CHAPTER TEN Consumerism and the Reorientation of Antifraud Policy

The postwar tightening of laws against business fraud occurred during a period of remarkable prosperity. Rapid economic growth between 1940 and 1970 moved tens of millions of Americans into the middle class, raising social expectations.

Although America's consumer society had deep historical roots, the embrace of consumption took on new dimensions after World War II. Politicians and other arbiters of public values came to define social aspirations in terms of home ownership, possessions such as cars and televisions, and the capacity to pursue chosen lifestyles. Such messages were amplified by advertising barrages from corporations and ubiquitous depictions of material plenty in radio dramas, movies, and television shows. This perspective privileged technologically driven improvements in living standards and a concomitant widening of consumer choice. Over the same decades, the nation's leading financial institutions, led by the NYSE, developed comprehensive public relations programs to bring the masses into the financial markets. This renewed drive to democratize investment, along with the expanding scope of institutional investors such as pension funds, insurance companies, and mutual funds, meant that by 1970, a majority of American families had a personal financial stake in the securities markets.1For some business elites and their political allies, the valorization of consumer culture and democratic participation in modern financial capitalism had deeper political purposes. One goal was geopolitical—to sharply differentiate the US economy, with its capacity to distribute the fruits of capitalism to a broad middle class, from its Soviet antagonist. A 1952 DuPont Chemicals advertisement that posed the question, “Which Marx Gets the Biggest Laugh?— Karl or Groucho”—encapsulated this line of argument. It lampooned the Marxist “joke” about “the impoverishment of the people” under capitalism, which “[y]ou don't get...

until you try to find a place to park, down-town amid all the impoverished people shopping like mad in the department stores,” or until “you see newsreels of the new Russian automobile,” which would “be sneered off any used-car lot in America.” Related messages focused more on domestic political economy. Through public relations and advertising that extolled free enterprise, the corporate establishment hoped to deflect calls by more militant labor unions for a greater say in the management of enterprise. Business elites further wished to constrain the broader New Deal focus on providing economic security and to forestall more substantial roles for the public sector, such as nationalized healthcare or expansive public housing projects. Such efforts did limit the place of government in American capitalism.2 But in nudging popular mores toward the imperatives of consumption and the views of Groucho Marx, the tribunes of free enterprise sharpened popular dissatisfaction with perceived duplicity by manufacturers, retailers, and financial firms.The mid-twentieth-century consumer economy, moreover, provided unscrupulous American firms with ample opportunities to generate dissatisfaction. American inner cities remained home to businesses that riffed off the venerable strategies of bait and switch advertising, high-pressure selling tactics, and reliance on deceptive credit terms. In the process of unleashing new frontiers for consumption, post-World War II suburbanization created further avenues for consumer fraud, with home improvement, automobile sales, electronics repair, and real-estate scams topping the list. By the 1960s, dramatic growth in the elderly population encouraged scams targeting seniors. After World War II, the panoply of available investments continued to include Ponzi schemes and scores of get-rich-quick stock promotions.

With so many targets remaining for would-be reformers, and with heightened popular sensitivities to duplicitous marketing, the embrace of antifraud initiatives allowed one to claim the mantle of consumerism.

Savvy politicians across the country recognized this opportunity, as did a slew of communitybased consumer organizations. The result was a renewed and reconfigured antifraud coalition, pushed by consumer activists and informed by sociological and legal research, with significant participation from leaders of both major political parties, including three successive US presidents. New antideception laws and agencies proliferated at all levels of government, reflecting the imperatives of consumer and investor protection. Nonetheless, macroeconomic challenges during the 1970s meant that public investments never quite matched rhetorical flourishes. Those same economic pressures set the stage for a conservative backlash against the most ambitious advances of the antifraud state.Expansion of the Antifraud Coalition

The impetus to redirect antifraud regulation toward consumer interests sprang from the discontent that ordinary Americans expressed as they navigated the postwar economy. All the paeans to technological improvement and the good life heightened expectations about consumer experience, even as the concerted efforts of social movements deepened American commitments to individual rights. As racial minorities, women, and other social groups pressed their claims through popular discourse and constitutional litigation, a larger fraction of the populace felt emboldened to demand their due, and so disinclined to remain silent suckers. The BBBs and law enforcement agencies reaped the resulting whirlwind, embodied in tens of thousands of annual consumer complaints that accused businesses of misleading or untruthful marketing pitches.

As in earlier eras, journalists played a central role in identifying the contours of business fraud and making them visible to the public. National magazines, such as Ebony and Better Homes and Gardens, along with leading newspapers, such as the Chicago Tribune and the New York Times, continued to cover business fraud. Every year, their journalists churned out hundreds of stories that alerted readers to the latest deceptions, covered enforcement actions, and dispensed advice about how to avoid scams or seek redress.

Prominent writers also updated the messages of Confessions of a Confidence Man and The Bargain Hucksters, publishing books that focused on the latest marketing depredations in urban neighborhoods and suburbia.3By the 1960s and 1970s, a growing number of urban newspapers and television stations gave individual reporters and columnists the opportunity to become local consumer sentinels. At the Philadelphia Tribune, a paper that focused on the local African American community, journalist Len Lear put together in-depth series on scams by home-improvement firms, used-car dealers, unscrupulous or phony doctors, and predatory life insurance companies. The paper also created “Mr. Help,” a service desk that readers could contact to ask for assistance in dealing with consumer complaints.4 Christine Winters, who wrote for the Chicago Tribune, pumped out dozens of articles on the consumer frauds prevalent in the Windy City. In Atlanta, station WAGA gave its consumer relations editor, Paul Reynolds, wide latitude to put together regular segments on automobile repair rip-offs and mail-order frauds. Television viewers in Washington, DC, received regular news coverage of consumer scams on three different local channels: the ABC and NBC affiliates and independent station WTTG.5 These reporters, joined on the fraud beat by counterparts throughout the nation, offered troubleshooting services for disgruntled consumers, much like those provided by BBBs.

Investigative journalism was accompanied by a growing corpus of social science research into the prevalence, dynamics, and policy responses to business fraud. In terms of sheer output, legal scholars dominated this academic discourse. The nation's leading law reviews published a steady flow of articles that documented trends in antifraud policies, evaluated their impacts, and proposed new approaches. Many of the most probing analyses came from student editors, who produced comprehensive “Notes” that detailed fraud law in action.

This conversation within legal academia increased in frequency and intensity from the mid-1960s through the late 1970s.6The most influential academic study, however, came from a sociologist, David Caplovitz, whose research into consumer culture in disadvantaged New York City neighborhoods came out in 1963 under the title The Poor Pay More: Consumer Practices of Low-Income Families. Caplovitz showed the limited choices confronting these residents and the extent to which merchants and door-to-door salesmen took advantage of them through “shady practices.” His catalogue of predatory retail tactics received extensive notice from national opinion-makers. It also helped to shape the agenda of the Kerner Commission on the race riots of the 1960s, whose 1968 report stressed commercial misrepresentations and abuses as contributing to urban unrest.7

By the early 1970s, a host of newer consumer groups had joined the antifraud fray. In almost every state, activists founded councils that focused on consumer education and policy work. From 1968 onward, these state-level groups were linked through national umbrella organizations such as the National Consumer Law Center and the Consumer Federation of America. In this same period, numerous community-based organizations were founded in the nation's largest cities. Usually possessing shoestring budgets and sometimes keeping their doors open for only a few years, these advocates were based in poor urban neighborhoods and manifested the creative activism that characterized the era's wider social movements. To the leaders of San Francisco's Consumer Action, Chicago's Community Thrift Club, or Philadelphia's Consumer Education and Protective Association (CEPA), governments needed to do far more to combat the cruelest scams, which targeted individuals with limited formal education and low incomes, often in inner-city African American and Latino communities.8

Nonprofit consumer groups, however, did not initially take the lead in translating popular anger into concrete proposals for new antifraud policies.

