CONCLUDING REMARKS

Behavior is one of the most important elements linked to most financial instruments. As it contains idiosyncratic characteristics, it brings challenges to map it with precise mathematical modelling.

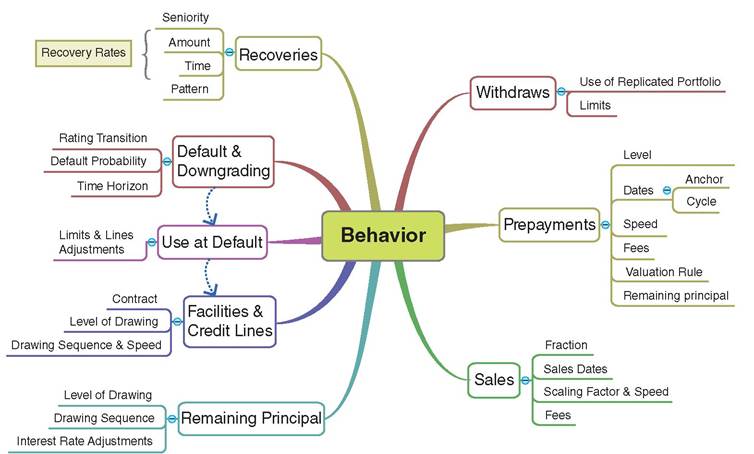

Prepaying a loan may be a useful option for the obligor—in other words, cancelling an unfavorable loan to renew it with better conditions. On the flipside, it may reduce significantly the investor’s income. In the models followed by marketplace lending, where no fees apply in case of prepayment, it is expected that any change of market conditions may encourage the obligors (borrowers) to prepay and indirectly roll over their loan with better rates. As we discussed in this chapter, the level, dates and speed of prepayments are modelled based mainly on historical observations. Any fees are estimated based on the remaining principal and duration of the loan. Finally, the valuation rule plays a significant role for estimating the prepayment amount.

The option of remaining principal draw-downs and the structure of facilities/credit lines contracts fall into the same category of behavior modeling. Note, however, that the former is mainly market and the latter counterparty driven. The level and the sequence of drawing the remaining principal and/or facilities are mainly following the counterparty liquidity needs. Thus, under liquid markets such types of behavior may have a low degree of risk; however under liquidity stress it may result in significant losses. Although credit finance provided via marketplace lending does not offer such options and types of contracts, the obligors joining credit deals may use them to pay the outstanding facilities and credit lines, e.g., credit cards.

For the behavior of withdraws, replicated portfolios are mainly used where they can be rather accurate under canonical expected conditions. At stress conditions, however, such behavior can damage13 the credit financial system.

To avoid such events institutions are setting certain limits. Note that such behavior does not exist in the marketplace lending model.

FIGURE 8.7 Elements of behavior analysis

Default and downgrading can significantly impact the value, income and expected cash flows of the credit portfolio. In the marketplace lending credit portfolios loans are uncollateralized with, in most cases, fixed and rather high interest rates, including market and credit spreads. Thus, borrowers may choose to default in case that future market conditions make the rules of the existing contractual loan agreement unfavorable. Furthermore, under stress conditions, counterparties at default may downgrade at significant degree and increase the credit speed. On the other hand, under liquid markets, counterparties may use facilities to avoid the default credit event. Primary marketplace lending is nowadays rather liquid, antithetically to banking lending market. Therefore, one can assume that some borrowers may use marketplace lending for avoiding default, indicating the use at default behavior risk.

As mentioned above, recoveries are the last resource for covering credit losses. Although in banking portfolios the rate of recoveries is rather well defined, linked to seniority class of the exposures, in the P2P model it is rather unknown whether recoveries can be expected, and to what degree.

Finally, the option of selling credit portfolios, fully or partially, can be useful in regards to funding and market liquidity as well as applying strategies for restructuring the existing portfolios. At the time of this writing, secondary market liquidity in P2P loans is still several years off.

Figure 8.7 summarizes all the main elements of financial behavior analysis.

NOTES

1. Due to lack of knowledge, laziness, negative feelings, or other reasons.

2. In the case of a delayed project there are, on the one hand, fewer requests for cash (expected drawdowns), but on the other hand this may be an indication that the project will not be completed.

In banking financial analysis, the latter case is considered as an indicator of credit default and thus the potential credit losses from the counterparty’s inability to pay back the drawing up today will affect future liquidity.3. I.e., committed and uncommitted, until further notice.

4. In most cases regarding saving accounts, however, credit institutions define some rules in regard to cash outs, i.e., notice and limits in withdrawals.

5. Liquidity funding management under stress financial conditions is defined in the contingency funding plans.

6. Morgenson, Gretchen (2008) “Behind Insurer’s Crisis, Blind Eye to a Web of Risk,” New York Times 27 September 2008, http://www.nytimes.com/2008/09/28/business/28melt.html?_r=0 &pagewanted=all, date accessed 21 April 2015.

7. Moldow, James (2014) “A Trillion Dollar market, by the People, for the People”, https://foundationcapital.com/assets/whitepapers/TDMFinTech_whitepaper.pdf, date accessed 21 April 2015.

8. Also called migration matrix.

9. Bradley, Anthony (2014) “Debt Crowdfunding Holds Much Promise,” Gartner Research, http://blogs.gartner.com/anthony_bradley/2014/10/22/debt-crowdfunding-holds-much-promise/, date accessed 25 May 2015.

10. Some practitioners are expressing recoveries as gross or net, i.e., gross recoveries include the effect of credit enhancements whereas the net recoveries are after credit enhancements. The natural way to define recoveries should be by using net recoveries as the credit enhancements are well defined whereas the expected recovery is driven by the counterparty behavior.

11. Based on Lending Club defaulting rules.

12. Lending Club (2015a) “What happens when a loan is ‘charged-off’?” http://kb.lendingclub.com/investor/articles/Investor/What-happens-when-a-loan-is-charged-off, date accessed 25 May 2015.

13. In financial crises started in 2007, few credit institutions defaulted due to behavior of high degree and speed of withdraws exercised by the depositors of current and saving accounts.

More on the topic CONCLUDING REMARKS:

- Concluding remarks

- Concluding Remarks

- Concluding Remarks

- Concluding Remarks

- CONCLUDING REMARKS

- Concluding Remarks

- Backhouse Roger, Baujard Antoinette. Welfare Theory, Public Action, and Ethical Values: Revisiting the History of Welfare Economics. Cambridge University Press,2021. — 301 p., 2021

- Some Philosophical Comments

- Gordon Matthew, Kaeuper Richard, Zurndorfer Harriet (eds.). The Cambridge World History of Violence. Volume 2: AD 500-AD 1500. Cambridge University Press,2020. — 696 p., 2020

- Concluding comment