The Four Fundamental Causes

4.3.1. Luck and Multiple Equilibria. In Chapter 21, we will see a number of models in which multiple equilibria or multiple steady states can arise because of coordination failures in the product market or because of imperfections in credit markets.

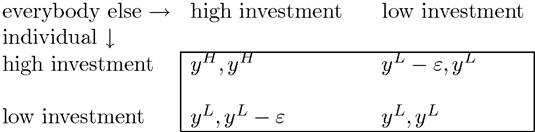

These models suggest that an economy, with given parameter values, can exhibit very different types of behavior, some with higher levels of income or perhaps sustained growth, while others correspond to poverty and stagnation. To give a flavor of these models, consider the following simple game of investment:

The top row indicates whether all individuals in the society choose high or low investment (focusing on a symmetric equilibrium). The first column corresponds to high investment by all agents, while the second corresponds to low investment. The top row, on the other hand, corresponds to high investment by the individual in question, and the bottom row is for low investment. In each cell, the first number refers to the income of the individual in question, while the second number is the payoff to each of the other agents in the economy. Suppose that yH > yl and ε > 0. This payoff matrix implies that high investment is more profitable when others are also undertaking high investment, because of technological complementarities or other interactions.

It is then clear that there are two (pure-strategy) symmetric equilibria in this game. In one, the individual expects all other agents to choose high investment and he does so himself as well. In the other, the individual expects all others to choose low investment and it is the best response for him to choose low investment. Since the same calculus applies to each agent, this argument establishes the existence of the two symmetric equilibria.

This simple game captures, in a very reduced-form way, the essence of the “Big Push” models we will study in Chapter 21.Two points are worth noting. First, depending on the extent of complementarities and other economic interactions, yH can be quite large relative to yL, so there may be significant income differences in the allocations implied by the two different equilibria. Thus if we believe that such a game is a good approximation to reality and different countries can end 136

up in different equilibria, it could help in explaining very large differences in income per capita. Second, the two equilibria in this game are also “Pareto-ranked”—all individuals are better-off in the equilibrium in which everybody chooses high investment.

In addition to models of multiple equilibria, we will also study models in which the realization of stochastic variables determine when a particular economy transitions from low- productivity to high-productivity technologies and starts the process of takeoff (see Section 17.6 in Chapter 17).

Both models of multiple equilibria and those in which stochastic variables determine the long-run growth properties of the economy are attractive as descriptions of certain aspects of the development process. They are also informative about the mechanics of economic development in an interesting class of models. But do they inform us about the fundamental causes of economic growth? Can we say that the United States is rich today while Nigeria is poor because the former has been lucky in its equilibrium selection while the latter has been unlucky? Can we pinpoint their divergent development paths to some small stochastic events 200, 300 or 400 years ago? The answer seems to be no.

U.S. economic growth is the cumulative result of a variety of processes, ranging from innovations and free entrepreneurial activity to significant investments in human capital and rapid capital accumulation. It is difficult to reduce these to a simple lucky break or to the selection of the right equilibrium, while Nigeria ended up in a worse equilibrium.