Instead, elected officials staked out this ground, with a few state attorneys general playing prominent roles. These officials had the responsibility of enforcing criminal fraud laws and recognized the political payoffs that might accrue to consumer champions. One way to cultivate such a reputation was to create antifraud bureaucracies. The first effort along these lines was instigated by New York Attorney General Louis Leffiowitz, a lifelong Republican stalwart.Hailing from an immigrant neighborhood on Manhattan's Lower East Side, Lefkowitz found himself inundated by consumer complaints about shady businesses and outright frauds after gaining office in 1956. The next year, he established a Consumer Frauds and Protection Bureau, which he made an internal funding priority. This new office developed ambitious strategies of public outreach, and increased its capacity to investigate complaints from disaffected New York consumers. It put out newsletters, pamphlets, and educational films, and issued a blizzard of press releases. Hardly a legislative session went by without Leffiowitz calling for the passage of some new law to deal with a dimension of consumer fraud that citizen complaints had brought to the attention of his staff attorneys. All of this activity received assiduous coverage from the state's news outlets and cemented the attorney general's popularity with New York voters, who returned him to office by large margins for over two decades.9

Lefkowitz pressed other states to address consumer fraud issues, and his long tenure in office advertised the electoral advantages of doing so. Elected officials elsewhere took note, with scores of prominent political figures seeking to position themselves as intrepid foes of consumer and investor fraud. Governors from both parties, including Connecticut's Abraham Ribicoff, New York's Nelson Rockefeller, Maryland's Spiro Agnew, and Georgia's Jimmy Carter, constructed anti-business fraud agendas. Even Ronald Reagan set out several proposals to constrain consumer fraud while serving as California governor.10

Attorneys general proved even more eager to build reputations as vocal defenders of the put-upon consumer. Often viewing their positions as steppingstones to governorships or US Senate seats, they grasped that aligning themselves with a burgeoning consumer movement represented excellent politics. These ambitious politicos ranged from liberal Democrats, such as Illinois's William Clark, to more conservative members of the party, such as North Carolina's Robert Morgan, and also included moderate Republicans such as Slade Gorton and Evelle Younger, from Washington and California, respectively. Each spearheaded antifraud agendas, lobbied state legislatures for more vigorous consumer protections and greater funding for consumer fraud divisions, and chased after media coverage.11

National political leaders soon joined the competition to burnish credentials as consumer advocates. Of all the voices asking for sterner antifraud policies, none had a bigger megaphone than occupants of the Oval Office. President Eisenhower had used that megaphone briefly after the television quiz show scandals. Subsequent presidential administrations did so more frequently, identifying antifraud reforms as national priorities. Presidents Kennedy, Johnson, and Nixon each used their bully pulpit to amplify public awareness of consumerism as a policy framework and commercial deception as an issue demanding legislative and administrative responses.

The Kennedy administration signaled its intentions in the fall of 1961, when Attorney General Robert F. Kennedy convened a national conference for lawenforcement officials on antitrust issues, consumer protection, and investment fraud. The following year, his brother, President John F. Kennedy, articulated an expansive commitment to consumerism in a Special Address to Congress. Modern consumers, Kennedy argued, faced unprecedented informational challenges. Firms throughout the country had embraced the impersonal marketing techniques of mass advertising, a bewildering array of credit terms, and confusing, nonstandard packaging techniques. In addition, the president stressed, the “voice” of consumers was “not always as loudly heard in Washington as the voices of smaller and better-organized groups” such as manufacturers, retailers, and trade associations. As a result, the federal government needed to develop a more cohesive program of consumer protection, tackling consumer safety, the problem of concentrated economic power, and the most prevalent versions of commercial deception. Kennedy concluded by calling for a consumer’s bill of rights featuring “the right to be informed—to be protected against fraudulent, deceitful, or grossly misleading information, advertising, and labeling.”12

Lyndon Johnson reprised all of these themes four years later in his own presidential message to Congress. For Johnson, America faced “new problems of prosperity” brought on by “new complexities and hazards” associated with “the march of technology” and marketing practices that made consumer “choices more difficult.” While lauding corporate innovation and cautioning against excessive meddling in “the free enterprise system,” the Texan nonetheless demarcated an indispensable role for government in safeguarding “the consumer... against unsafe products, against misleading information, and against the deceitful practices of a few businessmen that can undermine confidence in the vast majority of diligent and reputable firms.” In addition, he made federal action against business deceptions a central feature of his “Great Society” agenda, calling for legislation that would establish “new legal remedies” for misleading packaging, deceptive consumer lending terms, “sharp and unscrupulous” selling of interstate real estate, and conflicts of interest in the management of pension plans.13

Reversion of the White House to Republican control in 1969 did not prompt a wholesale rhetorical shift on these issues. Emulating his two predecessors, President Richard M. Nixon issued yet another special message to Congress, assuring the nation that “Consumerism... is here to stay” and that federal government remained committed to a “Buyer’s Bill of Rights” that included “the right to accurate information” that enabled the consumer “to make his free choice.” Nixon advocated several legal reforms designed to strengthen protections against marketplace deceptions and “dishonest... competitors,” including easing the rules for bringing federal consumer class-action lawsuits (though also requiring that such suits could only proceed after successful criminal prosecution of a business by the Justice Department), expanding the FTC's authority to ask for injunctions against deceptive corporations, and improving disclosure of warranty terms for durable goods.14

Such presidential pronouncements were augmented by new consumer offices. In 1963, President Kennedy established a White House Council on Consumer Affairs; the following year, President Johnson appointed Esther Peterson, a long-time activist in the consumer and labor movements, as head of the new council and Special Assistant to the President on Consumer Affairs. Although possessing a modest budget and still having other responsibilities in the Labor Department, Peterson gave consumer advocates a point person within the White House and kept in close contact with federal agencies and elected officials who focused on consumer issues. She also traveled the country to give speeches to consumer groups and business organizations, wrote extensively on consumerism, and stood ready to testify before Congress.15 After Peterson resigned her position in 1967, Johnson replaced her with Betty Furness, a career actress with close ties to Democratic Party leaders but far less experience involving consumer matters. Furness nonetheless developed a reputation as an effective opponent of the “rackets” that victimized “the elderly, the uninformed, the sick, and the poor.”16

President Nixon transformed the Advisory Council into an Office of Consumer Affairs within the White House, which he characterized as obliged to “take a leading role in the crusade for economic justice.” Nixon further asked Congress to create a Consumer Protection Division within the Department of Justice, which would have the authority to investigate consumer abuses, represent consumer interests before Congress and federal agencies, and coordinate enforcement efforts related to consumer protection statutes. He also urged every state that had not already done so to enact its own consumer protection law and establish a dedicated enforcement body. Nixon's appointee to head the White House office was Virginia Knauer, the former head of the Pennsylvania Bureau of Consumer Protection. Like Peterson and Furness, Knauer maintained a grueling travel and speaking schedule in order to keep consumer issues in national headlines. Through speeches and congressional testimony, Knauer depicted consumer fraud in even graver terms than had her predecessors, referring to it “as an insidious economic cancer which eats at the vitals of our society.” Deception by the “white collar fraud-robber,” she warned, threatened popular faith in the rule of law. It also “withers our moral fiber... [,] misdirects our economic resources... [, and] saps the strength of our free enterprise system.”17

