Intergenerational mobility: evidence

Section 10.3 presented a set of measures by means of which we can describe not only intra- but also intergenerational associations in a society. This section reviews evidence on such associations.

There are several earlier reviews of intergenerational income mobility. Solon (1999) reviewed intergenerational labor market with a focus on long-run earnings, whereas Solon (2002) focused on a subset of that literature, namely cross-national differences in mobility. Bjorklund andjantti (2009) built on and extended the empirical evidence assembled by Solon (1999). Black and Devereux (2011), who examined intergenerational links in income and education, emphasized evidence on causal links in intergenerational mobility. Blanden (2013) contrasted the crossnational evidence on intergenerational income, earnings, and education mobility with mobility in social class. Corak (2006, 2013a), in turn, emphasized policy implications. Corak (2013a) also drew on recent research about both socioeconomic gradients in child development and the emergence of economic persistence in labor markets.

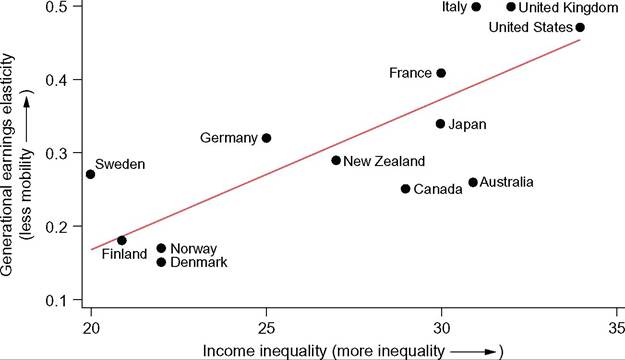

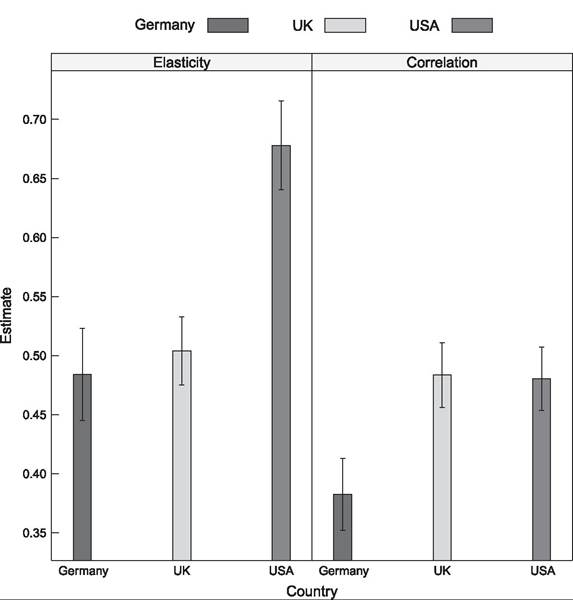

Several recent reviews present international evidence on intergenerational income persistence in a scatter plot, plotting the estimated persistence in different countries on the vertical axis and estimated income inequality, often in the parental generation, on the horizontal, adding a linear bivariate regression line (Bjorklund and jantti, 2009; Blanden, 2013; Corak, 2013a). Labeled the “Great Gatsby” curve by the then-chairman of the U.S. Council of Economic Advisors (Krueger, 2012), such plots are interpreted to suggest countries with higher persistence are also countries with greater inequality. Figure 10.13 reproduces the most recent such graph, from Corak (2013a, Figure 1). Although the precise estimates used by different authors vary, the results are broadly similar.

The Nordic countries have low persistence and low inequality; the United States, the UK along with France and Italy, have high persistence and reasonably high inequality.There are theoretical models that can account for the positive association between inequality and persistence. For instance, in Solon’s (2004) version of the Becker and Tomes (1979, 1986) model, the factors that drive intergenerational persistence, such as the heritability of human capital endowments, the returns to education, and the progressivity of public education expenditure, affect cross-sectional inequality with the same signs. In Hassler et al.’s (2007) model, which examines links between inequality and mobility under different kinds of labor market institutions, some institutional arrangements have mobility and inequality being inversely related (and hence persistence and inequality positively correlated). Checchi et al.’s (1999) model of beliefs about own ability, educational choice and mobility can also generate positive as well as negative associations between inequality and mobility depending on the model parameters. As we shall see, however, it is far from clear that intergenerational persistence and inequality are, in fact, as clearly positively correlated as Figure 10.13 suggests.

Figure 10.13 The Great Gatsby curve: the relationship between intergenerational earnings persistence and cross-sectional income inequality. Note: Income inequality is measured by the Gini coefficient of disposable household income in 1985 taken from the OECD. Persistence is measured as the Beta of parental and son earnings. Sons are born in early 1960s, and outcomes for them are measured in late 1990s. See Corak (2013a,b) for further detail. Source: Corak (2013a, Figure 1).

This part of the chapter proceeds as follows. In Section 10.5.1, we discuss data requirements and special problems that come up in estimating intergenerational and family associations.

