Switzerland

Solid economic fundamentals help cushion the growth headwinds

GDP

USD807.7bn (World ranking 20)

| Population | 8.8mn (World ranking 100) |

| Form of state | Confederation |

| Head of government | Viola Amherd (President for 2024) |

Next elections 2027, Legislative

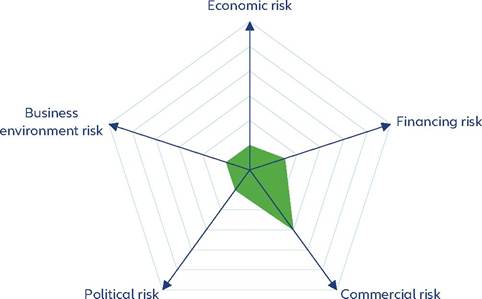

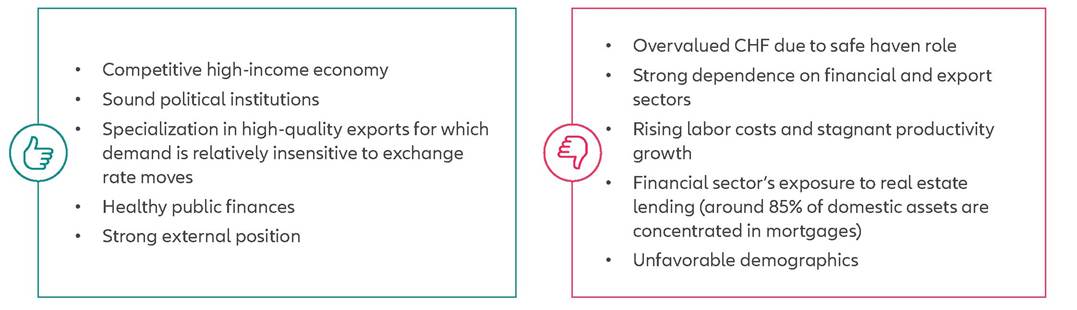

Strengths & weaknesses

Economic overview

Solid economic fundamentals help cushion the growth headwinds

Switzerland boasted a solid growth track record in the two decades leading up to the Covid-19 shock, recording average annual GDP growth of +2% - notably above the +1.7% for the Eurozone as a whole.

The Swiss economy was more resilient than its European peers and recorded output loss of only 2.3%. The economy recovered strongly and returned to its pre-pandemic size already in Q1 2021, with annual growth of +5.4% in 2021 and +2.7% in 2022. The first half of 2023 was still quite robust with +0.9%. Domestic demand and increased industrial exports supported growth. However, the slowdown in the global economy and lower international demand for goods exports are pressuring down the manufacturing sector and the associated exports.Despite a lower recession risk compared to its European neighbors, the Swiss economy is not immune to the global economic slowdown. The construction sector is struggling next to cyclical pressures in manufacturing. But the services sector shows some resilience. Moreover, there are strong structural underpinnings of private consumption, including the solid labor market situation.

Unemployment will remain low at around 2% to 2.5% up to 2025 and elevated household savings should help cushion the negative impact on spending. We expect real GDP growth to follow an increasing trajectory: +1.5% in 2024 and +2.3% in 2025. Switzerland is one of the few countries where insolvencies are already back above pre-crisis levels in 2022 and they are increasing further by +8% in 2023, but they will drop by -6% in 2024.Switzerland has managed to keep inflation in check due to a strong Swiss Franc which has reduced the cost of imported goods and services. Other factors include a more favorable energy mix (with electricity demand almost entirely met by hydropower and nuclear power), the highest share of regulated prices in Europe and a lower weight for energy and food in the consumer price index compared to other countries. Inflation dynamics have eased significantly over the last year. In Q1 of 2023, inflation rose to 3.2%, although it fell significantly again in the second and third quarter of 2023 to 2.1% and 1.6%, respectively. The increase at the beginning of the year was primarily due to electricity and gas prices. But services and food also contributed to inflation. We expect inflation to come down to 1.6% in 2024 and 1.2% in 2025.

Low short-term financing risk

Overall, indicators show that the short-term financing risk is low thanks to the solid faring of public finances with the budget balance balanced and public debt below 40% of GDP in 2023. In addition, Switzerland has consistently posted large current account surpluses thanks to a large positive balance in trade of goods as well as in services. The current account balance for Switzerland has rebounded since Covid-19, reaching 8% in 2023.The unilateral abolition of most import duties on almost all industrial goods from January 2024 is estimated to lower the federal revenue by 0.7%.

Very favorable business environment

The Swiss business environment proves very strong: the country scores very well in regulatory quality, rule of law and control of corruption. Switzerland boasts a well-educated labor force. It ranks at the top among other OECD high income countries.

More on the topic Switzerland:

- Weapons and People: Depositions in Natural Places

- Introduction

- Introduction

- Introduction

- Bovine Tuberculosis (BTB) in Cattle in Zambia

- Introduction

- CHAPTER 41 HARMFUL ALGAL BLOOMS INCLUDING Cyanobacterial toxicosis

- Allianz Research. Country Risk Atlas 2024: Assessing non-payment risk in major economies. Allianz,2024. — 179 p., 2024