By identifying consumer protection as a national priority and characterizing business fraud with such stark images, the Kennedy, Johnson, and Nixon White Houses greatly enhanced the place of consumer fraud on the nation's policy agenda. Their administrations took place toward the end of a period of growing presidential influence, in which the challenges of depression, world war, and the struggle against communism had consolidated power in Washington, the executive branch, and the White House. It was also the “golden age” of broadcast television, which allowed the head of the Executive branch unmediated access to the citizenry at large. In an era in which presidents often framed public debate, their imprimaturs mattered, even if specific legislative proposals did not always meet the approval of more militant consumer organizations. Presidential insistence about the salience of any specific issue deepened public awareness of it. Such presidential blessings also stimulated more news coverage and journalistic investigations, galvanized the academics, interest groups, politicians, and career bureaucrats who most cared about an issue, and encouraged new policy ideas and more intense coalition-building.18

Within Congress, a cluster of long-serving members carved out complementary niches as champions of tougher consumer fraud policies. These public servants had imbibed the critique of unregulated capitalism and the positive view of governmental power ushered in by the New Deal. Democratic Senator Warren Magnuson of Washington, one of the most committed consumer advocates on Capitol Hill, encapsulated this perspective in The Dark Side of the Marketplace, a well-received 1968 book that assessed numerous threats to economic welfare, health, and safety. As Magnuson confidently remarked in the book's introduction, he was “certain that we all share the common conviction that... it is no longer a question of whether the consumer will be protected, but rather a question of how.”19 Magnuson, along with hundreds of elected officials who shared that conviction, believed that the state could redress socioeconomic problems. These national politicians, like their counterparts on the state level, also calculated that seeking out concrete strategies for combating business fraud would cement their stature and popularity. Like Magnuson, most of these congressmen and senators were Democrats who hailed from more industrialized parts of the country, such as the Midwest, Northeast, or Pacific Coast. Among senators, they included Paul Hart of Michigan, who became a key advocate for fair packaging and labeling legislation; Paul Douglas of Illinois, the chief proponent of truth in lending reform; and Harrison Williams of New Jersey, who provided leadership on the issue of fraudulent interstate real-estate developments. In the House, Democrats such as John Moss of California and Howard Rosenthal of New York City emerged as prominent sponsors of antifraud legislation. These elected officials convened the legislative hearings and sometimes asked for the agency studies that built an evidentiary case for reform. They oversaw the drafting process by staff and managed bills as they moved through committee, floor consideration, and final negotiations among congressional leaders and the White House.20

Despite the central role of elected officials in turning domestic policy agendas toward the problem of business fraud in the early 1960s and maintaining public focus thereafter, the strategic preferences of consumer activists increasingly shaped legislative and administrative action. Once the newer consumer organizations and lawyer-activists had gained a footing in cities, state capitals, and Washington, DC, they had perches from which to influence policy discussions. This growing clout manifested itself at every stage of the policymaking process, as illustrated by the hearings on consumer law held by a Senate subcommittee in 1969 and 1970. Convened to consider responses to legislative proposals that would strengthen the FTC's ability to fight consumer frauds, the subcommittee's witness list included trade association representatives and corporate CEOs. Unlike the discussions that produced fur- and wool-labeling legislation in the 1950s, however, Congress now invited consumer organizations to the policymaking table. Indeed, the hearings were set up by testimony from representatives of these groups—George Gordin, Jr., of the National Consumer Law Center; Walker Sandbach, executive director of Consumers Union; and Edward Berlin, general counsel of the Consumer Federation of America. As consumerism took hold in the United States, its leaders began to shape the legislative agendas and the formulation of specific policy proposals, and antifraud reforms took on a more populist hue.21

The individual who had perhaps the greatest role in setting the broader consumerist agenda, activist lawyer Ralph Nader, did not take the lead in channeling calls for action against consumer fraud, though he did give the issue some attention. In 1969, Nader charged a group of law students to prepare a detailed study of the FTC itself, focusing on its regulation of deceptive marketing practices. The result was a critical report that helped to lay the intellectual foundation for later FTC reforms. He also drove the longstanding and eventually unsuccessful effort to create a national Consumer Protection Agency, which would have had the power to investigate issues related to consumer fraud, monitor fraud-related enforcement efforts, and shape new regulatory initiatives. But Nader focused far more on other consumer issues, such as product safety, environmental protection, the reinvigoration of antitrust enforcement, and the selective dismantling of industry-specific regulatory structures. As a result, the consumerist challenge to deceptive marketing had more of a pluralist flavor, with studies and proposals emanating from across the new organizations that emerged in the 1960s and 1970s.22

A Wave of Regulatory Action

At all levels of government, elected, appointed, and career officials at once recognized and emboldened advocates of enhanced consumer protection measures. Public servants sometimes transformed the more diffuse popular sentiment for enhanced consumer protection into concrete reform proposals, and more frequently appropriated the ideas put forward by academic experts and consumer organizations. They built coalitions within legislatures and executive agencies for new antifraud policies and engineered compromises to overcome entrenched opponents of change. Argument by argument, hearing by hearing, and debate by debate, they deepened the legitimacy of using public power to beat back the unscrupulous bait and switch artist and peddler of misrepresented goods, services, and investments. The result was a groundswell of antifraud reforms adopted between the Kennedy and Ford administrations, in Washington, state capitals, and cities alike.

At both the national and state levels, regulators and legislators took aim at the decades-old problem of spurious cures and medical treatments. Officials at the Food and Drug Administration (FDA) spearheaded the most comprehensive initiatives, as when they convened three massive National Congresses on Medical Quackery with the AMA in 1961, 1963, and 1966. These meetings of medical experts and policymakers highlighted the extent to which false “medical messiahs” still preyed on the sick and terminally ill, and helped to galvanize support for tightening up marketing regulations. The most important congressional response came in the 1962 amendments to the Food and Drug Act. This legislation shifted regulatory authority over the advertising of medical products and services from the Federal Trade Commission to the FDA, mandated scientific proof of medical efficacy before firms could market drugs or other treatments, and required meticulous attention to scientific studies in the making of any therapeutic claims.23 Within the states, more vigorous regulation of fraudulent healthcare providers occurred partly through occupational licensing boards. Several states also adopted “pure drug statutes” and regulatory oversight bodies patterned on national policy frameworks, in the hopes of rooting out adulterated, misbranded, and sham medical products.24

Leaning on the Democratic congressional supermajorities of the mid- 1960s, consumer advocates enacted a trio of antifraud measures: the 1966 Fair Packaging and Labeling Act, the 1967 Interstate Land Sales Full Disclosure Act, and the 1968 Truth in Lending Act. Each of these statutes again sought to redress imbalances in information by requiring businesses to furnish purchasers with truthful, standardized statements as to the quantity, quality, and cost of goods, assets, or credit; each further authorized the FTC to enforce these disclosure obligations.25 State and local governments embraced a slew of additional antifraud proposals. One popular reform imposed mandatory cooling- off periods—two or three days in which customers could cancel purchases or contracts—in commercial sectors notorious for high-pressure tactics, such as home improvement repairs. Several jurisdictions also tightened the regulation of consumer credit arrangements.26

Within the realm of investor protection, more expansive governmental reforms occurred through legislation and administrative action, often driven by appointed officials and career civil servants at the SEC. The mid-1960s revamping of New Deal securities regulation, which was set up by the SEC's nineteen-month Special Study of Securities Markets, stands out for this type of policy entrepreneurship.27 Taking place at the start of the Kennedy administration, the Special Study was a response to a fraud scandal on the American Stock Exchange (AMEX). In 1960, regulators and the press discovered that for nearly a decade, the Re brokerage firm, a leading voice in internal AMEX governance, had engaged in market manipulations and insider trading.28 This incident might have generated a fairly narrow assessment of the shortcomings in AMEX self-regulation. Instead, SEC commissioners William Cary, Jack Winter, and Emanuel Cohen opted for a much broader inquiry. Recognizing that the financial markets had undergone profound transformations since the start of the New Deal, they convinced Congress to furnish $750,000 (as a share of the economy, roughly equivalent to $22 million in 2016 dollars), for an examination of shifting investing practices and the evolution of regulatory institutions. The commissioners asked Milton Cohen, a leading securities lawyer with SEC experience, to oversee the investigation. Its charge was to examine regulatory relationships among investment banks, corporations, and brokerage firms, on the one hand, and stock exchanges, professional gatekeepers, the NASD, and the SEC, on the other. Cohen agreed, but only after securing guarantees that the commission would not be able to demand revisions of study findings.29

