France

Cyclical headwinds, structural challenges

| GDP | USD2782.9bn (World ranking 7) |

| Population | 67.9mn (World ranking 21) |

| Form of state | Semi-presidential republic |

| Head of government | Emmanuel Macron (President) |

| Next elections | 2027, Presidential and legislative |

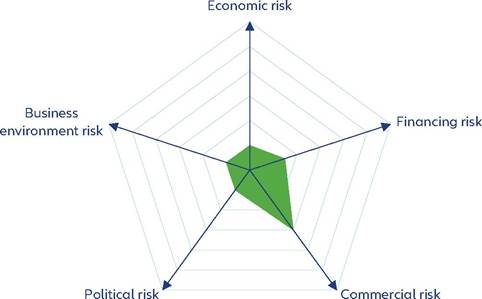

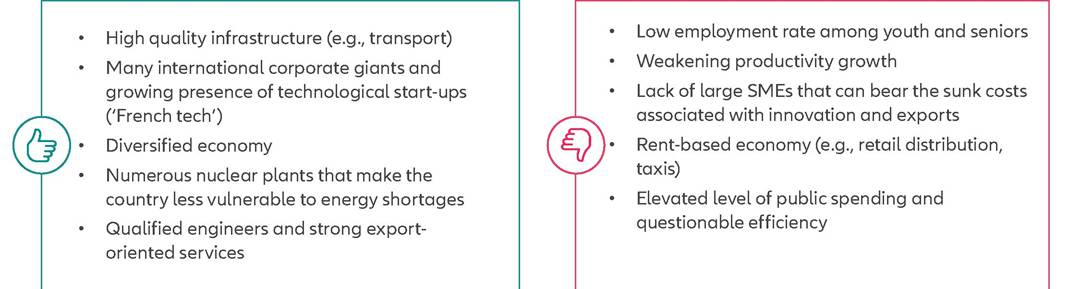

Strengths & weaknesses

Economic overview

Economy stagnating

The French economy has grown little since end 2022, held back by high energy costs gradually feeding through into corporates' bills, depressed household confidence, lackluster export growth and the effects of the ECB's tightening monetary policy.

Against this backdrop, the government has rolled out large support packages since the end of 2021 - including a generous tariff shield - to cushion the impact of the energy crisis on households and corporates' finances. Furthermore, growth momentum had benefited from the resumption of nuclear production and the build of stocks by corporates to replenish low inventories. The French economy should be stuck in this around zero growth environment through the middle of 2024. Corporate investment, which has held up well in 2023, should weaken as cash buffers are being depleted and external funding is drying up in a high interest rate environment. Growth should receive a boost from much lower inflation, which will support household income and consumption, but households will remain cautious for much of 2024, as indicated by persistently high savings intentions. The government has started to tighten fiscal policy to reduce a large fiscal deficit, but in 2024 most of the tightening will stem from the unwinding of energy subsidies, with expected little growth-hurting impact insofar energy prices remain contained. Tight fiscal policy will nevertheless increasingly constrain growth from 2025.Inflation has cooled down rapidly since the beginning of 2023, amid the unwind of supply-chain disruptions, lower commodity prices and persistently weak underlying demand. We expect it to be fully normalized by the summer of 2024, at below +2%, as indicated by corporates' weakening selling price expectations.

Corporate sector and public sector vulnerabilities

French corporate profit margins have been squeezed since the war in Ukraine. Excluding the transportation services and energy sectors, margins are at their lowest level since the mid-1980s. Low pricing power, alongside rapid rises in wage costs (the minimum wage is indexed to inflation) and declining productivity have kept companies from increasing their margins, especially in the services sector.

French corporates have persistently run large negative financial balances (i.e., they must rely on external funding or cash reserves to fund investment spending) over the past two decades. Over the past two years, external funding has dried up as interest rates have increased sharply. In this context, corporates have funded their investment by digging into their cash buffers. But those reserves have now pulled back below their trend, while it has become more difficult to roll over short-term credit lines. The financial environment is thus becoming more challenging for French corporates, especially SMEs. Excluding micro firms, corporate bankruptcies have surged over the past months. Thankfully, corporates have partially shielded their balance sheets against elevated interest rates through higher prices and larger interestyielding assets: their interest coverage ratio (post-tax profit over net interest expenses) remains contained, though decreasing rapidly.

level. More concerning, the underlying efficiency of labor seems to have decreased. Dynamic investment through 2022 and an expected increase in youth work efficiency (notably apprentices) should sustain an improvement of labor productivity in the next couple of years but we do not expect a return to the pre-pandemic implied path. The continuous drop in school proficiency for French students and poor skills of the labor force is a big headwind for future productivity growth. Furthermore, long-lasting structural issues (e.g., the lack of qualified workers, skill mismatches and little incentives to start work) are likely to prevent a significant drop of the unemployment rate below 7% in coming years.

Export performance is an area where France continues to underperform. French export volumes are well below their pre-pandemic implied path, held back by low exports of transport materials. On the positive side, exports of services have been dynamic since the pandemic. Export performance has been held back by a wide range of structural issues. The government has rolled out ambitious industrial subsidies to try to shore up manufacturing and exports, but incentives for corporates to restore production in a low potential growth country are weak. To boost the post-Covid-19 export recovery, the challenging sectoral specialization (e.g., aircraft and automobiles), poor price and quality competitiveness and the lack of qualified (technical) workers are amongst the chief issues to address.

The public sector's balance sheet bore the brunt of the dual shocks of the pandemic and the energy crisis. Public debt has increased by about 14 points of GDP between 2019 and 2023, more than in the Eurozone and the US. Elevated inflation has initially boosted tax receipts but is now pushing up 'catch up' spending (such as the indexation of social benefits and civil servants' wages). The government has also pushed through tax cuts on households and corporates and ramped up industrial subsidies massively.

Amid the re-introduction of European fiscal rules, we expect the government to broadly stick to the rules-binding 0.5% of GDP of fiscal consolidation per year from 2025, but risks of fiscal slippages are high. Nevertheless, public debt as a share of GDP should remain broadly flat at an elevated level.Stark improvement in the labor market but productivity performance a weakness

France's labor market has held up remarkably well since the pandemic. The unemployment rate has dropped while net job creations were the most dynamic among the large, developed nations since the pandemic, especially for the young. The labor participation rate picked up sharply to reach its highest recorded level. Despite weakening hiring intentions, unemployment is not expected to increase by much amid large labor shortages. Labor market strength is an important buffer against fading economic momentum.

Nevertheless, dynamic employment is partly the by-product of poor productivity performance. Abundant labor, sizeable hiring of young people and labor hoarding have weighed on French productivity, which sits well below its pre-pandemic

More on the topic France:

- ACKNOWLEDGEMENTS

- The British slave-free colony in Sierra Leone

- Syria

- The Danish colonial project on the Gold Coast

- Allianz Research. Country Risk Atlas 2024: Assessing non-payment risk in major economies. Allianz,2024. — 179 p., 2024

- Violence and the Family

- Legal battlefields after the 1994 genocide In Rwanda

- The British in the Coral Sea: Fiji