Even 400 years ago, the historical conditions were very different in the United States and in Nigeria, and as will discuss further below, this led to different opportunities, different institutional paths and different incentives. It is the combination of the historical experiences of countries and different economic incentives that underlies their different processes of economic growth.Equally important, models based on luck or multiple equilibria can explain why there might be a 20-year or perhaps a 50-year divergence between two otherwise-identical economies. But how are we to explain a 500-year divergence? It certainly does not seem plausible to imagine that Nigeria, today, can suddenly switch equilibria and quickly achieve the level of income per capita in the United States.[7] [8] Most models of multiple equilibria are unsatisfactory in another fundamental sense. As in the simple example discussed above, most models of multiple equilibria involve the presence of Pareto-ranked equilibria. This implies that one equilibrium gives higher utility or welfare to all agents than another. While such Pareto-ranked equilibria are a feature of our parsimonious models, which do not specify many relevant dimensions of heterogeneity that are important in practice, it is not clear whether they are useful in thinking about why some countries are rich and some are poor. If indeed it were possible for Nigerians to change their behavior and for all individuals in the nation to become better-off (say by switching from low to high investment in terms of the game above), it is very difficult to believe that for 200 years they have not been able to coordinate on such a better action. Most readers will be aware that Nigerian history is shaped by religious and ethnic conflict, by the civil war that ravaged the nation, and is still adversely affected by the extreme corruption of politicians, bureaucrats and soldiers that have enriched themselves at the expense of the population at large. That an easy Pareto improving change exists against this historical and social background seems improbable to say the least. To be fair, not all models of “multiple equilibria” allow easy transitions from a Pareto inferior equilibrium to a superior equilibrium. In the literature, a useful distinction is between models of multiple equilibria, where different equilibria can be reached if individuals change their beliefs and behaviors simultaneously, versus models of multiple steady states with history dependence, where once a particular path of equilibrium is embarked upon, it becomes much harder (perhaps impossible) to transition to the other steady state equilibrium (see Chapter 21). Such models are much more attractive for understanding persistent differences in economic performance across countries. Nevertheless, unless some other significant source of conflict of interest or distortions are incorporated, it seems unlikely that the difference between the United States and Nigeria can be explained by using models where the two countries have identical parameters, but have made different choices and stuck with them. The mechanics of how a particular steady-state equilibrium can be maintained would be the most important element of such a theory, and other fundamental causes of economic growth, including institutions, policies or perhaps culture, must play a role in explaining this type of persistence. Put differently, in today’s world of free information, technology and capital flows, if Nigeria had the same parameters, the same opportunities and the same “institutions” as the United States, there should exist some arrangement such that these new technologies can be imported and everybody could be made better-off. Another challenge to models of multiple steady states concerns the ubiquity of growth miracles such as South Korea and Singapore, which we discussed in Chapter 1. If crosscountry income differences are due to multiple steady states, from which escape is impossible, then how can we explain countries that embark upon a very rapid growth process? The example of China may be even more telling here. A different, and perhaps more promising, argument about the importance of luck can be made by emphasizing the role of leaders. Perhaps it was Mao who held back China, and his death and the identity, beliefs and policies of his successor were at the root of its subsequent growth. Perhaps the identity of the leader of a country can thus be viewed as a stochastic event, shaping economic performance. This point of view probably has a lot of merit. Recent empirical work by Jones and Olken (2005) shows that leaders seem to matter for the economic performance of nations. Thus luck could play a major role in cross-country income and growth differences by determining whether growth-enhancing or growth-retarding leaders are selected. Nevertheless, such an explanation is closer to the institutional approaches than the pure luck category. First of all, leaders will often influence the economic performance of their societies by the policies they set and the institutions they develop. Thus, the selection and behavior of leaders and the policies that they pursue should be a part of the institutional explanations. Second, Jones and Olken’s research points to an important interaction between the effect of leaders and a society’s institutions. Leaders seem to matter for economic growth only in countries where institutions are non-democratic or weak (in the sense of not placing constraints on politicians or elites). In democracies and in societies where other institutions appear to place checks on the behavior of politicians and leaders, the identity of leaders seems to play almost no role in economic performance. Given these considerations, we conclude that models emphasizing luck and multiple equilibria are useful for our study of the mechanics of economic development, but they are unlikely to provide us with the fundamental causes of why world economic growth started 200 years ago and why some countries are rich while others are poor toady. 