CHAPTER NINE Moving toward Caveat Venditor

Shortly after Franklin Delano Roosevelt’s inauguration in March 1933, he sent a special message to Congress that called for federal regulation of the securities markets. Taking note of the “severe losses” that investors had incurred “through practices neither ethical nor honest on the part of many persons and corporations selling securities,” the new president asked for legislation that would require comprehensive disclosures by marketers of stocks and bonds.

The enormity of the Great Depression, he argued, demanded new standards for communication by public corporations, investment bankers, and other players in financial markets. In order to restore “public confidence” in mechanisms of capital allocation, Congress had to place “the burden of telling the whole truth on the seller.” Without oversight that ensured candor by the vendors of investments, Roosevelt proclaimed, stock exchanges and the bond markets would remain moribund, as shell-shocked investors shunned public securities.1Roosevelt’s plea represented a turning point in the policing of business fraud in the United States. After some wrangling over details, Congress acceded to his request, creating a powerful agency to supervise America’s capital markets, the Securities and Exchange Commission (SEC). Along with the 1938 Wheeler-Lea Act, which extended the FTC’s jurisdiction over duplicitous marketing, the creation of the SEC vastly expanded federal responsibility for regulating the truthfulness of economic speech. During the New Deal, the nation’s elected officials pledged to redress informational asymmetries within America’s industrialized, continental economy. They chose to act through robust bureaucracies that would monitor national marketplaces and combat deceptive business practices. These developments ushered in a half-century of intensive public action to constrain economic duplicity.

Congress, statehouses, and city councils passed legislation that attacked such deceit, both in general and with respect to specific markets such as retail trade, franchising, and consumer credit. From the late 1950s through the 1970s, states and municipalities also launched new agencies charged with combating business fraud.One must be careful not to overstate the degree of change associated with post-New Deal antideception regulation. Legislators and other policymakers had many earlier experiments upon which to build, and the fraud-fighting endeavors of the mid-twentieth century retained key features of those precursors. The waxing insistence that sellers face stricter standards at no point meant forsaking the assumption that economic actors had to be able to fend for themselves. Roosevelt explained that his call for tighter securities regulation did not absolve buyers from the duty to keep a sharp lookout. Rather, the proposal “adds to the ancient rule of caveat emptor [‘Let the buyer beware'] the further doctrine: ‘Let the seller also beware' [caveat venditor]” The crafting and implementation of New Deal securities legislation adhered to this formulation. Indeed, almost all of the antifraud policies enacted by American legislatures and regulatory agencies between 1933 and the 1970s were premised on due diligence by economic actors. Those policies also reflected abiding anxieties about extending too much power to administrative bureaucracies, whether through overgenerous budgetary allocations or the granting of undue discretionary authority. As a result, even at the height of the more expansive mid-twentiethcentury American state, nongovernmental and self-regulatory organizations continued to play key roles in the antifraud regulatory environment.

The Roosevelt administration's embrace of caveat venditor nonetheless signaled a shift in political discourse and policy. For the following four decades, American legislators and regulators from both political parties gave less credence to assertions of economic freedom, and worried more about preserving popular confidence in markets or treating economic actors fairly.

They also framed antifraud policies in terms of consumer and investor protection. Indeed, only with the New Deal did those phrases come into common currency.2The next three chapters survey American fraud policing from the New Deal through the 1970s. This chapter considers antifraud efforts into the early 1960s, focusing on federal regulation of the financial markets and retail marketing, as well as related undertakings by Better Business Bureaus. Chapters Ten and Eleven grapple with the impact of consumerism on antifraud regulation from the late 1950s through the late 1970s. Together, these three chapters document wide-ranging attacks on commercial deception through legislative statutes, administrative rule-making, and, in some contexts, judicial interpretation. They also chart the bipartisan construction of a much denser and more integrated network of antifraud institutions, both public and outside the state. Despite enduring constraints on the reach and effectiveness of antifraud regulation, all of this activity circumscribed the scale, scope, and impact of marketplace deceptions.

Institutional Designs and Intellectual Foundations

New Deal antifraud regulation was born out of anxieties about the securities markets, which focused on decades-long patterns of self-dealing, manipulation, and misrepresentation, given new intensity by the post-World War I boom and subsequent stock market crash. During the dramatic run-up in stock prices from 1920 to 1929, Wall Street depended on a wider base of shareholders. Having become accustomed to investment through the World War I Liberty Bond campaign, and bombarded by the hard-sell techniques of fastgrowing brokerages such as Merrill Lynch, several million middle-class Americans joined the investing class.3 These newcomers purchased not just the securities of established sectors such as banking, insurance, transportation, and mining, but also shares in manufacturing, retail firms, and investment trusts, as well as foreign bonds.

The mix of strong demand, unsophisticated purchasers, and weak regulatory constraints generated powerful incentives for deceit.As Chapter Five demonstrated, mail fraud enforcement had targeted stock and bond swindlers since the late 1870s, and interstate investment fraud became a more substantial priority for the Post Office Department in the 1910s and 1920s, resulting in scores of prosecutions and convictions. During World War I, the Treasury Department's Capital Issues Committee received the authority to scrutinize proposed initial public offerings and to disallow the marketing of any issues deemed to be inconsistent with the war effort. Far more substantial regulatory legislation occurred at the state level, with the outpouring of blue-sky laws.

Rather than truly discriminating filters, however, state regulatory schemes proved to be at once porous and overly restrictive. The former problem resulted from legislative exemptions, either for sectors such as utilities and banking, or for companies with listed securities. The Investment Bankers of America (IBA), founded in 1913 to fend off the threat posed by blue-sky laws, worked hard to establish safe harbors for stocks and bonds sold on exchanges. Woeful bureaucratic limitations further hampered state regulation. Legislative appropriations often allowed only cursory enforcement, and even the best- funded agencies did not constrain the tip sheets and telephone boiler rooms that drove interstate sales. At the same time, promoters inveighed against bluesky licensing requirements. To these apostles of enterprise, the new rules created legal “shackles” that only reinforced the power of established stock exchanges and investment banks, while placing a “strait jacket [on] industrial development.”4

Even New York's far-reaching attempts to curb securities fraud through the 1921 Martin Act and the creation of a dedicated Bureau for the Prevention of Fraudulent Securities (BPFS) faced important limits.

From 1925 onward, it distributed compulsory questionnaires to promoters and stock brokerages, so that it might learn about questionable practices even without specific complaints from investors.5 BPFS attorneys initiated thousands of fraud investigations during the 1920s and 1930s, pursued hundreds of injunctive proceedings to force firms out of business, and brought scores of criminal prosecutions. Its success rate in the courts, moreover, represented a distinctive break from the hapless record of nineteenth-century state antifraud enforcement actions. As with requests for mail fraud orders, most BPFS motions for injunctions and the appointment of receiverships went uncontested; the Bureau usually prevailed when promoters or brokerages opposed it in court, and its criminal fraud prosecutions, while far less common than injunctive proceedings, typically resulted in convictions.6 BPFS could and did point to successful enforcement actions against large-scale investment frauds. Attorneys general and their deputies took every opportunity to crow about their fearless takedowns of the New York's Consolidated Stock Exchange during the mid-1920s, George Graham Rice's promotion of the Idaho Copper Mine, Charles Bob's looting of a mining investment trust, and many other financial frauds. Officials also stressed that the Bureau's impact extended beyond putting investment swindlers out of business or in jail, because initial inquiries from staff attorneys often convinced securities firms to reform their marketing practices.7Despite official breast-beating, contemporaries questioned how much enforcement of the Martin Act curbed the hawking of fraudulent investments. There were too many dodgy promoters for a few dozen investigators, attorneys, and clerks to track down, leading to laments from attorneys general about stingy appropriations and an impossible workload. Too often, critics such as the Progressive lawyer Samuel Untermeyer argued that enforcement under the Martin Act would merely “lock the stable door on these promotion frauds after the stock had been distributed and the thieves had bolted with their swag.” Furthermore, court orders to dissolve fraudulent securities firms, again like mail fraud orders, did not prevent seasoned operators from relaunching scams through new firms.

