Taiwan

Seeking growth in an uneasy (geo)political landscape

| GDP | USD791bn (World ranking 2022) |

| Population | 23.3mn (World ranking 2022) |

| Form of state | Semi-presidential republic |

| Head of government | Lai Ching-te (President-elect) |

| Next elections | 2028, Presidential and legislative |

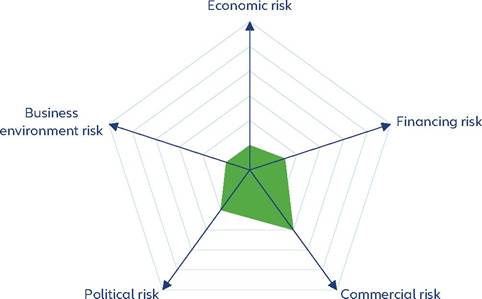

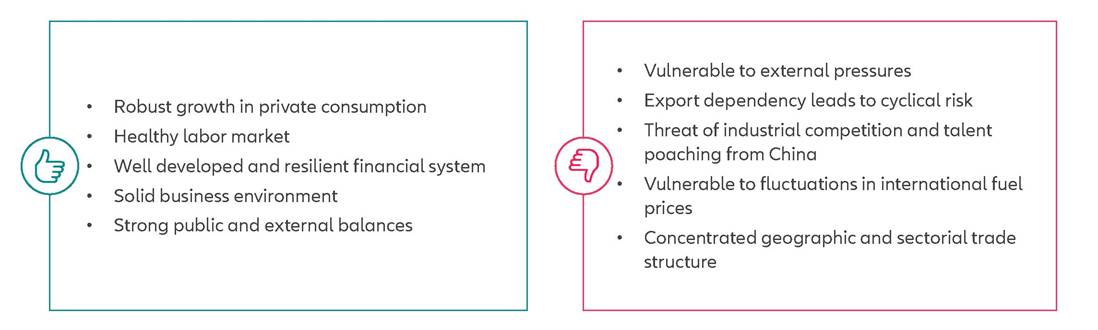

Strengths & weaknesses

Economic overview

Strong position in the global value chain ensures stable growth momentum

Taiwan has recorded robust GDP growth over the past decades, with an average annual rate of +3.9% in the 2000s and +3.6% in the 2010s.

Even during the years of the Covid-19 crisis, the economy showed remarkable resilience, recording a growth of +3.4% in 2020, +6.6% in 2021 and +2.6% in 2022, broadly outpacing the annual average growth of the Asia- Pacific region by +1.2 pps during this period (+4.2% vs. +3%). In addition to effective containment strategies and swift policy action, the economy's competitiveness in terms of manufacturing, notably of semiconductors can be attributed to its resilience during this period when most economies were not spared by the public health crisis. However, on the back of softer global demand and a downturn in the electronics cycle, we estimate economic growth in Taiwan to have slowed to +1.2% in 2023. Looking ahead, we expect the economy to grow by +2.8% in 2024 and +2.6% in 2025 on the back of continued growth in private consumption, a recovery in global trade, especially with a gradual reversal in the electronics cycle downturn and de-stocking in China, the US and the EU. However, weaker-than-expected demand due to high interest rates in advanced economies and cross-strait tensions pose downside risks to our forecasts.Fiscal policy in Taiwan has been broadly accommodative. To provide relief during the pandemic, the government accelerated fiscal spending through measures such as tax breaks, loan moratoria and subsidies. The annual fiscal deficits came in at -2.9% of GDP in 2020 and -2.1% of GDP in 2021 before declining to -1.7% of GDP in 2022. Going forward, we expect the fiscal balance to turn to a slight surplus starting in 2023 (+0.3%) and moderate in 2024 and 2025 (+0.2%) on the back of softer government expenditure and increases in tax enforcement, reflecting their attempts to impose fiscal discipline.

