STOCK INVESTMENT STYLES

Stocks constitute a considerable part of investment portfolios. Thus, high importance should be placed on stocks and stock investment styles before choosing a particular portfolio investment strategy.

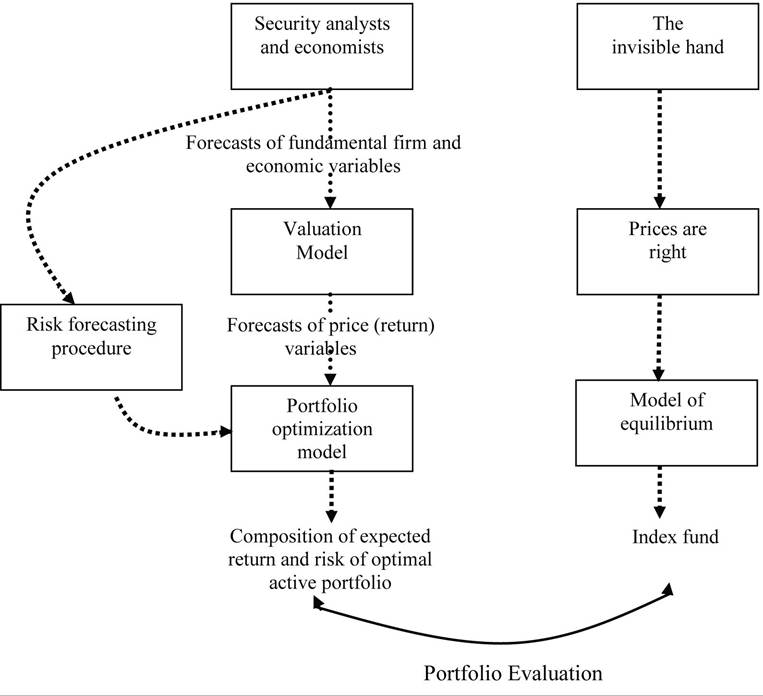

Deciding on the correct stock investment style is regarded as the most critical step of investment decision procedures.Figure 2. Stock portfolio management strategies

Source: Elton, E. J., & Gruber, M. J. (1995) Modern Portfolio Theory and Invesment Analysis, Fifth Edition, p. 688. New York: John Wiley and Sons Inc.

The concept of investment style refers to the goals of a portfolio manager and the types of assets held in the portfolio (Rao, 2006). Investment style might also refer to the categorization of stock managers according to their performance. An investment manager’s performance within the market is closely related to the investment style employed (Bailey, Richards, & Tierney, 2007, p. 780). Different investment styles were developed near the end of the 1960s. In his 1966 study, William Sharpe defined investment style as the stock investors’ tendency to invest on some particular stock groups1. Stock investment styles became widespread in various Indexes in following years.

Later, Wilshire Associates and the Frank Russel Company created their own stock investment style Indicies in 1978 and 1979, respectively (Ahmed, Gallo, Lockwood, & Nanda, 2003, p. 294).

To express an investment, descriptive terms such as growth, income, momentum and value are often used. The most widespread investment style categories are value and growth investments. In addition to these categories, there are various investment styles in which portfolios are splitted into different sub-categories (e.g., small-cap, mid-cap, and large-cap) according to their market capitalizations.

The core idea of stock portfolio investment styles is to hold the stocks sharing the same characteristics under the same style category. The stocks within the same categories have similar risk and profit characteristics while they show different risk and profit characteristics than the stocks in different categories in time (Ahmed, Gallo, Lockwood, & Nanda, 2003, pp. 293-294).Value vs. Growth Investing

The concepts of “value” and “growth” have a long history in the field of stock investment management, and both concepts are widely used in defining investment management funds and classifying stocks (Michaud, 1999, p. 1). With the rise of institutional investments, security analysts have been separated into two groups since the 1960s; value investing and growth investing (Speidell & Graves, 2003, p. 172).

Growth stock portfolio strategy was first introduced by two professional investors, David

L. Babson and T. Rowe Price, during the period following World War I when there was remarkable economical growth (Bauman, Conover, & Miller, 1998). Babson (1951)2 and Price claimed that investing in firms with above-average growth provides very high portfolio performance (Bauman & Miller, 1997). In the following years, value stock portfolio strategy attracted attention as another alternative to growth strategy. In fact, the value stock portfolio strategy was first championed in the early 1930s by Benjamin Graham and David Dodd, the pioneers of Fundamental Security Analysis (see also Graham & Dodd, 1934).

