The future of accountancy profession in the digital era

S. Fettry

Universitas Katolik Parahyangan, Bandung, Indonesia

T. Anindita & R. Wikansari

Politeknik APP Jakarta, Indonesia

K. Sunaryo

Universitas Pembangunan Jaya, Tangerang Selatan, Indonesia

ABSTRACT: The technology evolution is escalating rapidly.

It has changed the business environment, including accountancy profession. Digitization makes various disruptive changes in accounting practices. Failure to keep pace with the digitization will be a disaster for the accountancy profession. The digital technology generates hard challenges for accountants. This study aims at examining the perception of accountants of the digital era and to identify some important impacts of digitization on accountancy profession. A strategy on how to exploit the digitization is required for the benefit of accountancy profession. The study is based on a perception survey. Data are collected by distributing questionnaires to Indonesian accountants. An inclusive literature review is conducted to get more comprehensive understanding. The finding of this study indicates that the digitization has changed the way of thinking and practicing in accounting field. It is revealed that most accountants recognize the digitization as both benefits and challenges. It is concluded that most of accountants have confronted the technological revolution. Furthermore, it is suggested that advanced research should explore the topic in a larger area for a comparative study. The main contribution of this study is some identified strategies for accountancy profession to cope with the future digital era.1 INTRODUCTION

Nowadays, digital era has already evolved very fast in all aspects of life. The invention of computing and networking made everything become digitized. Digitizing has changed the business environment significantly, including the accounting field (Arnaboldi et al.

2017). It will affect the accounting profession permanently so that accountancy profession must respond to it in an effective way (Hunton 2015). The new modern technology of social, mobile and cloud platform (SoMo- Clo) has an effect on accountants’ work and way of thinking (Al-Htaybat & von Alberti-Alhtaybat 2017, Stanciu & Gheorghe 2017). Radical innovation in digital technology such as cloud computing, mobile devices, internet of things, big data, analytics software, and artificial intelligence is altering all aspects of business (Bhimani & Willcocks 2014).Technology advancement improves the efficiency and quality of accounting services and expands the scope of accounting services (Liu & Vasarhelyi 2014). The new IT solution and computing based solutions offer high level of accuracy, effectiveness, and efficiency in accounting services (Stanciu & Gheorghe 2017). However, it is perceived that the technology will replace some works in accounting (Accountancy Europe 2017, Guthrie & Parker 2016, Frey & Osborne 2013). This technology revolution will reduce the demand for accountants (Samkin & Stainbank 2016). Hood (2015) mentions that the technology forces will devalue the accountancy professional services. Therefore, the impact of digital era is questioned on whether it has a positive or negative effect on the accountancy profession.

This study explores the perception of the digital era and identifies some important impacts of digitization on accountancy profession by conducting survey on Indonesian accountants and literature review on various relevant readings. This paper is divided into five section. The first section introduces the background of the study. The second section provides a brief description of digitizing in accounting. The third section describes how survey and literature review were conducted. The fourth section presents and discusses the findings. The last section draws a conclusion based on the finding and offers some recommendations for future and further studies.

2 DIGITIZATION IN ACCOUNTING

The term digitization refers to the process of converting analogue data, e.g. images, video, and text, into a digital form (Oxford English Dictionary 2010). When used to improve business activities, this process is called digitalization (Brennen &