Headline inflation remained relatively high compared to historical levels in 2021 (+2%), 2022 (+3%) and 2023 (+2.5%) (albeit low relative to international standards) and has consequently led to the tightening of domestic monetary policy since March 2022, with a cumulative increase of +75bps so far, with the policy rate currently standing at

I. 875%. Looking ahead, we expect a gradual easing of monetary policy by the Central Bank of the Republic of China (CBC) as we forecast inflation to ease to +1.8% in 2024 and +1.2% in 2025, in addition to limited incentives for further tightening due to slowing growth in money supply (M2) and the weak economic outlook. However, risks to inflationary pressures from higher international fuel prices, adverse weather conditions (notably on food prices) and a weakening currency cannot be completely ruled out.

Solid macro-fundamentals tied down by geopolitical tensions

On the back of a well-developed and resilient financial system and sound external and fiscal balances, the shortterm financing risk in Taiwan remains low. We expect the fiscal balance to register a surplus in the near term until 2025, public debt to remain low at 22% of GDP in 2024 and 19% in 2025 and the current account balance to stabilize around 12% of GDP during this period.

Taiwan exhibits robust external balances with a strong track record of more than 20 years of large current account surpluses - reflecting its strong position within the global value chain. The expected recovery in global trade, in particular a reversal of the global electronics cycle downturn, will only fuel this trend going forward. Consequently, we expect the economy's current account balance to register a surplus of 12.1% of GDP in 2024 and

II. 7% in 2025. Further, we expect gross external debt to remain low, below 30% of GDP in the near-term. However, the economy's strong dependence on external trade makes it vulnerable to challenges in the external environment. Worsening geopolitical risks and rising cross-strait tensions are also softening inbound foreign investment flows from multinational firms.

Business-friendly environment, with broad political stability

Taiwan has a solid business environment with well-developed physical infrastructure, an educated workforce and businessfriendly policies. The Heritage Foundation's annual Index of Economic Freedom surveys have put Taiwan in the top ten out of 185 economies in recent years (rank 4 in 2023), reflecting very strong scores with regard to property rights, judicial effectiveness, government integrity, tax burden, business freedom and trade freedom. Indicators that have the potential to improve further include those related to labor freedom and financial freedom. Likewise, the World Bank Institute's annual Worldwide Governance Indicators 2022 survey suggests that the regulatory and legal frameworks are business-friendly and the level of corruption is low. On the downside, Taiwan scores less favorably with regard to environmental sustainability, owing to a very low level of renewable electricity output and a moderate recycling rate, although it does well with regard to energy use and CO2 emissions. Overall, Taiwan ranks 109 out of 210 economies in our proprietary Environmental Sustainability Index.

As we were expecting in our baseline scenario, the 2024 presidential elections were won by Lai Ching-te of the Democratic Progressive Party (DPP) with a share of 40.05% of total votes - slightly higher than that of his opponent Hou Yu-ih from the opposition Kuomintang (KMT), who earned 33.49% of votes.

By contrast, KMT won the legislative elections with 52 seats while DPP lost ten seats and retained 51. Since 57 seats are needed for a parliamentary majority, the third party - Taiwan People's Party (TPP) which won eight seats will be the kingmaker until the next elections. These results lead us to expect a broad containment in cross-strait tensions in the near term ans with negligible impacts on businesses and financial markets as the DPP's China-skeptical policy stance will be constrained by the opposition's push for a more conciliatory approach. However, uncertainties to the medium-term political stability of the economy cannot be ruled out and will remain a function of the collaboration between the government and the opposition, as well as factors external to Taiwan.

More on the topic Taiwan:

- with Hsin-hui I. H. Whited[151]

- Introduction

- Normative Implications of Parallel Constitutional Identities

- Contributors

- Minority Groups and Secessionist Movements

- Bibliographic Essay

- LIST OF CONTRIBUTORS

- Judicial reasoning and contextual imperatives

- China was no less violent than any other society in the early modern age. Like Europe, late imperial China had its fair share of wars of empire and peasant rebellions, as well as violent crimes of murder, assault, rape and robbery.

- Abstract