Philippines

Navigating structural challenges to unlock further growth potential

| GDP | USD404.3bn (World ranking 39) |

| Population | 115.6mn (World ranking 13) |

| Form of state | Presidential Republic |

| Head of government | Ferdinand Marcos Jr. (President) |

| Next elections | 2025, legislative |

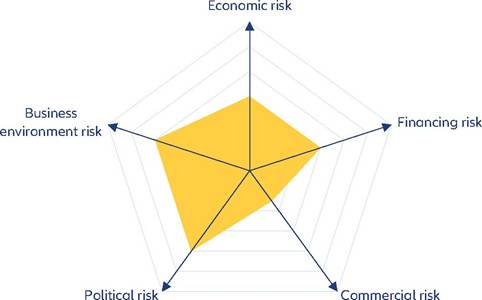

Strengths & weaknesses

Economic overview

Economic slowdown in the clear - growth to accelerate in the medium term

The Philippines has experienced strong GDP growth over the past two decades, with +4.5% on average in the 2000s and +6.4% in the 2010s. The Covid-19 pandemic hurt the economy severely, with GDP contracting by -9.5% in 2020 (the worst full-year recession on record) with a patchy recovery in 2021, growing by +5.7% amidst challenges in managing the public health crisis locally. Restrictive measures related to the pandemic were fully lifted by October 2022 and the economy experienced a strong rebound, growing by +7.6% in 2022. In 2023, the economy slowed down, with growth estimated to have moderated to +5.1% in 2023 on the back of headwinds such as the challenging external environment in terms of demand, high inflation and tight monetary policy. The nearterm growth trajectory of the Philippines paints a promising picture, with growth expected to rise to +5.7% in 2024 and stabilizing at an average of +5.9% in the medium term until 2030, supported by a recovery in external demand (notably for electronics), private consumption and investments - accelerated by the diversification of supply chains away from China.

Fiscal policy has been broadly expansive since the pandemic, with the fiscal deficit rising from 1.5% of GDP in 2019 to 5.5% of GDP in 2022. We estimate the fiscal deficit to have narrowed to 4.8% in 2023 and to consolidate gradually to 3.9% by 2025 as the government tries to optimize its revenues and expenditures. However, high interest payments on debt and support for low-income households mean that achieving the pre-pandemic (2010-19) average of 0.5% remains a challenging task at hand for the policymakers.

In terms of prices, we expect inflation to slow down to 3.4% and 3% in 2024 and 2025 respectively, well within the target range of 2-4% of Bangko Sentral ng Pilipinas (BSP) - the central bank of the Philippines. This is in comparison to a 15-year high of 6.1% in 2023. After an off-cycle hike of the policy rate to tame inflation in October 2023, the central bank will maintain a neutral policy stance going forward before a gradual easing when the economy avoids upside risks to inflation.

Deteriorated, yet manageable public finances with a volatile external balance

Broadly, the Philippines' short-term financing risk is deemed medium. However, the deteriorating public finances are worth monitoring, especially given the fact that the fiscal deficit remains significantly elevated relative to pre-pandemic levels. Further, the level of foreign direct investments remains low which will be worth monitoring as the president aims to improve the business environment to attract foreign investments.

The fiscal deficit rose during the Covid-19 crisis and is unlikely to return to the pre-pandemic level in the coming few years. At the same time, public debt rose to 60% of GDP in 2022 and 2023, from less than 40% in 2019. Going forward, it should moderate to around 55% on average in 2024 and 2025, which means that although it will remain above the pre-pandemic average of around 40%, it is lower than the levels seen in the 2000s (close to 60% on average during the period 2000-2010).

Further, the situation is not critical in the short to medium term, in part thanks to the country's reliance on domestic rather than external financing. On the external balances front, the current account deficit widened to 4.5% of GDP in 2022 on the back of markedly increasing energy prices (the Philippines is a net energy importer). We estimate it to have narrowed to 3% in 2023 and to decline further to 2.1% by 2025 supported by lower imports of fuel and capital goods and a recovery in goods and services trade. However, the country relies significantly on remittances for domestic consumption and is therefore vulnerable to challenges in the external environment. Further, the economy's heavy reliance on the exports of electronics (more than 50% of its total exports) makes it vulnerable to cyclical swings in the sector.Impediments to further economic progress: a weak business environment and political tensions

With a lower-than-average performance, the business environment in the Philippines broadly remains weak. The economy was ranked 80 out of 185 economies in the Heritage Foundation's Index of Economic Freedom survey 2022, down from rank 73 based on the survey conducted in 2021. The decline was primarily driven by significant weaknesses in terms of property rights, judicial effectiveness and government integrity. However, on the positive side, indicators for government spending, fiscal health and tax burden performed well. Meanwhile, the World Bank Institute's Worldwide Governance Indicators 2022 survey indicates that problems related to the rule of law and corruption warrants serious attention. Lastly, our proprietary Environmental Sustainability Index suggests that renewable electricity output, recycling rate and climate change vulnerability remain weak spots for the economy, thereby limiting its potential for accelerating growth.

Ferdinand Marcos Jr. was elected president of the Philippines in mid-2022 with a landslide victory and is able to count on the support of a majority in the House of Representatives (the lower house) and the Senate (the upper house). These factors and his emphasis on broad-based policy continuity in line with his predecessor Rodrigo Duterte suggest government stability during his presidential term, although risks such as geopolitical escalations with China (as he leans more towards the US contrary to the previous government which leaned more towards China) and falling public support due to an economic slowdown warrant prudent monitoring. It will be worth monitoring the next legislative elections, due in 2025.

More on the topic Philippines:

- Synopsis

- Discrimination

- Contributors

- Bui Ngoc Son, Malagodi Mara (eds.). Asian Comparative Constitutional Law, Volume 1: Constitution-Making. Hart Publishing,2023. — 495 p., 2023

- AppendixA: Data

- Conclusion

- Harker C., Horschelmann K. (Eds.). Conflict, Violence and Peace. Springer,2017. — 456 p., 2017

- Fundamentalist Islam: Afghanistan and the Taliban

- FISH

- The historical record: how traditional is local government in Asia?