PRISONERS’ DILEMMA

A detailed concept of the Prisoners’ Dilemma is provided by Kuhn (2007).

The Prisoners’ Dilemma in an Oligopolistic Structure

Stories of the water meter and airlines industries (Pindyck & Rubinfeld, 1995, p.

467) may resemble that of the Indian banking industry in that the lending business of the public sector banks was almost threefold that of the private sector banks during the financial year 2011-2012 (Reserve B ank of India, 2012). The ratio remained the same in the previous financial year. This consistency may act as a barrier to the entry of a new private sector bank. In this circumstance, the Indian public sector banks may cooperate and divide the market between themselves. However, if they chose competition in lieu of cooperation they may earn only a modest profit. Thus one may consider the Prisoners’ Dilemma among these banks.The Issue of Predatory Pricing

Recently, the RBI approved the entry of serious corporate players into the banking industry (Prasad, 2013). A major policy departure by the State Bank of India by offering zero balance savings accounts may be conceived as predatory pricing with a view to discourage the entry of well-established corporate houses to the banking business (Kurain, 2013).

The Prisoners’ Dilemma and the Lender-Borrower Game

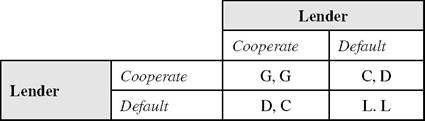

Following the symmetric 2x2 Prisoners’ Dilemma with ordinal payoffs in Kuhn (2007), one may conceive a game between a lender and a borrower. There may be two cases of cooperation in this case:

1. The borrower is steadily paying the EMIs and the lender is happy - this is the case of a borrower with the top most score given by the CIBIL (Credit Information Bureau (India) Limited, 2013);

2. The borrower defaults and both parties agree to go for a loan restructuring (Alexander & Antony, 2012).

There may be three cases of non-cooperation when the borrower defaults;

1.

Only the borrower disagrees to any loan restructuring;2. Only the lender disagrees to any loan restructuring and

3. Neither agrees to a loan restructuring.

One may substitute

1. ‘Lender’ with ‘Row,

2. ‘Borrower’ with ‘Column’,

3. ‘Default’ with the term ‘Defect’,

4. ‘R’ with the term ‘Gain’ or ‘G’ and (v) ‘P’ with the term ‘Loss’ or ‘L’.

One may interpret ‘T’ as temptation of not cooperating alone and ‘S’ as surplus generated out of cooperating alone. Thus may be obtained the pay-off matrix in Table 4.

The pay-offs are ordinal (i.e., comparable with respect to being less or more), but the exact amount or quantity thereof cannot be known. There may be alternative situations of the Prisoners’ Dilemma given:

Table 4. The lender-borrower game

• Strict Inequality: D > G > C > L, in this case where defaulting is a strictly dominating strategy when the present value of the collateral mortgage is less than the present value of the exposure at default (i.e. outstanding loan). There is no need to assume any other loan covenant except a collateral mortgage. When the present value of the collateral mortgage is more than the present value of the exposure at default, the strict inequality is C > D (i.e. cooperation is the strictly dominating strategy).

• Weak Inequality: D ≥ G > L > C, when the present value of the collateral mortgage is equal to the present value of the exposure at default defecting may be weak strategy as a dominating strategy.

More on the topic PRISONERS’ DILEMMA:

- The dilemma of rules

- The Agency-Based Collectivist Argument from the Discursive Dilemma

- Developments in the New Welfare Economics and the Economic Theories of Justice

- Evolution of property rights

- References

- Punishing was one thing, preventing another. If the state could head crime off at the pass, it would save itself enormous bother.

- Democracy, Revolution and Terrorism

- The Red Word ofIvan Kulyk

- 14 The Magistracy - a Professional Court?

- JUDICIAL INTERVENTION