Growth accounting, the linearity critique, and other contributions

This section summarizes a variety of additional insights related to idea-based growth models. Section 6.1 discusses growth accounting in such models, showing that scale effects have accounted for only about 20 percent of U.S.

growth in the post-war period. Increases in educational attainment and increases in R&D intensity account for the remaining 80 percent. Section 6.2 considers a somewhat controversial “linearity critique” of endogenous growth models that first appeared in the 1960s. Finally, Section 6.3 will discuss briefly several other important contributions to the literature on growth and ideas that have not yet been mentioned.6.3. Growth accounting in idea-based models

Growth accounting in a neoclassical framework has a long, illustrious tradition, beginning with Solow (1957). As is well known, such accounting typically finds a residual, which is labeled “total factor productivity growth” (TFP growth). In some ways, endogenous growth models can be understood as trying to find ways to endogenize TFP growth, i.e. to make it something that is determined within the model rather than assumed to be completely exogenous. Having such a model in hand, then, it is quite natural to ask how the model decomposes growth into its sources. That is, quantitatively, how does a particular model account for growth?

Jones (2002b) conducts one of these growth accounting exercises in an economic environment that is basically identical to that analyzed in Section 4. In the long run in that model, per capita growth is proportional to the rate of population growth of the idea-producing regions. Off a balanced growth path, of course, growth can come from transition dynamics, for example, due to capital deepening or to rapid growth in the stock of ideas. Given the stylized fact that U.S. growth rates have been relatively stable over a long period of time, one might be tempted to think that the U.S.

is close to its balanced growth path so that growth due to transition dynamics is negligible. On the contrary, however, Jones shows that just the opposite is true. Approximately 80 percent of U.S. growth in the post-war period is due to transition dynamics associated in roughly equal parts with increases in educational attainment and with increases in world R&D intensity. Only about 20 percent of U.S. growth is attributed to the scale effect associated with population growth in the idea-generating countries.[29]This finding raises a couple of important questions. First, how it is that growth rates can be relatively stable in the United States if transition dynamics are so important? The answer proposed by Jones (2002b) can be seen in a simple analogy. Consider a standard Solow (1956) model that begins in steady state. Now suppose the investment rate increases permanently by 1 percentage point. We know that growth rates rise temporarily and then decline. Now suppose the investment rate, rather than staying constant, grows exponentially. We know that this cannot happen forever since the investment rate is bounded below one. However, it could happen for awhile. In such a world, it is possible for the continued increases in the investment rate to sustain a constant growth rate that is higher than the long-run growth rate. In the idea-based growth model analyzed by Jones (2002b), it is not the investment rate in physical capital that is driving the transition dynamics. Instead, educational attainment and research intensity (the fraction of the labor force working to produce ideas in advanced countries) appear to be rising smoothly in a way that can generate stable growth, at least as an approximation.

The second natural question raised by this accounting concerns the future of U.S. growth. If 80 percent of U.S. growth is due to transition dynamics, then a straightforward implication of the result is that growth rates could slow substantially at some point in the future when the U.S.

transits to its balanced growth path. To the extent that population growth rates in the idea-producing countries are declining, this finding is reinforced. Still, there are many other qualifications that must be made concerning this result. Most importantly, it is not clear when the transition dynamics will “run out”, particularly since the fraction of the labor force engaged in research seems to be relatively small. In addition, the increased development of countries like China and India means that the pool of potential idea creators could rise for a long time.6.2. The linearity critique

This section considers the somewhat controversial “linearity critique” of endogenous growth models that first appeared in the 1960s. A coarse version of the criticism is that such models rely on a knife-edge assumption that a particular differential equation is linear in some sense. If the linearity is relaxed slightly, the model either does not generate long-run growth or exhibits growth rates that explode. This section first presents the basic issue and then attempts to show how it can be used productively to make progress in our understanding of economic growth.[30]

Growth models that are capable of producing steady-state growth require strong assumptions. For example, it is well known that steady-state growth is possible only if technological change is labor-augmenting or if the production function is Cobb- Douglas.[31] Another requirement is that the model must possess a differential equation that is linear. That is, all growth models that exhibit steady-state growth ultimately rest on an assumption that some differential equation takes the form

Growth models differ primarily according to the way in which they label the X variable and the way in which they fill in the blank in this differential equation.[32]

Forexample, in the Solow (1956) model without technological progress, the differential equation for capital accumulation is less than linear, and the model cannot produce sustained exponential growth.

On the other hand, when one adds exogenous technological change in the form of a linear differential equation At = gAt, one obtains a model with steady-state growth. Inthe AK growth models of Frankel (1962) and Rebelo (1991), the law of motion for physical capital is assumed to be linear. Inthe human capital model of Lucas (1988), it is the law of motion for human capital accumulation that is assumed to be linear. Finally, in the first-generation idea-based growth models of Romer (1990), Aghion and Howitt (1992) and Grossman and Helpman (1991), it is the idea production function itself that is assumed to be a linear differential equation.This kind of knife-edge requirement has made economists uncomfortable for some time. Stiglitz (1990) and Cannon (2000) note that this is one reason endogenous growth models did not catch on in the 1960s even though several were developed.[33] Solow (1994) resurrects this criticism in arguing against recent models of endogenous growth.

What is not sufficiently well appreciated, however, is that any model of sustained exponential growth requires such a knife-edge condition. Neoclassical growth models are not immune to this criticism; they just assume the linearity to be completely unmotivated. One can then proceed in two possible directions. First, one can give up on the desire that a model exhibit steady-state growth. It is not clear where this direction leads, however. One still wants a model to be able to match the steady exponential growth exhibited in the United States for the last 125 years, and it seems likely that a model that produces this kind of behavior will require a differential equation that is nearly linear. Alternatively, one can see the linearity critique as an opportunity for helping us improve our growth models. That is, if a growth model requires a linear differential equation, one can look for an economic explanation for why linearity should hold and/or seek empirical evidence supporting the linearity.

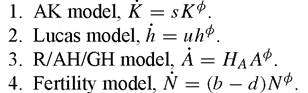

To see how this might work, consider briefly the main types of endogenous growth models and the key differential equations of those models:

In each case, we can ask the question: “Why should we believe that φ ≈ 1 is valid in this model?”. In particular, we consider the following experiment. Suppose we hold constant the individual decision variables (e.g. the investment rate in physical capital or time spent accumulating human capital). Suppose we then double the state variable. Do we double the change in the state variable?

In the AK model, φ is the elasticity of output with respect to capital. In the absence of externalities, this elasticity is the share of capital in income. Narrowly interpreting the model as applying to physical capital, one gets a benchmark value of about 1 /3. Some people prefer to include human capital as well, which can get the share a little higher.[34] But then one must appeal to large externalities, and these externalities must be exactly the right size in order to get φ ≈ 1.

Now turn to the human capital model of Lucas (1988). Consider a representative agent who lives forever and spends 10 hours per week studying to obtain skills. Are the skills that are added by one period of this studying doubled if the individual’s stock of human capital is doubled? A natural benchmark might be that studying for 10 hours a week adds the same amount, whether one is highly skilled or has little skill. It is far from obvious that the 10 hours of studying increases skills proportionately over time.[35]

This chapter has already discussed the Romer/AH/GH assumption of φ = 1. Recall that one can make a case for φ < 0 if it gets harder over time to find new ideas or φ > 0 if knowledge spillovers increase research productivity, or even φ = 0 if researchers produce a constant number of ideas with each unit of effort.

The case of φ = 1 appears to have little in the way of intuition or evidence to recommend it.Finally, the last case above suggests placing the linearity in the equation for population growth, as was done implicitly in the models discussed earlier in the chapter. It can be thought of in this way: Let b and d denote the birth rate and the mortality rate for an individual, respectively. Hold constant an individual’s fertility behavior, and suppose we double the number of people in the population. A natural benchmark assumption is that we double the number of offspring. This is the intuition for why a linear differential equation makes sense as a benchmark for the population growth equation.