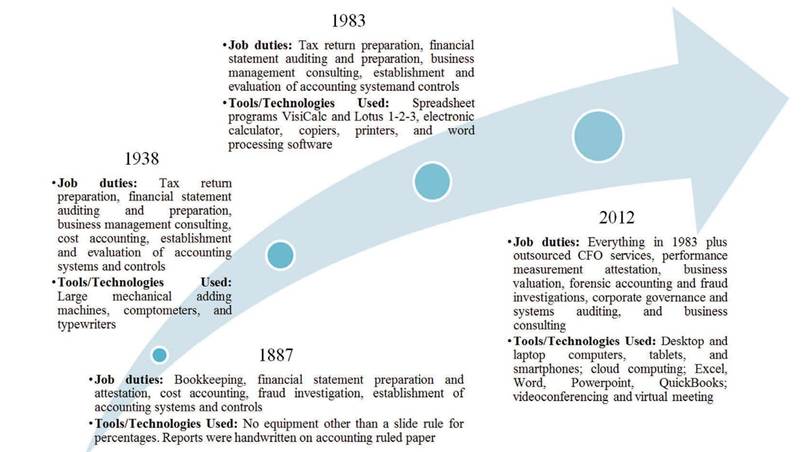

Figure 1. Transformation Duties of Accountancy Profession and Related Technologies Used. Source: Mendlowitz & Drew (2012).

Kreiss 2014). The digitization is about utilizing a new technology and integrating it with existing technology (Barashyan 2017).

Accounting has evolved from a simply book keeping to a sophisticated computerized information system to support decision making by both internal and external parties. The digitization in accounting has already started in the 90s, since the complex accounting information system was invented and evolved in more sophisticated ERP system, cloud computing, big data, mobile technology, social media, and internet of things (Rindasu 2017). This chronicle of technology advancement has effect on accounting profession as depicted in the Figure 1.

Today, the technology has brought the accountancy profession to the digital era to which accountancy professionals has responded by improving the accounting standards and procedures in accordance with the technology advancement. Accountants have been forced to change significantly in their services of compilation, assurance, tax and managerial consultation (Hunton 2015). There are some benefits and costs of digitization in accounting as listed in Table 1.

Table 1. Benefit and cost of digitizing in accounting.

| Benefit | Cost |

| • Faster cycle times - these include credit approvals, payment and collections, posting of transactions, closing of the books, generation of reports and more time available for higher-level analysis • Broader geographic reach • Continuous service availability, 24/7 access, and more satisfied internal and external customers • Reduced error rates - that means fewer transactions with errors as well as fewer errors • Reduced accounting staff and improved productivity • Better cash management - efficient payments and effective collections • Cost saving in mail, paper and storage of paper • Improved audit trails and security | • Investment required in computer hardware and software • Initial need for expensive consultants • Cost involved in system, processes, processing of information and report generation changes • Continual training or retraining needs and/or requirements for personnel with specialized skills • User resistance • Careful attention needs to be paid to security, control and audit requirements for financial transactions during the initial configuration. If the initial configuration of the system is not correct or the integration with ERP software or legacy system is faulty, then there are recurring costs and fewer benefits from the implementation. |

Source: Deshmukh (2006).

3 RESEARCH METHOD

This study was an on-line perception survey by distributing a questionnaire to Indonesian accountants, both practitioners and academicians. The items of the questionnaire were developed by adapting the concept of technology barometer introduced by the Accountancy Europe (2017). Only valid data were tabulated and analyzed using the perception descriptive technique. In addition, inclusive literature review from relevant accounting studies was conducted for the extensive analysis to get more comprehensive understanding on empirical evidence from the survey result. The questionnaire was distributed and collected in July 2018, by which 166 data were captured. The participants were selected using a snowball sampling technique. The first target participants were well- known accountants registered as member of accountancy profession association in Indonesia. The sampling method was purposive in nature based on certain criteria such as respondents’ willingness to fill out the on-line short survey and at least one year working experience in accounting field. The respondents consisted of 102 academicians, 46 practitioners, and 19 mixed respondents from various area in Indonesia, i.e. Ambon, Bandung, Batam, Bekasi, Bogor, Cilegon, Citeureup, Depok, Garut, Jakarta, Jambi, Jayapura, Jember, Jombang, Makassar, Manado, Medan, Palembang, Pangkalpinang, Pekanbaru, Pontianak, Probolinggo, Serang, Sidoarjo, Sidrap, Solo, Surabaya, Surakarta, Tangerang Selatan, Tara- kan, Tegal, and Yogyakarta. The survey captured their perception about the effect of digital era toward accountancy profession. This heterogeneous samples will give different perspectives into account.