Value Investment Style

The roots of value investment style date back to the book, Security Analysis, written by Graham and Dodd in 1934. In this method, stocks which are under-priced or priced correctly have an ascending potential (Shi & Seiler, 2002). Value investing is based on choosing less expensive stocks compared to some particular variables which include the following:

1. Profits-per-stock or price/profit ratios;

2.

Cash flows per stock or price/cash flow ratios;3. Books values per stock; and

4. Market price/book value ratios (Estrada, 2005).

Fund managers preferring value investing strategies usually detect solid companies although they may not be very popular3. The fund managers then buy these companies’ stocks at bargain prices. Most investors preferring value investing strategy believe the majority of the value stocks arise from misvaluations of risk and profit potentials or over reactions given to negative events (Gastineau, Olma, & Zielinski, 2007, p. 432). The basic idea behind this strategy is that when the real values of the companies’ stocks are finally noticed, the value of those stocks will increase (Wilkens, Heck, & Cochran, 2006). Nonetheless, sometimes investors do not notice the real values for an extended period of time or it never occurs. Therefore, value investors are those investors who are eager to wait and be patient for a long time to obtain their reward (Sincere, 2004, p. 72; Strong, 2007, p. 156).

The typical characteristics of value investing can be summarized as follows (Little, 2007):

• The profits of the companies per share are above average.

• The profit shares of the companies are high.

• Sectors in which companies operate are well-grounded.

• Stock holding period is usually longer than that of growth stocks.

However, while value investment is defined as the investments on under-valued stocks which have lower Price/Profit (P/P) and Market Price/ Book Value (MP/BV) ratios, this definition is not adequate to reflect varying investor behaviors. When classifying under-valued stocks, some value investors consider specific criteria and make long term investments on stocks, while others believe the best time to buy stocks is when there are big sales and the prices decrease. However, some value investors behave more actively and purchase great quantities of stocks of firms they believe are under-valued, and they believe the values of such stocks will increase.

Therefore, they begin pressing companies to make changes so the values will increase sooner (Damodaran, 2003, p. 219). The common principle behind the value investing style is the idea that the best investments are those made from companies having internal or sectoral problems and are otherwise out of favor.Growth Investing Style

Another active portfolio management approach is the Growth Investing Strategy. The main idea of the growth investing is focusing on the growing or potentially growing stocks (Shi & Seiler, 2002). In other words, growth investing strategies focus on firm having considerable growing potential and higher prices compared to profits, cash flows, book values, bonuses, or other factors (Estrada, 2005). Low current return levels and high MP/ BV and P/P ratios are the typical features of the growth investing portfolios (Bodie, Kane, & Marcus, 2003, p. 290).

Managers preferring growth investing seek companies with strong performance, are of high quality, and have important achievements such as patents. The investors are ready to pay high prices for those progressive company stocks in hopes of selling them for even higher prices in the future. The risk here is that the value of such companies’ stocks could decrease sharply due to negative rumors about them4. Another risk is the prospective profits expected per share might not be realized (Gastineau, Olma, & Zielinski, 2007, p. 433).

The typical characteristics of growth investing can be summarized as follows (Little, 2007):

• The companies show higher ratios than their average growth ratios of return and profit.

• The companies serve in expanding sectors.

• The companies do not pay profit shares.

• High growth companies usually go beyond their expected profits.

• The length of the stock holding periods is determined by the growth regularity of the company.

Growth stock managers concentrate on identifying stocks for which growing expectation is high (Michaud, 1999, p.

1). Additionally, they tend to make investments on large and progressive sectors such as technology, health care, and consumer goods (Gastineau, Olma, & Zielinski, 2007, p. 433). In summary, growth investors make investments on the companies which are growing and whose profits are increasing, while value investors make investments on firms being traded at lower prices or having small earnings. Table 1 presents the strategies for value and growth investors.Table 1. Preferences of value and growth investors

| Value Investors | Growth Investors |

| Prefer the companies reporting sank profit margins. | Prefer healthy and ascending margings. |

| Seek companies with descending gains or with no gain at all. | Search for companies having sharply increasing profit ratios. |

| Search companies whose recent profit reports have caused disappointment within the market | Determine the companies having positive surprises with their profits. |

Source: Domash, H. (2006). Fire Your Stock Analyst: Analyzing Stocks on Your Own. Financial Times, p. 262. New York: Prentice-Hall

Inc.