And Martin Act investigations targeted fringe operators—outsiders who dealt in unlisted stocks. Like the investigators of the Better Business Bureaus, the BPFS rarely scrutinized national financial elites.8Amid the prosperity unleashed by World War I, as well as a heightened pace of technological diffusion and a rapid expansion of consumer credit, shady practices became endemic in Wall Street. Large public corporations such as the Insull utilities’ holding companies took advantage of permissive accounting standards to inflate income statements, thereby facilitating the marketing of new securities.9 Corporate insiders and the managers of stock pools relied on a corrupt press corps to disseminate news favorable to their trades and manipulated prices directly through wash or matched sales—transactions in which they arranged to have confederates purchase shares to create the appearance of intensifying demand and increasing prices. Floor traders and specialists at the NYSE took advantage of knowledge about pending orders to engage in “frontrunning.” As these insiders received large orders that would affect prices, they first placed trades on their own account that would appropriate some of the economic value from those price movements.10 The investment trusts that sprang up during the 1920s created a culture of secrecy that abetted misrepresentation. Although fund managers claimed to have adopted sophisticated portfolio strategies that minimized risks, they often used investor funds to prop up struggling companies that they controlled, skimmed profits through undisclosed management and underwriting fees, and amplified risks by purchasing securities on margin.11

Investment banks and stock brokerages indulged in both conflicts of interest and deceptive practices. When underwriting initial public offerings of stock, investment bankers underpriced shares and reserved placements for corporate insiders and other favored clients, including members of the nation’s political and legal elite.12 In marketing the sovereign debt of struggling Latin American countries such as Peru, banking syndicates characterized the securities as low- risk, despite internal reports that warned of parlous fiscal situations.13 Banks and brokerage firms that sold securities to the broad middle class, such as National City, adopted several practices of the boiler room brigade. In addition to training salesmen in high-pressure tactics and implementing commissionbased remuneration policies that encouraged stretching of the truth, they trimmed the firms’ losses on poorly performing stocks in their portfolios by instructing sales personnel to push those securities on retail customers.14

On the eve of the Great Depression, New York Attorney General Hamilton Ward conceded that prevailing regulations, including his own state’s Martin Act, did little to prevent the most barefaced securities frauds. “The Martin Act,” Ward observed, “is no protection against the common thief who claims to be a broker or salesman and deals in worthless securities. From the petty grafter to the gang of high-pressure salesmen with plenty of money who open a big office, there is a large field in which the remedies provided by the Martin Act help but little.” Amid the wreckage strewn about the post-1929 financial landscape, the most ambitious forms of state antifraud legislation appeared even more insufficient.15

Malfeasance in the financial sector attracted public critiques before the New Deal, whether through the tell-all memoirs of stock operators Thomas Lawson, George Graham Rice, and Jesse Livermore, the analyses of academics such as economist William Z. Ripley, or the coverage of muckraking journalists such as John T. Flynn.16 But only with the Senate Banking Committee’s hearings on the securities markets did many Americans learn about the seamier side of the 1920s stock boom. These hearings, which began in the spring of 1932 and picked up momentum after Roosevelt’s election and the selection of Ferdinand Pecora as lead counsel, received saturation press coverage. The evidence presented by Pecora demonstrated the questionable ethics and behavior of vaunted firms, including National City Bank and J. P. Morgan. The hearings undercut Wall Street’s image, set off a political furor, and laid the groundwork for the Securities Act of 1933 and the Securities and Exchange Act of 1934.17

This pair of statutes remolded the marketing of securities. Although some Roosevelt administration officials and congressmen wished to create a federal “blue-sky” law, the chief drafters of the legislation, including Harvard law professors Felix Frankfurter and James Landis, viewed state regulatory approaches as failures. Instead of vesting the federal government with the obligation to certify new stock issues as reasonable propositions, Frankfurter and Landis joined two separate strategies of regulatory governance. The first involved bans on insider trading, market manipulations, and deceptions in initial public offerings and the secondary shares market. Here the architects of reform emulated the approach of the Martin Act, as well as state false pretenses laws and the federal mail fraud statute: they presumed that vigorous criminal prosecutions would deter outlawed behavior. The second strategy followed the longstanding logic of British financial regulation, which emphasized transparency in accounting and truthful marketing claims. The New Deal securities laws imposed rigorous disclosure requirements on public corporations, investment banks, and stock brokerages. But American legislators also extended the British approach. Across the Atlantic, the government depended on investors to identify wayward companies and promoters. Congress instead created an administrative regime to oversee provision of financial information, lodged in a new oversight body, the SEC.

Before investment banks could sell new securities to investors, they had to register proposed offerings (first with the FTC and, starting in 1934, with the SEC) and then wait twenty days before making sales. Registration documents had to furnish information about past performance, future strategy and prospects, assets and capital structure, and underwriting fees and sales commissions. If questions arose about veracity or completeness, firms could amend statements during the waiting period. If the SEC judged the information to be incomplete or untruthful, it could issue an administrative stop order that blocked offerings. Public companies further had to submit quarterly and annual statements about earnings and financial conditions, audited by independent accountants and consistent with accounting standards approved by the SEC in conjunction with the American Accounting Institute. The legislation furnished exemptions for small-scale stock offerings, closely-held companies with fewer than one thousand shareholders, and corporations with only instate investors; but it reached most stocks and bonds owned by American investors.18

Three later pieces of legislation completed the New Deal architecture of securities regulation, each designed in light of SEC investigations and hearings. The 1938 Maloney Act mandated the creation of quasi-public regulatory organizations to oversee America's hundreds of brokerages as well as the “over-the- counter” (OTC) market, which took place through telephone trades based on privately circulated price sheets, and which handled secondary bond transactions, stock purchases by large institutional investors, and trading in shares of unlisted companies. The new quasi-public associations would have authority to license brokers. They would further set training standards and rules of practice, monitor compliance with these rules, hear complaints from customers, and penalize brokers and firms that misled or mistreated investors. The SEC retained supervisory authority over self-regulatory institutions, as well as its own direct powers of rule-making, monitoring, and enforcement. After the passage of the Maloney Act, the industry settled on a single self-regulatory organization (SRO) to fulfill these roles, with the IBA reconstituting itself to become the National Association of Securities Dealers (NASD).19

Two years later, Congress enacted the Investment Companies Act and the Investment Advisers Act, which established regulatory oversight of investment trusts and the new fields of investment counselors and portfolio managers that had emerged after World War I. The first of these two statutes prohibited self-dealing in the selling and investment practices of mutual funds. It also barred individuals who had been sanctioned for securities fraud from serving as investment company directors or officers, required investment companies to register with the SEC, and mandated that those corporations provide investors with detailed updates about holdings, financial structure, and strategy. The second statute required advisers to register with the SEC and disqualified individuals who had participated in securities fraud; it further forbade material misrepresentations and mandated disclosure of potential conflicts of interest.20

On occasion, the SEC extended rules against deceptive practices, as in 1942, when it adopted Rule 10b-5. This regulation clarified the 1933 Securities Act's prohibition of fraud in securities transactions, declaring that it covered purchases as well as sales, omissions of material facts that made claims misleading, and any other kind of deceitful “device, scheme, or artifice.” For almost two decades, Rule 10b-5 remained a minor element of securities regulation, ignored by SEC enforcement staff and securities lawyers. But in 1961, more aggressive officials adopted an interpretative opinion that this rule prohibited stock trading by corporate officers who were taking advantage of nonpublic information, as well as the provision of such information to others who then traded on it.21