4.2.2. Geography. While the approaches in the last subsection emphasize the importance of luck and multiple equilibria among otherwise-identical societies, an alternative is to emphasize the deep heterogeneity across societies. The geography hypothesis is, first and foremost, about the fact that not all areas of the world are created equal. “Nature”, that is, the physical, ecological and geographical environment of nations, plays a major role in their economic experiences. As pointed out above, geographic factors can play this role by determining both the preferences and the opportunity set of individual economic agents in different societies. There are at least three main versions of the geography hypothesis, each emphasizing a different mechanism for how geography affects prosperity. The first and earliest version of the geography hypothesis goes back to Montesquieu ([1748], 1989). Montesquieu, who was a brilliant French philosopher and an avid supporter of Republican forms of government, was also convinced that climate was among the main determinants of the fate of nations. He believed that climate, in particular heat, shaped 139 human attitudes and effort, and via this channel, affected both economic and social outcomes. He wrote in his classic book The Spirit of the Laws: “The heat of the climate can be so excessive that the body there will be absolutely without strength. So, prostration will pass even to the spirit; no curiosity, no noble enterprise, no generous sentiment; inclinations will all be passive there; laziness there will be happiness,” “People are... more vigorous in cold climates. The inhabitants of warm countries are, like old men, timorous; the people in cold countries are, like young men, brave...” Today some of the pronouncements in these passages appear somewhat naive and perhaps bordering on “political incorrectness”. They still have many proponents, however. Even though Montesquieu’s eloquence makes him stand out among those who formulated this perspective, he was neither the first nor the last to emphasize such geographic fundamental causes of economic growth. Among economists a more revered figure is one of the founders of our discipline, Alfred Marshall. Almost a century and a half after Montesquieu, Marshall wrote: “...vigor depends partly on race qualities: but these, so far as they can be explained at all, seem to be chiefly due to climate.” (1890, p. 195). While the first version of the geography hypothesis appears naive and raw to many of us, its second version, which emphasizes the impact of geography on the technology available to a society, especially in agriculture, is more palatable and has many more supporters. This view is developed by an early Nobel Prize winner in economics, Gunnar Myrdal, who wrote “...serious study of the problems of underdevelopment... should take into account the climate and its impacts on soil, vegetation, animals, humans and physical assets—in short, on living conditions in economic development.” (1968, volume 3, p. 2121). More recently, Jared Diamond, in his widely popular Guns, Germs and Steel, espouses this view and argues that geographical differences between the Americas and Europe (or more appropriately, Eurasia) have determined the timing and nature of settled agriculture and via this channel, shaped whether societies have been able to develop complex organizations and advanced civilian and military technologies (1997, e.g., p. 358). The economist Jeffrey Sachs has been a recent and forceful proponent of the importance of geography in agricultural productivity, stating that “By the start of the era of modern economic growth, if not much earlier, temperate-zone technologies were more productive than tropical-zone technologies...” (2001, p. 2). There are a number of reasons for questioning this second, and more widely-held view, of geographic determinism as well. Most of the technological differences emphasized by these authors refer to agriculture. But as we have seen in Chapter 1 and will encounter again below, the origins of differential economic growth across countries goes back to the age of industrialization. Modern economic growth came with industry, and it is the countries that have failed to industrialize that are poor today. Low agricultural productivity, if anything, should create a comparative advantage in industry, and thus encourage those countries with the “unfavorable geography” to start investing in industry before others. One might argue that reaching a certain level of agricultural productivity is a prerequisite for industrialization. While this is plausible (at least possible), we will see below that many of the societies that have failed to industrialize had already achieved a certain level of agricultural productivity, and in fact were often ahead of those who later industrialized very rapidly. Thus a simple link between unfavorable agricultural conditions and the failure to take off seems to be absent.