Widespread use of value and growth investing strategies in active portfolio management is one of the most significant developments of recent years (Reilly &Brown, 1999, p. 670).

Value and Growth Investing Strategies as Mutual Complementaries

Growth and value investing strategies are not opposites; instead, they are different approaches to the same basic matter. Both strategies guide the investors through the choice of stocks. Though it is not possible to say exactly which strategy will bring more profit in the long-term, some studies argue that value investing strategies showe better performance than growth investing strategies. For example, Capaul, Rowley and Sharpe (1993) examined both strategies in different countries, suggesting that value investing portfolios bring higher profits.

Similarly, Arnott and Luck tested the performance of both strategies between January, 1975 and July, 2001 in Canada, England, Japan, Germany, and the USA to discover that value portfolios showed better performance than growth portfolios, except during the global technology bust which is also referred to as the Dot.com bubble of 2000.The changing nature of value and growth investing, which often overlaps with each other, pushes investors to seek new ways to solidify their positions. Some investment advisors state the best investment strategy is to construct half of a portfolio using the value approach and the other half using the growth investing approach. For example, the long-standing investment advisory firm Bernstein Global Wealth Management reported that the investing strategy having the best risk/profit profile is multi-style investing:5

...multiple investing style requires the investors to split the capital into the best bergains and best companies of the market. When either of those investments shows a bad performance, the other will balance it. The investor will get higher and more consistent profits comparing to any single style.

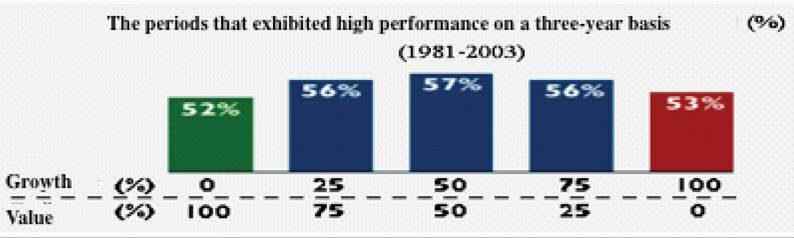

Figure 3 shows the result of the study conducted by Bernstein Global Wealth Management

Figure 3 shows the longest lasting high performance is achieved through multi-style investing. Beyond equal sharing of the two styles, any mixture of value and growth investing at any ratio shows higher performance than does that of their single use. Another solution for the fluctuation problem in value and growth investing strategies is to switch a poorly performing investing style with the other one immediately (Tengler, 2003, p. 3; Arnott & Luck, 2003, pp. 55-58), which also called the “active style switching strategy.” Arnott and Luck (2003) attempted to clarify which approach has higher performance by calculating the total return of US$1.00 invested in the value, growth, and active switching strategies. They limited their study in between January, 1975 and February, 2002.

Figure 3. Different compositions of value and growth investment strategies

Source: Mercer Investment Consulting, Standard & Poor's and Bernstein, Bernstein Global Wealth Management, “Multi-Style Investing: A Tale of Two Investment Styles. ”

Table 2 shows the growth of 1 US dollar invested using the value, growth, and active style switching strategies. When an active style switching strategy based on correct estimations is employed, it is obvious profit will be much higher than that of the value and growth investing strategies. The biggest challenges of the active style switching strategy are the high transaction costs and the difficulty of making correct estimations. In the very right column of Table 2 are the percentages of the months the growth strategies showed higher performance than value investing strategies. This supports the view that the value investing strategies are more efficient than growth investing strategies.

Momentum Investment Style

The concept of momentum is based on the movement of the speed of prices. Stocks with fast and continuous price movements are called “momentum stocks” (Uludag, 2007, p. 9). The investors adopting this style believe the stocks with high price performances will retain their high performance for an extended period of time. In other words, they prefer buying and selling the stocks for high prices. Typical characteristics of momentum stocks are as follows (Mitchell, 2007):

• Daily, weekly, or monthly relative price changes in high percentages.