All of this legislative and administrative action was premised on the use of regulatory power to reshape the business environment. The central goal of disclosure requirements on corporations and investment banks, like the licensing mechanisms for stock brokerages, stock dealers, and investment advisers, was to remake the structure and culture of the financial markets. Toward this end, legislative framers, along with SEC staff, enlisted the help of financial professionals. Policymakers concentrated on private gatekeepers such as corporate attorneys, who had the responsibility to oversee compliance with the new requirements, and public accountants, whom the legislation anointed as monitors of corporate financial statements. This strategy of administrative prevention retained punitive features. Failure to abide by disclosure requirements made corporations subject to civil and criminal penalties, as did adoption of deceptive or fraudulent marketing practices. The Securities Acts also gave investors standing to sue for damages if corporations had made false claims or withheld material information, and if investors had suffered losses due to reliance on false or incomplete representations. But their central aim was to construct a new set of norms and practices about communicating truthful financial information.22 The apex of regulatory power in this system lay with the SEC and its hundreds of government lawyers, economists, and bureaucrats. Nonetheless, its designers remained leery of gumming up the securities markets with excessive red tape. As a result, they delegated extensive responsibility for regulatory compliance to the long-established stock exchanges, the newly created NASD, and the legal and accounting professions.23

As with securities law, post-1933 regulation of duplicitous retailing built on institutional forerunners and involved more robust activity by the national government. The most important federal agency in this policy arena remained the FTC. During the 1910s and 1920s, FTC lawyers had investigated thousands of businesses to determine whether they had violated Section 5 of the FTC Act, which outlawed “unfair methods of competition.” Its inquiries generated hundreds of “cease and desist” enforcement actions, as well as many more stipula- tions—written pledges to discontinue objectionable business practices. At no point, however, did the FTC enunciate the marketing transgressions that would trigger investigations. FTC administrative law judges and commissioners rather laid out principles piecemeal in case opinions.

Through this common law-like accretion, the pre-New Deal FTC identified clusters of disfavored marketing deceptions. Misleading claims about the quantity, quality, or newness of goods raised the eyebrows of FTC officials, as did false assertions about place of origin, the nature of ingredients/compo- nents, and the seller's status within the business community. Other enforcement triggers included unjustified disparagement of competing firms; deceptive claims about prices, such as fake “going out of business” sales and the touting of big discounts from fictitious high list prices; and phony testimonials. The trade practice conferences of the 1920s and early 1930s, which hammered out voluntary codes of fair competition, applied these broad principles to the specific contexts of individual industries.24

From the onset of the New Deal through the 1960s, the FTC took a very dim view of these marketing tactics. As its investigators, hearings' officers, and commissioners evaluated allegations of commercial misrepresentations, they used a much lower evidentiary standard than that required for criminal fraud allegations. The issue of fraudulent intent did not factor into FTC assessments, at least as they substantiated cease and desist proceedings in court; nor did the question of whether purchases had been influenced by deceptive claims. Instead, as the Supreme Court ruled in the 1919 case of Sears Roebuck v. FTC, the Commission only had to find that advertising or other aspects of marketing “had a capacity or tendency to injure competitors directly or through deception of purchasers.”25

Later action by the courts and Congress expanded the reach of FTC regulation. Just a few months after President Roosevelt decisively shifted the Supreme Court's political balance through the appointment of Justice Hugo Black, that tribunal further lowered evidentiary requirements in FTC deception proceedings. The pivotal case was FTC v. Standard Education Society (1937), an appeal from an FTC cease and desist order against an encyclopedia distributor. According to the FTC, the firm's army of door-to-door salesmen falsely claimed that prominent figures had either contributed to or endorsed the encyclopedias; they told prospective purchasers that they wished to give them a set of volumes as a gift in order to gain access to their homes, before explaining that they would also have to pay for a ten-year subscription to monthly supplements; and they mischaracterized the regular purchase price as a steep discount. To argue its case in the federal courts, the Standard Education Society retained Henry Ward Beer, the fervent and long-time critic of expansive FTC administrative action. A federal appeals court vacated several elements of the FTC's order, resting its judgment on the logic of caveat emptor laid out by Beer. “We cannot,” the lower court argued, “take too seriously the suggestion that a man who is buying a set of books and a ten years' ‘extension service' will be fatuous enough to be misled by the mere statement that the first are given away, and that he is paying only for the second.” This opinion echoed the nineteenth-century jurists and editors who marveled at the stupidity of some Americans. On this view, if hopeless rubes insisted on ignoring telltale signs of imposition, courts had no business protecting them. After the FTC took the case to the Supreme Court, Justice Black rejected this contempt for the credulous sucker. “The fact that a false statement may be obviously false to those who are trained and experienced,” Black reasoned,

does not change its character, nor take away its power to deceive others less experienced. There is no duty resting upon a citizen to suspect the honesty of those with whom he transacts business. Laws are made to protect the trusting as well as the suspicious. The best element of business has long since decided that honesty should govern competitive enterprises, and that the rule of caveat emptor should not be relied upon to reward fraud and deception.

Black's opinion for the Court accordingly upheld the FTC order in its entirety.26 Like the post-1937 federal judiciary, Congress enlarged the FTC's fraud beat. During the 1920s, the Supreme Court had ruled that the FTC only possessed jurisdiction over duplicitous sales practices if it could show that they constituted “unfair methods of competition” that brought harm to other businesses. The 1938 Wheeler-Lea Act removed this limitation, prohibiting “deceptive practices” in interstate commerce regardless of losses incurred by other firms, and enhancing the FTC's powers to act against deceptively marketed food, drugs, and cosmetics.27

Buoyed by these moves by the Supreme Court and Congress, FTC hearing officers and commissioners pushed out the boundaries of illegal deception. From the 1940s through the mid-1960s, they continued to convene trade practice conferences, encouraging firms and trade associations to hammer out sectoral codes of fair competition. In the late 1950s, the Commission conducted economywide campaigns against fictitious pricing, bait and switch advertising, and deceptive guarantees. After distilling the broad principles that had underpinned cease and desist orders in these areas, it disseminated official guides and made them investigative priorities.28

These endeavors received deferential treatment from the federal courts. Midcentury appellate judges shied away from overturning FTC assessments in deceptive practices cases, even without evidence that customers had been deceived or that anyone had suffered quantifiable monetary harm. Members of the federal bench presumed that FTC experts could be trusted to look out for the “careless” and “least sophisticated” readers of advertising, identifying the tricky or ambiguous claims that would trip up easy marks. If those public servants found that descriptions of hair dye as “permanent” went beyond the legal pale, because the dye would not impact new growth, the courts would not upend their judgment. Nor would they overrule FTC findings that a company's “buy one, get one free” promotional campaign was deceptive, on the grounds that the firm had never sold the item at the stipulated price; or its rejection of a television shaving-cream advertisement that claimed the product could soften sandpaper, because the ad relied on “camera tricks” and a “simulated prop” made of Plexiglas covered in sand.29 As the eminent federal judge Learned Hand summed up the FTC's discretion in deception cases, it had the authority to require “a form of advertising clear enough so that, in the words of the prophet Isaiah, ‘wayfaring men, though fools, shall not err therein.'” FTC staff well understood the leeway that they enjoyed. The Commission's 1966 Manual for Attorneys described its mission as protecting the “most ignorant and unsuspecting purchaser.” This objective required that investigators assess the “general impression” of ads and promotional materials, but did not hinge on showings of intent and gave investigators flexibility in building cases, because establishing deceptiveness was not amenable to “any general or allpurpose rule of investigative procedure.”30 This paternalistic vision represented a stark reversal from the presumptions that defined transactions a century, or even a half-century, earlier.

