Mexico

Policy will be key to success

| GDP | USD1414.2bn (World ranking 14) |

| Population | 127.5mn (World ranking 10) |

| Form of state | Federal Republic |

| Head of government | Andres Manuel Lopez Obrador (President) |

| Next elections | 2024, General |

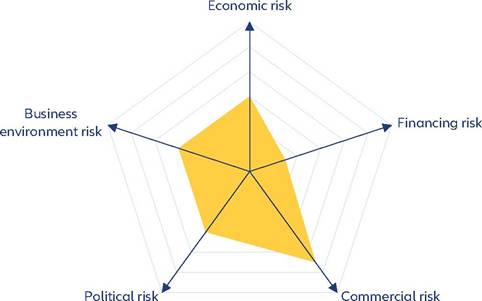

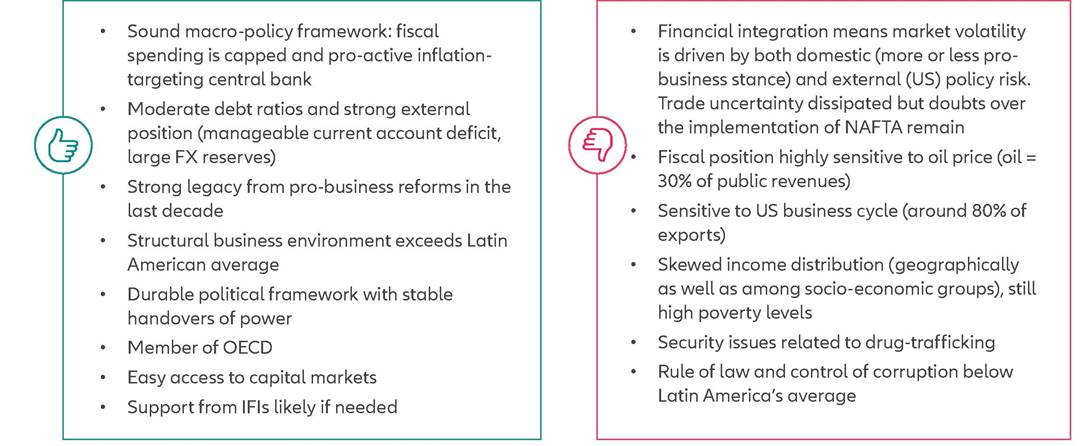

Strengths & weaknesses

Economic overview

Reforms needed to boost longer-term growth prospects

Mexico has a proven track record of implementing prudent macroeconomic and fiscal policies, establishing a certain degree of macroeconomic stability.

Despite a surge in Covid-19 infection rates, ongoing global supply chain disruptions and uncertainties arising from the Eastern European conflict, the Mexican economy witnessed a growth of +3.0% in 2022. This recovery was primarily attributed to the resilience of the manufacturing sector and modest improvements in the services sector, driven by positive changes in domestic spending, particularly in investments. In 2023, Mexico's economic activity continued its expansion, bolstered by growth in both services and industrial production, supported by a robust US economy, nearshoring trends, a tight labor market and rising wages. However, economic activity is expected to gradually lose momentum in the following quarters, primarily due to a weaker US economy and the lagged effects of tightening monetary policy. Our projection indicates economic growth reaching +3.4% in 2023, followed by a deceleration to an average of +2% in 20242025.In the medium term, depending on the national policy to be adopted by the next government - the elections will take place in June 2024 - the country's growth rates could rise. The country stands to benefit greatly from the nearshoring policy - in 2023 it became the top trading partner of the US, overtaking China and the IDB estimates that the additional gains from exports could reach USD30bn. However, the current protectionist/state policy towards the energy and mining sectors appears to be a limiting factor, as the state is unlikely to be able to cover the high levels of investment required (particularly in lithium extraction).

We anticipate a gradual easing of inflation in the coming period. The alleviation of shocks stemming from the pandemic and geopolitical tensions, such as the Russian- Ukrainian war, coupled with the current monetary policy stance, has contributed to the downward trajectory of inflation. It is essential to note that this path may not unfold linearly, as certain pressures persist within the services component, particularly in an economic environment demonstrating greater resilience than previously anticipated. Our projections indicate an average inflation rate of 5.5% and 3.8% for the years 2024 and 2025, respectively.

We anticipate that The Bank of Mexico (Banxico) will maintain its benchmark interest rate at 11.25%. With Banxico's board retaining its hawkish bias and aiming for an orderly and sustained convergence of headline inflation to the 3% target, the central bank announced its decision to keep the reference rate at its current level for an extended period. Assuming that disinflation persists, our expectation is for Banxico to gradually ease the policy rate starting from Q1 2024, reaching 7.75% by the end of 2027.

Solid external accounts, fiscal slippage to take time to fade

Mexico's external profile remains robust. The country has a track record of modest current account deficits (-1.3% as the historical average).

Nearshoring trends should support exports despite a slowdown in the US and should boost FDI inflows over the forecast period, helping Mexico to cover its current account dynamics comfortably. Should capital flows underwhelm, Mexico's reserves cushion will help to mitigate balance-of-payments risks.In anticipation of the 2024 general election, the Mexican government, led by Lopez Obrador, has shifted away from fiscal austerity that characterized the initial five years of his term. The projected fiscal deficit of 2.2% of GDP for 20252029 appears challenging, as the next president is unlikely to implement necessary spending cuts or fiscal reforms, leading to expected fiscal slippage. The forecast indicates a widening fiscal deficit from 3.8% of GDP in 2023 to 4.9% in 2024, the largest in over three decades. Despite the lack of commitment to substantive fiscal reform from potential successors Sheinbaum and Galvez, the next administration faces the delicate task of balancing spending control, political consolidation and economic growth. The deficit is projected to gradually narrow to 3% of GDP by 2028.

On a positive note, recent fiscal austerity has reduced the public debt/GDP ratio to an estimated 47.5% in 2023, down from the pandemic-era peak of 51.7%. However, due to election-related spending and modest fiscal reform, the ratio is expected to rise to 52.6% in 2028. Access to ample domestic financing and global capital markets positions the government to easily cover its financing requirements.

Competitive yet deteriorating business environment

The Heritage Foundation's Index of Economic Freedom 2022 survey assigns the country rank 67 out of 177 countries, above the regional and world averages, reflecting strong scores with regard to tax burden, government spending, tax freedom and investment freedom. However, Mexico scores less favorably regarding property rights, judicial effectiveness and government integrity due to weak rule of law, bias toward state-owned enterprises and policies that harm the private sector.

These factors will continue to weigh on the business climate.Political risk is assessed as moderate. Morena is expected to maintain its dominance leading up to the upcoming June 2024 presidential and legislative elections. While an opposition alliance, including the centrist Movimiento Ciudadano (MC), a growing minority party, may present a stronger challenge to Morena, differences in policies and negotiations over power-sharing quotas pose obstacles to forming such a coalition. The most recent polls show that Morena's representative, Sheinbaum, has 60% support, while her nearest rival, Xochitl Galvez, a right-wing senator and candidate for the opposition coalition, Frente Amplio por Mexico (Frente), has 33%. In light of these figures, Morena is poised strongly for the 2024 presidential race. Any opposition candidate faces a formidable task in uniting ideologically diverse parties, mobilizing disaffected voters and countering Morena's advantage as the incumbent party.