Other Variables that play a Role as Risk Factors

To complete the valuation of the market portfolio, another set of variables is required to attain the goal. Interest rates yield curves, exchange rate, as well as some other stock indexes may have an impact in the bank’s portfolio.

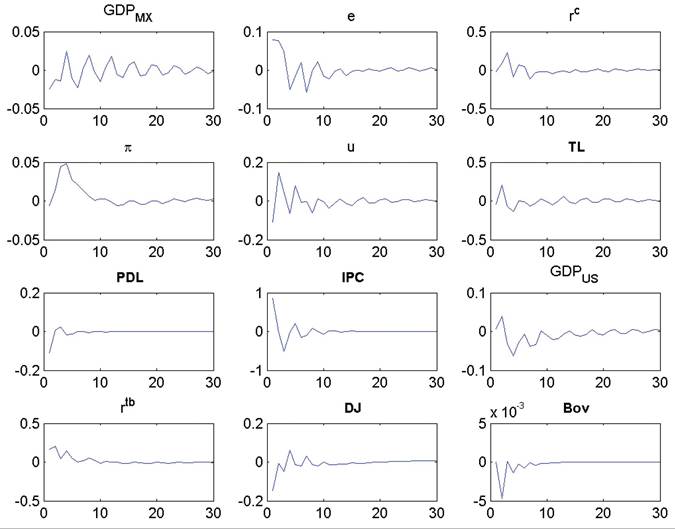

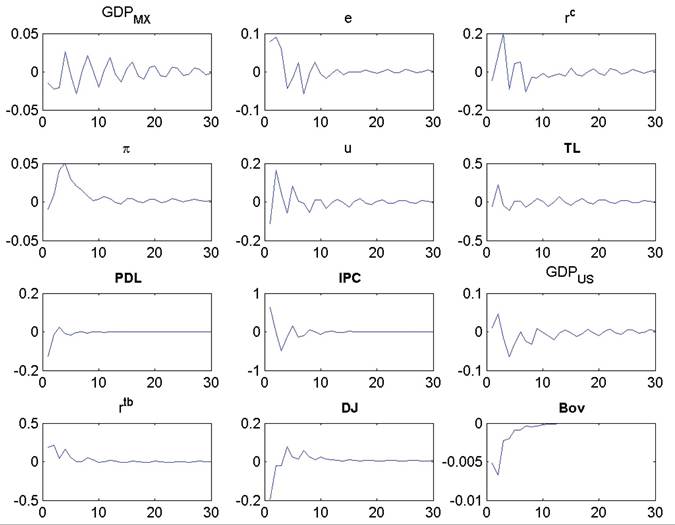

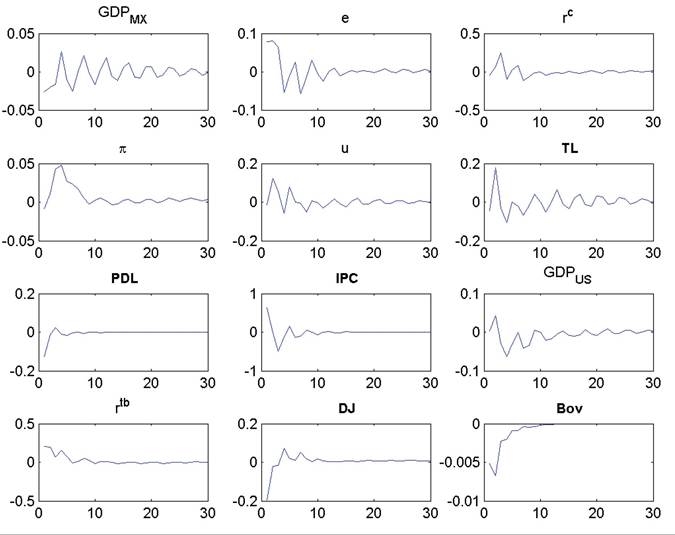

A more accurate modeling of these variables would require a much more complex framework and more detailed information, and that also would be beyond the scope of this work. Nevertheless, to model changes in these variables the spreads and stock indexes were modeled independently using autoregressive processes, and to get the interest rate curves for Cete, Tbill, and Libor, the variables used in the structural VAR were also used along with some nodes of the curve. Once these nodes were estimated, the curve was completed using a cubic Hermite polynomial.Figure 16. Impulse-response functions: change in Mexican GDP when other variables change by one standard deviation

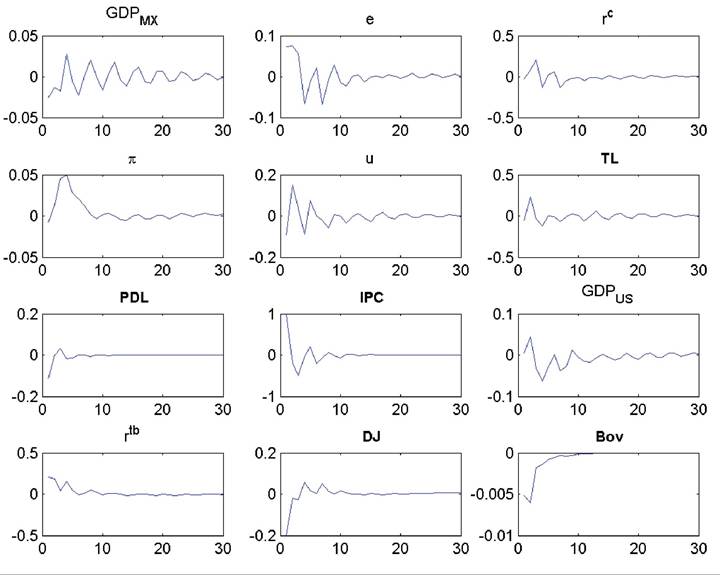

Figure 17. Change in real exchange rate when other variables change by one standard deviation