With America's entry into World War II, the national government refocused antifraud policy on military contracting and the regime of consumer price controls. As manufacturers retooled factories to meet the insatiable demand for weapons, munitions, tanks, and planes, reports surfaced of overbilling and other abusive practices. Federal officials responded by scrutinizing the work and billing practices of contractors and subcontractors. The armed services adopted stringent rules about quality control and cost structures, and backed them up with thousands of civilian inspectors and auditors who spent most of their time within factories. Congressional committees held a series of hearings to keep administration officials attentive to the task of keeping contractors honest. This oversight encouraged jawboning over charges and contract renegotiations. Where such informal pressure did not generate satisfactory outcomes, the Defense Department initiated dozens of high-profile prosecutions, which in most cases led to convictions.31

The crucial arbiter of the wartime retail economy was the Office of Price Administration (OPA), which had the task of enforcing rationing systems and price controls on consumer goods. In Washington, OPA economists and scientists set price ceilings and quality standards for a bewildering variety of consumer goods, and then constructed rationing regulations for crucial items such as gasoline and meat. Across the nation, local OPA officials, many of them former BBB leaders, enlisted hundreds of volunteer advisory groups and tens of thousands of local board members to assist with the formulation and implementation of regulations. A companion army of volunteer “price assistants,” mostly housewives, monitored compliance with price and quantity controls in retail outlets.32 Fraud enforcement represented only a minor aim for this gargantuan bureaucracy, which remained focused on tamping down inflation and ensuring the fair distribution of essential goods. But the organization nonetheless spearheaded hundreds of investigations across the country into ration-coupon counterfeiting, as well as the fraudulent sale of highly indemand rebuilt radio sets and used cars, leading to scores of arrests and trials.33

In the decade and a half after World War II, Congress passed a series of other statutes that targeted specific forms of commercial deceit, including the 1951 Wool Act and Fur Products Labeling Act, the 1958 Textile Fiber Products Identification Act, and the 1958 Automobile Information Disclosure Act. These statutes embraced the central regulatory strategy that animated New Deal securities law: information provision. Each specified several types of truthful information that businesses had to provide to their customers and defined standards for presenting that information. Together, they solidified the federal government’s commitment to acting against misleading and fraudulent forms of commercial speech, while also signaling an ongoing preference for enhancing the capacity of individuals to look after themselves.34

Post-World War II national policymakers exerted analogous efforts to rein in fraudulent educational institutions. Such concern reached back into the 1910s, when Better Business Bureaus, state prosecutors, and federal postal inspectors all began to wage battles against diploma mills. The creation of national higher-education grants and guaranteed loans through the GI Bill, however, gave the problem of educational fraud new salience. Now the issue was not just protecting the credulous or safeguarding the value of legitimate degrees and the standing of reputable educational institutions, but also preventing raids on the Treasury. After the 1944 passage of the GI Bill, there were periodic scandals involving fly-by-night vocational schools and more respectable institutions that misled prospective students about instructional quality or graduates’ career trajectories. The federal government’s primary regulatory response, heralded first in the 1952 Veterans’ Readjustment Assistance Act, depended on state and regional accrediting agencies. These nongovernmental organizations took on the role of certifying that universities, colleges, and proprietary vocational schools furnished bona fide educational programs, and so deserved eligibility for federal loans and grants. As with oversight stock brokerages, which relied on NASD scrutiny, attempts to combat fraud in higher education delegated key regulatory functions to quasi-public entities.35

Companion antifraud efforts occurred outside Washington, DC, as state and local governments added their own statutes and ordinances targeting consumer fraud. During the 1940s and 1950s, much of this legislative barrage singled out problems in specific economic sectors, such as marketing practices in the insurance industry (which was not subject to federal regulation, with the contested exception of advertising in national publications), or licensing and bonding regimes for occupations. The number of states that made instances of false advertising subject to prosecution as a misdemeanor also grew. By 1956, forty-three states had enacted such laws, with thirty-one mandating that prosecutors did not need to establish either knowledge or intent to obtain convictions.36

In one longstanding arena of antideception regulation—mail fraud enforcement—the judiciary did prune federal power. In a pair of cases, the Supreme Court ruled that the Post Office had to demonstrate fraudulent intent to justify the issuance of fraud orders, and that postal officials had to take greater care in framing the scope of such orders, so that they reached only activities shown to be fraudulent.37 These rulings, however, were premised on concurrent expansion of FTC authority, which gave the federal government an alternative administrative sanction for deceptive marketing practices—the FTC cease and desist order. The Post Office also retained authority to investigate allegations of mail fraud, initiating criminal prosecutions where appropriate.38 Thus, from the onset of the New Deal into the 1960s, tighter antifraud regulation represented a consistent feature of the American political economy.

There was no epochal event such as the 1929 stock market crash to serve as a generational touchstone for regulatory moves against duplicitous retail marketing. At no point did the specter of consumer fraud seem daunting enough to crash the entire economy. On occasion, smaller-scale incidents galvanized national concern over the willingness of businesses to shade the truth. In 1958, revelations that the major television networks had scripted popular game shows such as Twenty One and The $64,000 Question shocked elite commentators and ordinary viewers alike. A few years later, public disclosures that music companies showered DJs with inducements (“payola”) to play their records on radio programs produced similar reactions. These episodes generated high- profile congressional hearings, sparked some policy shifts, such as a federal law criminalizing payola, and encouraged the FTC to embrace a more aggressive posture toward deceptive business practices.39

In the absence of scandals, Americans continued to learn about the ongoing problem of consumer and financial fraud from commercial watchdogs. At no point did metropolitan newspapers cease to cover fraud prosecutions. As early as the 1930s, columnists such as the New York Post’s Sylvia Porter guided investors through the maze of modern capitalism, including advice on how to avoid financial swindles. The midcentury embrace of long-term investigative reporting produced numerous series on prevailing cheats, such as Jim Foree's five- part June 1957 expose for the Chicago Defender on sleazy automobile sales practices. Mid-twentieth-century national magazines also emulated their predecessors. Publications as various as Better Homes and Gardens, Reader’s Digest, Nations Business, the Saturday Evening Post, and Changing Times ran compendiums of business scams and recycled general cautions about the telltale signs of fraudulent marketing.40 A number of these journalists, such as Ralph Lee Smith, Frank Gibney, and Sidney Margolius, reached national audiences through books on frauds and rackets that drew on their careers covering consumer issues.41

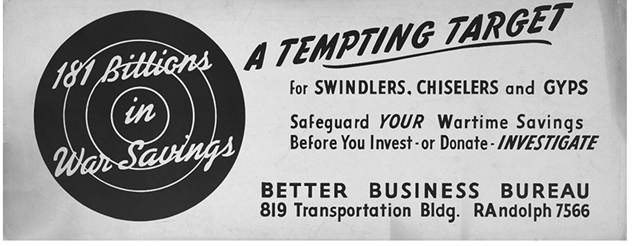

Antifraud sentinels in the press continued to have allies in the nation's network of Better Business Bureaus, which became even more entrenched during the postwar decades. The BBBs retained a focus on public education, as indicated by a massive campaign at the end of World War II to warn Americans about a flurry of investment frauds (Figure 9.1). By the 1950s, though, the BBBs put more effort into combating consumer fraud, a reflection of the deepening institutional framework of securities regulation. As Americans moved to the suburbs, BBBs followed right along, opening up offices in fast-growing new communities. By 1962, there were bureaus in 122 American cities and towns. They distributed a torrent of consumer guides to suburbanites, explaining how to look after their interests when dealing with a landscaping company, ordering television repairs, or purchasing an appliance on credit. In several cities, they produced radio and television segments that highlighted enduring problems of consumer fraud—three thousand radio and television episodes and forty thousand shorter public-service advertisements a year.42 In Chicago, for example, the long-running radio programs Hello Sucker and It’s Your Money ran weekly in the 1950s, warning listeners about frauds in automobile showrooms, among door-to-door salesmen, and through the marketing of franchising opportunities and residential developments.43 These campaigns rivaled the scale of BBB efforts in the 1920s.