[9] [10] The third variant of the geography hypothesis, which has become particularly popular over the past decade, links poverty in many areas of the world to their “disease burden,” emphasizing that: “The burden of infectious disease is... higher in the tropics than in the temperate zones” (Sachs, 2000, p. 32). Bloom and Sachs (1998) and Gallup and Sachs (2001, p. 91) claim that the prevalence of malaria alone reduces the annual growth rate of sub-Saharan African economies by as much as 2.6 percent a year. Such a magnitude implies that had malaria been eradicated in 1950, income per capita in sub-Saharan Africa would be double of what it is today. If we add to this the effect of other diseases, we would obtain even larger effects (perhaps implausibly large effects). The World Health Organization also subscribes to this view and in its recent report writes: “...in today’s world, poor health has particularly pernicious effects on economic development in sub-Saharan Africa, South Asia, and pockets of high disease and intense poverty elsewhere...” (p. 24) and “...extending the coverage of crucial health services... to the world’s poor could save millions of lives each year, reduce poverty, spur economic development and promote global security.” (p. i). This third version of the geography hypothesis may be much more plausible than the first two, especially since it is well documented in the microeconomics literature that unhealthy individuals are less productive and perhaps less able to learn and thus accumulate human capital. We will discuss both the general geography hypothesis and this specific version of it in greater detail below. But even at this point, an important caveat needs to be mentioned. The fact that the burden of disease is heavier in poor nations today is as much a consequence as a cause of poverty. European nations in the 18th and even 19th centuries were plagued by many diseases. The process of economic development enabled them to eradicate these diseases and create healthier environments for living. The fact that many poor countries have unhealthy environments is, at least in part, a consequence of their failure to develop economically. 4.2.3. Institutions. An alternative fundamental cause of differences in economic growth and income per capita is institutions. One problem with the institutions hypothesis is that it is somewhat difficult to define what “institutions” are. In daily usage, the word institutions refers to may different things, and the academic literature is sometimes not clear about its definition. The economic historian Douglass North was awarded the Nobel Prize in economics largely because of his work emphasizing the importance of institutions in the historical development process. North (1990, p. 3) offers the following definition: “Institutions are the rules of the game in a society or, more formally, are the humanly devised constraints that shape human interaction.” He goes on to emphasize the key implications of institutions: “In consequence [institutions] structure incentives in human exchange, whether political, social, or economic.” This definition encapsulates the three important elements that make up institutions. First, they are “humanly devised”; that is, in contrast to geography, which is outside human control, institutions refer to man-made factors. Institutions are about the effect of the societies’ own choices on their own economic fates. Second, institutions are about placing constraints on individuals. These do not need to be unassailable constraints. Any law can be broken, any regulation can be ignored. Nevertheless, policies, regulations and laws that punish certain types of behavior while rewarding others will naturally have an effect on behavior. And this brings the third important element in the definition. The constraints placed on individuals by institutions will shape human interaction and affect incentives. In some deep sense, institutions, much more than the other candidate fundamental causes, are about the importance of incentives. The reader may have already noted that the above definition makes institutions a rather broad concept. In fact, this is precisely the sense in which we will use the concept of institutions throughout this book; institutions will refer to a broad cluster of arrangements that influence various economic interactions among individuals. These include economic, political and social relations among households, individuals and firms. The importance of political institutions, which determine the process of collective decision-making in society, cannot be 142 overstated and will be the topic of analysis in Part 8 of this book. But this is not where we will begin. A more natural starting point for the study of the fundamental causes of income differences across countries is with economic institutions, which comprise such things as the structure of property rights, the presence and (well or ill) functioning of markets, and the contractual opportunities available to individuals and firms. Economic institutions are important because they influence the structure of economic incentives in society. Without property rights, individuals will not have the incentive to invest in physical or human capital or adopt more efficient technologies. Economic institutions are also important because they ensure the allocation of resources to their most efficient uses, and they determine who obtains profits, revenues and residual rights of control. When markets are missing or ignored (as was the case in many former socialist societies, for example), gains from trade go unexploited and resources are misallocated. We therefore expect societies with economic institutions that facilitate and encourage factor accumulation, innovation and the efficient allocation of resources to prosper relative to societies that do not have such institutions. The hypothesis that differences in economic institutions are a fundamental cause of different patterns of economic growth is intimately linked to the models we will develop in this book. In all of our models, especially in those that endogenize physical capital, human capital and technology accumulation, individuals will respond to (profit) incentives. Economic institutions