Through confidential questionnaires to brokerage firms and detailed interviews of regulators and individuals who worked within the financial markets, Cohens team of sixty-five veteran staffers amassed a mountain of evidence. They traced the emergence and rapid growth of institutional investors, documented the regulatory challenges posed by a quadrupling in the frequency and value of securities transactions since the 1930s, and completed several case studies of malfeasance and conflicts of interest on the part of securities promoters and stock brokerages. The team of lawyers and analysts then crafted detailed recommendations for legislative reforms.30 Upon the completion of the Special Study, the SEC convened a liaison committee with finance leaders to draft formal legislative proposals. Although Congress did not accept every one of the Special Study's recommendations, its monumental final report established an evidentiary and conceptual basis for the next fifteen years of national legislation regarding securities regulation. The chief antifraud measures of the 1964 Amendments to the Securities Acts, including a significant expansion in the number of firms subject to disclosure rules and NASD membership, and imposition of tighter regulatory oversight of sales practices by brokerages, emerged from the Special Study.31

Richard Nixon's victory in 1968 did not temper the SEC's commitment to full disclosure and candor in the securities markets. Acting at the request of SEC staff attorneys who wished to expand the agency's enforcement tools, federal judges acceded to requests for disgorgement and restitution orders that furnished at least partial compensation to defrauded investors. The judiciary further accommodated the filing of private class-action suits by lawyers representing large numbers of similarly situated disgruntled investors.32

During the 1960s and 1970s, the clear trend remained placing higher regulatory barriers in the way of promoters, stock dealers, or corporate officers who wished to pull fast ones on the investing public. Born out of profound economic crisis, the New Deal administrative structures that sought to constrain securities fraud became entrenched features of the financial marketplace. These frameworks came to enjoy bipartisan support among political elites (though Democratic administrations in the 1940s and 1960s proved more willing to extend antifraud rules than did the Eisenhower administration). Despite initial antagonism from some parts of the financial sector, the cratering of business during the 1930s led a generation of stockbrokers, investment bankers, accounting firms, and securities lawyers to accept both the new regime of information disclosure and the more extensive prohibitions against market manipulation and insider trading. As SEC career attorney David Silver later recalled, in the post-World War II decades, “there were a lot of memories of the trials and tribulations of Wall Street, how the shenanigans of Wall Street really fit into the Great Depression.... [T]here was a general perception that the misbehavior of financial institutions had an awful lot to do with what happened in the country.” This view was widely embraced within the halls of the SEC, whose staff shared a conviction that honest communication was not only crucial to the proper working of capital markets, but also for their broader democratic legitimacy.33

Deceptive claims in the booming domain of business franchising attracted similar regulatory attention. This mode of business organization had been a feature of the American economy since the mid-nineteenth century. But it burst onto the suburban landscape after World War II, as franchisors offered American consumers reliability in goods and services (branded clothing, fast food, motels) while achieving the economies of scale that came with a national or regional footprint. Purveyors of retailing concepts liked franchising because it slashed the capital costs and risks associated with expansion, while securing the entrepreneurial energies and sweat equity of franchisees. Franchise owners appreciated the business training that they received, the extensive advertising campaigns mounted by the home office, and buy-in requirements that were less than the capital needed to launch standalone small businesses.34 The meteoric growth of postwar franchising, however, elicited duplicitous sales practices. Plenty of advance-fee scams tempted Americans to chase after the dream of proprietorship by throwing their savings at nonexistent franchisors. Many prospectuses for legitimate franchising opportunities also downplayed the number of competing franchises in an area and the implications of ongoing financial obligations, while exaggerating likely income streams.35

Beginning in the late 1960s, policymakers took regulatory aim at these problems. Once more, the dominant instinct was to protect would-be smallbusiness owners with strategies of information disclosure. Through an array of civil actions brought by aggrieved franchisees, state and federal judges signaled a willingness to treat franchise contracts as investments subject to the New Deal regime of securities regulation. State legislatures also enacted laws that compelled franchisors to furnish prospects with detailed, truthful information about their training programs, ongoing financial obligations, and calculation of franchisee earnings projections. Drawing on the provisions of these state statutes, the FTC followed suit with a Franchise Disclosure Rule. This administrative action, which took a full six years to move through the rule-making process, imposed extensive informational obligations on franchisors operating in interstate commerce.36

The congressional pinnacle of twentieth-century efforts to curb deceptive retail marketing occurred in 1975, with the passage of the FTC Improvement Act. This legislation gave the FTC authority to combat commercial deceit through its own administrative rule-making, which could create legally binding standards for industries or even the entire economy. It also augmented FTC enforcement powers. The commission could now seek substantial fines from businesses that did not comply with cease and desist orders or that violated an FTC administrative rule, as well as financial restitution for consumers harmed by such actions. FTC officials soon flexed their new muscles, notifying scores of corporations about their potential liability for deception-related fines and considering several far-reaching substantive rules. The most consequential, adopted in 1976, did away with the holder in due course doctrine concerning debt collection. This legal standard, once exploited by nineteenthcentury lightning-r od salesmen and then a mainstay of urban retailers of durable goods, had long protected third-party holders of consumer debt, such as finance companies, from legal defenses that the underlying commercial transaction had resulted from fraud.37 Even before the passage of the 1975 legislation, FTC officials experimented with ways to exert more pressure on national advertisers, introducing a policy in 1971 that required corporations to substantiate the factual assertions in their ads and, in the case of a demonstrated lack of substantiation, to run “corrective advertising” that alerted consumers to prior “questionable claims.”38

In addition to targeting specific marketing deceptions or extending the enforcement powers of existing agencies, states and local governments established many new bureaucratic beachheads against consumer fraud. Some states followed the path blazed by Louis Lefkowilz in New York, carving out consumer protection offices within the office of the attorney general; others created standalone consumer protection departments or agencies. By 1974, all but six states had also codified their legal regulation of consumer fraud through general consumer protection statutes, following one of three basic approaches. In thirteen states, legislatures enacted “Little FTC Acts” that borrowed the broad statutory language that had created the federal agency's antideception jurisdiction. These states all gave some department investigative authority and bestowed enforcement powers such as cease and desist orders, injunctive remedies, and restitution mechanisms. A few went so far as to proscribe “misleading” claims.39

Other states embraced the basic framework of two model consumer protection laws developed in the 1960s by legal scholars, legal elites, and good governance bodies such as the National Conference of Commissioners on Uniform State Laws. The first of these, the Uniform Deceptive Trade Practices Act (UDTPA), laid out several categories of prohibited marketing tactics, including “misrepresentation of the geographic origin of goods, disparagement of goods, services, and businesses, bait advertising, [and] price misrepresentation.” Rather than relying solely on criminal enforcement or administrative action by a state agency, the UDTPA created private actions that could be brought by affected consumers. The second effort, the Uniform Consumer Sales Practices Act (UCSPA), was the least common legislative template. It targeted an even wider set of commercial transactions, proscribing “unconscionable” as well as “deceptive” behavior by merchants. It further gave the state agency charged with overseeing consumer protection issues the power to bring class-action civil suits on behalf of consumers.40