National consumer organizations founded during the Great Depression, such as Consumer Research and Consumers Union, also monitored deceptive business practices as part of efforts to educate the parents of baby boomers and other postwar adults about how best to spend. As these organizations evalu-

Moving toward Caveat Venditor • 259

Figure 9.1: A BBB poster beseeching investors to remain vigilant in the face of post-World War II investment and charity frauds. W Dan Bell Papers, Denver Public Library, Western History Collection. Reproduced with permission.

ated product quality, they remained alert to marketing that pressed at the boundaries of acceptable puffery. Their newsletters and magazines then informed subscribers about products, services, and companies that flattered to deceive.44

Some of the most insistent post-World War II pleas for combating business fraud came from middle-class women, who took advantage of the growing tendency of economic discourse to feminize “the consumer” by picturing this abstract individual as a middle-class housewife. Cultural linkage of American household consumption to female decision-making had longstanding origins. The nineteenth-century birth of consumer education was bound up with the invention of home economics, a highly gendered undertaking. Mail-order houses, early department stores, and advertising agencies all directed marketing to potential female purchasers.45 But the equation of women with consumption decisions became even more common after World War II, as the figure of “Mrs. Consumer” became a common stand-in for the spending public, addressed in ads, referenced in the business pages, and depicted in antifraud literature, such as an early 1950s BBB poster that showed a skeptical housewife deflating the confidence of a door-to-door salesman by invoking the need to check out his firm with the local Bureau (Figure 9.2). “Mrs. Consumer” took on the gloss of the capitalist economy's true sovereign, the maker or breaker of corporate profitability. Through mounting consumer complaints to businesses, BBBs, and government officials, middle-class women deployed this rhetoric with regard to numerous consumer issues, including deceptive marketing. They organized as well, joining myriad neighborhood organizations that lent popular heft to consumerism.46

Figure 9.2: A skeptical Mrs. Consumer in a 1950s Better Business Bureau cartoon. Illustrated by Wilson Cutler as part of a series of educational slides commissioned by the Better Business Bureau.

Heightened expectations by consumers and investors encouraged diffuse support for antifraud regulation. Ongoing media coverage raised awareness of commercial deception and at least sometimes fostered public outrage over economic injustices. A steady increase in the number, kind, and reach of NGOs dedicated to fighting business fraud broadened the chorus of voices calling for antifraud measures, as well as the research base about marketing practices and consumer behavior. These developments swelled popular pressures for government action against commercial deceit and enlarged the stock of ideas about how to execute such regulatory campaigns. But the adoption of antifraud regulations between 1945 and the early 1960s rarely reflected vigorous grassroots mobilization.

During these years, regulatory action against misrepresentation was pushed by business interests, much as had been the case in nineteenth-century debates over fertilizer adulteration or the early twentieth-century campaign against false advertising. Adoption of more stringent labeling regimes for furs and textiles in the 1950s, for example, came at the behest of fur raisers, wool and cotton growers, and upscale manufacturers and retailers. Other than officials from regulatory agencies, representatives from these sectors were the only witnesses who testified before congressional committees considering labeling reforms. These groups alleged that discount sellers were engaging in rampant mislabeling that undercut public confidence in higher-quality goods; they also contended that many consumers were duped by such tactics, and needed protection that only strong public regulation could provide.47 Similarly, major record labels instigated the late 1950s payola investigations in the hopes of beating back inroads by independent producers. The latter had turned to payola as one way to introduce R&B, rock music, and African American artists to a wider public, focusing on new local radio stations that coveted young listeners. Even though the established music distributors also furnished DJs with gifts and favors, they calculated correctly that investigations into the industry’s endemic bribery and kickbacks would hamstring independents such as BMI and Ace Records.48

Advocacy for postwar antifraud regulation, however, did not always equate to regulatory capture, in which corporate puppeteers lay behind more stringent regulatory action, pulling the strings of public officials in order to fend off competitive threats.49 With some initiatives, such as moves against bait advertising and misleading pricing practices, antifraud professionals within the business establishment—BBB careerists, aided by counterparts at national advertising trade associations—stood out as the key figures driving regulatory agendas. From the 1930s onward, local BBBs and the National BBB identified such marketing practices as deserving of priority attention. During hundreds of trade practice conferences, BBB leaders hammered out detailed specifications about what constituted bait and switch tactics, false comparisons with competing retailers, and fake assertions about sale discounts. By the early 1950s, the Bureaus had developed comprehensive standards in these areas, whether for consumer goods such as vacuum cleaners and automobiles, or for services provided by home improvement companies and insurance companies. These codes served as templates for the FTC’s regulatory rule-making and enforcement priorities, which targeted bait advertising in late 1958, deceptive pricing in 1959, and deceptive advertising of guarantees in 1960.50

Postwar BBB officials, moreover, articulated an expansive antifraud philosophy that reflected an institutional mission distinct from that of their corporate funders. C. W. Dessart, a trade practice consultant specializing in the regulation of car marketing, articulated this stance in a sharply worded 1957 letter to a Texas auto dealer who had opposed more stringent antifraud rules for the industry. “As a dedicated automobile man, and as a Better Business Bureau Trade Practice Consultant,” Dessart explained to the dealer,

we admit to a kind of bias. For we are biased against the petty thief who filches pennies from a blind man’s cup; we are biased against the “shopper” who lies about what the “other dealer allowed him” for his old “heap” and the merchant whose business ethics and “law” is that of the shady business jungle, and whose theme song is “CAVEAT EMPTOR”—“let the buyer beware;” we are most decidedly biased against the merchant in any line—including automobiles—whose technique is to trade upon and exploit human ignorance and credulity, and who as an automobile “Medicine Man” pitches his “snake oil” by mass advertising to today's Mortimer Snerds, instead of to the yokels from the tail-gate of a horse drawn wagon as in the earlier days.51

For Dessart, sharp practices in retailing had no place in modern America. This mindset percolated throughout the national network of long-s erving BBB professionals.

The voices raised up against American business fraud during the Great Depression, World War II, and the immediate postwar period, then, reflected important continuity. As was the case during the Progressive era, some business interests continued to see deceptive sales cultures either as a short-term competitive threat or a longer-term menace to consumer confidence. And a cadre of antifraud professionals often took the lead in formulating legal reforms and setting enforcement priorities. Indeed, Presidents Truman and Eisenhower refrained from the full-throated critique of caveat emptor that had framed New Deal securities regulation.

To be sure, Harry Truman treated consumer welfare and the equitable distribution of America’s economic bounty as policy lodestars for his “Fair Deal.” These broad goals shaped his thinking about using fiscal policy to tame the business cycle and extending prosperity to a wider circle of Americans through national health insurance, expansion of Social Security, stronger protections for labor unions, federal aid for education and housing, stricter antitrust enforcement, and civil rights legislation. But at no point did Truman make consumer protection a centerpiece of his domestic agenda.52 While in office, Dwight Eisenhower signaled concern that American businesses faced too much heavy-handed governmental oversight. “The great economic strength of our democracy,” he proclaimed in his first message to Congress, “has developed in an atmosphere of freedom. The character of our people resists artificial and arbitrary controls of any kind.” This philosophy guided Eisenhower’s legislative priorities and appointments to regulatory agencies such as the SEC and FTC.53 Thus, it should come as little surprise that the pace of major federal antifraud initiatives slowed in the decade and a half after World War II, or that antifraud legislation adopted by Congress in this time period, such as the Textile Fiber Identification Act, came at the behest of business interests.

Toward the end of Eisenhower’s time in office, however, the television quiz show and payola scandals elicited a few presidential echoes of FDR’s rhetorical shots against unscrupulous stock promoters. Ike denounced the quiz show frauds “as a terrible thing to do to the American public” and described payola as an affront to “public morality.” In both cases he called for investigations and prevention of reoccurrences, which nudged Congress to pass legislation criminalizing fakery over the airwaves.54 These responses presaged more sustained presidential engagement with deceitful marketing and business fraud as national problems.

