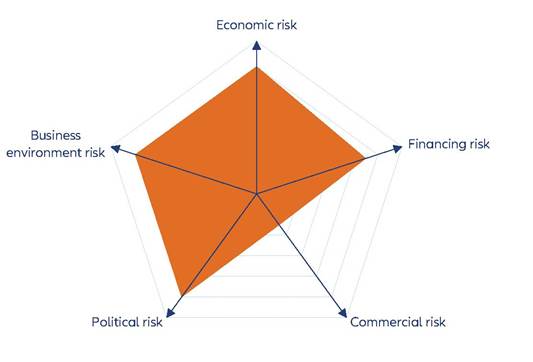

Solid macroeconomic fundamentals but high structural risks

| GDP | USD78.7bn (World ranking 73) |

| Population | 10.2mn (World ranking 91) |

| Form of state | Presidential republic |

| Head of government | Ilham Aliyev (President) |

| Next elections | 2024, Presidential |

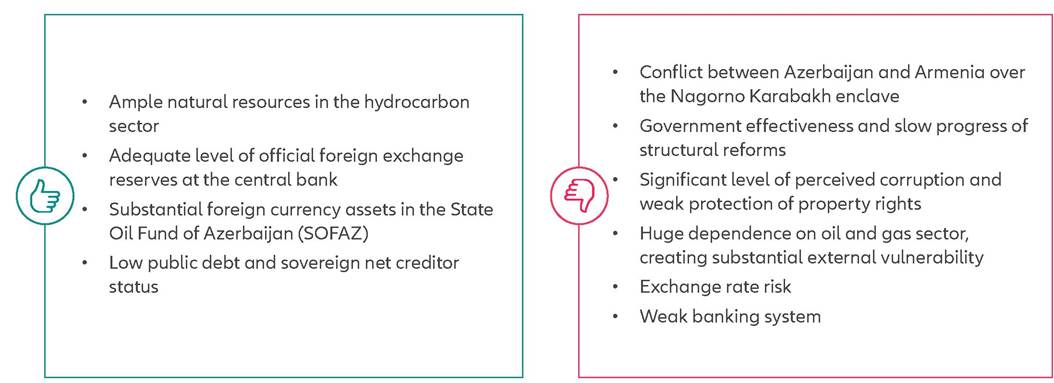

Strengths & weaknesses

Economic overview

Sluggish growth, lower inflation and continued currency risk

Azerbaijan's high dependence on the hydrocarbon sector and global oil and gas prices has resulted in a regime of low and volatile GDP growth since 2011, with annual average real GDP growth of just +1.5% over the past 13 years.

In 2021-2022, the country experienced a strong rebound from the double whammy of the global Covid-19 pandemic and the slump in oil prices in 2020. Real GDP grew by +5.6% in 2021 and +4.6% in 2022 after dropping by -4.2% in 2020. The rebound was broad-based, driven by domestic demand and a strong expansion in the non-oil-and-gas sector as Azerbaijan recovered from the pandemic. The oil and gas sector was boosted by rising global oil and gas prices due to the war in Ukraine. However, economic growth decelerated markedly to just +0.8% in the first 11 months of 2023, with the hydrocarbon sector contracting by -1.6% while the non-oil and gas sector expanded by a resilient +3.2%. The economy has not yet benefited from increasing European demand for Azeri oil and gas. Looking ahead, we forecast annual real GDP growth to pick up to around +2.5% in 2024-2025.Consumer price inflation accelerated from an average of 2.8% in 2020 to 6.7% in 2021 and 13.9% in 2022 on the back of surging global food and energy prices as well as supply disruptions, as seen elsewhere in the emerging market world. The Central Bank of Azerbaijan (CBA) responded with gradual monetary tightening; it hiked its key policy interest rate in ten steps from 6.25% in September 2021 to 9.00% in May 2023. Headline inflation peaked at 15.6% y/y in October 2022 and remained in double digits until mid-2023 before rapidly falling to 2.6% in November, because of higher interest rates, sluggish domestic demand and base effects. As the latter will wane this year and the CBA has begun with moderate rate cuts, we expect inflation to pick up to an average annual 3.5% to 5% in 2024-2025.

