Overaccumulation and Pareto Optimality of Competitive Equilibrium in the Overlapping Generations Model

Let us now return to the general problem, and compare the overlapping-generations equilibrium to the choice of a social planner wishing to maximize a weighted average of all generations’ utilities.

In particular, suppose that the social planner maximizes where βs is the discount factor of the social planner, which reflects how she values the utilities of different generations. Substituting from (9.1), this implies:

where βs is the discount factor of the social planner, which reflects how she values the utilities of different generations. Substituting from (9.1), this implies:

subject to the resource constraint

Dividing this by L (t) and using (9.2), the resource constraint can be written in per capita terms as

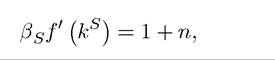

The social planner’s maximization problem then implies the following first-order necessary condition:

Since This result is not surprising; the

This result is not surprising; the

social planner prefers to allocate consumption of a given individual in exactly the same way as the individual himself would do; there are no “market failures” in the over-time allocation of consumption at given prices.

However, the social planner’s and the competitive economy’s allocations across generations will differ, since the social planner is giving different weights to different generations

355

as captured by the parameter βs. In particular, it can be shown that the socially planned economy will converge to a steady state with capital-labor ratio ks such that

which is similar to the modified golden rule we saw in the context of the Ramsey growth model in discrete time (cf., Chapter 6).

In particular, the steady-state level of capital-labor ratio ks chosen by the social planner does not depend on preferences (i.e., on the utility function u (∙)) and does not even depend on the individual rate of time preference, β. Clearly, ks will typically differ from the steady-state value of the competitive economy, k*, given by (9.9).More interesting is the question of whether the competitive equilibrium is Pareto optimal. The example in Section 9.1 suggests that it may not be. Exactly as in that example, we cannot use the First Welfare Theorem, Theorem 5.6, because there is an infinite number of commodities and the sum of their prices is not necessarily less than infinity.

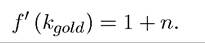

In fact, the competitive equilibrium is not in general Pareto optimal. The simplest way of seeing this is that the steady state level of capital stock, k*, given by (9.9), can be so high that it is in fact greater than kg,,ld. Recall that kg,,ld is the golden rule level of capital-labor ratio that maximizes the steady-state level of consumption (recall, for example, Figure 8.1 in Chapter 8 for the discussion in Chapter 2). When k* > kgr,lr∣, reducing savings can increase consumption for every generation.

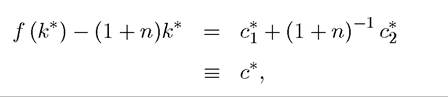

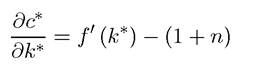

More specifically, note that in steady state we have

where the first line follows by national income accounting, and the second defines c* as the total steady-state consumption. Therefore

and kgθid is defined as

Now so reducing savings can increase (total) consumption

so reducing savings can increase (total) consumption

for everybody.

If this is the case, the economy is referred to as dynamically inefficient—it involves overaccumulation. Another way of expressing dynamic inefficiency is that

that is, the steady-state (net) interest rate is less than the rate of population

is less than the rate of population

growth. Recall that in the infinite-horizon Ramsey economy, the transversality condition (which follows from individual optimization) required that r > g + n, therefore, dynamic inefficiency could never arise in this Ramsey economy. Dynamic inefficiency arises because of

the heterogeneity inherent in the overlapping generations model, which removes the transversality condition.

In particular, suppose we start from steady state at time Consider

Consider

the following variation where the capital stock for next period is reduced by a small amount. In particular, change next period’s capital stock by and from then on,

and from then on,

imagine that we immediately move to a new steady state (which is clearly feasible). This implies the following changes in consumption levels:

generation can be allocated equally during the two periods of their lives, thus necessarily increasing the utility of all generations. This variation clearly creates a Pareto improvement in which all generations are better-off. This establishes:

PROPOSITION 9.6. In the baseline overlapping-generations economy, the competitive equilibrium is not necessarily Pareto optimal. More specifically, whenever r* < n and the economy is dynamically inefficient, it is possible to reduce the capital stock starting from the competitive steady state and increase the consumption level of all generations.

As the above derivation makes it clear, Pareto inefficiency of the competitive equilibrium is intimately linked with dynamic inefficiency. Dynamic inefficiency, the rate of interest being less than the rate of population growth, is not a theoretical curiosity. Exercise 9.8 shows that dynamic inefficiency can arise under reasonable circumstances.

Loosely speaking, the intuition for dynamic inefficiency can be given as follows. Individuals who live at time t face prices determined by the capital stock with which they are working. This capital stock is the outcome of actions taken by previous generations. Therefore, there is a pecuniary externality from the actions of previous generations affecting the welfare of the current generation. Pecuniary externalities are typically second-order and do not matter for welfare (in a sense this could be viewed as the essence of the First Welfare Theorem). This ceases to be the case, however, when there are an infinite stream of newborn agents joining the economy. These agents are affected by the pecuniary externalities created by previous generations, and it is possible to rearrange accumulation decisions and consumption plans in such a way that these pecuniary externalities can be exploited.

A complementary intuition for dynamic inefficiency, which will be particularly useful in the next section, is as follows. Dynamic inefficiency arises from overaccumulation, which, 357

in turn, is a result of the fact that the current young generation needs to save for old age. However, the more they save, the lower is the rate of return to capital and this may encourage them to save even more. Once again, the effect of the savings by the current generation on the future rate of return to capital is a pecuniary externality on the next generation. We may reason that this pecuniary externality should not lead to Pareto suboptimal allocations, as in the equilibria of standard competitive economies with a finite number of commodities and households. But this reasoning is no longer correct when there are an infinite number of commodities and an infinite number of households. This second intuition also suggests that if, somehow, alternative ways of providing consumption to individuals in old age were introduced, the overaccumulation problem could be solved or at least ameliorated. This is the topic of the next section.

9.5.

More on the topic Overaccumulation and Pareto Optimality of Competitive Equilibrium in the Overlapping Generations Model:

- Overaccumulation and Pareto Optimality of Competitive Equilibrium in the Overlapping Generations Model

- Contents