Challenges of Enforcement

New Deal and post-World War II antifraud statutes, of course, did not immediately transform legal culture and day-to-day economic relations any more than the formal legal reforms of the previous century. Policy innovations do not magically elicit adequate enforcement. Once again, we need to consider law in action—the meanings of all the new statutory requirements and administrative rules to aggrieved consumers, embattled firms, and consumer watchdogs; the legal system’s mediation of fraud-related disputes; and the impact of new legal norms on the beliefs and values that influence economic behavior. With the pivot toward the legal principle of caveat venditor, American policymakers filled in the latticework of a modern antifraud state. By 1960, thousands of individuals worked for antifraud institutions, deepening organizational capacity, constructing enforcement networks across jurisdictions and agencies, and encouraging professionalization of antifraud regulators. In some arenas, such as securities regulation, these endeavors achieved significant improvements in the trustworthiness of commercial speech. Wrestling with the flim-flam man, however, continued to require constant monitoring, patient investigation, shrewd deployment of resources, and unwavering vigilance, and the wrestlers did not always live up to these exacting requirements.

Mid-twentieth century antifraud enforcement efforts confronted numerous obstacles that had deep historical roots. Echoes of longstanding popular attitudes toward hucksterism represented one complication. Despite the shifts away from the premises of caveat emptor in American law, many corners of society retained contempt for the sucker and grudging admiration for those who took advantage of them. Post-World War II overviews of prevalent consumer and investor scams often marveled at the wondrous gullibility of those “suckers” who bit on the truly “preposterous,” “incredible,” “astonishing,” “fantastic swindles” lurking about the American marketplace. Accounts of specific fraud scandals, such as the 1948 implosion of Arthur Knetzers Ponzi-like car deposit scheme in southern Illinois, or the 1961 collapse of David Farrell's guaranteed trust deed investments in southern California, elicited analogous amazement at just how “eager” and “naive” investors and consumers could be.55 American linguistic practices also still communicated a disfavored status for those taken in by bait and switch advertising or investment scams. Even when seeking to warn consumers and investors about the need for skeptical appraisal of puffery, mid-twentieth-century commentators tagged those who lacked such habits with unflattering monikers. One list included “come-on, flyflat, John, juggins, or pigeon”; another “apple, bates, boob, chump, clown, easy mark, addle-cove, addict, egg, fink, lily, mooch, mug, pushover, top, [and] sweet pea.”56 Such turns of phrase did not imply abiding concern or respect.

The picaresque confidence man also continued to receive frequent billing in popular culture. W. C. Fields's 1939 film You Can’t Cheat an Honest Man became a mainstay of postwar television, repeating the message that those preyed on by financial bilkers had only their own greed to blame. It was joined by such hits as A Day at the Races (1937), The Rainmaker (1955), and The Music Man (1962). These productions offered sympathetic characterizations of grifters who relied on their wits to navigate unforgiving worlds. As one writer observed about the ongoing cultural status of the confidence man, he remained “an eccentric, a source of anecdote, a joke quickly told.” Even within the consumer movement, more conservative spokespersons such as Frederick Schlink of Consumers Research opposed stringent antifraud regulation, repeating the argument that it was impossible to hornswoggle “an honest man,” and worrying that regulatory paternalism would render consumers unthinking “wards of the state.”57

These undercurrents of mockery toward fraud victims and approbation for tricksters were not as powerful as in the nineteenth or early twentieth century. Most post-World War II discussions of swindles and commercial impositions stressed the psychological vulnerability of consumers and investors to well- constructed deceptions. A 1960 article in Changing Times, a personal finance magazine aligned with moderate Republicanism, conveys this common interpretive stance. The author of this catalogue of prevalent swindles and marketing trickery declared that “No one is safe” from commercial and financial fak- ery; that “[a]nybody can be a victim”; that “fraud operators can strike anywhere and anyone.” 58 By the same token, perpetrators of business frauds received scorn as “heartless” criminals.59

Still, wonderment at the credulity of American consumers and investors remained a feature of public discourse and private attitudes, as did some ambivalence about the “golden fleecers” who so artfully separated them from their savings. Such sentiments could hinder antifraud prosecutions. Amid lingering norms that harkened back to the age of caveat emptor, the psychology of embarrassment or denial still led many shorn Americans to keep quiet. According to Nathaniel Goldstein, New York attorney general in the mid-1950s, the vast majority of defrauded investors fell into this category, letting “pride keep them from filing complaints against the sharpers.”60 Even when victims were not dissuaded from making public complaints, there might be considerable delay between the moment of deception and its recognition by the consumer or investor, complicating any investigation. As in previous eras, the tiny stakes of many scams constituted a further barrier to action. Because many consumer frauds filched only small sums from individual purchasers, most victims did not chase after satisfaction.61

In both financial and consumer fraud cases, moreover, key actors in the American justice system viewed allegations of marketplace deceptions with jaundiced eyes. Outside the ranks of specialized antifraud agencies and divisions, the legal fraternity often retained personal standards that hewed closely to those of W. C. Fields, or even P. T. Barnum. In the decades before the emergence of public-interest law firms and a plaintiff’s bar that specialized in classaction suits, American attorneys were more accustomed to the perspective of business interests than that of consumers or investors, and so tended to sympathize with that viewpoint. Thus, if disgruntled consumers or investors sought out legal advice about how to handle some allegedly deceptive transaction, they were likely to be counseled against pursuing criminal complaints. For similar reasons, many mid-twentieth-century prosecutors were disinclined to bring fraud-related charges against businessmen. Moving in the same social and political circles as retailers and real-estate developers, and often contemplating returns to private practice, they had incentives to avoid antagonizing future clients.62

Prosecutors also knew that criminal fraud cases were often hard to win, for the same reasons as in earlier periods. The artful dodging of duplicitous businessmen, so vexing to late nineteenth-century postal inspectors and early twentieth-century BBB managers, continued to trouble antifraud enforcers. Pitchmen of mid-twentieth-century get-rich-quick schemes proved no less capable than their predecessors of moving boiler rooms from location to location, or of seeking out friendly jurisdictions from which to operate. Improvements in communications even expanded their geographic options. After the creation of the SEC, Canadian cities became popular bases for peddling penny stocks to American investors over the phone.63

The wide expanses of the United States also still offered escape routes for the purveyors of consumer frauds, as was made clear by the decades-long predation by a clan of several hundred petty swindlers known as “The Travelers” or “The Terrible Williamsons.” This set of related Scottish families maintained a nomadic lifestyle, moving from town to town pitching “bogus goods and services,” such as the cheapest textiles passed off as fine imports, shoddy driveway resurfacing, or ineffective roof sealing. The Williamsons took care to “stop in one location just long enough to bilk the local citizenry out of as many hard earned dollars as possible” before a chorus of complaints raised the alarm with local police. In those unusual circumstances in which members of the clan stuck around long enough to face arrests and criminal charges, they had little compunction about skipping bail. As a result, postwar BBBs officials and journalists issued repeated public warnings about their exploits.64

When victims were willing to file complaints and testify in court, and law enforcement officials were able to corral alleged perpetrators, prosecutors still had to weigh the drain on resources that fraud cases often entailed. Although the post-1945 judiciary accommodated antifraud reforms that lowered evidentiary burdens in administrative enforcement actions, the legal requirements for criminal fraud convictions remained steep. Just as in the previous century, much investigative legwork was necessary to substantiate fraud prosecutions. Establishing the false claims that underpinned marketing deceptions, as well as reliance on those falsehoods by victims and the fraudulent intent of defendants, often required interviews with far-flung witnesses and, in financial cases, expert accounting analysis. Prosecutors might have needed weeks to present such evidence before grand juries or in court, which meant that fraud cases clogged criminal dockets. The nature of the evidence at issue further gave well-prepared defense counsel opportunities to slow matters down with procedural challenges. These considerations shaped case selection even among prosecutors who made fraud cases a priority.65

