Neoclassical Growth with Physical and Human Capital

Our next task is to incorporate human capital investments into the baseline neoclassical growth model. This is useful both to investigate the interactions between physical and human capital, and also to generate a better sense of the impact of differential human capital investments on economic growth.

Physical-human capital interactions could potentially be important, since a variety of evidence suggests that physical capital and human capital (capital and skills) are complementary, meaning that greater capital increases the productivity of high human capital workers more than that of low skill workers. This may play an important role in economic growth, for example, by inducing a “virtuous cycle” of investments in physical and human capital. These types of virtue cycles will be discussed in greater detail in Chapter 21. It is instructive to see to what extent these types of complementarities manifest themselves in the neoclassical growth model. The potential for complementarities also raises the issue of “imbalances”. If physical and human capital are complementary, the society will achieve the highest productivity when there is a balance between these two different types of capital. However, whether the decentralized equilibrium will ensure such a balance is a question that needs to be investigated.The impact of human capital on economic growth (and on cross-country income differences) has already been discussed in Chapter 3, in the context of an augmented Solow model, 401

where the economy was assumed to accumulate physical and human capital with two exogenously given constant saving rates. In many ways, that model was less satisfactory than the baseline Solow growth model, since not only was the aggregate saving rate assumed exogenous, but the relative saving rates in human and physical capital were also taken as given.

The neoclassical growth model with physical and human capital investments will enable us to investigate the same set of issues from a different perspective.Consider the following continuous-time economy admitting a representative household with preferences

where the instantaneous utility function u (∙) satisfies Assumption 3 (from Chapter 8) and p > 0. I ignore technological progress and population growth to simplify the discussion. Labor is again supplied inelastically.

Let us follow the specification in Chapter 3 and assume that the aggregate production possibilities frontier of the economy is represented by the aggregate production function:

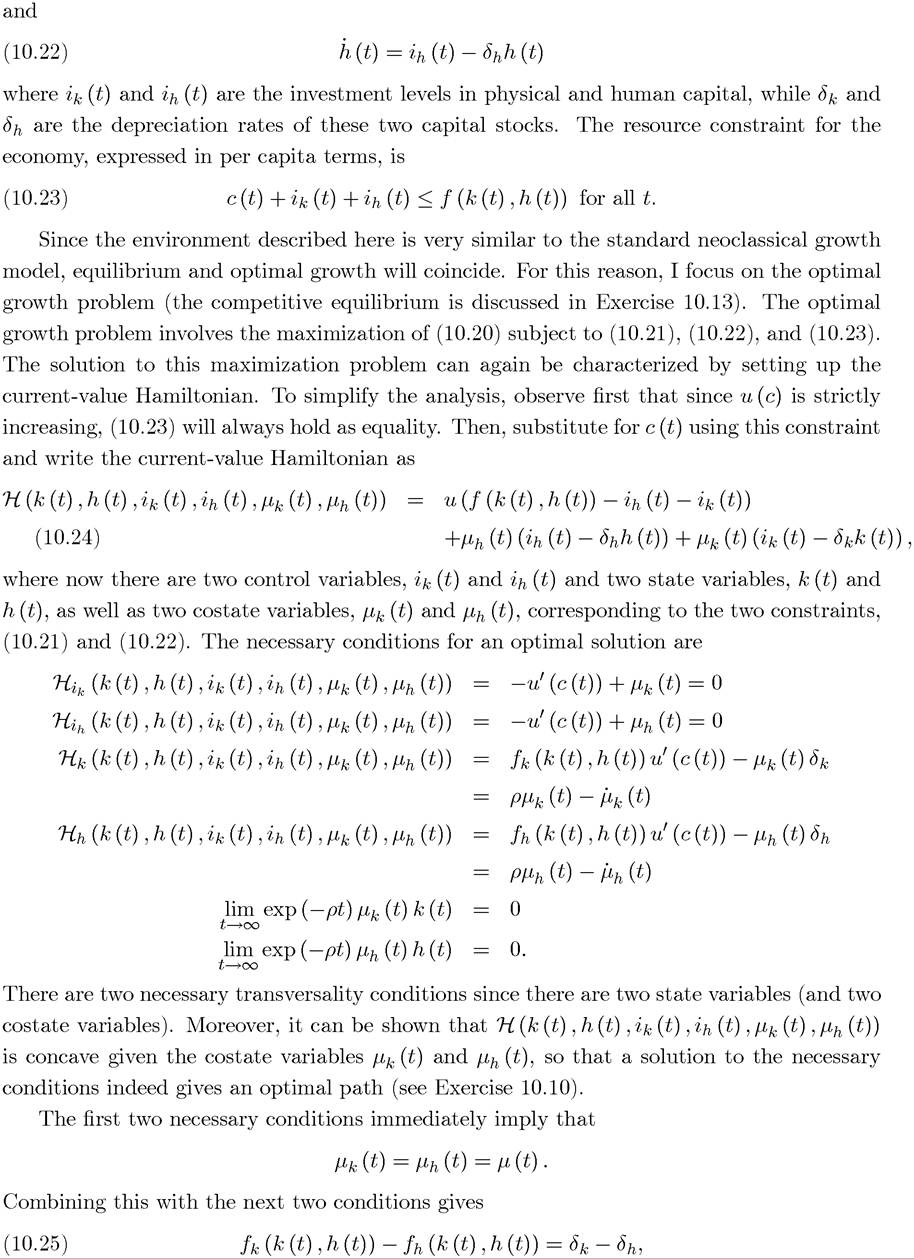

where K (t) is the stock of physical capital, L (t) is total employment, and H (t) represents human capital. Since there is no population growth and labor is supplied inelastically, L (t) = L for all t. This production function is assumed to satisfy Assumptions 10 and 20 in Chapter 3 (recall that these assumptions generalize Assumptions 1 and 2 to this aggregate production function with three inputs). As already discussed in that chapter, a production function in which “raw” labor and human capital are separate factors of production may be less natural than one in which human capital increases the effective units of labor of workers (as in the analysis of the previous two sections). Nevertheless, this production function allows a simple analysis of neoclassical growth with physical and human capital. As usual, it is more convenient to express all ob jects in per capita units, thus we write

Proof.

See Exercise 10.12.?