In Section 10.5.2, we review studies of intergenerational persistence and mobility in the United States. The focus on this country is motivated, as in the intragen- erational mobility case, by the sheer amount of evidence about mobility in the United States relative to that in other countries. First, we examine evidence on the level of the intergenerational elasticity (IGE) of earnings or income—first for father-son pairs, and then widen the scope to look at broader pairings of parents and offspring—and then examine evidence about trends in the IGE over time. (The IGE is the Beta measure discussed in Section 10.3; we use both terms interchangeably in this section.) We then examine evidence that is based on measures that go beyond the simple log-linear Galtonian regression Beta (IGE), product-moment correlation coefficient r: for example, quantile regressions, transition matrices, nonparametric conditional mean functions. In Section 10.5.3, we examine evidence on intergenerational mobility from other countries, following the same structure as for the United States. In Section 10.5.4, we examine evidence on another way to measure the importance of family background, the sibling correlation; and in Section 10.5.5, we discuss other approaches to intergenerational mobility, old and new. Section 10.5.6 concludes.10.5.1 Data and Issues of Empirical Implementation

As discussed in Section 10.4.1, any study of income mobility faces three “W” issues: mobility of What, among Whom, and When? For intergenerational mobility, each question must be answered twice, once in each of the parental and offspring generations. As with intragenerational mobility, researchers’ choices are constrained with the available data.

At one level, just as with intragenerational income mobility, mobility of “What” refers to the income concept that is used. The overwhelming majority of studies we review use the labor market earnings of the parent and the offspring with several variations, discussed in Section 10.4.1.

Other choices might add nonlabor income sources from the market such as capital income to measure factor or market income. If the goal is to examine the intergenerational association ofliving standards, it would make sense to study disposable income (i.e., to add public transfers and deduct income taxes paid). It would seem reasonable to have identical answers to the “What” question in both generations. It is frequently the case that available data do not support such a choice; it is not unusual for “income” to be family income in the parental generation and to be earnings in the offspring generation.[628]The aim of early research on this topic was to measure the intergenerational association of “permanent” income, which was believed to be captured quite well by labor market earnings. It has long been recognized (see Atkinson, 1981b) that short-run income measures are different from longer-run measures because of transitory fluctuations, and that the associations sought were those of the more stable or permanent measures ofliving standards.

As with intragenerational mobility, “Whom” refers to the definition of the incomereceiving unit in both the parent and child generation. Most studies that are modeled on Solon (1992) examine mobility of father-son pairs, ignoring the incomes of other household members. Many departures from this are due to data-related reasons. For instance, studies such as that of Zimmerman (1992), which relies on data from the U.S. National Longitudinal Survey of Youth (NLSY), uses family income in the parental generation, as that is the only income concept available in that data source.[629]

The Whom question becomes more complex when the intergenerational associations of women’s incomes are studied and compared with those of men. Over the last four to five decades, women’s labor market attachment has increased substantially in most developed nations, with female labor force participation rates increasingly resembling those of men.

However, around the age commonly believed to be appropriate for measuring men’s long-run income (around age 40), women often have breaks from employment due to childbirth and child care. Studies that examine women’s intergenerational mobility are more likely to examine family or household income as a better gauge of their living standard than individual incomes. Comparing mobility across men and women would then naturally also need to examine family or household income for men (Chadwick and Solon, 2002; Raaum et al., 2007).There is an added dimension to the Whom question, namely the nature of the parentoffspring relationship. In the early intergenerational studies of Atkinson (1981b), Solon (1992), and Zimmerman (1992), the parent-child association was more or less driven by the survey design—“children” were the children of the sample parents who were followed up in adulthood. However, children can have multiple parents—stepparents, adoptive and foster parents in addition to birth parents. Common choices are to restrict the population to those parent-offspring pairs where the offspring was observed as living with the parent at some age, say 10 or 16, or to birth parents. One aspect of this Whom dimension is the role of separated families. Should one focus on associations of offspring income with the head in lone-parent families or on father-child associations? Some studies, especially based on register data, have examined the sensitivity of the population of parent-child relationships and found differences across definitions and family types to be relatively small.[630]

As with the two other “W” questions, the When question for intergenerational mobility analysis is mostly a superset of that for intragenerational mobility. Most of the same questions addressed in Section 10.4.1 need to be resolved for both the parent and offspring generations. The underlying data record income for a specific period: often annual income data but in some cases “current” income data are available.

But, in contrast to the case ofintra- generational mobility, shorter-run fluctuations are noise that make more difficult the uncovering of the more interesting underlying longer-run incomes. This leads directly to the issue of over what periods, and over what ages, incomes should be studied (and aggregated) to give reasonable measurements of longer-run economic status. And if, due to data limitations, ideal measurements cannot be made, how are mobility measurements affected? The two main issues that have been addressed are transitory variation in observed income measures, and “life cycle” bias (Jenkins, 1987; Grawe, 2006). We discuss these in turn.Since at least Atkinson (1981b), it has been recognized that transitory errors in parental income lead to an errors-in-variables (downward) inconsistency in the estimated intergenerational elasticity. Since the seminal paper to empirically address this issue (Solon, 1992), many studies have exploited this finding.[631] Solon’s estimate of intergenerational persistence for the United States, based on averages across 5 years of parental income, resulted in point estimates of Beta that are between 10% and 70% larger than the estimates derived using a single year of parental income.

Recent work on so-called generalized-errors-in-variables (GEIV) model calls into question the assumption that transitory income variations have the same properties as classical measurement errors (Bohlmark and Lindquist, 2006; Haider and Solon, 2006). The GEIV model for the annual income process of an individual in family i in generation j (=Offspring, Parent) at age t relates permanent income y and transitory errors v to annual or current income by (Haider and Solon, 2006)