Banker's acceptance

With banker's acceptances it is a bank that takes on the liability to pay a sum of money on a fixed date.

Example 14.14

The use of a banker’s acceptance

A German company purchases ˆ8.5 million of goods from a Swiss company.

It draws up a document promising to pay for the goods in 90 days’ time, which its bank accepts, that is, it is obliged to pay ˆ8.5 million when it is due.By stamping ‘accepted’ on the document, the document becomes more valuable than if the promise to pay was given by the buying company only. Also it is a negotiable (sellable) instrument.

Twenty days after the Swiss exporter receives the banker’s acceptance (BA) it decides to sell it in the money market to raise some extra short-term finance. It is sold at a discount of 0.95%. To calculate how much (the selling price) it receives:

Selling price = Face value - (Face value ? Discount percentage)

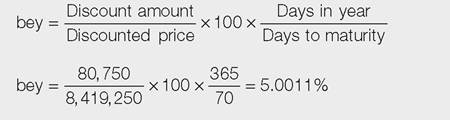

To calculate the annual rate of interest, the bond equivalent yield, which this is costing them:

The exporter can shield itself from the risk of exchange rates shifting over the remaining 70 days until the BA pays out by discounting the acceptance, receiving euros and then converting these to Swiss francs. And, of course, the exporter is not exposed to the credit risk of the importer because it has the guarantee from the importer’s bank.

The 360-day convention

A point of potential confusion: bear in mind that in the US and many other money markets the rate of discount is quoted as an annualised rate based on a 360-day year.

Example 14.15

A US banker's acceptance

If an institution sells a BA with a face value of $10 million when the rate of discount is quoted at 3.05% based on a 360-day convention and the length of time to maturity is 60 days, the amount to be received is: