Poland

The worst is over but the recovery will be mild

| GDP | USD688.2bn (World ranking 21) |

| Population | 37.6mn (World ranking 39) |

| Form of state | Parliamentary republic |

| Head of government | Donald Tusk (PM) |

| Next elections | 2025, Presidential |

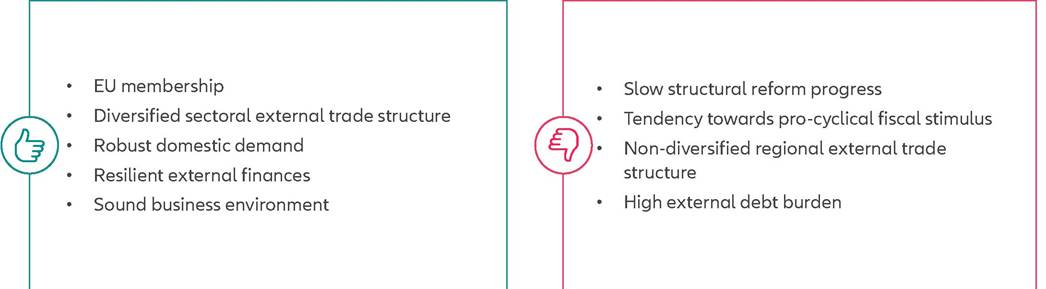

Strengths & weaknesses

Economic overview

Moderate recovery and sticky inflation in 2024

The outlook for the Polish economy deteriorated as a result of the war in Ukraine.

Following a strong post-Covid-19 rebound with +6.9% real GDP growth in 2021 and +8.8% y/y in Q1 2022, economic activity has cooled markedly since Q2 2022 as production was hit by supply-chain disruptions and rising input costs, notably surging energy prices. Full-year growth held up well in 2022, at +5.3%, thanks to pent-up consumer spending and solid investment activity. But in 2023, consumption fell markedly and a sharp drop in inventories was noticed as the full impact of the war hit the Polish economy, notably higher inflation and interest rates. The decline in domestic demand also pulled down real imports while real exports stagnated. Hence a positive contribution from net trade has mitigated the downturn and ensured that the economy just avoided a full-year contraction of GDP in 2023. Looking ahead, we forecast moderate real GDP growth of about +2.5% in 2024 and +3% in 2025, on the back of a recovery in consumer spending and continued robust investment.Consumer price inflation reached a peak of 18.4% y/y in February 2023.

Thereafter, it rapidly eased to 6.1% in December thanks to the unwinding of the energy and food price shocks in 2022. Going forward, fading base effects will slow down disinflation in 2024. Moreover, substantial fiscal spending pledges of the newly elected government as well as strong wage growth remain an upside inflation risk, requiring continued cautious monetary policy. We forecast inflation to average approximately 5% in 2024 and 4% in 2025. It may return to the National Bank of Poland's (NBP, the central bank) inflation target of 2.5%±1pp only at the end of 2025. The NBP hiked the policy interest rate to 6.75% in September 2022 and kept it there for a year until it pivoted with a large 75bps rate cut in September 2023, followed by a 25bps cut in October. Thanks to the rapid disinflation process, the NBP shifted its focus to supporting the ailing economy and was thus one of the first central banks in Europe to embark on a monetary easing cycle. We expect continued gradual monetary easing in 2024, matching the disinflation process.Public finances require monitoring but external finances have improved

Poland's public finances have deteriorated since 2019 but should remain manageable until 2025. Strong economic growth supported fiscal consolidation in 2014 to 2019 despite a moderately lax fiscal policy stance at the time. Fiscal deficits were low and public debt fell from 56% of GDP in 2013 to 46% in 2019. A huge fiscal stimulus program against the backdrop of the Covid-19-induced recession reversed that trend in 2020. The government posted a fiscal deficit of around -7% of GDP and public debt rose back to 57% of GDP. The economic rebound in 2021 and high inflation in 2022, which raised nominal GDP, lowered the debt-to-GDP ratio back to 49%. In 2023, increased spending on defense, public sector wages and social benefits as well as some pre-election stimulus widened the fiscal deficit to an estimated -5% of GDP. Looking ahead, the deficit is unlikely to narrow much in 2024 owing to the large spending pledges of the new government.

However, the latter is likely to be more cooperative with the EU than the previous government and may also embark on some fiscal consolidation after 2024, to comply with the EU fiscal rules. This provides the opportunity to unlock EU funds of up to 14% of GDP over 2024-2027, which will boost investment and economic activity and thus lower the fiscal deficit and public debt to GDP ratios beyond 2024. We forecast that the annual fiscal deficit will narrow gradually to approximately -3% of GDP by 2028 and public debt will stabilize at about 52% of GDP.Poland's external finances improved in 2023 after they deteriorated in the previous three years. The current account balance posted manageable annual deficits of -1.4% and -3% of GDP in 2021 and 2022, respectively, driven by surging energy import prices. The moderation of these prices in 2023 combined with faltering imports in the wake of subdued domestic demand has moved the current account back into an estimated surplus of around +1% of GDP. We forecast continued but smaller surpluses in 2024-2025 as imports are expected to recover more strongly than exports. On another positive note, foreign exchange (FX) reserves have recovered as well after they declined from mid-2021 to end-2022, due to the financing of the external deficit during that period. Current reserves cover almost five months of imports and, in other terms, more than all external debt payments falling due in the next 12 months - both of which are comfortable ratios. Meanwhile, the gross external debt to GDP ratio has fallen to just below 50%, down from 63% in 2020 and is now one of the lowest ratios compared to peers in Central and Eastern Europe.

Sound business environment

The Polish business environment is well above average, despite a perceived deterioration over the past years. The World Bank Institute's annual Worldwide Governance Indicators surveys suggest that the regulatory framework is business-friendly though a certain level of corruption is still perceived as present and the legal framework has worsened since 2014. The Heritage Foundation's 2023 Index of Economic Freedom survey assigns Poland rank 40 out of more than 180 economies, reflecting strong scores regarding property rights, tax burden, trade freedom, investment freedom and financial freedom. However, weaknesses remain regarding judicial effectiveness. Our proprietary Environmental Sustainability Index puts Poland at rank 51 out of 210 economies, reflecting strengths in energy use and CO2 emissions per GDP, water stress and general vulnerability to climate change, though there are still weaknesses in renewable electricity output and the recycling rate.

More on the topic Poland:

- Poland

- CHAPTER NINE THE LAST ACTS IN POLAND

- The Union of Poland and Lithuania

- 39 Ukrainian Lands in Interwar Poland

- 25 The Partitions of Poland, 1772-1795

- Ukrainian Lands in Interwar Poland

- Ukrainian Lands in Interwar Poland

- The Disappearance of Poland-Lithuania

- The Transfer of Populations between Poland and Ukraine

- Lithuania and the Union with Poland

- Lithuania and the Union with Poland

- Poland’s Policies toward the Ukrainians