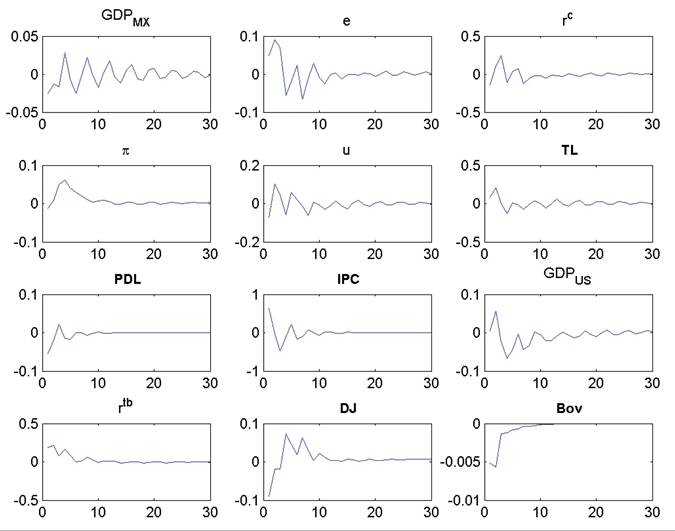

Figure 18. Impulse-response functions: Change in Cete interest rate when other variables change by one standard deviation

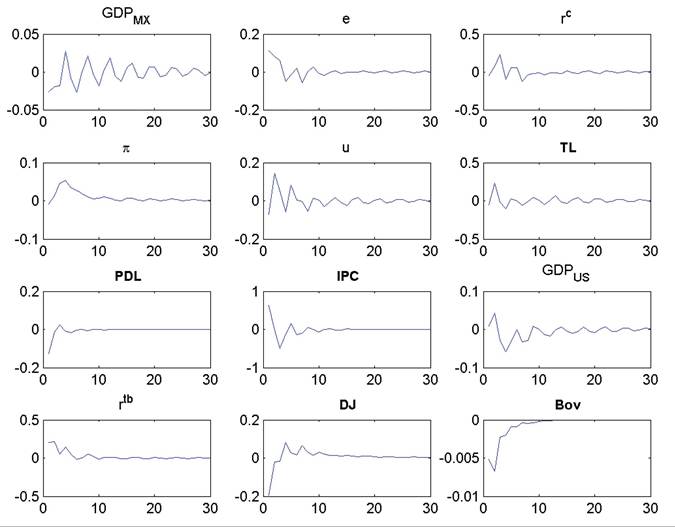

Figure 19. Impulse-response functions: Change in loans in good standing when other variables change by one standard deviation

Figure 20. Impulse-response functions: Change in past-due-loans when other variables change by one standard deviation

Figure 21.

Change in IPC stock index when other variables change by one standard deviation

3. Scenario Generation

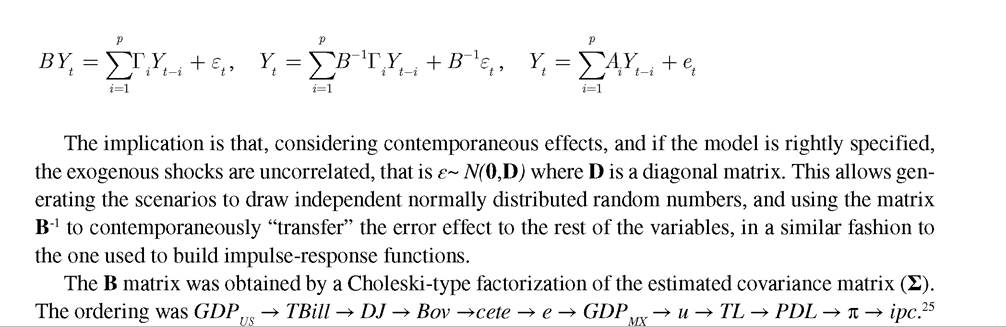

Once all the parameters were estimated, the generation of scenarios was done simulating random shocks and transferring the effects of the shocks using a Choleski-type decomposition of the covariance matrix estimated from the macro model.

Formally, the structural model is assumed to include a matrix of coefficients of contemporaneous effects:

Each realization of ε together with the estimated coefficients determines projected levels of the relevant variables in the model. To complete the scenario, the interest rate curves are also affected by the same shocks (for example, the TBill curve is affected by the same shock that affected the TBill in the VAR model) and the other variables are affected by autonomous shocks.

Credit deserves a lengthier discussion. It seems that a greater effort was exerted on the market side of the losses distribution, and to some extent, it is right. The fundamental problem is the disparity of the risk horizon for both portfolios. While for market a one month horizon seems too long, for credit one month is hardly enough for marginal changes. This is the trade-off facing all those studying the joint distribution: to sacrifice accuracy in market position and to analyze a longer term to get significant credit effects or to get more accurate market losses but accepting that credit losses will be low and any significant credit effect will materialize in a few more months. We opted for the second option, and to determine the effect of shocks in credit losses the estimator for the change in delinquency rate was used as a proxy for credit losses weighted by current levels of delinquency rates by bank.

More on the topic Other Variables that play a Role as Risk Factors:

- THE PORTFOLIO CONCEPT

- THE ROLE OF ITSG IN E-BANKING

- Appendix B: Variables in cross-country growth regressions

- Money Growth and Inflation

- TECHNICAL FACTORS OF NEEDLE ELECTROMYOGRAPHY

- Reviewers

- REVIEW OF FORENSIC ASSESSMENT INSTRUMENTS

- CHAPTER 38 ASPERGILLOSIS

- Peripheral Vascular Disease

- HEARING DISORDERS