Amid the institutional ferment and confidence in robust government that characterized the late 1960s and early 1970s, urban officials joined the anticonsumer fraud bandwagon. Major cities such as Boston, New York, Jacksonville, Louisville, Chicago, and Seattle passed local ordinances that codified prohibitions against deceptive marketing and established their own Offices of Consumer Affairs or Consumer Protection Agencies. This flurry of institutionbuilding was matched by metropolitan county governments such as Long Island’s Nassau County, Maryland’s Montgomery County, and southern Florida's Dade County.41

The rise of consumerism also had far-reaching impacts on the realm of business self-regulation. BBB officials recognized that as unions created consumer offices to assist their members, as dozens of independent consumer groups emerged, and as more and more states and cities established consumer protection agencies, advertising and marketing self-regulation faced powerful new institutional competitors. These developments expanded both the number of voices seeking to shape antifraud policy and the potential venues for registering consumer complaints. BBB leaders such as Denver’s W. Dan Bell pointed to the tide of consumer regulation as they sought to persuade local and national businesses to increase their financial support of advertising selfregulation. As early as 1961, Bell berated other BBB managers and his own membership about the grave dangers facing “the Better Business Bureau movement.” The AFL-CIO’s Consumer Counselling Program and the reemergence of “professional consumer groups”; the looming creation of a Colorado State Consumer Fraud Bureau, or even a federal “Department of the Consumer”; the emergence of “exposure” books such as Vance Packard’s The Waste Makers and Frank Gibney’s The Operators, which stoked mounting “expressions of suspicion and distrust” from consumers about American business; all of these developments threatened to “siphon away an inestimable amount of ‘selfregulation’ and BBB strength.” Unless the business community replaced its “ ‘token’ financial backing” and “lip service” with resources to sustain meaningful self-regulation, Bell and other BBB executives warned, there was reason to worry about “the survival of the kind of economy under which America had grown to greatness—the free enterprise system.”42

A consensus also emerged by the end of the 1960s that the BBBs required not only more funding, but also a fundamental reorganization. Centralization of authority in a new Council of Better Business Bureaus, the thinking went, would improve the consistency of operations and allow individual BBBs to receive some income from the national organization, lessening dependence on local businesses. This approach would also enable the BBB network to make substantial investments in information technology to improve management of the overwhelming bits of information that crowded into BBB offices. A 1969 management consulting study by Knight, Gladieux, & Smith called for all of these changes, ratifying proposals that had long circulated among the Bureau's leaders. The BBB network immediately set about implementing them, without significant objections.43

For the BBB old guard who worked either at the national level or in metropolitan areas that were part of the Northeast, the Midwest, or the West Coast, the Bureau network needed to accommodate a historical transformation that was too strong to simply oppose. These leaders, including Kenneth Barnard, Victor Nyborg, John O'Brien (who had a long career running BBBs in Akron and St. Louis), and Edward Gallagher (who had run the Boston Bureau for decades) had spent their working lives learning how to cooperate with the steadily expanding antifraud state. Their strategic sensibilities meshed with the moderate conservatism of an Eisenhower or Lefkowilz. They accepted the basic structure of the welfare state and more vigorous antifraud policing, but looked to soften public antagonism toward business. These figures had built close relationships with antifraud regulators from both parties, though they leaned toward Republican regulators such as Earl Kintner who were strong supporters of business self-regulation.44

To veterans of “truth in advertising” campaigns, the social and political transformations that had put Kennedy and Johnson in the White House were irreversible. With consumer protection occupying a central position on the nation's policy agenda, they argued that the BBBs had to maintain a critical distance from business and deepen working relationships with consumer groups and governmental consumer protection agencies, so that its officials might continue their roles as regulatory brokers. Unless the organization adapted to consumerism, “recogniz[ing] the permanence of this ‘consumer voice' movement, and mov[ing] to join it in a more positive way,” the BBBs ran the risk of becoming irrelevant. If the network did adapt, it could take advantage of its favorable reputation, indicated by both opinion polls and the frequency of public contacts with local BBBs, to shore up its position as a “respected, independent” guardian of commercial morality, an “even-handed... informal court of appeals” for “the customer.” The goal, as one insurance executive with close ties to the BBB movement argued in the fall of 1971, was one of “triangulation: Find the point in the center of, but equidistant from, business, the Federal Trade Commission, and Ralph Nader.”45

In Chicago, longtime BBB head Kenneth Barnard followed this logic in responding to proposals for the creation of an Illinois Bureau of Consumer Fraud. Barnard supported the idea, though only if the new agency would concentrate on prosecuting the worst offenders, thereby increasing the leverage that BBB officials could exert on firms. For officials such as Victor Nyborg, this kind of political flexibility would not only make antifraud work more effective, but also inoculate Bureaus against charges of “always needing to be against everything.”46

The BBB strategy of triangulation further extended procedural protections for businesses that ran afoul of its standards for truth in advertising. In 1971, the Advertising Federation of America, the American Association of Advertising Agencies, and the Association of National Advertisers agreed to the creation of a National Advertising Review Board (NARB), which would be run under the auspices of the newly formed Council of Better Business Bureaus (CBBB). Drawing on proposals that had circulated among BBB officials since 1960, as well as a British system of advertising self-regulation that had begun in 1962, the NARB comprised five-person panels selected from fifty board members—thirty executives from national advertisers, ten representatives of the advertising industry, and ten independent experts on marketing, who were to represent the public. It heard cases of alleged marketing deception whenever advertisers disputed the findings of the CBBB’s newly formed National Advertising Division (NAD), which had the responsibility of monitoring television, radio, and national publications and assessing allegations of misrepresentation. The NARB could also take jurisdiction whenever a public complainant objected to an NAD ruling that an ad was not so deceptive as to merit action.47

The procedural mimicry of the administrative state by the BBBs did have limits. Local BBBs did not institute formal hearings in advance of decisions to issue a NIPI directive against an advertiser, nor ensure that the official who authorized the NIPI did so without any prior knowledge or involvement in the case; most bureaus did not create review boards of any kind; and those that existed did not, like the NARB, create a public record of their proceedings and determinations. Indeed, when the Little Rock BBB’s Advertising Review Board experimented in the mid-1960s with the creation of written rulings and a requirement that media outlets abide by NIPI declarations as a condition of BBB membership, the FTC ruled that such formal processes overstepped the bounds of legitimate self-regulation, shading over into the realm of illegal restraints on trade.48 In order to skirt similar legal concerns, the ad industry limited the NARB’s sanctions to publicity and formal referral to the appropriate federal agency, usually the FTC. Still, the day-to-day regulatory efforts of BBBs testify to the salience of due process as a postwar institutional ideal.

The antifraud institutions created during the late 1960s or 1970s relied heavily on young turks fresh out of college or law school, sometimes with an internship or a year or two of work for community organizations under their belts. In the state and local consumer protection agencies, many leaders were true believers with experience in the consumer movement rather than politicos who spied a popular wave. Several of these appointees came from the growing ranks of activist lawyers. Philip Schrag, consumer advocate in the New York City Department of Consumer Affairs (DCA), had served as a community lawyer working for the National Association for the Advancement of Colored People (NAACP) Legal and Educational Defense Fund. Others hailed from the journalist’s consumer beat or came up the ranks of government agencies with consumer-related missions. In Minnesota, the head of the State Consumer Service during the early 1970s, Sherry Chenoweth, had covered consumer issues as a local television reporter. The inaugural head of the Los Angeles Consumer Affairs Bureau, Fern Jellison, had several decades of experience in the city office charged with regulating charities. In Chicago, Jane Byrne became the head of that city’s Department of Consumer Sales, Weights, and Measures after years of Democratic Party activism and positions in city antipoverty programs.49 One of the most prominent local consumer agency leaders, New York City Commissioner of Consumer Affairs Bess Myerson, turned to consumer protection from a career as a model and television actress that had been kick-started by her winning the Miss America pageant in 1945. Although Myerson faced derision upon assuming office, she used her celebrity status to expand public awareness of consumer programs and build political support for them.50 Regardless of the career avenues that led to leadership in local consumer protection bureaucracies, these positions attracted energetic figures who embraced consumerism and policy experimentation.