Figure 3.

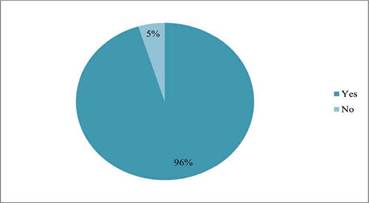

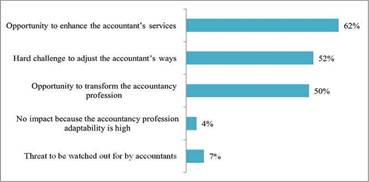

As accountant, I do some technology related activities.development was perceived an opportunity to enhance the accountancy profession. Most agreed that the technology development had no impact on the accountancy profession. Therefore, as Figure 3 suggests, almost every accountant do some technology related activities.

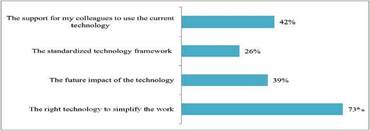

Figure 4 gives an obvious picture that in order to confront the technology advancement, training in newest technology the most frequent activity in accountants’ workplace. Special survey on technology advancement is very rarely conducted by accountants. Figure 5 depicts that mostly accountants’ technology-related activities are aimed to simplify their day-to-day works. The standardized technology framework is not much of their concern.

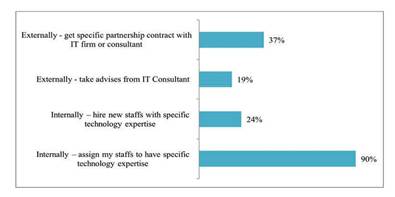

Figure 6 shows that most accountants are supported by internal staff with specific technology expertise. IT consulting services are rarely used because of the high consultation fee. Figure 7

4 RESULTS AND DISCUSSION

4.1 Survey results from Indonesian accountants

The internal consistency reliability of the survey questionnaire was measured by the Kuder-Richard- son Formula 20. The KR-20 coefficient 0.725 shows that the test had a high reliability.

The survey results are depicted in Figures 210. Figure 2 shows that the technology

Figure 4. Activities have been initiated at my workplace to confront the technology advancement.

Figure 2. The impact of technology development on accountancy profession.

Figure 5. The focus of my technology-related activities.

Figure 6. The way of my works is supported by the technology advancement

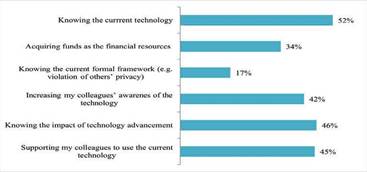

Figure 7.

My challenges in the fast advancement of technology.explains that the strongest challenge of technology advancement for accountants is knowing the current technology. The formal technology framework does not concern them much.

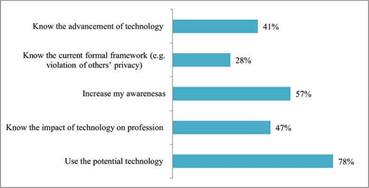

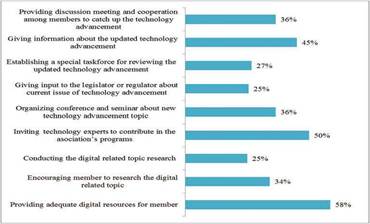

Figure 8 outlines some types of assistance provided by the accountancy profession association to its individual member. The most expected assistance is about how to use various potential technologies. Socialization on current formal technology framework is the least expected assistance. Based on Figure 9, the accountancy profession association is expected to organize some technology advancement related activities. The provision of adequate digital resource is highly expected by members of the accountancy profession association. Giving inputs to legislator or regulator and conducting digital related topic research do not concern them much.

Figure 8. Support from the accountancy profession association for me.

Figure 9. Kinds of technology advancement related activity must be conducted by the accountancy profession association.

Figure 10. Issues to take into account by the accountancy profession association when meeting the legislators or regulators.