• Sharp ascending from low volume range to high volume range.

• High profit development in short terms (e.g., 3-month periods.)

• Increase-oriented changes in the estimations of analysts.

• High cash flows addressing stocks which signal the institutional investors’ purchases.

Momentum investors purchase stocks having the highest dynamism in the market in the belief that the current increase will continue (Gastineau, Olma, & Zielinski, 2007, p. 433). The risk of this style is the possibility that investors might fail in selling the stocks before their increasing performance gets weaker. The momentum strategy, which is based on the idea that past tendencies will continue in the future, can be divided into two sections: price momentum and earning momentum (Reilly & Brown, 1999, p. 665). The price momentum strategy is briefly defined as buying the high performing stocks and selling the poorly performing stocks by observing their recent performances (Bird, Casavecchia, & Woolley, 2008). The earning momentum strategy is a type of active investing strategy which focuses on the companies showing high profit growth during 3-month periods during the year (Maginn, Tuttle, McLeavey, & Pinto, 2007, p. 870).

Table 2. Performance comparison of the value, growth, and active style switching strategies

| Yearly Growth of 1 US Dollar in 26 Years (1/75-2/02 Returns) | The Percentage of the Months in which Growth> Value | |||

| Countries | Value | Growth | Active Swithing* | |

| America | 51 | 33 | 231 | 45 |

| England | 102 | 57 | 465 | 45 |

| Japan | 16 | 3 | 74 | 42 |

| Canada | 31 | 10 | 768 | 46 |

| Germany | 29 | 13 | 186 | 48 |

* It was assumed the money was invested on the better one of value and growth strategies and the transaction cost equalled one percent.

Source: Arnott, R. D., & Luck, C. G. (2003). The Many Elements of Equity Style: Quantitative Management of Core, Growth, and Value Strategies. The Handbook of Equity Style Management, Third Edition, Edited by T. D. Coggin and F. J. Fabozzi, p. 58. New York: John Wiley & Sons Inc.

Technical Investment Style

The methods used in most investment strategies are techniques labeled technical analysis by market actors (French, 1989, p. 362). The technical analysis approach assumes the best way to estimate the stocks’ future is to scrutinize the past actions of interest rates, stock prices, and other market variables (Reilly & Brown, 1999, p. 408). Beyond the matter of which stocks to select, investors using technical analysis specialize on when to buy those stocks as well. In this style, investors examine the early trends of companies and stocks, but do not concern themselves with internal activities such as fundamental investors do (Kiyosaki & Lechter, 2000). Instead, technical investors believe all factors concerning a company are already reflected in the stock prices and therefore largely ignore factors such as financial tables, fiscal policies, economical climates, or sectoral tendencies (Dourraa & Siy, 2000). They make use of price graphics, formations, and market indicators to analyse stock markets.

Market indicators are generally divided into three categories (Dourraa & Siy, 2000):

• Monetary Indicators: These are the economic data such as interest rates and signal the economic climates in which the companies serve. Such external factors directly affect the profitability and stock price of the company.

• Sentiment Indicators: Indicators concerning investors’ expectations.

• Momentum Indicators: Signs such as price/trading volume indicators, the correlations between the number of ascending and descending stocks, and comparisons of changing trading volumes.

The technical investment style is advantageous as it is easy to learn and practice because it does not require subjective judgement or financial wisedom and all necessary information is easy to obtain (French, 1989, p. 372). However, there are some criticisms regarding this style (Reilly & Brown, 1999, p. 629). First, the idea that stock prices reflect all the needed information and it is easy to obtain implies the existence of a weak form of market activity. Furthermore, empirical studies support the active market hypothesis. Therefore, it does not seem possible any investor can profit above the market line. In addition, when all investors use the same information to make identical investment decisions, it is not possible for any investor to have a gain as the stock price will then gravitate towards a new balance. However, once the technical investing method is successful, all other investors will practice this method and will no longer be advantageous anymore.