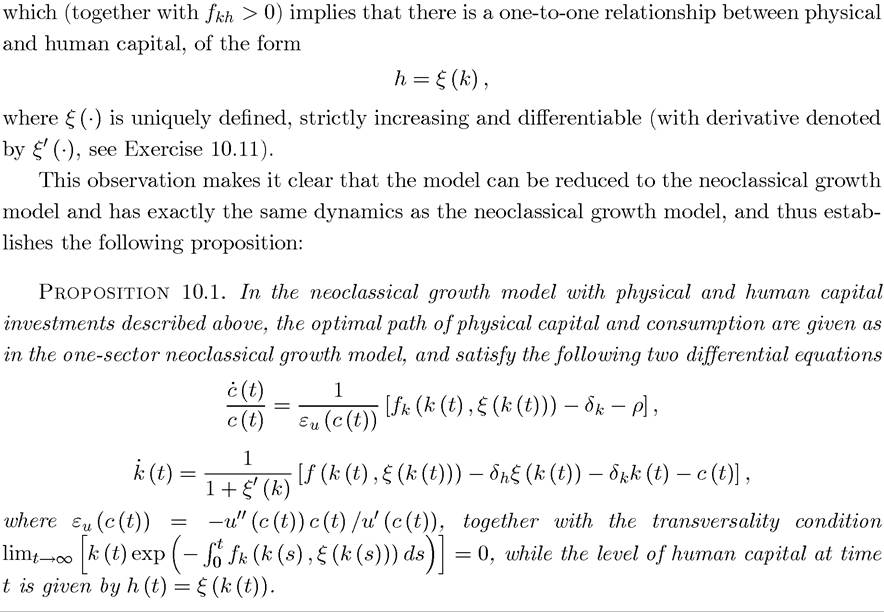

What is perhaps more surprising, at first, is that eq. (10.25) implies that human and physical capital are always in “balance”. Initially, one may have conjectured that an economy that starts with a high stock of physical capital relative to human capital will have a relatively high physical to human capital ratio for an extended period of time. However, Proposition 10.1 and in particular, eq. (10.25) show that this is not the case. The reason for this is that there is no non-negativity constraints on the investment levels. If the economy starts with a high level of physical capital and low level of human capital, at the first instant it will experience a very high level of ih (0), compensated with a very negative i⅛ (0), so that at the next instant the physical to human capital ratio will have been brought back to balance. After this, the dynamics of the economy will be identical to those of the baseline neoclassical growth model. Therefore, issues of imbalance will not arise in this version of the neoclassical growth model. This result is an artifact of the fact that there are no non-negativity constraints on physical and human capital investments. The situation is somewhat different when there are such non-negativity or “irreversibility” constraints, that is, if for all

for all

t. In this case, initial imbalances will persist for a while. In particular, it can be shown that starting with a ratio of physical to human capital stock (k (0) /h (0)) that does not satisfy (10.25), the optimal path will involve investment only in one of the two stocks until balance is reached (see Exercise 10.15). Therefore, with irreversibility constraints, some amount of imbalance can arise, but the economy quickly moves towards correcting this imbalance.

Another potential application of the neoclassical growth model with physical and human capital is in the analysis of the impact of policy distortions.

Recall the discussion in Section 8.10 in Chapter 8, and suppose that the resource constraint of the economy is modified to where τ ≥ 0 is a tax affecting both types of investments. Using an analysis parallel to that in Section 8.10, we can characterize the steady-state income ratio of two countries with different policies represented by τ and τ0. In particular, let us suppose that the aggregate production function takes the Cobb-Douglas form

where τ ≥ 0 is a tax affecting both types of investments. Using an analysis parallel to that in Section 8.10, we can characterize the steady-state income ratio of two countries with different policies represented by τ and τ0. In particular, let us suppose that the aggregate production function takes the Cobb-Douglas form

In this case, the ratio of income in the two economies with taxes/distortions of τ and τ0 is given by (see Exercise 10.16):

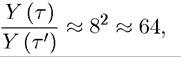

If we again take α⅛ to be approximately 1/3, then the ability of this modified model to account for income differences using tax distortions increases because of the responsiveness of human capital accumulation to these distortions. For example, with α⅛ = α⅛ = 1 /3 and eightfold distortion differences, we would have

which is a huge difference in economic performance across countries.

Therefore, incorporating human capital into the neoclassical growth model provides one potential way of generating larger income per capita differences. Nevertheless, this result has to be interpreted with caution. First, the large impact of distortions on income per capita here is driven by a very elastic response of human capital accumulation. It is not clear whether human capital investments will indeed respond so much to tax distortions. For instance, if these distortions correspond to differences in corporate taxes or corruption, we would expect them to affect corporations rather than individual human capital decisions.

This is of course not to deny that in societies where policies discourage capital accumulation, there are also barriers to schooling and other types of human capital investments. Nevertheless, the impact of these on physical and human capital investments may be quite different. Second, and more important, the large implied elasticity of output to distortions when both physical and human capital are endogenous has an obvious similarity to the Mankiw-Romer-WeiFs approach to explaining cross-country differences in terms of physical and human capital stocks. As discussed in Chapter 3, while this is a logical possibility, existing evidence does not support the notion that human capital differences across countries can have such a large impact on income differences. This conclusion equally sheds doubt on the importance of the large contribution of human capital differences induced by policy differences in the currentmodel. Nevertheless, the conclusions in Chapter 3 were subject to two caveats, which could potentially increase the role of human capital; large human capital externalities and significant differences in the quality of schooling across countries. These issues will be discussed below.

10.5.