RECOVERIES

Having credit enhancements attached to the credit exposures investors can precisely estimate the net exposure, and thus losses, after the default event. Indeed, credit exposure is not always fully covered by the credit enhancements.

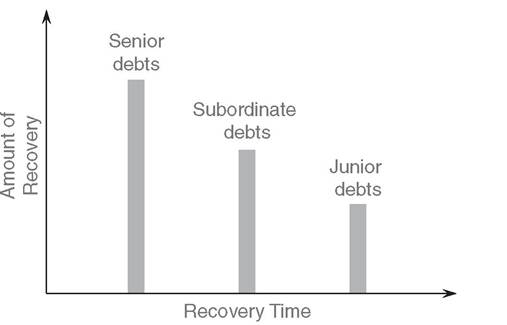

Thus, additional recoveries10 may be used for the remaining exposure and corresponding losses.The degree of the expected recovery, after the credit enhancements, is mainly dependent on the seniority of the exposure. Thus, senior debts are paid out first and have a higher probability and amount of payment whereas subordinate and junior debts have rather lower probability (see Figure 8.6). The recovery rates are mainly defined by applying statistical analysis but also some qualitative assumption and mapped as a recovery rate pattern. Institutions define the recovery rates for mapping both the amount and the time in which the corresponding recovery cash-flows are expected. The recovery pattern describes how this amount is to be regained over time.

There are several parameters that need to be considered in recovery behavior analysis including the seniority class, the net and gross exposures, the expected amount of recovery, and the expected recovery pattern.

Portfolio loans constructed in marketplace lending are uncollateralized; thus interest income and recoveries may be the only sources of covering the credit losses. Defaulted borrowers may decide to recover part of the outstanding obligation for avoiding further downgrading and loss of reputation. Nevertheless, recoveries in marketplace lending are a rare occurrence, for example,11 when a loan no longer has a reasonable expectation of further payments, it earns “charged off” status. The platform may sell such loans to a third party, and if the third party recovers the outstanding capital fully or partially, investors receive a pro rata

FIGURE 8.6 Expected recovery rates for senior, subordinate and junior debts

share of the sales proceeds or recovered capital. One marketplace lending platform admits that recoveries on previously charged-off loans are infrequent.12

8.8

More on the topic RECOVERIES:

- As we mentioned in Chapter 9, the status of a borrower and his contract is either “default” or “non-default.”

- NET EXPOSURE

- As already discussed, financial contracts contain rules used to sufficiently extract the financial events given the actual and assumed market and counterparty conditions.

- Boon Andrew. The Ethics and Conduct of Lawyers in England and Wales. Hart Publishing,1999. — 808 p., 1999

- Griffiths-Baker Janine. Serving Two Masters: Conflicts of Interest in the Modern Law Firm. Hart Publishing,2002. — 227 p., 2002

- Grisso T.. Evaluating Competencies: Forensic Assessments and Instruments. 2nd edition. — Springer,2002. — 564 p., 2002

- Luban David. Legal Ethics and Human Dignity. Cambridge University Press,2007. — 350 p., 2007

- Ayupova Z.K.. Theory of state and law: textbook. - Almaty: Kazakh University,2015. - 192 pages., 2015

- Allen Danielle, Benkler Yochai et al. (eds.). A Political Economy of Justice. The University of Chicago Press,2022. — 416 p., 2022

- Barnes Rudolph C.. Military Legitimacy: Might and Right in the New Millennium.Frank Cass,1996. — 198 p., 1996

- Bedner Adriaan (ed.).. Real Legal Certainty and its Relevance: Essays in Honor of Jan Michiel Otto. Leiden University Press,2018. — 261 p., 2018

- Fridson M., Alvarez F.. Financial Statement Analysis. John Wiley & Sons, Inc.,2002. — 413 p, 2002

- Banking, Finance, and Accounting: Concepts, Methodologies, Tools, and Applications. IGI Global,2014. — 1593 p., 2014