Income Investing

Income investors act on those stocks which exhibit high, reliable, and continuous profit. These so-called income stocks belong to firms earning higher profit compared to the stock prices (Mittra & Gassen, 1981, p. 24). The profits belonging to these stocks are usually above that of average stocks and possess the potential to compete with debt securities. In addition, a sound and standing profit policy provides reliable information about the companies’ future performance and income stream (Tengler, 2003, p. 24). It is very important for these investors to estimate income streams. Income investors deal with the current return of the stock prices rather than their appreciation (Mit- tra & Gassen, 1981, p. 24). Income investing is a long-term and low risk investing style (Mitchell,

2007), and income-focused portfolios usually have lower risk levels are often composed of fixed yield securities like bonds (Bronson, Scanlan, & Squires, 2007, p. 35).

Fundamental Investing

Fundamental investing strategy is based on the ideas of fundamental analysis. While fundamental analysis is a combination of methods assessing future gains potential and making deductions through the examination of the financial condition of the companies, the fundamental investing strategy is a tool using the findings obtained from fundemantal analysis (French, 1989, p. 362). In this strategy, investors focus on macro-economic events, sectoral developments, and basic information about the companies (e.g., financial statements). The executives of fundamental investing have a pretty long term perspective and they ground their investment decisions on the comparison of the intristic value which is reached through the stock’s current price and long term assessment of the company (Koller, Goedhart, & Wessels, 2005, p. 538). They argue the stocks should be purchased for a price below their intristic value.

Fundamental investors believe there are intristic values which depend on the economic conditions of prices, and that these values should be assessed by examining factors such as current profits, cash flows, interest rates, and risk variables (Reilly & Brown, 1999, p. 198). Considering the sector and the overall economy, investors can analyze financial statements of companies in detail. Providing the market value of a stock is lower than the intristic value and the difference covers the sanction costs, they then purchase that particular stock (Bird, Casavecchia, & Woolley,

2008). Fundemantal investing is superior to technical investing as the former is based on facts about the company and are more practical according to the efficient market hypothesis. Nonetheless, this strategy is criticized because the company data and analysis results can reach investors late; in addition, sometimes the balance sheets distract investors from actual conditions (Karan, 2004, p. 439).

Market Capitalization Investing

Market capitalization is the value obtained by multiplying the market value of a company’s stocks with the number of outstanding stocks. Market capitalization is a criterion of a company ’ s magnitude (Dow, 1998; Faerber, 2008, p. 216). It is also an important criterion for investors when choosing stocks. Stocks belonging to small companies provide fast developing potential and small research areas to investors, while stocks belonging to large companies provide stability, diversified returns, presumable profits, and a parallel position to the market index6 (Mitchell, 2007).

Company magnitude is among the variables which are widely used to measure long term abnormal gainings in the extant financial lit- erature7. When studies were conducted, it was seen that small companies sometimes exhibited better performance than big companies or vice versa. However, in the long-term, it was proven that companies with small market capitalization showed better performance than those companies with high market capitalization. Banz (1981) and Reinganum (1981) showed in their study that small companies provide higher rates of return than do large companies. They found that even after making necessary arrangements on the stocks against risk there were systematic differences in average returns.

Fama and French (1992) stated that variables of company magnitude and the book value/ market value could successfully explained the differences in the average stock returns in the period of 1963-1990. They reached that the high returns that the small companies provided were the counter balance of the high risks they have. On the other hand, since the size effect8 could not explain much in the period 1977-1990, they concluded that size effect is not explanatory in some periods. Reinganum (1983) studied on long term portfolio strategies and he found that the small companies’ rates of return are considerably high even without daily rebalancing. Accordingly, the value of 1 dollar invested on the smallest company at the end of 1962 became higher than 46 dollars at the end of 1980. On the other hand, during the same period, the portfolio composed of big companies provided a growth of 4 dollars only; and medium- sized companies provided a growth of 13 dollars. As a whole, it was observed that the portfolios composed of small companies showed higher performance. It is always stated by professionals or academics that there should be a systematic approach in choosing stocks. There exist many studies and sources which are full of recommendations on stock choosing and portfolio construction.

REFERENCES

Ahmed, P., Gallo, J. G., Lockwood, L. J., & Nanda, S. (2003). Multistyle equity investment models. In T. D. Coggin, & F. J. Fabozzi (Eds.), The Handbook of Equity Style Management (3rd ed.). Hoboken, NJ: John Wiley & Sons Inc.

Arnott, R. D., & Luck, C. G. (2003). The many elements of equity style: Quantitative management of core, growth, and value strategies. In T.

D. Coggin, & F. J. Fabozzi (Eds.), The handbook of equity style management (3rd ed., pp. 47-74). Hoboken, NJ: John Wiley & Sons Inc.

Bailey, J. V., Richards, T. M., & Tierney, D. E. (2007). Evaluating portfolio performance. In J. L. Maginn, D. L. Tuttle, D. W. McLeavey, & J. E. Pinto (Eds.), Managing Investment Portfolios: A Dynamic Process (3rd ed.). Hoboken, NJ: John Wiley & Sons Inc.

Banz, R. W. (1981). The relationship between return and market value of common stocks. Journal of Financial Economics, 9, 3-18. doi:10.1016/0304-405X(81)90018-0

Bauman, W. S., Conover, C. M., & Miller, R. E. (1998). Growth vs value and large cap vs small cap stocks in international markets. Financial Analysts Journal, 54(2), 75-89. doi:10.2469/faj. v54.n2.2168

Bauman, W. S., & Miller, R. E. (1997). Investor expectations and the performance of value stocks versus growth stocks. The Journal of Portfolio Management, Spring, 23(3), 57-68.

Bird, R., Casavecchia, L., & Woolley, P. (2008). Insights into the market impact of different investment styles. Retrieved from http://econpa- pers.repec.org/RePEc:uts:pwcwps:1.

Bodie, Z., Kane, A., & Marcus, A. J. (1996). Investments (3rd ed.). New York: McGraw-Hill Inc./Irwin.

Bodie, Z., Kane, A., & Marcus, A. J. (2003). Essentials of investments (5th ed.). New York: The McGraw-Hill Companies.

Bronson, J. W., Scanlan, M. H., & Squires, J. R. (2007). Managing individual investor portfolios. In

J. L. Maginn, D. L. Tuttle, D. W. McLeavey, & J.

E. Pinto (Eds.), Managing investment portfolios: A dynamic process (3rd ed.). Hoboken, NJ: John Wiley & Sons Inc.

Capaul, C., Rowley, I., & Sharpe, W. F. (1993). International value and growth stock returns. Financial Analysts Journal, 49(1), 27-36. doi:10.2469/faj.v49.n1.27

Damodaran, A. (2003). Investment philosophies: Successful strategies and the investors who made them work. New York: John Wiley & Sons Inc. Dixit, A. K., & Pindyck, R. S. (1994). Investment under uncertainty. Princeton, NJ: Princeton University Press.

Dourraa, H., & Siy, P. (2002). Investment using technical analysis and fuzzy logic. Fuzzy Sets and Systems, 127, 221-240. doi:10.1016/S0165- 0114(01)00169-5

Dow, C. G. (1998). Large cap versus small cap investing. Retrieved from http://www.dows.com/ Publications/large_cap_versus _small_cap.htm

Elton, E. J., & Gruber, M. J. (1995). Modern portfolio theory and invesment analysis (5th ed.). New York: John Wiley and Sons Inc.

Estrada, J. (2005). Adjusting P/E ratios by growth and risk: The PERG ratio. International Journal of Managerial Finance, 1(3), 187-203. doi:10.1108/17439130510619631

Faerber, E. (2008). All about stocks: The easy way to get started (3rd ed.). New York: McGraw-Hill.

Fama, E. F., & French, K. R. (1992). The cross-section of expected stock returns. The Journal of Finance, 47(2), 427-465. doi:10.1111/j.1540-6261.1992.tb04398.x

French, D. W. (1989). Security and portfolio analysis: Concepts and management. Columbus, OH: Merrill Publishing Company.

Gastineau, G. L., Olma, A. R., & Zielinski, R. G. (2007). Equity portfolio management. In J. L. Maginn, D. L. Tuttle, D. W. McLeavey, & J. E. Pinto (Eds.), Managing investment portfolios: A dynamic process (3rd ed., pp. 407-476). Hoboken, NJ: John Wiley & Sons Inc.

Gitman, L. J., & Joehnk, M. D. (1988). Fundamentals of investing (3rd ed.). New York: Harper and Row Publishers.