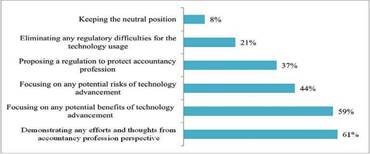

Figure 10 lists the most important issues the accountancy profession association is expected to discuss with the legislators or the regulators.

4.2 The impact of digital era on accountancy profession

Digital era makes accountants engage new technologies. The new analytical tools, cloud computing, and social media are challenges for accountants. Accountants have to employ these kinds of new technology to address the many radical changes expected to happen. Mobile devices make it easy to connect with every one in any where and any time. Accountants have been touched by the technology advancement. Big data concept stems from the internet of things gives potential new area to be explored by accountants. Unstructured or semi-structured data will be counted. Artificial intelligence and modern robotic automation will replace any regular repetitive duties of accountants. Accountants will have more complex duties to create value for organization (Richins et al. 2016).

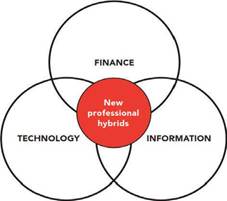

In the future, Association of Chartered Certified Accountants (ACCA) and Institute of Management Accountants (IMA) Report (2013) predict that accountancy profession, as shown in Figure 11, will become new professional hybrids

Figure 11. Newprofessionalhybrids. Source: ACCA and IMA Report (2013).

responsible for interpreting every analytical data and transforming them into valuable insight so that the business can makes commercial value on it (CGMA Report 2014). Consequently, the new professional hybrids will work with IT professionals, data scientists and business managers to have more comprehensive analysis for a more meaningful insight. Data analytic will be very crucial for businesses, and accountants must have the high level of analytical skill in addition to technical skills.

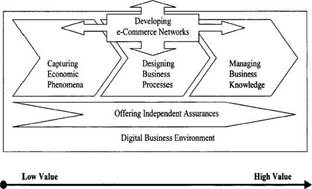

Figure 12 illustrates a digital accounting value chain as general framework for understanding the impact of digital era on accountancy profession (Hunton 2015). The highest value is how to manage the business knowledge optimally. Available digital technology will be used to get this highest value by capturing any economic phenomena, redesigning the business processes, and disseminating knowledge to decision makers.

Some studies give list of potential impacts of digitalizing era on accountancy profession (Taylor et al. 2017) as follow:

a. The rapid pace on global financial accounting and reporting standards;

b. The importance of real-time dynamic reporting;

c. The new format of management control systems;

d. The audit risk assessment based on data analytic and population;

Figure 12. The Digital Accounting Value Chain. Source: Hunton (2015).

e. The improved productivity by forecasts and sensitivity analysis based on external data;

f. The continuous assurance in timelier and more relevant audit reporting; and

g. The better understanding of restatements, fraud, and going-concern issues.

Furthermore, accountants will be required to protect sensitive information in the business system and application (Chorafas 2008). Cybercrime is another challenge to be coped by accountants. Information security will be the area to be solved. The new IT-based environment causes other problems. Web-based applications are at risk of being hacked. The cloud computing makes data management related works tougher. Privacy protection development will be crucial. Digital exchange of information between organization and external parties causes a set of risk exposure such as questionable data integrity. Hence, the system architecture of organization needs to be developed well and secure.

In this digital era, the role of accountancy profession will be changed into more strategic ones. Accountants will take a position as important partners of organizational changes (Nga & Mun 2013). Accountants will have more tasks in planning and strategic area. Accountant will be the future middle man in every organization (King 2014).

4.3 Strategies to exploit the digital era

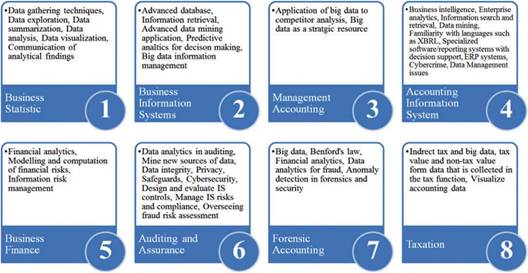

A strategy to exploit the digital era can be developed based on the accountancy academicians and practitioners’ perspectives. Accountancy academicians concern that the beneficial digital era must be anticipated with highly prepared human resources; i.e., the accountants themselves. An appropriate accounting education becomes an absolute requirement. The accounting curriculum must be evaluated and revised to address the new needs and challenges in the digital era. In this regard, there are some topics specific suggested by Gamage (2016) to be included in courses of accounting education as illustrated in Figure 13.

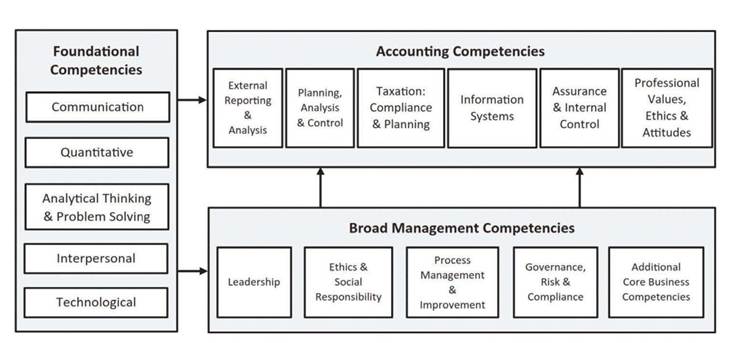

The basic strategy is developing a comprehensive framework for competency-based curriculum in accounting education. Hard skills and soft skills of accountants must be sharpened. There are various must-have skills for an accountant including perception skills, communication skills, interpersonal skills, personal/self skills, and technical/analytical skills. These skills will be created by integrating development of all competencies, i.e. foundational competencies, broad-management competencies, and accounting competencies (Lawson et al. 2014). The proposed competency-based curriculum framework is as follows (Figure 14):

Figure 13. New topics in courses of accounting education. Source: Gamage (2016).

Figure 14. Integratedcompetencyofprofessionalaccountant. Source: Lawson et al. (2014).

From the accountancy practitioners’ perspectives, accountants must aware of the latest technology advancement. Accountants have to pay a closer attention to how the technology will impact their works. Accountants must be ready for any potential radical changes in accounting. The accountancy profession associations must familiarize their members with the new emerging technology knowledge. The fast technology evolution must be anticipated by the accountancy profession. The technology advancement will always give new opportunities for accountants. But at the same times, it is always followed by other consequences such as new kinds of threat to the accounting works. The accountancy profession must aware of the high impact of increasingly digital era on their works.

5 CONCLUSION

Digital era with its emerging technologies has already changed the most accountants’ works and the way of thinking. It is concluded that accountants have confronted the technological revolution. Accountancy executives must have relevant technology literacy. Accountancy academicians are responsible for preparing the next generation to get ready the digitalized world. It is suggested that further research explore the impact of a particular digitization on accountant profession for more detailed empirical study. Further research can be carried out in a longer time and larger area of survey and an in-depth interview with some accounting experts as informants for a comparative study. The main contribution of this research is some identified strategies which can be implemented by the accountancy profession both academicians and practitioners in order to gain extra advantages of the digital era.

REFERENCES

Association of Chartered Certified Accountants (ACCA) & Institute of Management Accountants (IMA). 2013. Big Data: Its power and perils. Retrieved from http://www. accaglobal.com/bigdata.

Accountancy Europe. 2017. Technology Barometer: Survey Results. Brussels: Accountancy Europe.

Al-Htaybat, K. & von Alberti-Alhtaybat, L. 2017. Big Data and corporate reporting: impacts and paradoxes. Accounting. Auditing & Accountability Journal 30(4): 850-873.

Arnaboldi, M, Busco, C. & Cuganesan, S. 2017. Accounting, accountability, social media and big data: revolution or hype? Accounting, Auditing & Accountability Journal 30(4): 762-776.

