Bill of exchange

Bills of exchange are used by companies to facilitate trading by granting a credit period to a customer. The customer signs a bill (accepts it) promising to pay a sum of money to the seller at a set date.

Example 14.13

Bill of exchange

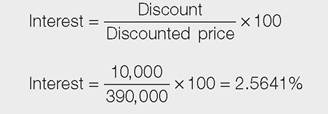

A customer has accepted a bill of exchange which commits it to pay £400,000 in 180 days. The supplier needs to raise cash immediately and so sells the bill to a discount house or bank for £390,000. The discounter will, after 180 days, realise a profit of £10,000 on a £390,000 asset. To calculate the effective rate of interest over 180 days:

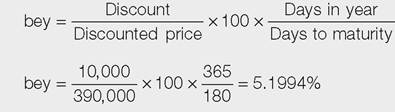

To calculate the annual rate of interest, the bond equivalent yield, this equates to:

Through this arrangement the customer has the benefit of the goods on 180 days' credit, the supplier has made a sale and immediately receives cash from the discount house amounting to 97.4359% of the total due. The discounter, if it can borrow its funds at less than 2.5641% over 180 days, turns in a healthy profit.