Grinold, R. C., & Kahn, R. N. (2000). Active portfolio management: A quantitative approach for providing superior returns and controlling risk (2nd ed.). New York: McGraw-Hill Company. Horowitz, J. L., Loughran, T., & Savin, N. E. (2000). The disappearing size effect. Research in Economics, 54, 83-100. doi:10.1006/ reec.1999.0207

Istanbul Menkul Kiymetler Borsasi (IMKB). (2008). Menkul kιymetlere yatιrιm. Retrieved from http: //www.imkb.gov. tr/Libraries/Egi - tim_Setleri/menkul_k%c4%b1ymetlere_ yat%c4%b1r%c4%b1m.sflb.ashx

Karan, M. B. (2004). Yatirim analizi ve portfoy yonetimi. Ankara, Turkey: Gazi Kitabevi.

Kiyosaki, R. T., & Lechter, S. L. (2000). Rich dad’s guide to investing: What the rich invest in, that the poor and the middle class do not! Retrieved from http://olesiafx.com/Rich-Dad-s-Guide- To-Investing-What-The-Rich-Invest-In-Robert- Kiyosaki/24.The-qualified-investor-fundamental- investing-technical-investing-stock.html

Koller, T., Goedhart, M., & Wessels, D. (2005). Valuation: Measuring and managing the value of companies (4th ed.). New York: John Wiley & Sons Inc.

Little, K. (2007). Getting started in stocks: Growth or value investor? Understanding value and growth stock investing is smart move. Retrieved from http://stocks.about.com/od/tradingbasics/ a7072707Buy1.htm

Maginn, J. L., Tuttle, D. L., McLeavey, D. W., & Pinto, J. E. (2007). Managing investment portfolios: A dynamic process (3rd ed.). Hoboken, NJ: John Wiley & Sons Inc.

Michaud, R. O. (1999). Investment styles, market anomalies and global stock selection. New York: The Research Foundation of The Institute of Chartered Financial Analysts, Wiley-Blackwell.

Mitchell, L. (2007). A beginner’s guide to investment styles. Retrieved from http://www. moneyweek.com/investment-advice/a-beginners- guide-to-investmen t-styles.aspx

Mittra, S., & Gassen, C. (1981). Investment analysis and portfolio management. New York: Harcourt Brace Jovanovich Inc.

O’Shaughnessy, J. P. (2005). Whatworks on Wall Street: A guide to the best-performing investment strategies of all time (3rd ed.). New York, NY: McGraw-Hill Companies.

Rao, D. N. (2006). Investment styles and performance of equity mutual funds in India. Retrieved from http://ssrn.com/abstract=922595.

Reilly, F. K., & Brown, K. C. (1999). Investment analysis and portfolio management (6th ed.). New York: Dryden Press, WB Sounders-Harcourt College Publishers.

Reinganum, M. R. (1981). Misspecification of capital asset pricing: Empirical anomalies based on earnings’ yields and market values. Journal of Financial Economics, 9, 19-46. doi:10.1016/0304- 405X(81)90019-2

Reinganum, M. R. (1983). Portfolio strategies based on market capitalization. Journal of Portfolio Management, 9(2), 29-36. doi:10.3905/ jpm.1983.408902

Sharpe, W. F., & Alexander, G. J. (1990). Investments (4th ed.). Englewood Cliffs, NJ: PrenticeHall Inc.

Shi, S. W. W., & Seiler, M. J. (2002). Growth and value style comparison of U.S. stock mutual funds. American Business Review, 20(1), 25-32.

Sincere, M. (2004). Understanding stocks. New York: The McGraw-Hill Companies Inc.

Sorensen, E. H., Miller, K. L., & Samak, V. (1998). Allocating between active and passive management. Financial Analysts Journal, 54(5), 18-31. doi:10.2469/faj.v54.n5.2209

Speidell, L. S., & Graves, J. (2003). Are growth and value dead? A new framework for equity investment styles. In T. D. Coggin, & F. J. Fabozzi (Eds.), The handbook of equity style management (3rd ed.). Hoboken, NJ: John Wiley & Sons Inc.

Stowe, J. D., Robinson, T. R., Pinto, J. E., & McLeavey, D. W. (2002). Analysis of equity in- vestmentes: Valuation. Baltimore, MD: United Book Press Inc., Association for Investment Management and Research.