More generally, I would make the claim that population growth is the least objectionable place to locate a linear differential equation in a growth model, for two reasons. First, if we take population as exogenous and feed in the observed population growth rates into an idea-based growth model, we can explain sustained exponential growth. No additional linearity is needed. Second, the intuition above suggests that it is not crazy to think this differential equation might be close to linear: people reproduce in proportion to their number.[36]

This is one example of how the linearity critique can be used productively. Proponents of particular endogenous growth models can seek evidence and economic insights supporting the hypothesis that the particular engine of growth in a model does indeed involve a differential equation that is close to linear.

6.4. Othercontributions

There are a number of other very interesting papers that I have not had time to discuss. These should be given more attention than simply the brief mention that follows, but this chapter is already too long.

Kortum (1997) and Segerstrom (1998) are two important papers that present growth models that exhibit weak scale effects. Both are motivated in part by the stylized fact that total U.S. patents granted to U.S. inventors does not show a large time trend for nearly a century, from roughly 1910 until 1990. If patents are a measure of useful ideas, this fact suggests that the number of new ideas per year might have been relatively stable during a time when per capita income was growing at a relatively constant rate. How can this be? In the models provided above, the stock of ideas grows at a constant rate, just like output. Kortum (1997) and Segerstrom (1998) solve this puzzle by supposing that ideas, at least on average, represent proportional improvements in productivity. The

papers also assume that new ideas are increasingly difficult to obtain, so that in steady state, a growing number of researchers produce a constant number of new ideas, which in turn leads to a constant rate of exponential growth.

Romer (1994a) makes an interesting point that appears (at least based on citations) to have been under appreciated in the literature. The paper considers the welfare cost of trade restrictions from the standpoint of models in which ideas play an important role. In neoclassical models, trade restrictions, like other taxes, typically have small effects associated with Harberger triangles that depend on the square of the tax rate. In contrast, Romer shows that if trade restrictions reduce the range of goods (ideas) available within a country, the welfare affect is proportional to the level of the tax rate rather than its square. As a result, distortions that affect the use of ideas can have much larger welfare effects than those same distortions in neoclassical models.

Acemoglu (2002) surveys a number of important results that come from thinking about the direction of technological change. In this general framework, researchers can choose to search for ideas that augment different factors. For example, they may search for ideas that augment capital or skilled labor or unskilled labor. Other things equal, a market size effect suggests that research will be targeted toward augmenting factors that are in greater supply, especially when these factors can be easily substituted for other factors of production.

Greenwood, Hercowitz and Krusell (1997) and Whelan (2001) focus on the rapid technological change that is associated with the declines in the relative prices of consumer and producer durables (driven in large part by the rapid declines in the quality- adjusted price of semiconductors). Greenwood, Hercowitz and Krusell (1997) show that investment-specific technological change can account for roughly half of per capita income growth in the United States in recent decades. Whelan (2001) extends this analysis by tying it to the introduction of chained indexes in the national income and product accounts.

Finally, it is worth mentioning again that this chapter has largely omitted a very important part of the literature on growth and ideas, that associated with the Schumpeterian models of Aghion and Howitt (1992) and Grossman and Helpman (1991). These models were applied in detail to international trade in Grossman and Helpman (1991). Aghion and Howitt (1998) contain a rich analysis of an even wider range of applications, to such topics as unemployment, the effects of increases in competition, patent races, and leader-follower effects in R&D. In addition to these excellent treatments, a separate Handbook chapter by Aghion and Howitt surveys some of these important topics.

7.

More on the topic Growth accounting, the linearity critique, and other contributions:

- Growth accounting, the linearity critique, and other contributions

- Contributions

- CONTENTS OF VOLUME 1B

- Aghion Philippe, Durlauf Steven N. (eds.). Handbook of Economic Growth. Volume 1. Part B.North-Holland,2005. — p. 1061-1822, 2005

- Oral Accounting

- Humility and oppressive structural power - a critique

- Michel Foucault's provocative critique of the modern prison system, first published in 1975, raises important questions about the evolution of justice in the West.

- The slogans ‘live unnoticed' and ‘do not participate in politics', the inability to perform feats or contributions for the benefit of the community, and the mockery of great politicians of the past all clearly demonstrate the Epicurean disinterest in political communities to their philosophical adversaries.

- A third thesis (and its critique)

- Endogenous growth: Infinite lifetimes