shape these incentives. Therefore, we will see that the way that humans themselves decide to organize their societies determines whether or not incentives to improve productivity and increase output will be forthcoming. Some ways of organizing societies encourage people to innovate, to take risks, to save for the future, to find better ways of doing things, to learn and educate themselves, to solve problems of collective action and to provide public goods. Others do not. Our theoretical models will then pinpoint exactly what specific policy and institutional variables are important in retarding or encouraging economic growth. We will see in Part 8 of the book that theoretical analysis will be useful in helping us determine what are “good economic institutions” that encourage physical and human capital accumulation and the development and adoption of better technologies (though “good economic institutions” may change from environment to environment and from time to time). It should already be intuitive to the reader that economic institutions that tax productivityenhancing activities will not encourage economic growth. Economic institutions that ban innovation will not lead to technological improvements. Therefore, enforcement of some basic property rights will be an indispensable element of good economic institutions. But other aspects of economic institutions matter as well. We will see, for example, that human capital is important both for increasing productivity and for technology adoption. However, for a broad cross-section of society to be able to accumulate human capital we need some degree of equality of opportunity. Economic institutions that only protect a rich elite or the already-privileged will not achieve such equality of opportunity and will often create other distortions, potentially retarding economic growth. We will also see in Chapter 14 that the process of Schumpeterian creative destruction, where new firms improve over and destroy incumbents, is an essential element of economic growth. Schumpeterian creative destruction requires a level playing field, so that incumbents are unable to block technological progress. Economic growth based on creative destruction therefore also requires economic institutions that guarantee some degree of equality of opportunity in the society. Another question may have already occurred to the reader: why should any society have economic and political institutions that retard economic growth? Would it not be better for all parties to maximize the size of the national pie (level of GDP, economic growth etc.)? There are two possible answers to this question. The first takes us back to multiple equilibria. It may be that the members of the society cannot coordinate on the “right,” i.e., growthenhancing, institutions. This answer is not satisfactory for the same reasons as other broad explanations based on multiple equilibria are unsatisfactory; if there exists an equilibrium institutional improvement that will make all members of a society richer and better-off, it seems unlikely that the society will be unable to coordinate on this improvement for extended periods of time. The second answer, instead, recognizes that there are inherent conflicts of interest within the society. There are no reforms, no changes, no advances that would make everybody better-off; as in the Schumpeterian creative destruction stories, every reform, every change and every advance creates winners and losers. Our theoretical investigations in Part 8 will show that institutional explanations are intimately linked with the conflicts of interests in society. Put simply, the distribution of resources cannot be separated from the aggregate economic performance of the economy—or perhaps in a more familiar form, efficiency and distribution cannot be separated. This implies that institutions that fail to maximize the growth potential of an economy may nevertheless create benefits for some segments of the society, who will then form a constituency in favor of these institutions. Thus to understand the sources of institutional variations we have to study the winners and losers of different institutional reforms and why winners are unable to buy off or compensate losers, and why they are not powerful enough to overwhelm the losers, even when the institutional change in question may increase the size of the national pie. Such a study will not only help us understand why some societies choose or end up with institutions that do not encourage economic growth, but will also enable us to make predictions about institutional change. After all, the fact that institutions can and do change is a major difference between the institutions hypothesis and the geography and culture hypotheses. Questions of equilibrium institutions and endogenous institutional change are central for the institutions hypothesis, but we have to postpone their discussion to Part 8. For now, however, we can note that the endogeneity of institutions has another important implication; endogeneity of institutions makes empirical work on assessing the role of institutions more challenging, because it implies that the standard “simultaneity” biases in econometrics will be present when we look at the effect of institutions on economic outcomes.[11] In this chapter, we will focus on the empirical evidence in favor and against the various different hypotheses. We will argue that this evidence, by and large, suggests that institutional differences that societies choose and end up with are a primary determinant of their economic fortunes. The further discussion below and a summary of recent empirical work will try to bolster this case. Nevertheless, it is important to emphasize that this does not mean that only institutions matter and luck, geography and culture are not important. The four fundamental causes are potentially complementary. The evidence we will provide suggests that institutions are the most important one among these four causes, but does not deny the potential role of other factors, such as cultural influences. 