BARGAINING

Economic games may be cooperative or noncooperative depending on whether or not sellers make joint strategies. Negotiations are conducted regarding chargeable interest rates between lenders and borrowers.

Cooperative games may be explained via the following example: If the cost of lendible funds, which includes deposit costs, etc., is 10% and the borrower is willing to pay up to 12%, both the lender and the borrower would be better off if the rate of interest charged on the loan is somewhere above 10% and below 12%.The Case of a Private Borrower

The bargaining process in a bilateral monopoly model under the conditions of rationality and efficiency is described by Gravel and Rees (2004). The same may apply to the banks and their borrowers in India. In India, banks must lend a minimum of 40% ofthe net demand and time liabilities (NDTL) (i.e., aggregate demand and time liabilities minus interbank deposits). For the banking industry as a whole, the proportion of loans continued over many years must be above 60% of the industry NDTL, in view of the risk averse attitudes of some of the banks who turn away from the financial markets and non-government borrowers. Subject to its objectives of the IBA via its website, the following assumptions of bilateral monopoly are necessary for building up a model of bargaining:

1. The IBA plays the role of the Union of the banks;

2. A bank participates in the bargaining on behalf of the Union;

3. On the borrowers’ side, there is a venture capitalist firm as a monopolist in the product market;

4. The product of the above firm with its unique features is not produced by any other firm; and

5. There is no previous record or history of similar businesses.

Assumption 3 is derived from the fact that for a venture capitalist in India without any prior record of success, the cost of raising fund from the capital market may be too high; hence, the need to borrow from a bank.

Assumption 5 implies that: (a) non-bank financial companies do not want to extend credit to the bank and; (b) the firm can approach only a bank for funds because of the social objectives of the banks in India. If Gravel and Rees (2004) is strictly followed with respect to the above loan, the profit function of the firm stands to be:

where

R(L) = PQ(L), C(L) = iL, R(L) = revenue function, C(L)= cost function, L = amount of loan, i = interest rate to be paid by the firm, P = price s = fraction of the loan amount applied for, actually disbursed to the firm,

1-s = proportion ofthe down-payment amount, and Q = quantity sold.

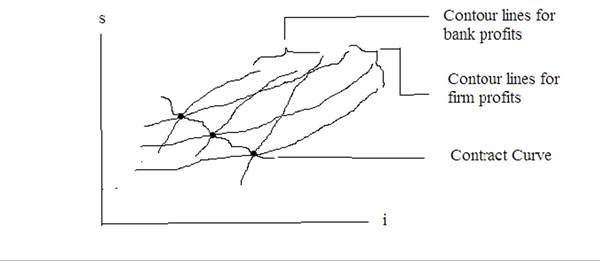

However, this may not be relevant to the bargaining process. Rather, ‘nF’ may be defined to vary inversely with the interested rate ‘i’ as well as ‘1-s’, because in an emerging economy it sounds quite plausible that a budding entrepreneur does not have much cash to start the business. Hence ∏f = f(i, s), where the partial derivatives of ∏f with respect to ‘i’ and ‘s’ are negative and positive, respectively. Since the non-satiation assumption works for ‘ s’, not ‘i’ the contour line in the i-s plane would be positively sloped for a fixed amount of profit from the firm’s viewpoint provided the assumptions of completeness, transitivity, reflexivity and continuity hold here.

The profit function of the bank with respect to the loan is

where r' = reverse repo rate - this is the rate at which the bank park their funds with the RBI. It is the lowest in the fund market.

The above objective function implies that for every one unit of the disbursed loan amount, the bank charges an economic rent ‘i-r” and for the amount of loan not delivered at all, it charges the monopoly interest rate ‘i’. The non-satiation assumption here holds only for ‘i’, not ‘s’, while all other five assumptions those hold for ‘nF’, hold for ‘Ďâ’ also.

For any fixed ∏b the contour lineof the alternative sets of ‘i’ and ‘s' would be a positively sloped line. If ‘i’ and ‘s’ are somehow fixed to be constants and the firm refuses to accept the fractions ‘i’ and ‘s’, it must stop production.

Similarly, the bank must also shut down the lending business if it sticks to a particular combination of ‘i’ and ‘s’. Regarding continuity of the businesses, both parties must reach some agreement via adjustment of these two fractions. Here, both of the parties have positively sloped contour lines for different levels of profit, but the magnitude of the slope would differ depending upon the magnitude of the marginal rate of substitution of ‘i’ for ‘s’ (Figure 1). Again, the slope is likely to increase less for every consecutive equal increase in the interest rate in the case of a lender than it is in the case of a borrower due to the differences in the exact forms of the two objective functions. An intersection between the two is a point of possible agreement. Once the agreement is reached, it is stable because of the legal procedure which follows. The contract curve denotes the set of possible agreement points for consecutive higher and higher levels of profits.

If the bank treats ‘i’ and ‘s’ as constants, there may be no loan agreement and in that case the entire amount ‘L’ may need to be lent to the RBI at the rate ‘rz’. As a case for failure in bargaining, the simple bargaining model in Varian (1992) may apply to the sellers and buyers of funds. Banks prefer to deploy some deposits for one year. Keeping in mind the cost of funds, the bank expects a minimum return of rl per annum from a borrower with some specific credit profile (i.e., AA+). This is the bank’s reservation price of funds for AA+ borrowers. Taking all borrowers across the credit ratings, the minimum reservation price is called the base rate (Reserve Bank of India, 2010). However, every prospective rational borrower (henceforth ‘she’) is willing to pay a maximum cost for funds which is her reservation price given the return from her business or income from her profession.

Both parties are aware of each other’s reservation price. The bank has knowledge about the returns from various businesses and incomes from various professions and the rates charged by other banks to similar borrowers. The bargain revolves around the spread between the above two reservation prices denoted by ‘v’. She places a request for loan with the manager of a bank branch where she has a current or savings account.The manager initially may quote a higher rate than the base rate. She may attempt to depress the rate to a level close the base rate. If she further attempts to bargain down, the manager may make a take-or-leave offer and the bargaining process ends without any result. From start to finish, the entire process may take more than one visit to the branch. If they cannot reach any conclusion after several visits, the loan does not occur. But, owing to the time value of money, inflation etc the spread is being continuously discounted.

Being a rational entity, banks do not wish to retain idle funds. The bank discounts the spread

Figure 1. Contour lines and contract curve

at a daily rate ‘i1’ and she discounts it at a daily rate ‘i2’. If, on the first meeting, the parties did not agree on the loan, the manager retains the idle fund. The present value of the spread for the next day is ψe'i1. This is available to her on the next day to share with the manager provided the bargain leads to lending. But the present value of the spread from her view point is ψe'i2. If she feels the market liquidity condition to be comfortable (i.e., i2 < i1), she may go to another bank because she will not accept the position ψe-i1 < ψe-i2. However, if the market is suffering from a liquidity crisis, she may agree to borrow. But even if the manager feels a lack of demand for funds owing to comfortable market liquidity, he can not offer a higher spread than ψ by offering a rate below the base rate. The base rate works as a constraint on the bargaining process. It imposes a downward restriction on the price discovery process in the loan market.

More on the topic BARGAINING:

- Wage Bargaining and the Wage Equation

- CONCLUSION: PREVENTING BARGAINING FAILURE

- The self-curing failures of the Coasean bargaining

- Integrative Negotiation

- Distributive Negotiation

- Labor-Management Conflict

- REFERENCES

- THE PROCESS OF CONFRONTING TERRORIST-RELATED CONFLICT

- What We Know

- Aaron Director and Labor Problems