In numerous policy domains, the New Deal and Cold War eras generated state-building predicated on linkages to a dense network of quasi-public and nongovernmental institutions. The national defense establishment drew on the analysis furnished by social scientists based in universities, think tanks, and nonprofit organizations. The New Deal farm state incorporated not only new programs within the federal Agriculture Department and companion statelevel agencies, but also a complex set of organizations that spoke for farmers and farmworkers, as well as elected committees of local farmers, who had responsibilities for implementing federal agricultural programs. Regulatory governance over the content of American film, radio, and television relied on industry self-regulatory bodies. Post-World War II federal grant programs in healthcare and higher education depended on quasi-public mechanisms of accreditation.51 The elaboration of the American antifraud state mirrored these other complex regulatory ecologies. By the mid-1970s, the antifraud terrain encompassed not only a thicket of public laws and administrative rules adopted by every level of government, but also myriad public and quasi-public agencies, as well as a burgeoning army of private watchdogs and gatekeepers.

Within all of these institutions, regulatory protagonists shared, for the most part, the premises that Warren Magnuson had articulated in his preface to The Dark Side of the Marketplace. Consumer and investor protection, including protection against mendacious businesses, was a fundamental element of government. American marketplaces should not operate according to the unforgiving logic of caveat emptor. As FDR had argued in his message to Congress on securities regulation, sellers had obligations to customers, competitors, and the wider society. They, too, needed to look sharp, lest they run afoul of the many legal prohibitions against dishonest marketing and the mushrooming public and quasi-public institutions charged with enforcing them. Consumer activists such as Colston Warne, the Amherst economics professor and longtime president of Consumers Union, and business regulators, including Republicans such as Louis Lefkovitz and FTC Commissioner Paul Rand Dixon, pressed this argument repeatedly. They insisted that “caveat emptor has now become outmoded and caveat venditor must be the foundation of the marketplace”; that “protection from some business frauds cannot be afforded except by government protection”; that “the obsolescent and socially destructive idea of caveat emptor should be appropriately buried as a relic of the days of simple markets and well-understood commodities.”52

A diverse chorus of voices from the business community ratified this turn away from caveat emptor. As early as 1960, the Advertising Federation of America characterized the legal principle of caveat venditor as a “fact” that advertisers ignored at their peril. By the late 1960s and early 1970s, this premise suffused business discourse. A Rhode Island paint dealer who wished to boast of his quality products could title a newspaper advertisement “Caveat Vendi- tor,” while a manufacturer of construction materials could trumpet in its 1972 annual report that it had long ago replaced “caveat emptor” with the principle, “Let the buyer have faith.” Even the conservative United States Chamber of Commerce conceded that commercial fraud was “Everybody’s Problem, Everybody’s Loss.”53

The inclination to bow before the dictates of consumerism did not quash disagreements over the best means to hold mendacity in check, nor disputes over how tightly constraints on sellers should pinch. In his 1969 message on consumerism, for example, Richard Nixon drew distinctions between his views and those of many consumer activists and Democrats. His steadfast commitment to a Buyer's Bill of Rights, Nixon explained, “did not mean that caveat emptor... had been replaced by an equally harsh caveat venditor” nor that “government should guide or dominate individual purchasing decisions,” a view that pleased the conservative Chicago Tribune.54 The Chamber of Commerce accepted that consumer fraud was a national problem, but still worried about excessively “rigid and cumbersome” antifraud legislation and preferred solutions that depended on mechanisms of business self-regulation.55 For all the efforts of BBB leaders to cast their organization as a “militant instrument of impartial enforcement” and a steward of “the public trust,” they embraced negative conceptions of economic liberty associated with American conserva- tivism. The BBB's core mission was to safeguard the “free enterprise system,” whether from confidence-s apping swindlers and chiselers, heavy-handed government bureaucracies, or impatient and unfair consumers.56 The politicians and interest groups with such viewpoints did not shy away from voicing their concerns in debates over fraud policies. Because of their influence, even the most aggressive antifraud legislation emphasized regimes of information disclosure that would empower consumers and investors to make better choices. And in states controlled by Republicans or conservative Southern Democrats, consumer fraud measures stressed cooperation with the business establishment.57

Nonetheless, it is striking how often participants in the 1960s and 1970s debates over antifraud policies framed the formal shift away from caveat emptor in epochal terms. In reviewing The Dark Side of the Marketplace, Morton Mintz, a Washington Post political reporter, commented that the older injunction that buyers beware “should have died centuries ago and been buried alongside those primitive deities in whose names millions of goats, sheep, and virgins were sacrificed.” Before a 1971 audience of business executives, Elizabeth Hanford, Nixon's deputy assistant for consumer affairs, remarked that “the days of caveat emptor are past and the days of caveat vendor are at hand.” Even a professor of marketing at a Louisiana university, writing in 1974 for a publication read chiefly by sales managers, judged that the United States had “entered a new and extended era in which the possibility of class-action suits coupled with the adequate enforcement of federal and state consumer legislation means the seller also must beware. The day of caveat vendor is here!” The exclamation point suggests the degree of confidence in the durability of this new regulatory world.58

We shall have occasion to revisit this confident prediction of a new age of legal antagonism to the business cheat in light of contrary developments over the subsequent four decades. For the moment, we should take note of its central assumptions about the educational force of new antifraud rules and the impact of fraud enforcement. New language in the statute books, the daily compilations of rules in the Federal Register, and the pronouncements of state and local consumer protection agencies did not necessarily transform legal and commercial culture. Policy innovations did not automatically remake norms nor elicit “adequate enforcement” in the 1970s any more than in the 1870s, 1920s, or 1950s.

Retracing Paths of Education and Enforcement

The early twentieth-century movement for “truth in advertising” had invested first and foremost in public outreach, on the theory that the best way to constrain fraud was to inoculate potential victims against the enticements of get- rich-quick promoters, slick salesmen, and deceptive ads. The BBBs had retained this focus after World War II. As consumerism gained momentum in the 1960s and early 1970s, every antifraud organization, whether established by statutory authority or private initiative, did likewise. Investments in public education were cheap and embraced by politicians across the political spectrum. Who could object to attempts to steel investors and consumers against the wiles of the shape-shifting sharper?

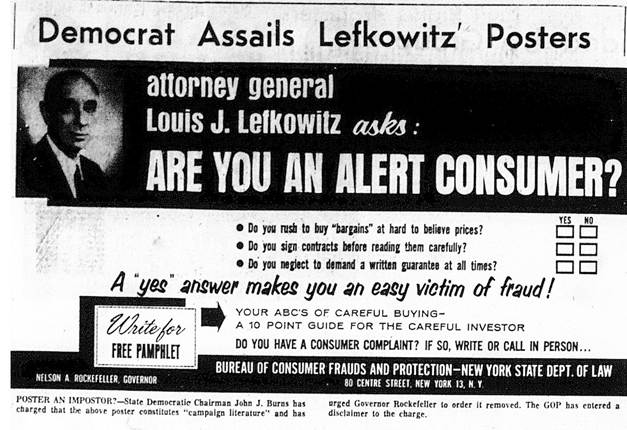

The flurry of informational posters, booklets, and pamphlets emanating from antifraud organizations intensified after 1960. Public education efforts turned to short films such as The Fine Art of Fraud, a twenty-minute overview of fraud techniques produced by the New York attorney general's office in 1966, radio and television spots, and consumer-related high school and college curricula.59 Whatever the medium of communication, the content mirrored the basic messages conveyed by antifraud journalism. Most materials explained prevalent swindles and recommended that investors or consumers rely on professional experts to guide their economic decision-making. In case these messages did not hold the rip-off artists at bay, public education campaigns implored victims not to suffer in silence, but rather to “be public spirited and make a big squawk.” Like their counterparts earlier in the century, post-World War II antifraud organizations argued that “by making known your dissatisfaction, you may save others from being victimized.” The consistent plea, like the messaging of the NACM during their Progressive era battles against credit