4.2.4. Culture. The final fundamental explanation for economic growth emphasizes the idea that different societies (or perhaps different races or ethnic groups) have different cultures, because of different shared experiences or different religions. Culture is viewed, by some social scientists, as a key determinant of the values, preferences and beliefs of individuals and societies and, the argument goes, these differences play a key role in shaping economic performance. At some level, culture can be thought of as influencing equilibrium outcomes for a given set of institutions. Recall that in the presence of multiple equilibria, there is a central question of equilibrium selection. For example, in the simple game discussed above, will society coordinate on the high-investment or the low-investment equilibrium? Perhaps culture may be related to this process of equilibrium selection. “Good” cultures can be thought of as ways of coordinating on better (Pareto superior) equilibria. Naturally, the arguments discussed above, that an entire society could being stuck in an equilibrium in which all individuals are worse-off than in an alternative equilibrium is implausible, would militate against the importance of this particular role of culture. Alternatively, different cultures generate different sets of beliefs about how people behave and this can alter the set of equilibria for a given specification of institutions (for example, some beliefs will allow punishment strategies to be used whereas others will not). The most famous link between culture and economic development is that proposed by Weber (1930), who argued that the origins of industrialization in Western Europe could be traced to a cultural factor—the Protestant reformation and particularly the rise of Calvinism. Interestingly, Weber provided a clear summary of his views as a comment on Montesquieu’s arguments: “Montesquieu says of the English that they ‘had progressed the farthest of all peoples of the world in three important things: in piety, in commerce, and in freedom’. Is it not possible that their commercial superiority and their adaptation to free political institutions are connected in some way with that record of piety which Montesquieu ascribes to them?” Weber argued that English piety, in particular, Protestantism, was an important driver of capitalists development. Protestantism led to a set of beliefs that emphasized hard work, thrift, saving. It also interpreted economic success as consistent with, even as signalling, being chosen by God. Weber contrasted these characteristics of Protestantism with those of other religions, such as Catholicism and other religions, which he argued did not promote capitalism. More recently, similar ideas have been applied to emphasize different implications of other religions. Many historians and scholars have argued that not only the rise of capitalism, but also the process of economic growth and industrialization are intimately linked to cultural and religious beliefs. Similar ideas are also proposed as explanations for why Latin American countries, with their Iberian heritage, are poor and unsuccessful, while their North American neighbors are more prosperous thanks to their Anglo-Saxon culture. A related argument, originating in anthropology, argues that societies may become “dysfunctional” because their cultural values and their system of beliefs do not encourage cooperation. An original and insightful version of this argument is developed in Banfield’s (1958) analysis of poverty in Southern Italy. His ideas were later picked up and developed by Putnam (1993), who suggested the notion of “social capital,” as a stand-in for cultural attitudes that lead to cooperation and other “good outcomes”. Many versions of these ideas are presented in one form or another in the economics literature as well. Two challenges confront theories of economic growth based on culture. The first is the difficulty of measuring culture. While both Putnam himself and some economists have made some progress in measuring certain cultural characteristics with self-reported beliefs and attitudes in social surveys, simply stating that the North of Italy is rich because it has good social capital while the South is poor because it has poor social capital runs the risk of circularity. The second difficulty confronting cultural explanations is for accounting for growth miracles, such as those of South Korea and Singapore. As mentioned above, if some Asian cultural values are responsible for the successful growth experiences of these countries, 146 it becomes difficult to explain why these Asian values did not lead to growth before. Why do these values not spur economic growth in North Korea? If Asian values are important for Chinese growth today, why did they not lead to a better economic performance under Mao’s dictatorship? Both of these challenges are, in principle, surmountable. One may be able to develop models of culture, with better mapping to data, and also with an associated theory of when and how culture may change rapidly under certain circumstances, to allow stagnation to be followed by a growth miracle. While possible in principle, such theories have not been developed yet. Moreover, the evidence presented in the next section suggests that cultural effects are not the major force behind the large differences in economic growth experienced by many countries over the past few centuries. 4.4.