Barashyan, A. 2017. Bibliometric Study on Digital Accounting Linked with Pedagogical View. (Master’s Thesis). Saimaa University of Applied Sciences.

Bhimani, A. & Willcocks, L. 2014 Digitisation, ‘Big Data’ and the transformation of accounting information. Accounting and Business Research 44(4): 469-490.

Brennen, S. & Kreiss, D. 2014. Digitalization and Digitization. Culture Digitally. Retrieved from http://culture digitally.org/2014/09/digitalization-and-digitization.

Chartered Global Management Accountants Report (CGMA). 2013. From insight to impact: unlocking Opportunities in Big Data. United Kingdom: CGMA.

Chorafas, D.N. 2008. IT auditing and Sarbanes-Oxley compliance: key strategies for business improvement. New York: CRC Press.

Deshmukh, A. 2006. Digital accounting: The effects of the internet and ERP on accounting. IGI Global.

Frey, C. & Osborne, M. 2013. The Future of Employment: How susceptible are Jobs to Computerisation. Oxford University Programme on the Impacts of Future Technology.

Gamage, P. 2016. Big Data: are accounting educators ready? Accounting and Management Information Systems 15(3): 588-604.

Guthrie, J. & Parker, L.D. 2016. Whither the accounting profession, accountants and accounting researchers? Commentary and projections. Accounting, Auditing & Accountability Journal 29(1): 2-10.

Hood, D. 2015. Losing sleep: Leaders of the profession on its biggest nightmares. Accounting Today. Retrieved from https://www.accountingtoday.com/news/losing-sleep.

Hunton, J.E. 2015. The impact of digital technology on accounting behavioral research. Advances in Accounting Behavioral Research 5: 3-17.

King, E. 2014. London jobs: big drive for big data. Retrieved from http://www.icaew.com/en/members/ local-groups-and-societies/london.

Lawson, R.A., Blocher, E., Brewer, P.C., Cokins, G., Sorensen, J.E., Stout, D.E., Sundem, G.L., Wolcott, S. & Wouters, M. J.F. 2014. Focusing accounting curricula on students’ long-run careers: Recommendation for an integrated competency-based framework for accounting education. Issues in Accounting Education 29(2): 295-317.

Liu, L. & Vasarhelyi, V. 2014. Big Questions in AIS Research: Measurement, Information Processing, Data Analysis and Reporting. JIS. Spring editorial. M68

Mendlowitz, E. & Drew, J. 2012. Carousel of Progress. Journal of Accountancy 213(6): 15-20.

Nga, J. & Mun, S.W. 2013. The perception of the undergraduate students towards accountants and the role of accountants in driving organizational change. A case of study of a Malaysian business school. Education + Training 55(6): 500-519

Oxford English Dictionary. 2010. Oxford Advanced Learner’s Dictionary. New York: Oxford University Press.

Richins, G., Stapleton, A., Stratopoulos, T. C. & Wong, C. 2016. Data Analytics and Big Data: Opportunity or Threat for the Accounting Profession? Retrieved from https:// papers.ssrn.com/sol3/papers.cfm?abstract_id=2813817.

Rindasu, S. 2017. Emerging information technologies in accounting and related security risks - what is the impact on the Romanian accounting profession. Accounting and Management Information Systems 16(4): 581-609.

Samkin, G. & Stainbank, L. 2016. Teaching and learning: Current and future challenges facing accounting academics, academicians, and the development of an agenda for future research. Meditari Accountancy Research 24(3): 294-317.

Stanciu, V. & Gheorghe, M. 2017. An exploration of the accounting profession - The stream of mobile devices. Accounting and Management Information Systems 16 (3): 369-385.

Taylor, A.M., Chen, Y., Estes, T.E., Hanks R.L. & Ramey, Z.M. 2017. Big Data Analytics: Megatrends to Business Success. Internal Auditing. July/August 2017: 26-32.