Mid-twentieth-century criminal fraud prosecutions also ran into difficulties with juries and trial judges. The former could struggle to keep track of complex evidence about obscure financial transactions, manifest skepticism about the extent to which defendants had meant to deceive their counterparties, or demonstrate reluctance “to stigmatize a man as a criminal” because sales pitches had taken a few liberties with the truth. The latter often refused to see fraud charges as meriting the degree of concern shown to instances of violent crime, or went out of their way in jury instructions to emphasize that fraud convictions required a showing of fraudulent intent beyond a reasonable doubt.66 These stubborn dimensions of the legal system meant that some criminal sanctions against hucksterism went unused. Despite the steady passage of statutes criminalizing false advertising, prosecutions almost never occurred, because prosecutors viewed indictments as disproportionate responses to deceptive marketing.67

In addition, charismatic businessmen accused of fraud retained their penchant for avoiding criminal penalties, even after business failures that resulted in losses to investors, employees, and creditors. The 1949-50 trials of automobile impresario Preston Tucker suggests how the best defense attorneys had a knack for leading judges and juries to see their clients as sympathetic if flawed entrepreneurs. After World War II, the Tucker Corporation developed a new motor car, the Torpedo, in the hopes of cashing in on voracious demand created by rising household incomes and a wartime production ban. This vehicle possessed several technological innovations, but was beset by cost overruns and the gargantuan capital requirements of launching a new automobile firm. To raise cash, Tucker sold hundreds of dealerships to local businessmen and thousands of purchase options to consumers, while regaling potential investors with his company's prospects. After national magazine stories raised questions about corporate financial practices and a series of engineering difficulties, the firm spiraled into bankruptcy.

At this juncture, officials at the SEC, Post Office, and FBI became convinced that Tucker was emulating several fraudulent interwar carmakers, such as the Pan Motor Company of St. Cloud, Minnesota, which built factories and prototypes as part of elaborate schemes to bilk investors. As a result, they charged Tucker and seven other corporate officers with mail and securities fraud. Two high-profile trials led first to a mistrial and then acquittals. In the second trial, the judge instructed jurors about the high legal bar for fraud cases, informing them that they could convict only if they found that the defendants had made false statements and promises out of “a purpose and design to cheat.” Jurors rejected the prosecutor's argument that a mix of unrealistic projections, aggressive salesmanship, and generous executive compensation met such an exacting standard.68 Versions of this script recurred through the Cold War decades, as judges and juries declined to follow the lead of prosecutors in fraud cases brought against flamboyant leaders of failed corporations.69

Even when prosecutors won fraud cases, they often despaired over continuing judicial leniency. Whether fraud convictions came under state false pretense laws, the federal mail fraud statute, or prohibitions against securities fraud, defendants received minimal sentences. More often than not, unsavory characters who had filched large sums received only “wrist slaps”: probation, suspended sentences, or jail terms of a few months.70 The disinclination of judges to “rap their knuckles a little harder” when staring down at individuals convicted of business fraud had ramifications for plea bargaining. Because defense lawyers knew the score, plea deals rarely imposed jail time and often mandated only consent decrees that accepted findings of legal violations without admission of guilt.71

In earlier decades, frustrations with criminal fraud prosecutions had encouraged innovations such as the postal-fraud order and informal pressure on publications to reject advertising from offending firms. These tactics had elicited howls about creeping despotism, prompting adoption of procedural protections, which, in turn, had limited the effectiveness of administrative remedies. Proceduralism became even more deeply ingrained after World War II. Within the criminal courts, the dominant trend, driven by a Supreme Court concerned about civil liberties, was to give defendants greater access to legal representation and to ensure observance of procedural safeguards. Tougher appellate scrutiny of criminal convictions sometimes meant the overturning of fraud convictions on procedural grounds.72 That possibility expanded the tactics employed by defense attorneys in business fraud cases, because trial judges operated in the shadow of the appellate bench.

Heightened concern for procedure also cramped administrative enforcement. Here, the legal terrain was reshaped by the 1946 Administrative Procedure Act, which mandated extensive opportunities for public comment as part of the rule-making process and required that administrative actions mimic criminal process. Parties facing enforcement actions had to receive ample notice of specific allegations; they enjoyed rights to legal representation, access to incriminating evidence, and reasonable accommodation in preparing defenses; they could expect that hearing officers, investigators, and prosecutors would all be separate individuals, and that hearing officers would explain the legal basis of findings to them. Such protections, embraced as well by state Administrative Procedure Acts, extended the time and resources needed to pursue administrative orders against firms accused of deceitful marketing.73

Given sufficient bureaucratic capacity, the extensions of American commitment to the rule of law need not have presented insuperable enforcement problems. Some antifraud agencies, moreover, were able to build sizable organizations. The SEC began the post-World War II era with a budget of $4.6 million, which enabled it to maintain a staff of nearly 1,200, including more than three hundred employees in regional offices. But even at the most well- funded agencies, antifraud officials often still felt hard-pressed to meet their responsibilities in light of the growing population and economic activity. The SEC's budget did not keep pace with the explosive growth in securities origination and trading in the fifteen years after World War II, and budget cuts under Eisenhower forced the Commission to slash its staff by a quarter. Appropriations for the FTC's regulation of antideceptive practices did increase at a rate comparable to that of economic growth between 1945 and 1965. But its deceptive-practices unit struggled to handle thousands of annual complaints about false advertising and misleading sales techniques.74

Even more so than in the 1920s, administration action at the postwar FTC became notorious for its languid pace. Investigations often took months or years and then had to go through secondary reviews by staff attorneys.75 Consideration of formal cases by hearing officers and then the full commission took even longer, as high-level staff evaluated the analyses and conclusions of investigators and prevailing rules encouraged continuances. Every few years, an FTC chairman would declare war on internal delays and preside over speed- ups that would reduce bottlenecks. But a “dilatory and over-legalistic” institutional culture would then reassert itself. Although the courts mostly upheld FTC findings, appeals tacked on more time. In one convoluted case brought against Carter's Little Liver Pills for dubious health claims, the interval between the first investigation and the last court challenge was sixteen years. More often, three to five years elapsed before the conclusion of all appeals, far longer than the typical length of advertising campaigns. In addition, once FTC cease and desist orders became final, the agency allocated minimal resources to check on compliance. The agency developed a reputation for “snail-like procedures” and a “comatose spirit,” becoming known to the capital's chauvinistic wags as the “old lady of Pennsylvania Avenue.”76

The regulatory odyssey of Michigan's Holland Furnace Company suggests the capacity of some larger corporations to exploit these bureaucratic shortcomings. Holland Furnace had franchises in most states. Working door-to- door, its sales agents would create the impression that they were either government safety inspectors or private heating engineers, and ask to see the furnace. If homeowners agreed, agents would disassemble it and then spin grave tales of impending disaster via cataclysmic explosion, asphyxiating fumes, or engulfing conflagration. Next would come high-pressure pitches for replacement models, along with refusals to reassemble the old unit on the grounds that salesmen would not be “accessories to murder.” Holland managers gave salesmen extensive training in these tactics; the company also structured compensation incentives to encourage the hard sell.77

Holland executives pushed this selling scheme beginning in the mid-1930s. Scores of consumer complaints led the FTC to issue a cease and desist order against the firm in 1936. But the sales force ignored it. Years of additional complaints prompted another FTC investigation in 1954, which after four grinding years of procedural challenges culminated in a second cease and desist order. Holland personnel gave this order and a subsequent court decree the same short shrift. The firm continued to advertise for branch sales agents, whom it promised to “teach our business,” enabling them to make “above average wages while you learn and higher wages once you are experienced” Holland management also scoffed at fraud investigations by state and local agencies, raising every conceivable legal objection. Only in 1965, when a federal judge found the corporation in criminal contempt of the court decree, sentenced the former company president to a short prison term, and levied a fine of $100,000, did the firm take meaningful steps to root out abusive practices.78

Daunting practical realities confronted mid-twentieth-century enforcers of laws against business fraud: reticence among the fleeced; migratory swindlers; echoes of the world of caveat emptor that ricocheted around some corners of the criminal justice system; hyper-legalism; budgetary allocations that failed to match legislative aspirations. But regulatory officials were not without their own resources in coping with such challenges. Just as the history of American business fraud foreshadowed these problems, it also suggested regulatory rejoinders. Every facet of early twentieth-century American campaigns against business fraud reappeared in post-World War II initiatives, at a greater scale and intensity.