Strong, R. A. (2007). Management for practical investing (4th ed.). Toronto, Canada: Cengage Learning.

Tengler, N. (2003). New era value investing: A disciplined approach to buying value and growth stocks. New York: John Wiley & Sons Inc.

Uludag, D. T. (2007). Value stocks vs. growth stocks: A comparison of the investment styles and an analysis of Istanbul stock exchange. Ankara, Turkey: Capital Markets Board of Turkey.

Wilkens, K. A., Heck, J. L., & Cochran, S. J. (2006). The effects of mean reversion on alternative investment strategies. Managerial Finance, 32(1), 14-38. doi:10.1108/03074350610641848

KEY TERMS AND DEFINITIONS

Active Portfolio Management: Active portfolio management objects passive portfolio management and accepts markets are not effcient in all form of efficiency. Therefore, a portfolio manager can get abnormal return on markets by using different investment strategies and tactics.

Growth Investing Style: Growth investing style focuses to find stocks that has a growth potential in future.

International Stock Investment: Selecting worldwide-based investment instruments such as foreign stock, emerging markets stock etc. as part of an investment portfolio.

Passive Portfolio Management: Passive portfolio management defends, markets are efficient and and investor can’t get abnormal return. Thus, an investor should hold market portfolio instead of holding single stocks. Buy and hold strategy and indexing strategy are passive portfolio management stragies.

Portfolio Management Strategies: Portfolio management is about maximazing the return of portfolio at a given risk level. In portfolio management process, assets are allocated among different investment instruments.

Stock Investment Styles: Portfolio managers can choose stocks by using different types of investment styles such as growth investing style, value investing style, momentum investing style, technical investing style, income investing style, fundamental investing style and market capitalization investing style.

Value Investing Style: Value investing style focuses to find mispricing and qualified stocks.

ENDNOTES

Sharpe, W. (1966) “Mutual Fund Performance,” Journal of Business, 39, 119-138. See also, Babson, D. L. (1951) “The Case of Growth vs. Income Stocks on a Yield Basis,” David L. Babson and Company Inc., Weekly Staff Letter, September 17, 1951.

Value investors had significant profits in the past. For instance, oil stocks, having very high values in 70s, decreased dramatically and some investors bought these pretty cheap stocks in 1980s and they got great profits afterall. Similarly, after Clinton’s fail in his effort to reform the health policies, the stock values of health sector decreased and some investors made investments on those stocks

and they got considerable profits in return (Tengler, 2003: 1).

TDAmeritrade, “Growth vs. Value: Two Approaches to Stock Investing,”

Bernstein Global Wealth Management (2004), “Multi-Style Investing: A Tale of Two Investment Styles,” http://www.bernstein. com/public/story.aspx?cid=744&nid=185. As the companies having high market capitalization are bigger than the companies having low capitalization they can be assumed to have a safer structure. Nonetheless, the companies having very low capitalization values have bigger growing potential as they are small in present.

See also.: Banz, R. W. (1981) “The Relationship Between Return and Market Value of Common Stocks,” Journal of Financial Economics, 9, 3-18; Reinganum, M. R. (1983) “Portfolio Strategies Based on Market Capitalization,” The Journal of Portfolio Management, Winter, Vol: 9, No: 2, 29-36; Horowitz, J. L., T. Loughran ve N. E. Savin (2000) “The Disappearing Size Effect,” Research in Economics, 54, 83-100.

Size effect is the term which is used to express the tendency that the small companies have higher returns than the big companies (Horowitz, Loughran, & Savin, 2000: 97).

This work was previously published in Economic Behavior, Game Theory, and Technology in Emerging Markets, edited by Bryan Christiansen and Muslum Basilgan, pages 368-384, copyright 2014 by Business Science Reference (an imprint of IGl Global).

518

More on the topic STOCK INVESTMENT STYLES:

- THE PORTFOLIO CONCEPT

- THE CONCEPT OF INVESTMENT AND INVESTMENT PROCESS

- INVESTMENT AND PROJECT

- Section 6 Emerging Trends

- ABSTRACT

- REGIONAL DEVELOPMENT AND INVESTMENT BANKS

- Countless books have been written on the subject of “picking stocks.”

- Taking stock of situationism

- PM STANDARDS AND INVESTMENT ANALYSIS

- Inde