WHAT IS REVENUE?

Suppose, for example, that an entrepreneur launches a restaurant franchising business. The fictitious Salsa Meister International does not operate any Salsa Meister restaurants.

It merely sells franchises to other entrepreneurs and collects franchise fees.The franchised restaurants, sad to say, consistently lose money. That fact has no bearing on Salsa Meister International’s accounting profit, however. The restaurants’ operations are not part of Salsa Meister International, their revenues are not its revenues, and their costs are not its costs. Salsa Meister International’s income consists entirely of franchise fees, which it earns by rendering the franchisees such services as developing menus, providing accounting systems, training restaurant employees, and creating advertising campaigns.

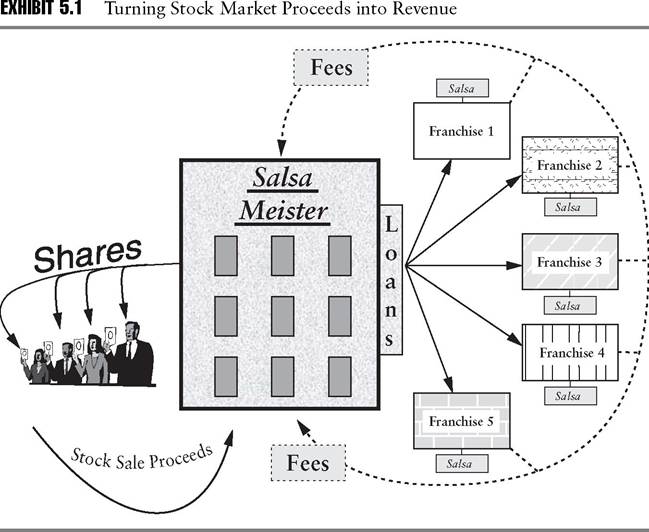

An astute analyst will ask how money-losing franchisees come up with cash to pay fees. The diagram in Exhibit 5.1 answers this riddle. Salsa Meister International sells stock to the public, then lends the proceeds to the

franchisees. The franchisees send the cash right back to Salsa Meister International under the rubric of fees. Salsa Meister International gratefully accepts the fees, which exceed the modest costs of running a corporate headquarters, and renames them revenue.

According to generally accepted accounting principles, Salsa Meister International has earned a profit. Investors apply a price-earnings multiple to the accounting profit. On the strength of that valuation, the company goes forward with its next public stock offering. Once again, the proceeds finance the payment of fees by franchisees, whose numbers have meanwhile increased in connection with the Salsa Meister chain’s expansion into new regions.

Accounting profits rise and the cycle of relabeling stock market proceeds first as fees and finally as earnings starts all over again.The astute analyst is troubled, however. Cutting through the form of the transactions to the substance, it is clear that Salsa Meister International’s wealth has not increased. Cash has simply traveled from the shareholders to the company, to the franchisees, and then back to the company, undergoing a few name changes along the way.

Merely circulating funds does not increase wealth. If Jack hands Jill a dollar, which she promptly hands right back to him, neither party is better off after the “transaction” than before it. By definition, neither Jack nor Jill has earned a bona fide profit. Salsa Meister International has not earned a bona fide profit, either, regardless of what GAAP may say about accounting profits.

Sooner or later, investors will come to this realization. When that happens, the company will lose its ability to manufacture accounting profits by raising new funds in the stock market. Salsa Meister’s stock price will then fall to its intrinsic value—zero. Investors will suffer heavy losses that they could have avoided by asking whether the company’s reported profits truly reflected increases in wealth. Moreover, the investors will continue making similar mistakes unless they begin to understand that bona fide profits sometimes differ radically from accounting profits.

More on the topic WHAT IS REVENUE?:

- REVIEW QUESTIONS

- Conclusion

- Individual R&D Uncertainty and the Stock Market

- 7 The Keynesian Model of Income Determination in a Three Sector Economy: Introduction of the Government Sector

- Constantinople: The Imperial Capital

- Case Study

- Political Institutions and Growth-Enhancing Policies

- Future Directions and Conclusions About CMS and Organizing

- Ricardian Equivalence and the Ramsey Model

- Aggregate Capital Accumulation in a Ramsey Model with Money