Technological Factors

While online banking features have made banking services convenient and available, the advancement of technology and the development of the Internet have also led to concerns for the security of customers’ personal information and internet transactions (Bakar et al., 2011).

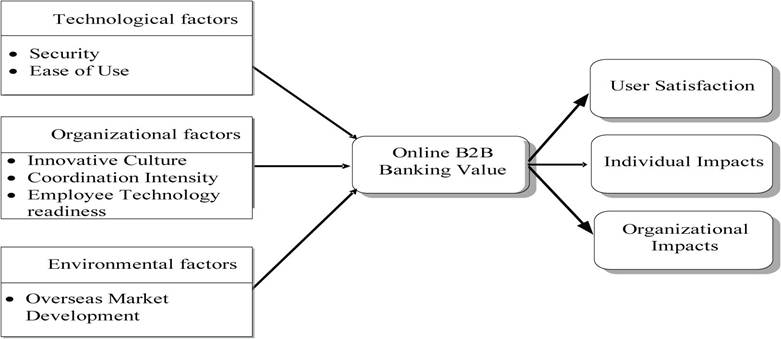

Financial institutions have moved to protect the information transmitted and processed when banking online (Makowski, 2007). However, threats such as phishing and personal identify fraud are growing and making online banking vulnerable to unauthorized use (Bakar et al., 2011). Banks have no control over the systems used by their customers and thus cannot control risks caused by such systems. For this reason, the banks cannot assume liability for them. Moreover, laws related to security and privacy issues remained unclear, which affects whether online banking is perceived as trustworthy by its users (Chong, Ooi, Lin, & Tan, 2010). Customers consider security to be very important when making online transactions. In B2B e-markets, security is one of the most influential factors for firms (Zhao, Wang, & Huang, 2008). Previous research has also argued that security was a significant determinant of online banking (Yoon, 2010). Further, the e-commerce literature considers security a significant determinant of the perceived value of Internet technology (Yang & Peterson, 2004). If customers do not trust organizations within the context of the security provided, employees’ perceptions of the value of doing business with such customers are likely to be weakened.On the other hand, the Internet channel has been found to improve the efficiency of business transactions. It saves employee time and effort and reduces transaction costs. Ease of use of Internet transactions plays a pivotal role in customer satisfaction with online services (Yang & Peterson, 2004). Online B2B banking offers ease- of-use functions to firms in making transactions over Internet. Such a facility may be beneficial for firms in assessing international as well as domestic customers, ultimately increasing their market reach. Thus, they are likely to gain value from it. In particular, ease of use is an important antecedent to perceived value for new adoption (Ko, Kim, & Lee, 2009; Venkatesh, Ramesh, & Massey, 2003). Presently, in the B2B context online banking remains immature. Its value as experienced by employees is thus more likely to grow with increased ease of use of e-banking systems. Therefore, we hypothesize (Figure 1):

H1: The higher the degree of the system security, the greater will be the online B2B banking value;

Figure 1. Research framework

H2: The higher the ease of use in online banking system has, the greater will be the online B2B banking value.

More on the topic Technological Factors:

- Health economics

- Science and technology studies and economic sociology

- THE INNOVATION-CO-EVOLUTION-COMPLEXITY PERSPECTIVE

- THE BASIC ELEMENTS OF ICTS

- The new economy

- Other Variables that play a Role as Risk Factors

- This chapter explores the constitution of the knowledge-based economy as an increasingly hegemonic meta-object of governance (and, indeed, meta-governance) in response to the crisis of Atlantic Fordism.1

- Growth and development

- Introduction

- AT&T: THE UNIFIED TELEPHONE REGIME