In April 2017, the CBA shifted back from a floating exchange rate regime to a “stabilized arrangement”, with the manat (AZN, the local currency) trading at 1.70:1.00 versus the USD, which has been maintained until early 2024. However, analysis of the real effective exchange rate has indicated a significant overvaluation of the AZN since Q3 2021, which amounted to around 12% at end-2023. Hence there is a considerable risk of a sudden sharp depreciation or devaluation of the AZN in the event of a domestic or external shock to the economy.

Comfortable public and external finances

Azerbaijan's public and external finances strongly benefited from the surge in global oil and gas prices in 2021-2022. After a crisis-response program to address the adverse effects of the Covid-19 pandemic and low oil prices moved the fiscal account into a deficit of -6.7% of GDP in 2020, the budget posted sizeable surpluses in 2021-2023. As hydrocarbon prices are forecast to remain broadly at the levels seen in 2023, we project continued annual fiscal surpluses in 20242025. Meanwhile, gross public debt should remain moderate at around 20% of GDP.

Azerbaijan's current account rebounded to a large surplus of +15% of GDP in 2021 after a tiny pandemic-related deficit in 2020.

After surging further to around +30% of GDP in 2022, the annual surplus is estimated to have narrowed markedly in 2023 due to significantly lower nominal oil and gas exports. Going forward, we project continued comfortable external surpluses of around +10% of GDP in 2024-2025.The official foreign exchange (FX) reserves of the CBA (USD12bn at end-2023) cover a comfortable ratio of six months of imports. Moreover, combined with the assets held by the State Oil Fund of Azerbaijan (SOFAZ), they cover over 35 months of imports, providing a sufficient buffer for standard trade finance. The assets held by SOFAZ had declined in the wake of both the oil-price slump in 2014-2015 and the local banking crisis (IBA debt restructuring) in 2017, but they recovered thereafter and remained broadly stable during the Covid-19 crisis, reaching a new high of USD56bn at end-2023 (approximately 65% of expected GDP). This means that the sovereign will remain a solid net creditor in the coming years.

Structural and political weakness

The structural business environment in Azerbaijan is weak and has deteriorated in recent years. The World Bank Institute's annual Worldwide Governance Indicators surveys continue to indicate substantial weaknesses regarding regulatory quality and the rule of law and control of corruption. The Heritage Foundation's Index of Economic Freedom survey 2023 assigns Azerbaijan rank of 75 out of more than 180 economies, a significant worsening from rank 38 in the 2021 survey on the back of deteriorating property rights, judicial effectiveness and government integrity. Moreover, our proprietary Environmental Sustainability Index ranks Azerbaijan only 181 out of 210 economies, reflecting serious weaknesses regarding renewable electricity output, water stress and the recycling rate.

Political risk is set to remains high in the Caucasus region. After the conflict between Azerbaijan and Armenia over the Nagorno-Karabakh enclave had been ongoing for around 30 years, Azerbaijan eventually took over the previously de facto independent territory in 2023. However, this is unlikely to bring a stable peace. Azerbaijan and Armenia took a series of steps to reopen negotiations towards a peace settlement in late 2023, but a final settlement is unlikely to be achieved in 2024. A potential next flashpoint could result from Azerbaijan's intention to establish a transport corridor through Armenia to the Azerbaijani exclave of Nakhichevan.

More on the topic Azerbaijan:

- Index

- 11 Meanwhile in Europe

- JUDGING ACHIEVEMENTS AND LIMITS

- Appointment and Dismissal of Government

- Ukraine: Between Empires and National SelfDetermination

- The Slavs, the Empire, and the Rise of Islam