Fortifying the Antifraud State

Aware of their limitations, postwar antifraud organizations looked to maximize monitoring capacity and efficiently deploy resources for enforcement. One priority was to improve coordination and information-sharing among the agencies with jurisdiction over business frauds—an echo of the American Agriculturist’s network of correspondents, the NACM's “rogue's gallery” and the compendiums of quackery and quacks put together by the AMA's Bureau of Investigation. As soon as the SEC opened its doors, officials forged close relationships with federal postal inspectors, state securities regulators, and criminal investigators and prosecutors. Within months, the SEC collected sufficient data to construct a comprehensive set of “securities violation records” This “central index and clearing house” maintained details on about fifteen thousand Americans and Canadians who had faced allegations of securities fraud. In addition to keeping the index up to date, the SEC sent out a “monthly confidential bulletin” to its bureaucratic partners and contacted them about thousands of individual cases. By 1950, the fraud register comprised details on over fifty-three thousand stock promoters, brokers, and salesmen. SEC staff also analyzed the records to spot “overall pattern[s]," and always made the files

Moving toward Caveat Venditor

271

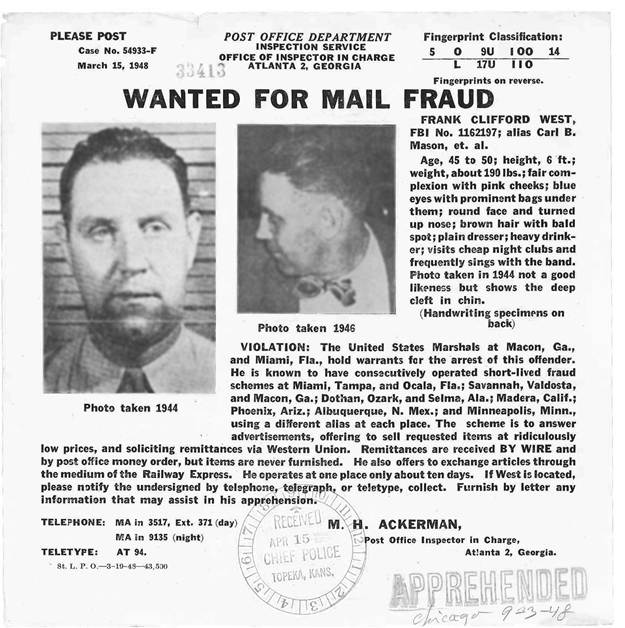

Figure 9.3: A Post Office “Wanted” poster, detailing the degree of information collected, and hinting at its national distribution (with receipt by the Topeka, Kansas, police, and a notation of the suspect being apprehended in Chicago). Author's collection.

available to state and local officials to assist with “current enforcement problems.”79 The postal inspectorate developed analogous information systems, as well as national distribution of “wanted” posters. The latter, such as a 1948 bulletin for Frank Clifford West, “alias Carl B. Mason” (Figure 9.3), included not only photographs, but also capsule biographies (in West’s case, consumer fraud schemes in seven separate states), fingerprints, and even handwriting samples. These national information systems facilitated the tracking down of even the most migratory swindlers.

Postwar antifraud agencies extended their reach through heavy reliance on self-regulatory organizations. New Deal securities regulation incorporated pri

vate regulatory gatekeepers from the start. The SEC leaned not only on securities exchanges and the NASD, but also on corporate accountants and attorneys. Exchange staff closely monitored transactions for indications of market manipulation. The NASD's inspectors visited brokerages far more often than their SEC counterparts, and its officials could levy punishments on individuals and firms that unfairly treated investors, including fines, suspension, and expulsion. Accountants and attorneys had professional obligations to keep corporations attuned to the new set of regulatory rules.80

As investor confidence returned during and after World War II, cooperation from self-regulatory institutions and professional gatekeepers became ever more crucial. By the late 1950s, the annual value of shares traded on registered exchanges eclipsed that of the 1930s by more than 300 percent. Investors could buy more than 7,500 stock issues on those exchanges or over the counter, while the number of brokerages approached five thousand, accompanied by nearly 1,500 firms that offered investment advice.81 Faced with the enormity of the American financial markets, SEC officials presumed that prevention of securities fraud would have to rest on a solid foundation of “selfregulation,” “self-discipline in the brokerage community,” and a commitment among lawyers and accountants to foster “compliance with the law.” The relentless circulation of capital threatened to overwhelm centralized regulatory oversight.82

Outside of finance, trade associations for broadcasters, news publications, and advertising agencies took on responsibilities for keeping deception out of major marketing channels.83 But the most important NGOs involved in antifraud enforcement remained the Better Business Bureaus. The post-World War II BBBs continued to encourage consumers with grievances against businesses to contact them. Millions of Americans internalized these pleas, bombarding BBB offices with letters and phone calls that raised questions or concerns. Although most complaints did not allege fraud, a significant fraction did so. A steady stream of BBB members complained about advertising and marketing tactics by competitors. These two streams of accusations prompted over thirty thousand annual investigations nationwide. In addition, BBB officials scanned newspaper and magazine advertisements and then sent out a corps of several hundred professional shoppers to discover whether enterprises lived up to their marketing promises. This ongoing policy of “shopping the ads” triggered additional inquiries. BBB activities amplified the monitoring activities of state agencies such as the FTC, which could only invest limited resources in surveillance of broadcast and print advertising.84

In hundreds of civil and criminal cases at every jurisdictional level, BBB officials coordinated with government investigators and prosecutors. BBB offices further responded to regular requests from governmental officials for assistance with enforcement efforts. During the early years of the New Deal, for instance, the Missouri commissioner of securities, resident in Jefferson City with no budget for investigative staff, pleaded with the St. Louis, Kansas City, and Springfield BBBs to forward intelligence about firms dealing in securities without licenses, or about “duly licensed dealers and brokers who may be adopting shady or questionable methods in the distribution of securities.” After World War II, the Federal Housing Authority asked for BBB assistance in policing the submission of “completion certificates” by construction and home improvement companies, which were required for homeowners to receive FHA mortgages. The FHA's deputy commissioner went so far as to ask every office to “establish a working relationship with the local” BBB, because such “close cooperation... will serve as one means of maintaining a close watch over... operations in your area.”85

The post-World War II BBB network never enjoyed statutorily sanctioned authority like that of the NASD in securities regulation, though BBB leaders sometimes hoped for such formal delegation. As the head of Denver's BBB mused in an early 1960 memo, “Maybe we could dare to propose that BBBs be set up like Eric Johnston's operation in the movie industry; or NASD's operation in the securities business, the Commissioner of Baseball, etc.”86 Such tentativeness suggests minimal confidence in achieving official grants of power. Nonetheless, the BBBs' post-1945 activities meant that the line between public and private business regulation continued to blur, as efforts by public and private agencies shaded into one another, even without explicit legislative delegation.

By the 1950s, the more established antifraud organizations, whether inside or outside the state, boasted numerous long-serving career professionals. These individuals had familiarity with marketplace deceptions, kept abreast of new variations, and knew how to conduct fraud investigations. The best of these careerists appreciated the challenges of navigating criminal and administrative enforcement actions and grasped the importance of sensible prosecutorial discretion, given limited institutional resources. They also enjoyed strong personal relations with their peers in other agencies.