Figure 10.1: Poster from the New York Bureau of Consumer Frauds and Protection, 1966. Reprinted from the Albany Times-Union, Aug. 11, 1966, with permission.

fraud, was one of social obligation—to “Help Protect others” by “making it more difficult for the... disreputable retailer to do business.” To facilitate such communitarian goals, antifraud communications, such as a 1966 poster from the New York State attorney general’s office (Figure 10.1), made a point of explaining where consumers or investors could seek assistance from nongovernmental consumer groups and state agencies. They also detailed how to put together an effective complaint.60

For all the heightened attention in the 1960s to commercial predation faced by the urban poor, the educational materials produced by the antifraud state targeted a middle-class audience. In beseeching readers to run investment ideas by a banker or financial adviser, the authors had professionals and small business more in mind than day laborers or the rural poor. The Fine Art of Fraud included dramatizations of bait and switch marketing by a travel agent hawking European vacations to a pair of white schoolteachers, as well as a high-pressure pitch for a referral-selling scheme, made by a cultured salesman to a prim white couple in their comfortable suburban home. These were not the scams operating in the Puerto Rican neighborhoods of the Bronx, on the South Side of Chicago, across the Watts neighborhood of Los Angeles, or in the hollows of Appalachia. Graphics in consumer protection pamphlets re-

fleeted comparable expectations about readership. For the Washington attorney general's office, the image of the consumer who had to watch out for bait and switch advertising was a well-coiffed middle-aged white woman. When Pennsylvania's Bureau of Consumer Protection (BCP) crafted a “buyer's bible,” its choice of a prototypical purchaser was “Conrad Consumer,” an “average family man” depicted in cartoon form as a young middle-class white father in a cardigan sweater.61

In the wake of the 1960s summer riots that devastated poor neighborhoods in many large cities, the new consumer protection agencies and older self- regulatory agencies brought educational messages more directly to those inner city communities. In addition to setting up branch offices, state and local antifraud organizations put out Spanish-language versions of publications, equipped mobile outreach buses that could bring pamphlets and seasoned antifraud professionals to city neighborhoods, and participated in local consumer fairs. New York City's BBB hired African American consumer specialists to staff its new Harlem branch and commissioned the film Just Sign Here, which focused on frauds endemic to poorer communities rather than schemes that targeted those higher up the income ladder. At the national level, the FTC established a companion Consumer Protection Office for the District of Columbia, held a series of hearings on inner-city consumer fraud, and prioritized the hiring of African Americans for the consumer protection division.62

Community-based consumer and civil rights organizations, which possessed far more legitimacy within poor urban neighborhoods than most state or business-linked agencies, launched their own educational efforts. In Philadelphia, CEPA's monthly newspaper, Consumer Voice, mixed in-depth reporting on the marketing abuses afflicting poorer consumers with a hard-edged editorial posture. In San Francisco, the antipoverty organization Bay Area Neighborhood Development (BAND) set up a network of offices to assist consumers. BAND produced booklets that warned low-income residents about all manner of consumer deceptions, imploring readers, “FIGHT BACK! DON'T LET THE GYP ARTISTS GET AWAY WITH IT!”63 Regardless of the social milieu generating the outpouring of antifraud instruction, one might be tempted to see it solely in terms of the unending struggle to wise up individuals, whatever their ethnicity, race, gender, or social class. But a key goal of outreach, in this period as much as the Progressive era, was to buttress social norms against manipulative modes of selling.

State and local antifraud agencies also followed their predecessors in building informational networks and clearinghouses. Attorneys general built mechanisms to collect timely intelligence on fraudulent business activity in their states, and to share that intelligence with state agencies, local police departments, and prosecutors. Louis Lefkowitzs office again laid the foundation for such initiatives during the late 1950s and soon attracted imitators. In 1962, Maryland Attorney General Thomas Finan asked the State Police to establish a “special six-man intelligence unit” to aggregate information from local authorities about prevalent rackets and identify emerging statewide trends. By the mid-1960s, the Consumer Fraud Unit of the California attorney general's office had developed a far more ambitious framework, using reports that came in from local police and prosecutors as a basis for “multi-county fraud investigations” and “statewide criminal crackdowns.” Other states developed variations on this approach, including policy councils that brought local prosecutors together with state officials responsible for consumer fraud, and statewide computer databases on fraud investigations and prosecutions.64

These more sophisticated enforcement networks facilitated a growing number of city-specific and statewide prosecutorial sweeps, which targeted the chicanery that went on in many automobile dealerships, home improvement companies, television repair shops, and purveyors of miracle health cures. On occasion, local law enforcement moved in response to specific newspaper exposes and indignant editorial demands for action. With the rising tide of consumerism, more prosecutors saw great value in gaining notice as inveterate foes of rackets.65

Press releases, newsletters, and annual reports from these agencies trumpeted statistics and capsule summaries of successful enforcement actions, such as criminal convictions, fines, injunctions, consent decrees, and orders of business dissolutions. So, too, did a steady stream of articles on consumer fraud enforcement produced by attorneys general, heads of Consumer Protection Offices, and district attorneys for law reviews.66 Sometimes state-driven undertakings even zeroed in on larger business frauds with national reach. In the early 1970s, authorities in more than thirty states drew on their new antifraud powers to shut down Glenn Turner's pyramid sales schemes, which he had organized through the Koscot Interplanetary and Dare to Be Great corporations. Turner's business model involved selling cosmetics and then motivational books and tapes through multilevel distributorships, in which franchisees earned income through commissions earned by recruiting new franchisees. He pitched these distributorships through revivalist weekend- long meetings, held in convention centers. From Oregon to Michigan to Mississippi to Maryland, state prosecutors brought dozens of successful injunctive proceedings and criminal cases against Turner enterprises and midlevel franchisees.67

The Turner cases attest to the networks that state and local antifraud officials built to share policy ideas and enforcement techniques. Fraud fighters met at conferences convened by the National Association of Attorneys General (NAAG) and the Department of Justice. The NAAG published annual surveys of consumer fraud regulation, compiling statistics on consumer protection budgets and staffing and tracking legislative and administrative trends. Such efforts were accompanied by an uptick in academic scholarship on investor and consumer protection, as well as in news coverage. Ideas about how to combat business fraud circulated through all of these channels, encouraging national convergence of antifraud strategies.

In part because of this deepening antifraud network, the champions of consumerism remained aware of the enduring obstacles that confronted criminal fraud prosecutions and administrative antideception proceedings. By the early 1970s, the legal system's soft treatment of fraudulent business owners (and white-collar criminals more generally) was considered commonplace by prosecutors and legal sociologists.68 Recognition of this pattern also seeped into popular sentiment, sometimes prompting indignant protest after guilty verdicts for prominent businessmen led only to trifling sentences. In 1975, after a prominent San Diego banker received a suspended two-year sentence for a multi-million-dollar bank fraud, readers of the Los Angeles Times seethed in anger. To the twenty-five letter writers moved to comment about legal proceedings a two-hour drive away, the case showed that “America operates two systems of justice—one for the rich and powerful and another for the poor and powerless,” that “ 'lectric chairs ain't for millionaires,” that “you can't send Mr. San Diego to jail.”69

The men and women charged with running consumer protection agencies knew all about cases such as Holland Furnace and were determined to avoid such outcomes by taking tougher stances toward deceptive sellers. They had fought hard to gain access to more potent enforcement tools, such as the power to ask for injunctions, dissolutions of incorporation, and mechanisms of compulsory restitution. In the most egregious cases, state and local consumer protection agencies deployed such authority to good effect, every year shutting down hundreds of abusive retailers and service providers. As with late nineteenth-century postal officials and early twentieth-century regulators at the FTC, antifraud reformers of the late 1960s and early 1970s hoped to sidestep the inefficiencies of the criminal justice system through more nimble modes of regulatory governance. Had consumer protection champions possessed a deeper grasp of history, they might have tempered their expectations. Forceful antifraud tactics tended to generate complaints about autocratic governance that ran roughshod over individual rights and American values, which then prompted adoption of procedural protections, which in turn limited the effectiveness of administrative remedies. Post-World War II proceduralism deepened the democratic legitimacy of antifraud regulation, but at the cost of extending the rights of accused businesses, whether in criminal or administrative contexts.

