An Assessment of Pandemic Expenditures in the Context of Peacock-Wiseman Displacement Hypothesis

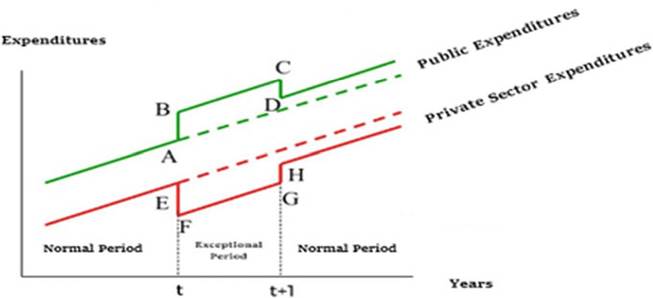

The Peacock-Wiseman Displacement Hypothesis is a fiscal theory asserting that the amount of public expenditure increases and private sector expenditures decrease during extraordinary periods (Ay 2014).

According to the Displacement Hypothesis, public expenditures decrease and private sector expenditures increase as the extraordinary periods end. However, it is emphasized that the level of public spending will never decrease before the extraordinary period (Yilmaz 2018) (Fig. 3.13).When the Peacock-Wiseman Displacement Hypothesis is evaluated regarding the COVID-19 Outbreak, it is seen that the epidemic period will cause an extraordinary leap in the amount of public expenditures. As a result of the researches, the country group with the highest leap in public expenditure is the developed economies.

Fig. 3.13 Peacock-Wiseman hypothesis. Source Created by author

Developing economies and low-income economies tend to use public expenditure instruments relatively less. This is due to structural problems and financial concerns these countries have. However, the COVID-19 Outbreak has been described as an “unprecedented crisis” due to its supply and demand-side economic effects, and it is emphasized for all country groups that public expenditure instruments are not cut in order for the economic recovery to develop smoothly in the future. In this context, developing countries and low-income countries other than developed economies are likely to experience a deeper economic recession during the epidemic period.

It is likely that the investment tendencies of developing countries, whose investment tendencies are relatively lower even in normal periods, will decrease due to the COVID-19 Outbreak. Moreover, due to the sharp decline in foreign direct investment worldwide, it would be difficult for these countries to make a leap forward in the medium term.

Therefore, actively using fiscal policy is a national policy method as required by the conjuncture. On the other hand, policies developed by governments in this direction are likely to have a positive impact on global trade and global finance. Therefore, in this extraordinary period, governments should activate their “shocking (counter) fiscal policies” without acting on ordinary period conditions and indicators (Yilmaz 2018). Otherwise, the negative externalities brought about by the epidemic will deepen the economic crisis environment and threaten the future of governments (politically) and entrepreneurs by increasing the economic costs. On the other hand, increasing unemployment, deterioration in income distribution and disruption of the education-health system will make it easier for the crisis to become an unprecedented crisis with a socio-economic nature (UN 2020).The COVID-19 Outbreak has revealed a period of great uncertainty on a global scale. Pre-epidemic predictions and predictions changed upon the epidemic, resulting in economic, political and social uncertainties. With the increasing risk factor in an environment of uncertainty, it becomes possible to experience market failure (missing information/asymmetric information). At this point, the public sector is expected to act with its regulatory and compensatory function. With the COVID-19 Outbreak, it is seen that policies in this direction are followed even in many liberal countries. However, at this point, flexible and reliable political capability becomes important. For example, the “delays problem” of fiscal policy makes it difficult to compensate for the risk in many countries during the epidemic period. The problem of delays decreases the compensatory ability of fiscal policy instruments (Ogretir 2017).

In other words, the efficiency of public expenditure tools in combating the epidemic may decrease with the problem of delays. The problem of delays stems from the fact that fiscal policy is made voluntarily without being based on fiscal rules.

In fact, the problem of delays, which is often referred to with monetary policy, is more common in voluntary fiscal policies. This is because indicators are not read with rules and bureaucracy and politics are delayed in decision making. As a result of such delays or misdiagnosis, the market balance deteriorates and economic stability disappears as a result of following opposite policies (OECD 2010). In order to avoid such situations, it is necessary to benefit from the stabilization of the budget. Governments should use their budgetary policy effectively to ensure economic stability (Sakal and Karadeniz 2019). However, the public spending policy, which will complicate the budget policy, should be supported by the revenue policy. In ordinary periods, increasing public expenditures followed by increasing the tax burden resulting in the increase in tax revenues may create tax pressure on taxpayers. This can have negative political consequences. However, as public spending increases in extraordinary periods will force the public sector financially, taxpayers may voluntarily participate in the increase in the tax burden. This is the tax compliance effect included in the Peacock-Wiseman Displacement Hypothesis. This situation is also referred to as the “Inspection Effect” in the finance literature.Due to the state of emergency, society’s resistance to tax is decreasing. It is a situation that allows governments to make the arrangements they want in their revenue policy. Because governments that want to get rid of the fiscal constraint act in a more disciplined way financially when they get the necessary tax revenues. In this context, in order to compensate for the costs of the economic and social crisis that started with the COVID-19 Outbreak, many countries have also put tax packages[10] on the agenda after spending packages. However, it is very difficult to implement these policies due to structural problems, especially in low-income country groups where there is a war (Akitoby et al. 2020). On the other hand, another factor that should be noted at this point is the inspection effect. The inspection effect arises as a result of the state’s need for public spending. Public expenditures are made to compensate for economic and social costs. If a government takes steps to increase the tax burden during the extraordinary period without increasing (or slightly increasing) the amount of public expenditure, this will further deepen the crisis environment and even reduce the tax effort rate.

On the other hand, tax expenditures per se will not be the solution. The market economy is based on financial mobility, and business downtime will pause this financial flow. As a result of the deterioration of financial indicators, tax revenues will shrink and companies will begin to go bankrupt. At this point, tax expenditure will only be political, not real.

3.4

More on the topic An Assessment of Pandemic Expenditures in the Context of Peacock-Wiseman Displacement Hypothesis:

- Açıkgoz B., Acar İ.A.. Pandemnomics: The Pandemic's Lasting Economic Effects. Singapore: Springer,2022. — 290 p., 2022

- Transfer Expenditures Measures Taken Against COVID-19 Pandemic in Turkey

- Economic Impact of COVID-19 Pandemic and Transfer Expenditures

- BoE, Coming Down with the Pandemic While in Brexit Pincer

- Transfer Expenditures and Their Economic Impact

- There have been several elaborations on the intermediate disturbance hypothesis

- DISPLACEMENT, SELF-ABASEMENT