Such safeguards, in combination with judicial skepticism about business fraud cases, often stymied expeditious redress for consumers. Although New York City armed its DCA with the power to ask for injunctions against deceptive firms, the city's judiciary and the clerks on whom they relied for advice frowned on the rapid-fire action contemplated by Mayor John Lindsay's administration and its consumer protection officials. Even in cases with extensive documentation of predatory behavior by businesses, some members of the New York City bench harbored concerns about issuing injunctions, believing they should “only be granted sparingly” before a final court finding that firms had committed fraud. The resulting delays could sour victims on consumer protection agencies, convincing them that there was little justice to be found through recourse to the new champions of consumer rights.70

Once again, the effectiveness of antifraud agencies depended on the extent of funding. During the 1960s and 1970s, state legislatures in heavily industrialized states such as Illinois appropriated sums for consumer protection bureaus that allowed them to establish several satellite offices. In some of the largest cities, urban consumer protection bureaus had budgets and staffs of even greater size. A few suburban agencies, like the one in Long Island's Nassau County, received significant resources: by the early 1970s, it enjoyed a $376,000 budget, enabling it to employ a staff of almost fifty.71

But American proceduralism often went hand in hand with budgetary stringency for regulatory agencies. Congress, state legislatures, and city councils proved far more willing to adopt new regulatory schemes that targeted hucksterism than to appropriate generous sums for implementation. Most public agencies charged with enforcing antideception law operated on a shoestring. Consumer protection divisions within the attorney general's office or standalone consumer protection agencies usually had only a few staff members. Funding for city and county consumer bureaus proved even less munificent. The Los Angeles Bureau of Consumer Affairs launched in 1972 with only twenty-one salaried personnel to police marketing practices in a city of almost three million—“only one ‘fraud catcher' for every 166,000 people.” It enjoyed that many staff only because the city was able to obtain a federal grant to defray the costs. During the early 1970s, the entire city of Philadelphia relied on the efforts of a consumer affairs staff of just three people. When the Prince George's County, Maryland, Consumer Protection Commission opened its doors in 1970, it had only a single commissioner and two assistants. Most consumer agencies, moreover, had responsibility for a much wider set of consumer issues than just combating commercial duplicity.72 At the New York City DCA, a staff of 350, around fifty of whom worked for the enforcement division, still groaned under the weight of tens of thousands of annual consumer complaints. Matters worsened considerably in the mid-1970s, when the city's fiscal woes led to budget reductions.73

Like public antifraud regulators, self-regulatory organizations confronted the problem of insufficient bureaucratic capacity. After years of rapid growth in the number of BBBs, member businesses, and collective financial resources, the 1960s brought relatively flat budgets, even as demands from consumers, businesses, and governmental agencies intensified. The BBB network expanded by an additional twenty-two locals between 1962 and 1972, but the total funds for operating budgets did not keep pace, approaching only $9 million in pledged memberships by 1972, just $2 million more than in 1962.74

Pinched budgets led to staffing shortfalls and associated declines in the quality of service. A 1971 report on the BBBs, undertaken by several law school students at the direction of New York congressman Benjamin Rosenthal, chronicled the impacts on organizational performance. Pressed to respond to all the letters, phone calls, and consumer visits, many bureaus sharply curtailed their public hours. Even though this move rationed access and created consumer frustrations, the BBBs still battled to keep track of all the information that they received. As the reliability of their files diminished, many consumers who managed to get through to BBB employees received false impressions when they inquired about businesses. The Rosenthal Report, modeled on the Nader-funded assessment of the FTC, further found that budgetary pressures had led most local bureaus to compromise some of their most basic moral commitments. Many had outsourced recruitment of new members to sales companies that engaged in high-pressure sales tactics and no longer screened new members to check on reputations, nor expelled members that repeatedly violated BBB standards. Most of these conclusions echoed the pronouncements of the confidential analysis of the Bureaus conducted by the management consulting firm, Knight, Gladieux, & Smith in 1969.75

Together, punctilious proceduralism and tight budgets raised the likelihood that grievances about deceptive selling practices would take a long time to wind their way through the system (widening the practical openings for “quick kill[s]”) or fall through bureaucratic cracks altogether.76 The publicity surrounding the inauguration of state local consumer protection offices, in conjunction with a more general societal embrace of consumerism, only heightened such pressures. That publicity elicited a torrent of complaints, which immediately taxed investigative and adjudicative capacities. One common strategy was to turn to volunteers who could assist with monitoring and complaint-taking, much like the nineteenth-century journal subscribers who answered the calls to become informal antifraud sentinels.

Thus, in the late 1950s, New York Attorney General Louis Lefkowitz convened a statewide committee of “100 housewives” to serve as unpaid adjuncts. These middle-class women likely had experience working with community organizations; some may have participated in the citizen networks that monitored World War II consumer price regulations.77 Lefkowitz asked the volunteers to “observe conditions which affect the purse strings,” channel consumer complaints to his consumer protection office, and serve as community spokespersons who would “alert and educate the buying public in the techniques of slick salesmen.” The attorney general also drew on unpaid law student interns, who processed less complex consumer complaints. Over the subsequent two decades, most state and local consumer agencies developed similar strategies. In some cases, as in the California attorney general's office during the early 1970s, agencies recruited volunteers to serve as mystery shoppers, who visited stores to assess “the validity of advertisements [and] sales practices.” Reliance on volunteers and interns extended regulatory footprints. The Office of Consumer Protection in New Jersey's Burlington County, created in 1969, had only two salaried staff members. But after the creation of a “volunteer army of 50 persons” in 1971, as well as a weekly local radio show that solicited complaints, it was able to handle a much larger caseload.78

Despite such measures, many of the new consumer protection agencies struggled to satisfy complainants, in much the same fashion as local BBBs. All too often, consumers encountered recurrent busy signals, delays before investigators could look into their allegations, or “referral runaround,” as overwhelmed complaint-takers directed them to other consumer protection bureaucracies. Confusion over which local, state, or federal agency to approach became commonplace; so did dissatisfaction with the pace of regulatory action. In many cases, formal proceedings within local or state consumer affairs offices bogged down in a procedural morass, leading angry citizens to throw up their “hands in frustration after struggling through phone calls, letters, or visits” to multiple agencies. The most jaded consumer protection officials tried to deflect unhappy consumers as much as solve their problems; the most well intentioned often felt as if they were “sitting at the bottom of the ocean bailing with a tin cup.”79

In spite of intention and occasional practice, the antifraud monitors came to function as a mediation service. In 1962, the Illinois attorney general had described the new Consumer Fraud Bureau (CFB) as dedicated to prosecuting “merchants who habitually employ fraud.” A decade later, the CFB instead proclaimed that it was “the face-to-face legal representative” of the “citizen who feels that he has been duped or wronged in a consumer transaction,” and that its chief goal was “recovering the individual’s money whenever possible”80